PRESENTATION TO SCOPA Reasons for the Delay in

(d) and 55(1)(d) of the Public Finance Management Act (PFMA),")

• RSA does not buy water from Lesotho • Lesotho")

Cost related payments (CRP’s) (Article 10 of the Treaty) •")

• TCTA Notice of Establishment (NOE) of")

Phase II Agreement of 2011 – Article")

")

683 1200 Website: http: //www.")

- Slides: 22

PRESENTATION TO SCOPA Reasons for the Delay in the Submission of TCTA’s Annual Report to Parliament 13 November 2019 1

LEGISLATIVE REQUIREMENTS • Sections 40(1)(d) and 55(1)(d) of the Public Finance Management Act (PFMA), 1999 (Act No. 1 of 1999) (PFMA), require the accounting officer of a department, trading entity and constitutional institution to - submit the annual report on the department’s past year activities, the financial statements for that financial year and the Auditor. General’s report on those statements to the National Treasury and to the Minister (as the responsible executive authority for the Department) within five months of the end of the financial year, which in effect means 31 August 2019. • Section 65(1)(a) of the PFMA, require the executive authority responsible for a department or public entity to table in the National Assembly the annual report and financial statements and the audit report on those statements, within one month after the accounting authority for the public entity received the audit report. • However, in terms of section 65(2)(a), if an executive authority fails to table the annual report and annual financial statements of the department or the public entity and the audit report on those statements in the relevant legislature within six (6) months (i. e. by 30 September 2019), a written explanation to the legislature must be submitted explaining the reasons for its inability to do so. 2

Problem Statement Significant differences of interpretation between the Auditor-General of South Africa and TCTA over the nature of the supporting documentation required to substantiate payments made by TCTA, on behalf of the Government of South Africa, to the Lesotho Highlands Development Authority and Lesotho Highlands Water Commission The difference in interpretation led to an initial “limitation of scope finding” that would have resulted in a qualified audit opinion. 3

Background: Integrated Vaal River System

The Choice South Africa had to Make • The Lesotho Highlands Water Project forms part of the Integrated Vaal River System. • To take the water from the Orange River in the vicinity of Gariep Dam and pump it to the Vaal River; or • Work with the Government of Lesotho to have the necessary infrastructure built in Lesotho and transferring the water by gravity into the Vaal River system. 5

LHWP PHASE II Transfer Tunnel 38. 2 km long 5. 2 m diameter Polihali Dam 163. 5 m high rockfill dam 49. 5 m Saddle dam

LHWP: PROJECT GOVERNANCE MODEL Minister of Water and Sanitation Republic of South Africa Designated Authority Minister of Water and Natural Resources Kingdom of Lesotho PS/DG Meeting Government of Lesotho Delegation Republic of South Africa Delegation Lesotho Highlands Water Commission - LHWC Approvals - Operations and Expenditures Monitoring - Project Performance and Risks Advise Principals - Strategic Intervention Reporting – Project Activities, Targets & Impacts Trans Caledon Tunnel Authority TCTA Chief Executive Officer q General Project Finance Mobilisation q Develop Project Funding Strategy q Present Funding Strategy to the LHWC q Operational Support: RSA Delegation Lesotho Highlands Development Authority - LHDA Chief Executive v 2. 2 billion cubic/meter Polihali Dam v 38 km long Polihadi/Katse Channel v Advance Infrastructure (access, feeder roads, power Communications, Bridges etc) v Socio-economic Measures v Environmental Mitigation Measures

GOVERNANCE ARRANGEMENTS • LHDA, a Lesotho parastatal, is responsible for the implementation of the LHWP located within Lesotho in terms of the Treaty between RSA and KOL signed in 1986. The Treaty provides that LHDA must account for all costs incurred on the LHWP Including the allocation of such costs to either RSA or KOL. • The LHWC, a bi-national Commission, is accountable to the two Governments for the successful implementation of the LHWP and has approval, monitoring and advisory powers over the project implementation activities of the LHDA and TCTA. The LHWC comprises of an RSA and GOL Delegation and reports to the respective Governments. The RSA Delegation reports to the DWS. The LHWC is the only body that has oversight over the LHDA’s project implementation activities within Lesotho and is responsible to protect the respective Governments interest on the project. The LHWC functions on a consensus basis, all decisions by the LHWC requires the consent of both Delegations to take effect. Effectively, this means no single Government can instruct the LHDA. • TCTA has therefore no direct access to the records of the LHDA or any direct oversight over the activities of the LHDA. 8

RSA Financial Obligations (1) • RSA does not buy water from Lesotho • Lesotho provides the infrastructure to deliver water to the border • South Africa pays: • LHDA for the costs incurred on the implementation and operation & maintenance of the Water Transfer (WT) portion of the LHWP in Lesotho • Monthly Royalty payments to GOL – Lesotho share of net benefit • Operating costs of the LHWC (RSA Delegation portion) • Payments are in terms of the 1986 Treaty and 2011 Phase II Agreement 9

RSA Financial Obligations (2) Cost related payments (CRP’s) (Article 10 of the Treaty) • RSA responsible for costs wholly and reasonably incurred on the implementation and O&M of WT part of the LHWP • CRP’s has taken the form of: • Payments by RSA to LHDA for costs incurred (Since 2005) • Repayment of loans raised by LHDA (Phase 1) • Method and timing Art 10(5) • Based on LHDA short-term cash flows 10

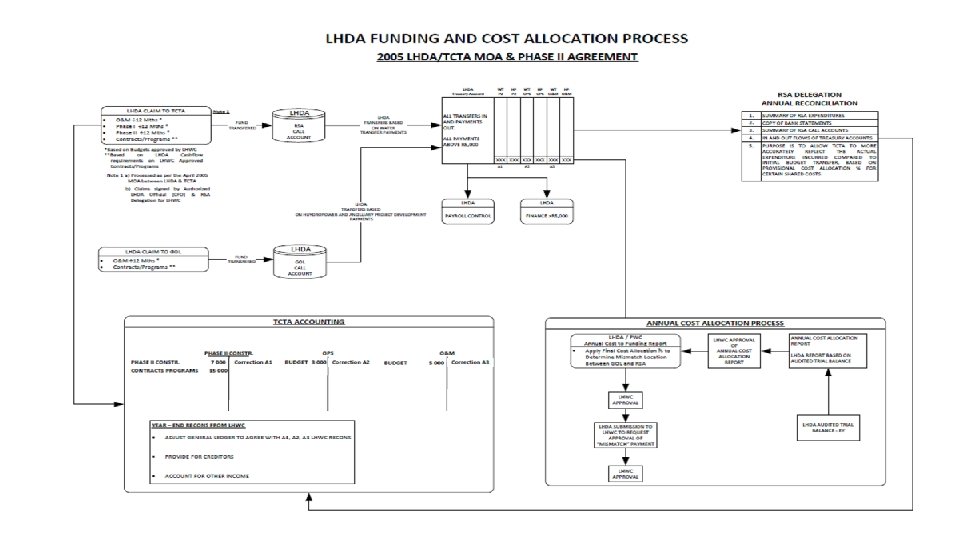

TCTA NON- TREATY FUNCTION ON LHWP (1) • TCTA Notice of Establishment (NOE) of 2000 (Section 24 (a) • To fulfil all RSA financial obligations “ in terms of or resulting from the Treaty, including: ” • The raising of money, and • Liability and financial risk management • TCTA Funding of LHDA Cost Related Payments • • TCTA/LHDA Memorandum of Agreement (MOA) of 2005 approved by LHWC Operating framework for payments to LHDA Monthly/weekly claims prepared by LHDA’s duly authorised CFO LHDA submits to RSA Delegation who certify before payment by TCTA • For Phase I – LHDA raised funding on RSA Government guarantee – TCTA repaid loans • KEY Objective of MOA – centralise funding within TCTA to limit RSA contingent liability for provision of guarantees. 11

TCTA NON- TREATY FUNCTION ON LHWP (2) Phase II Agreement of 2011 – Article 13 Funding Arrangements • TCTA responsible to raise funding within the RSA financial markets for Phase II • The TCTA/LHDA MOA of 2005 shall continue to apply • Limit treasury function i. e. only within TCTA • TCTA primary role for Phase II is to raise cost effective funding for the Water Transfer portion of Phase II 12

• Governance Structure – LHWC Treaty Safeguards • All expenditure (Budgets, Contracts, Loans) subject to LHWC approval to take effect • Cost Related Payments Article 10 – only cost wholly and reasonably incurred • Phase II Agreement: • Annual cost allocation report – LHWC approval • Annual cost to funding report – LHWC approval • Cost to funding report – subject to independent review (PWC) • LHDA subject to independent external audit – 100% clean audits 13

Understanding of Funding Arrangements 14

Accounting Treatment • The LHWP accounting treatment is almost unique in comparison with other accounting treatments in another countries • Such uniqueness does not lend itself to standardised accounting treatments • Since 2012, TCTA deemed IAS 11 as the most relevant accounting standard, and has accounted for the cost-related payments as a construction expense with the documentation provided by LHWC as sufficient evidence on which to make payment • However TCTA has recognised that the applied accounting policy i. e. expensing the LHDA costs, does not reflect the true nature of the transactions between TCTA and the LHDA and needs to be revised. The AGSA was not comfortable with this change. 15

STEPS TAKEN TO RESOLVE THE ISSUES • A meeting was held between LHDA, TCTA, AGSA and the department on the 02 and 18 September 2019 to resolve the issue of accessing the information in the possession of the LHDA. • The AGSA engaged with the external auditors of the LHDA following an introductory meeting held in Maseru on the 2 nd September 2019. • The AGSA reviewed the working papers of the LHDA external auditors and advised in a letter to TCTA dated 26 th September 2019 that the preliminary scope limitation findings have been resolved. • TCTA CEO met with the AGSA on 30 September 2019 to engage on the outstanding audit findings and agree a way forward to conclude the audit for 31 March 2019 financial year. • The adjusted AFS was submitted on the 21 st October 2019 still reflects these costs as expenses in the SCI with further adjustments made for accruals and prepayments made by the LHDA based on information obtained from the LHDA. • The AGSA indicated that substantial further audit work is required, and they will only be able to commence work on 15 th November 2019 due to prior allocation of resources to other on-going audits. • The additional audit work may take 3 to 4 weeks to conclude. Discussions are on-going with AGSA to explore a possible earlier start. 16

Expected Timelines for completion Audit • TCTA submitted adjusted AFS on 21 October 2019 • AGSA indicated commencement date 15 November 2019 • Planned audit period 3 to 4 weeks • Planned release of AFS before 31 December 2019 17

Consequence on WTE This delay therefore affected the Water Trading’s ability to adjust its financial statements as they are based on the TCTA financial models, hence, the Water Trading’s inability to submit the adjusted financial statement to the AGSA. Because WTE is part of the department’s annual report the department was therefore unable to table its annual report. 18

Implications on TCTA Borrowings • TCTA’s total outstanding borrowings amounts to approximately R 22 billion • Should an event of default occur loans may become immediately due and payable • Late submission or a qualified audit opinion could be viewed as an event of default • This may lead to TCTA been delisted from JSE • TCTA is actively managing this potential by keeping lenders informed on any delays and status of the audit 19

Way Forward A workshop will be held by TCTA with the Department of Water and Sanitation and other relevant parties to review the control environment and the appropriate accounting treatment 20

2 1 Thank you Questions …. TCTA Telephone: (012) 683 1200 Website: http: //www. tcta. co. za