PPT ON ACCOUNTING FOR HIRE PURCHASE AND INSTALMENT

- Slides: 38

PPT ON ACCOUNTING FOR HIRE PURCHASE AND INSTALMENT PURCHASE SYSTEM MADE BY: SURBHI-34 BHAVYA-108 AKANKSHA-138

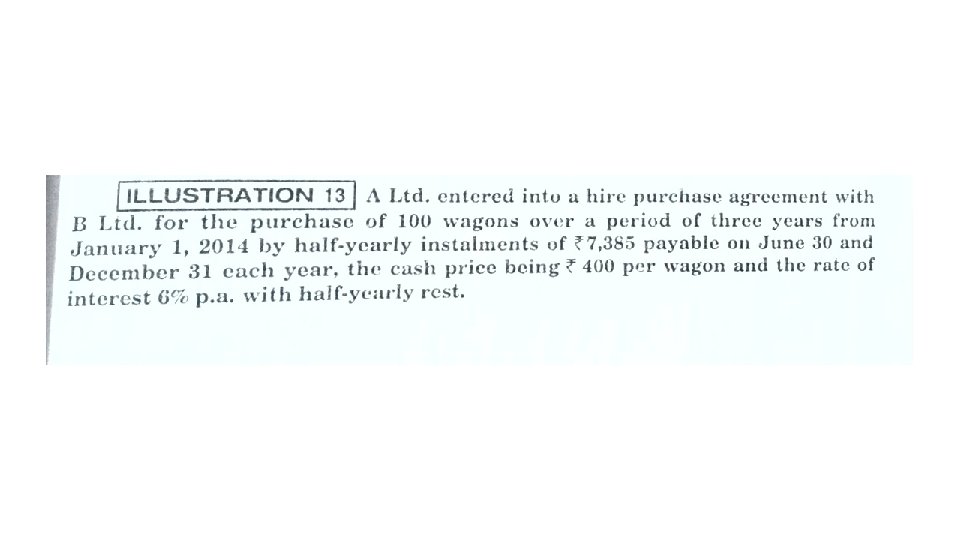

WHAT IS HIRE PURCHASE SYSTEM ? Under hire purchase system, the buyer acquires the possession of the goods immediately and agrees to pay the total hire purchase price in instalments, each instalment is treated as a hire charge until the payment of the last installment when ownership of the goods passes from the seller to the buyer.

FEATURES OF HIRE PURCHASE SYSTEM 1. Agreement between the seller and the buyer. 2. Possession immediately passes on signing agreement 3. Buyer makes payment in instalments over a period. 4. Ownership remains with seller until last installment. 5. Buyer has option to return goods and terminate deal. 6. Seller can repossess goods on default payment if any.

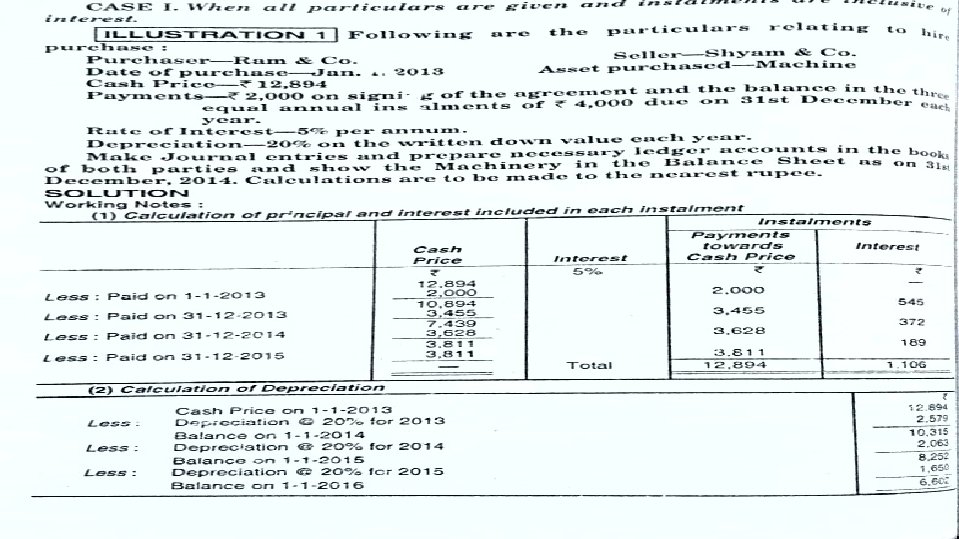

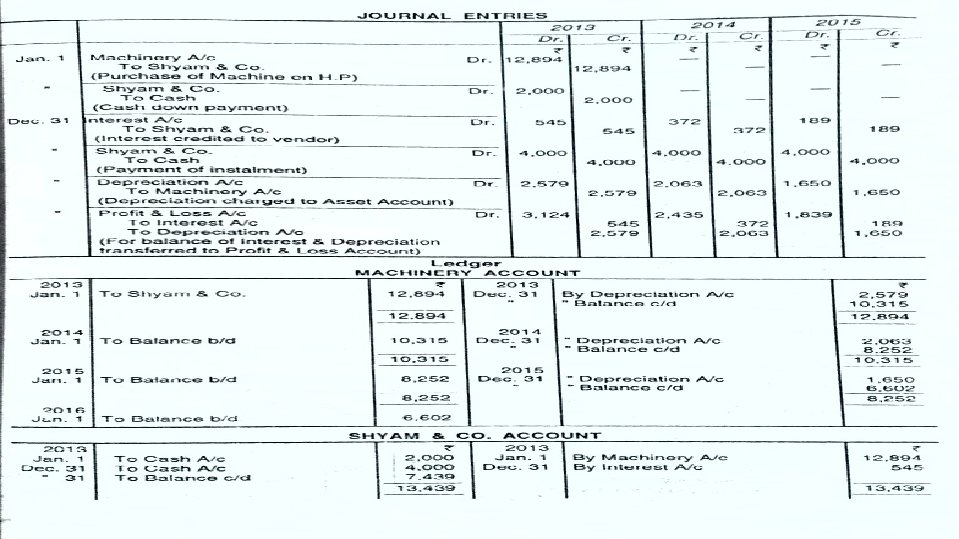

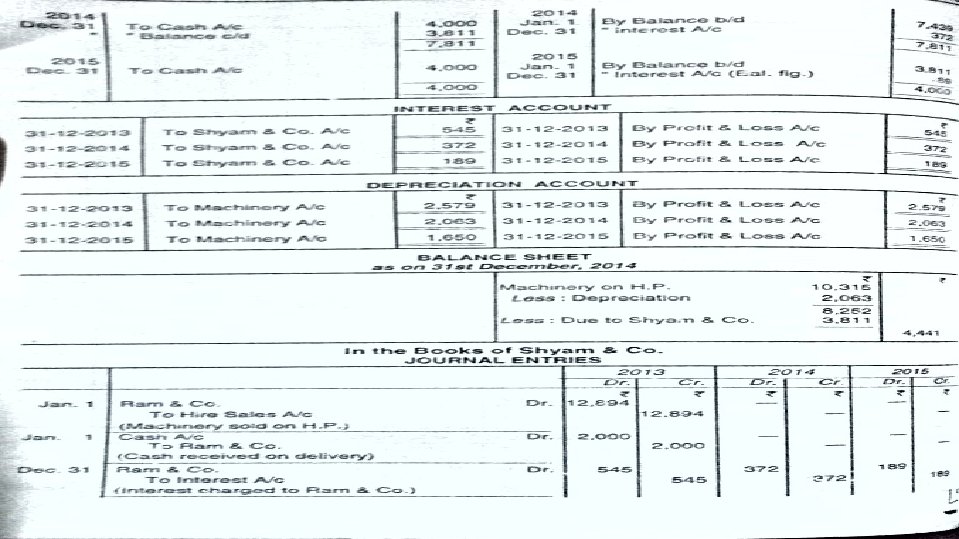

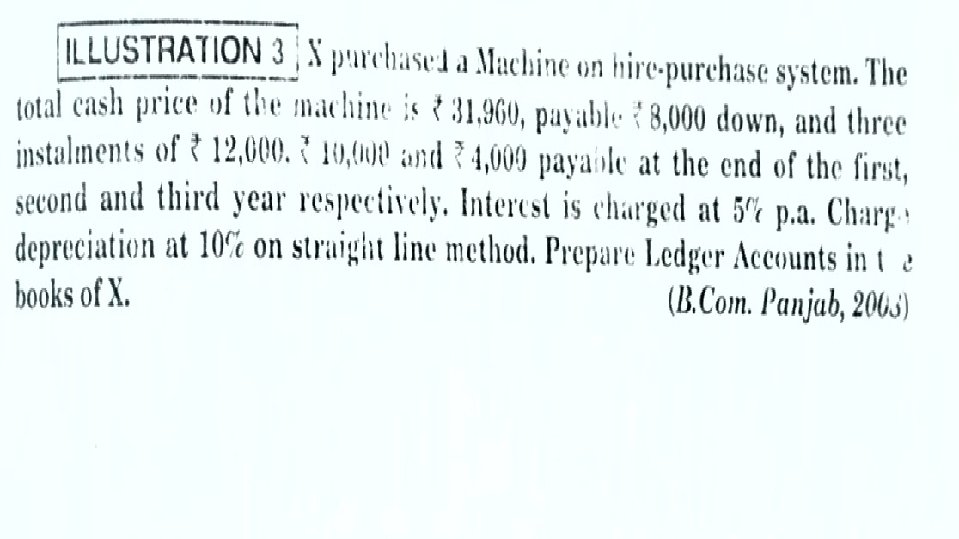

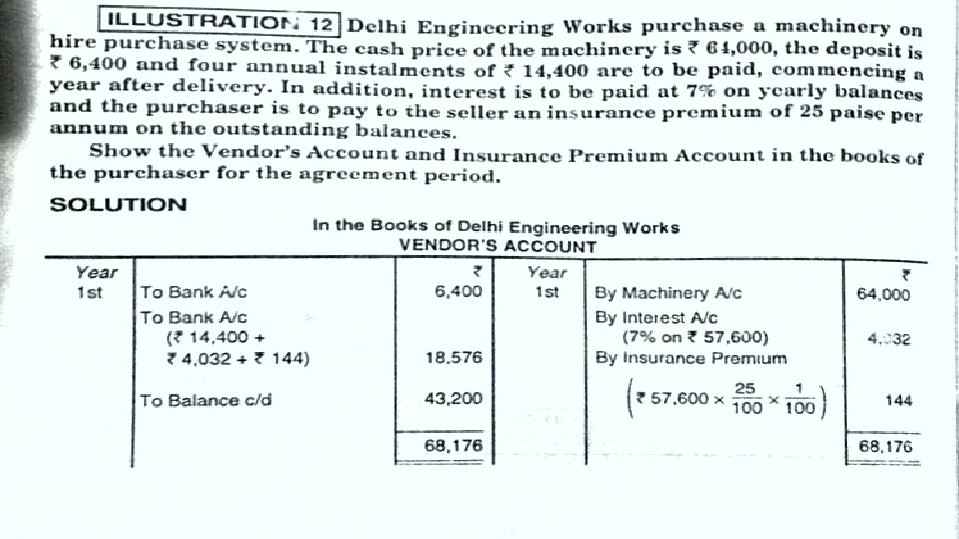

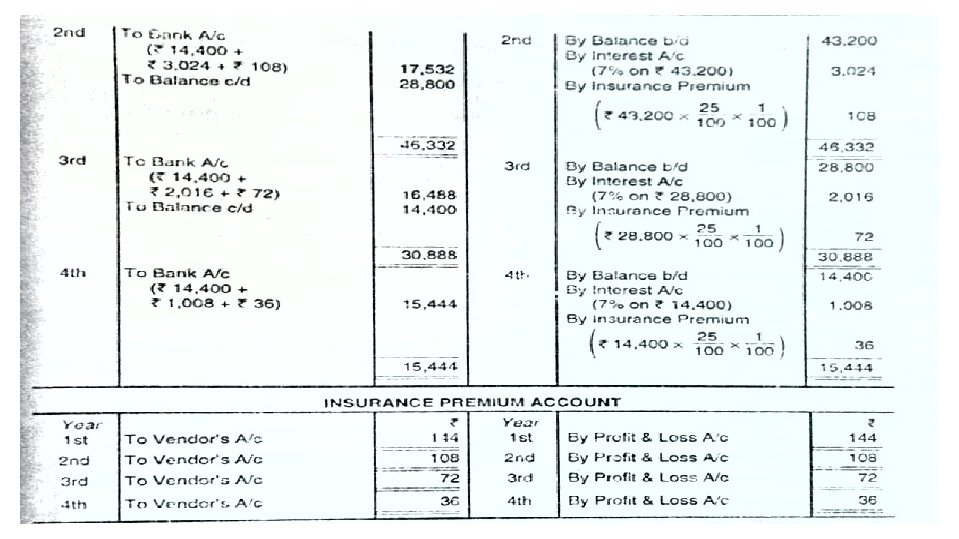

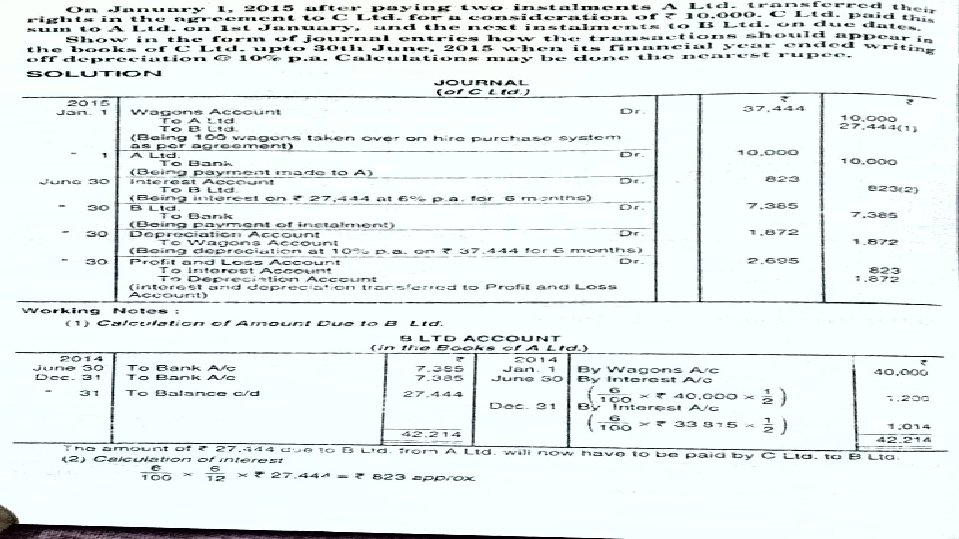

ACCOUNTING ENTRIES IN BOOKS OF BUYER • Asset Account. Dr. To hire vendor account • Hire vendor account. Dr. To cash/bank • Interest account. Dr. To hire vendor account • Hire vendor account. To bank Dr. • Depreciation account. Dr. To asset account • Profit and loss account. Dr. To interest account To depreciation account

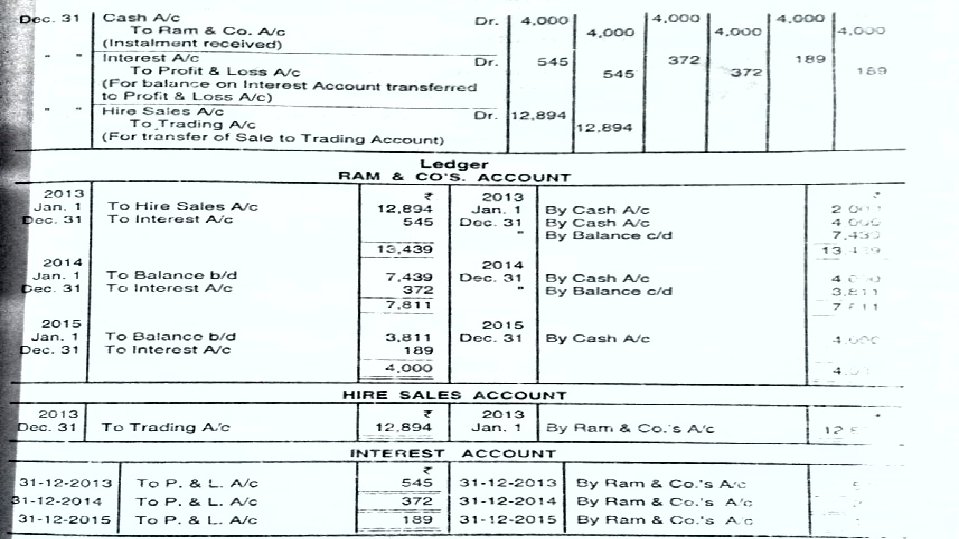

ENTRIES IN BOOK OF VENDOR’S • Hire purchaser’s account. Dr. To hire sales account • Cash/ bank account. Dr. To hire purchaser account • Hire purchaser’s account. Dr. To interest account ACCOUNT • Cash/Bank account. Dr. To hire purchasers a/c • Interest account. Dr. To profit and loss a/c

PURCHASE THROUGH FINANCIAL INSTITUTION When an asset is purchased on hire purchase, the purchaser sometimes gets it finance through some financial institutions. In such a case, the instalments are paid to financial institutions instead of vendor and right on the property will be that of financial institutions. In such a case account of financial institution will be opened in books of purchaser but other accounts will be same.

TRANSFER OF ASSET BY THE HIRE PURCHASER Sometimes the hire purchaser, with consent of the vendor, transfers the asset to some other person after paying someone instalments during the period of hire purchase agreement. Entries in books of transferee are: Asset account. Dr. To transferor’s account To vendor’s account

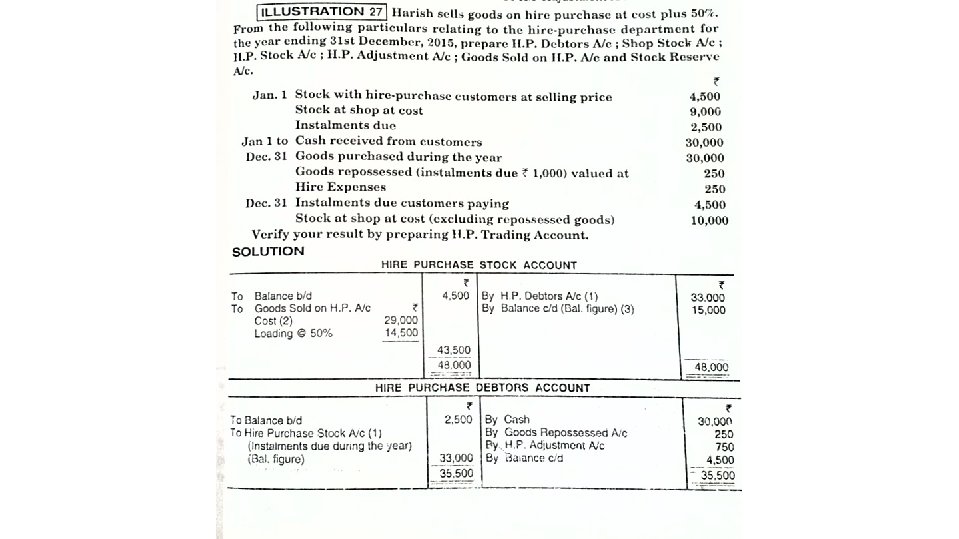

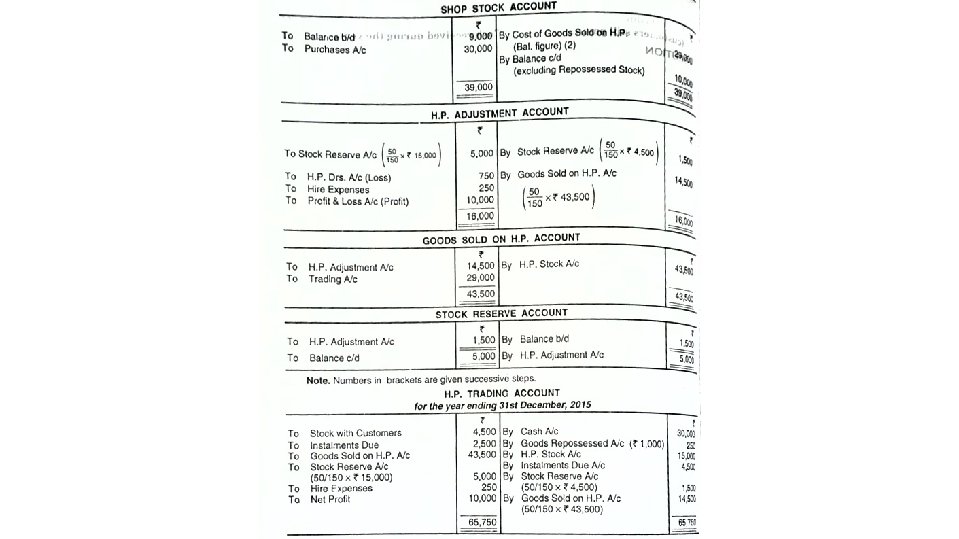

STOCK AND DEBTORS METHOD THIS IS AN ALTERNATIVE METHOD OF CALCULATING PROFIT OR LOSS OF THOSE TRADERS WHO SELL A NUMBER OF GOODS OF COMPARATIVELY SMALL VALUE DAILY ON THE HIRE PURCHASE SYSTEM.

JOURNAL ENTRIES • Shop stock a/c. Dr. To purchased a/c • Hire Purchase stock a/c. Dr. To goods sold on H. P. a/c • Hire purchase debtors a/c. To hire purchase stock a/c Dr.

WHEN GOODS ARE REPOSSESSED ON DEFAULT AND LOSS IS TRANSFERRED TO HIRE PURCHASE ADJUSTMENT A/C • Goods repossessed a/c. H. P. Adjustment a/c. Dr. To Hire purchase debtors a/c To Hire purchase stock a/c To H. P. Adjustment a/c

• Goods sold on H. P. a/c. To H. P. Adjustment a/c Dr. To trading a/c • Hire purchase adjustment a/c. Dr. To stock reserve a/c • Stock reserve a/c. Dr. To Hire purchase adjustment a/c • A) if profit -: . H. P. Adjustment A/c. Dr. To profit & loss A/c. B) if loss-: . Profit & loss A/c Dr. To H. P. Adjust. A/c

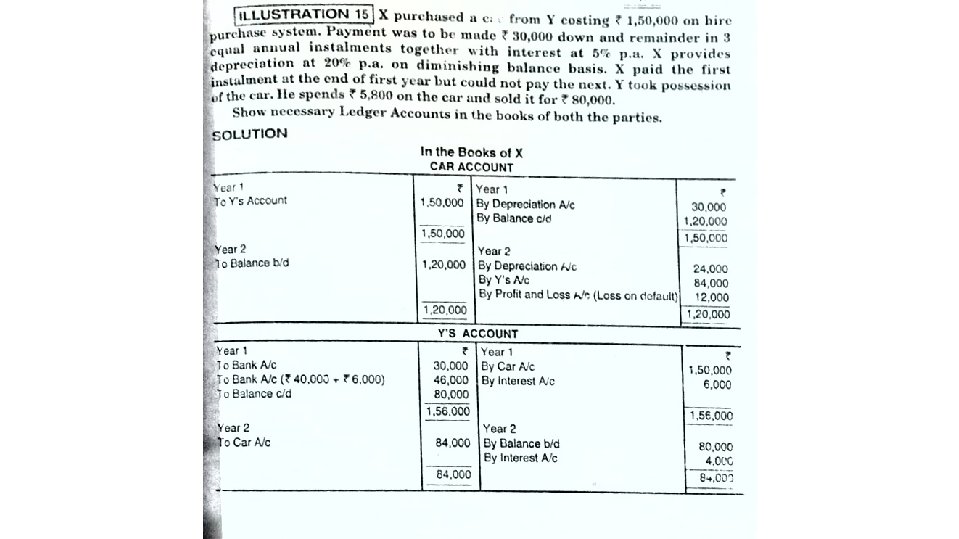

Default And epossession When the buyer makes default in the payment of any instalment, the vendor has a right to repossess the goods sold on hire purchase and forfeit whatever amount he has already received treating it as a hire charge. There are two possibilities in repossession of goods � When the vendor takes back the complete repossession of the asset. � When the vendor takes repossession of only a part of total asset sold to the hire purchaser.

When the Vendor takes back the complete repossession of the asset Journal Entries in the books of hire purchaser 1. Entry for interest due in the year of default Interest A/c Dr. To Vendor’s A/c 2. For transferring credit balance in vendor’s account to asset account Vendor’s A/c Dr. To Asset A/c 3. For providing depreciation for current year in current period Depreciation A/c Dr. To Asset A/c 4. Loss on default is closed by transferring to Profit and Loss A/c Profit & Loss A/c Dr. To Asset A/c

Journal Entries in the Books of Vendor 1. Entry for interest due in the year of default Hire Purchaser’s A/c To Interest A/c Dr. 2. On Repossession of Goods Repossessed A/c Dr. To Hire Purchaser’s A/c 3. For expenses incurred on goods repossessed to make them fit for sale Goods Repossessed A/c To Cash/Bank A/c 4. For cash received from sale of repossessed goods Cash/Bank A/c Dr. To Goods Repossessed A/c

Journal Entries in the Books of Vendor 5. Profit or Loss on repossession and is transferred to Profit and Loss A/c �If Profit Dr. Goods Repossessed A/c To Profit & Loss A/c � If Loss Profit & Loss A/c To Goods Repossessed A/c Dr.

When the vendor takes repossession of only a part of total asset sold to the hire oth the hire purchaser and vendor will not close vendor’s account and hire purchaser account in their respective books but an entry will be passed with the agreed value of that asset which has been taken back by the vendor will generally agree to take back a part of asset only at enhanced rate of depreciation. The hire purchaser will calculate the value of the asset left with him by the vendor by providing normal rate of depreciation and will keep this amount as balance carried down in the asset account. The asset account balance will show profit or loss on default and will be transferred to the profit and loss account.

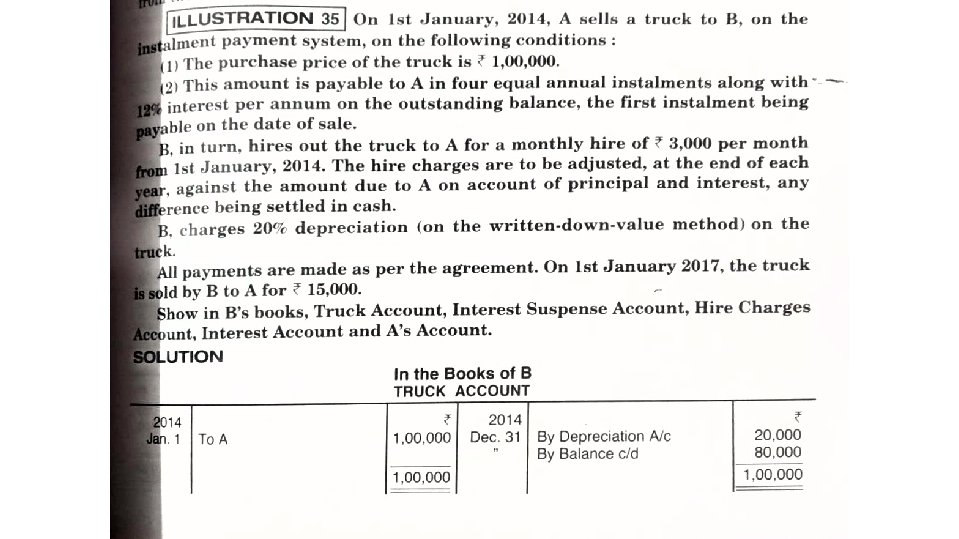

Instalment Purchase system Under instalment purchase system the possession as well as ownership passes from the seller to the buyer immediately on entering the agreement but the buyer agrees to pay the total price in instalment. If the buyer makes any default in the payment of any instalment, the seller has no right to repossession the goods. Main features of this system: 1. There is an agreement between the seller and the buyer. 2. The buyer is required to pay the total price in instalment. 3. The buyer get the possession and ownership of goods immediately after signing the agreement. 4. If there is any default in the payment of any instalment the seller has no right to repossess the goods.

Distinction between Hire purchase system & Instalment purchase system 1. Nature of contract : hire purchase is an agreement of hiring whereas instalment purchase system is an agreement of sale. 2. Ownership: under hire purchase system ownership remain with the seller until the payment of last instalment but under instalment purchase system ownership passes from buyer to seller immediately. 3. Right of disposal: under hire purchase system buyer cannot sell, destroy the goods but under instalment purchase system the buyer can do all this things. 4. Right under hire purchase system: under hire purchase system loss occur to good has to be borne by the hire vendor but in case of instalment purchase system any loss will have to be borne by the buyer. 5. Parties: under hire purchase system parties involved are called hirer and hire vendor where under instalment purchase system the parties involved are called buyer and seller.

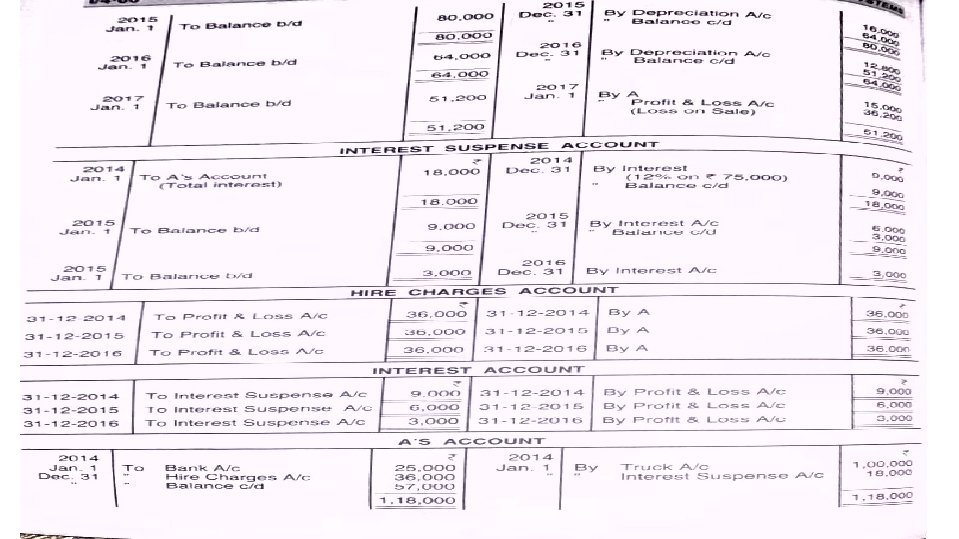

Accounting Entries In the Buyer’s book 1. When an asset is purchased on instalment purchase system Asset Account Dr. Interest Suspense A/c Dr. To Vendor’s A/c 2. For cash down payment on delivery Vendor’s A/c Dr. To Cash 3. For interest due at the end of the year Interest A/c Dr. To Interest suspense A/c

Accounting Entries 4. For the payment of first instalment Vendor’s A/c Dr. To bank A/c 5. For depreciation charge Depreciation A/c Dr. To Asset A/c 6. For transfer of interest and depreciation to Profit & Loss A/c Dr. To interest A/c To depreciation A/c

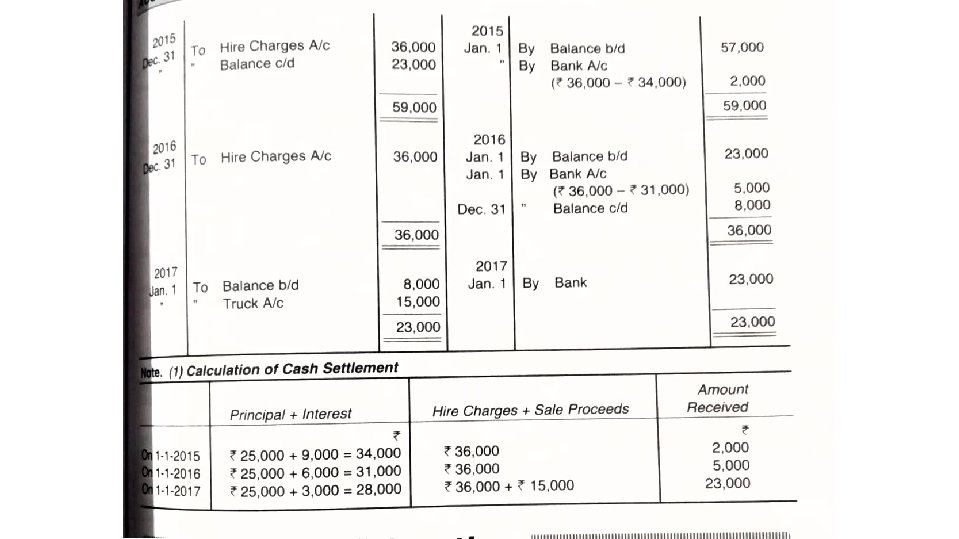

Accounting Entries • In Vendor’s Book 1. When goods are sold on instalment purchase system Purchaser A/c Dr. To sale A/c To interest suspense A/c 2. For cash received on delivery Bank A/c Dr. To purchaser A/c 3. For interest due on instalment at the end of the year Interest suspense A/c Dr. To Interest A/c

Entries Accounting 4. For receipt of amount of instalment Dr. Bank A/c To purchaser A/c 5. For transfer of interest to Profit & Loss A/c Interest A/c Dr. To Profit & Loss A/c