POSTING and GENERAL LEDGER General Ledger and Their

Office Equipment Date Description 2008 Aug 1 per Cash 2 per Cash")

Unearned Revenue Date Description Ref Debit (Rp) Credit (Rp) No : 23")

Date Bagus's Withdrawals Descriptio n 2008 Aug 30 Per Cash (in Rp)")

Date Salaries Expense Description 2008 Aug 15 per Cash 30 per Cash")

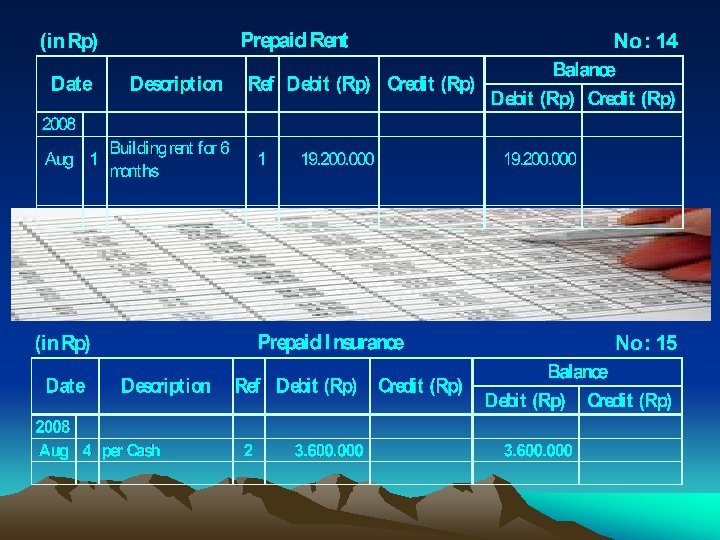

Date Description 2008 Aug 29 per Cash 3 260. 000")

- Slides: 29

POSTING and GENERAL LEDGER

General Ledger and Their Uses General ledger is a book containing each firm’s accounts Real Accounts Nominal Accounts

Real Accounts: § Cash Exam ples § Receivables § Supplies § Accounts Payable § Notes Payable Nominal Accounts o Salaries Expenses o Marketing Expenses o Depreciation Expense o Services Revenues o Interest Revenues

Types of General Ledger There are two types of accounts: o T – account form o Balance column account § There is a column for debit posting § A column to show the balance of the account if it’s a debit balance § A column to show te balance of the account if it happens to be a credit balance

Balance-column Account Form

POSTING v Posting is the transfer of accounting information from a journal to a ledger v This procedure is necessary in order to gather together the effects of business transactions on each type of asset, liability, and capital account. v At the end of a time period, summary totals of this account information can be compiled for use in the preparation of a trial balance and financial statement

Posting Illustrated D H Ledger A B C E G F

POSTING PROCESS A. B. C. D. E. F. G. H. Posting this journal entry with one debit and one credit involves the following Enter the date of the journal entry in the account to be debited (Cash account) Enter the amount of the debit in the debit column of the account to be debited (Cash account) Enter the cross reference in the ledger account to show that the debit was posted from the journal (Page 2) Enter the cross reference in the journal to show that the debit was posted to the appropriate account (Account 101) Enter the date of the journal entry in the account to be credited (Angga’s Capital account) Enter the amount in the credit column of the amount to be credited (Angga’s Capital account) Enter the cross reference in the ledger account to show that the credit was posted from the journal (page 6) Enter the cross reference in the journal to show that the credit was posted to the appropriate account (Account 300)

List of Accounts § A different company has different chart of accounts § The amount of accounts would depend on: a. The characteristic of an operating firm b. The activities volume c. The detailed information in the firm

S T N U O CC LIS A f To

Continuing. ……

Continuing ………

How each of the journal entries has been posted to the appropriate ledger accounts? The following is the list of accounts and their codes in Cipta Jasa Karya

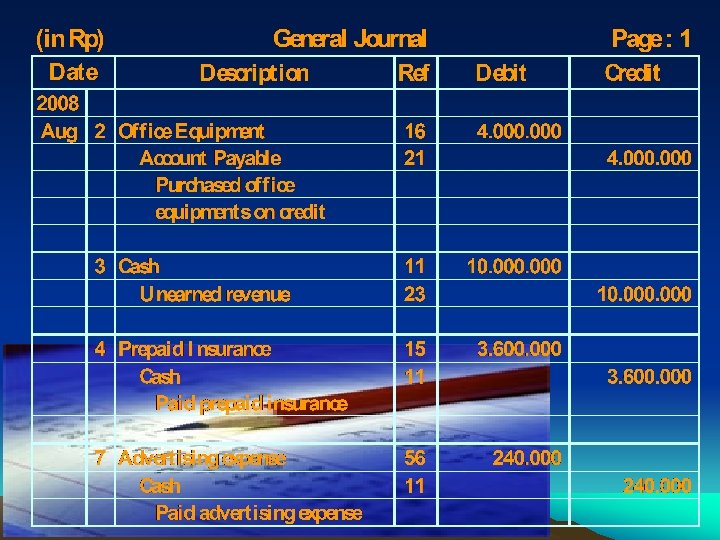

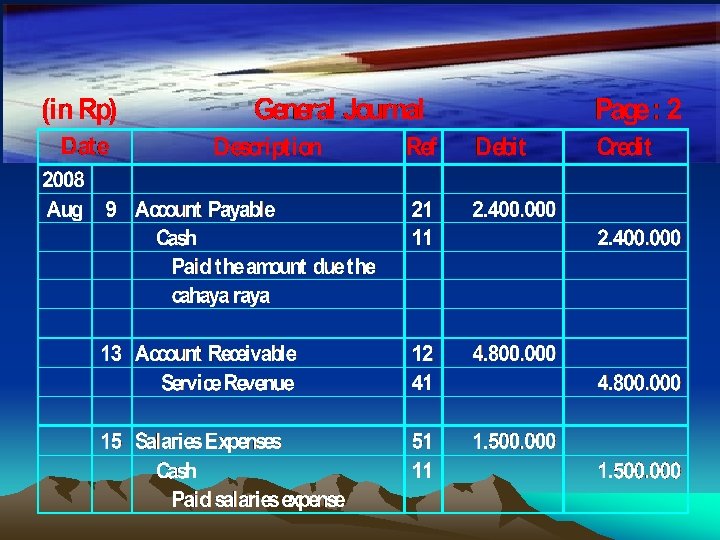

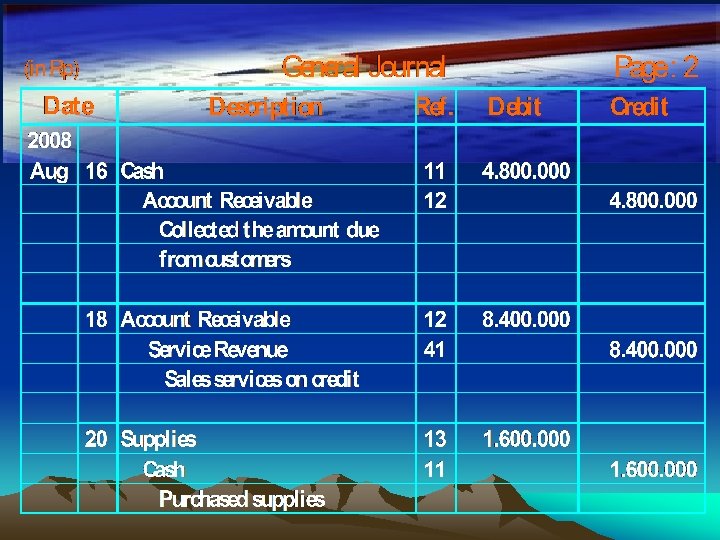

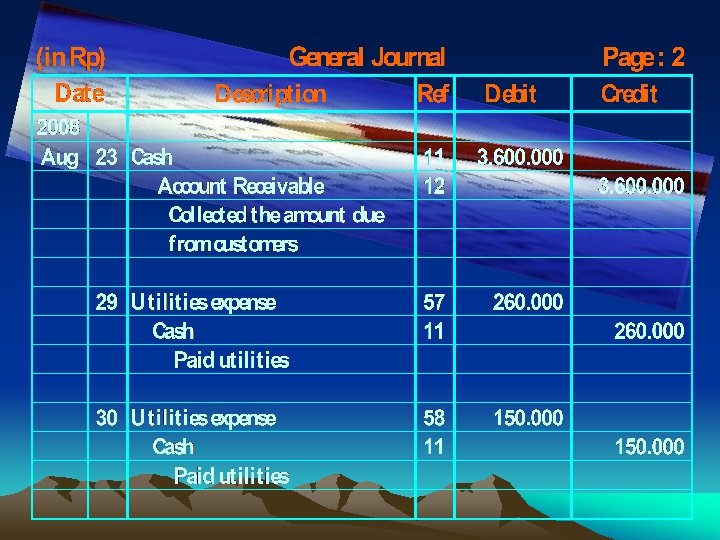

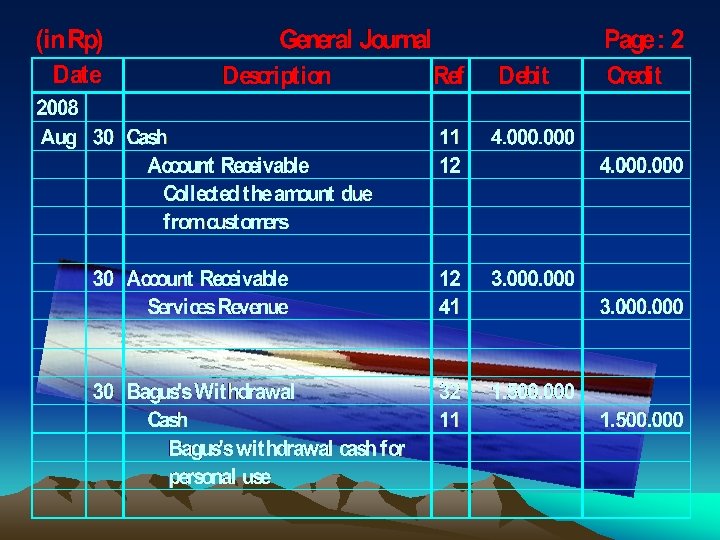

General Journal in Cipta Jasa Karya

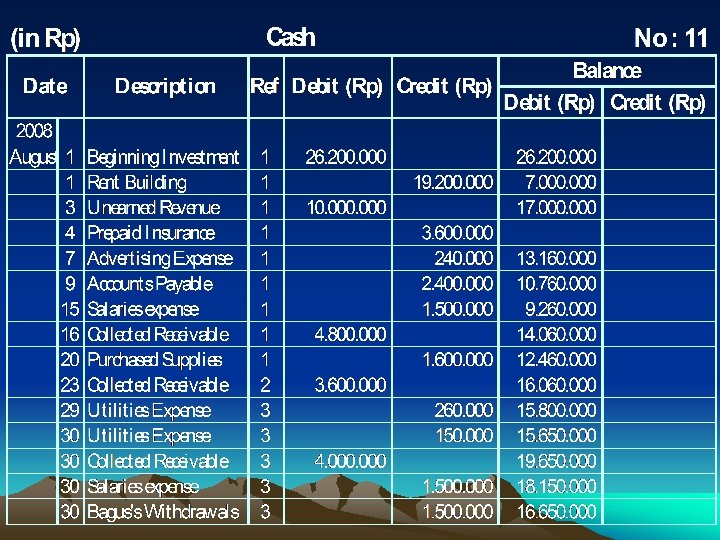

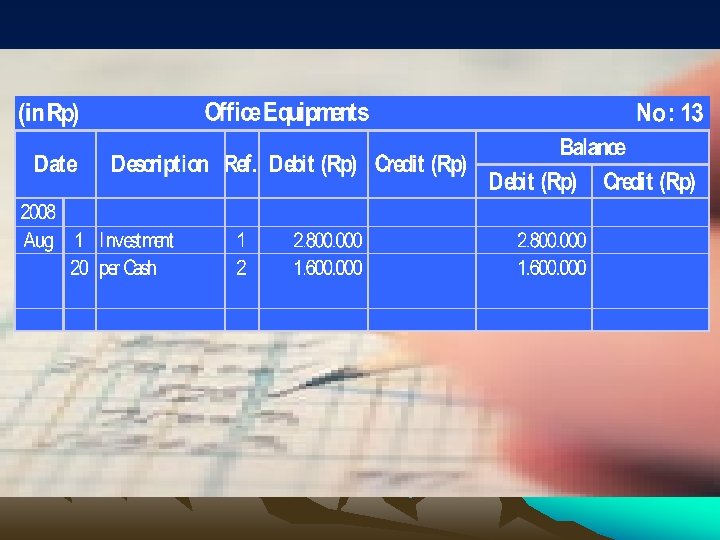

(in Rp) Office Equipment Date Description 2008 Aug 1 per Cash 2 per Cash Date Balance Ref. Debit (Rp) Credit (Rp) 1 1 25. 000 4. 000 25. 000 29. 000 Account Payable (in Rp) Description No : 16 No : 21 Balance Ref. Debit (Rp) Credit (Rp) 2008 Aug 2 Purchased on Credit 1 9 Paid 2 4. 000 2. 400. 000 1. 600. 000

(in Rp) Unearned Revenue Date Description Ref Debit (Rp) Credit (Rp) No : 23 Balance Debit (Rp)Credit (Rp) 2008 Aug 3 (in Rp) Date Collected Down Payment 1 10. 000 No : 31 Bagus's Capital Balance Ref Debit (Rp) Credit (Rp) Description Debit (Rp) Credit (Rp) 2008 Aug 1 Owner's Investment 2 54. 000

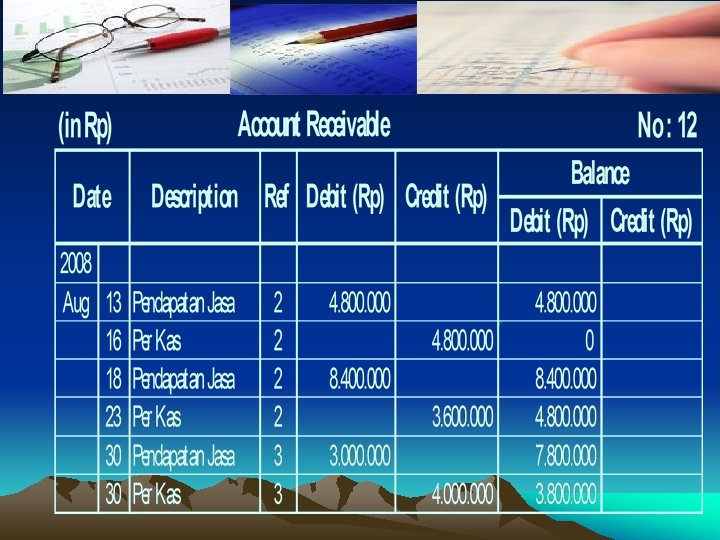

(in Rp) Date Bagus's Withdrawals Descriptio n 2008 Aug 30 Per Cash (in Rp) Dat e 2008 Ref Debit (Rp) Credit (Rp) 3 1. 500. 000 Aug 13 Receivables 18 Receivables 30 Receivables Re Debit f (Rp) 2 2 3 Balance Debit (Rp)Credit (Rp) 1. 500. 000 Servives Revenue Descripti on No : 32 No : 41 Credit (Rp) 4. 800. 000 8. 400. 000 3. 000 Balanc Debit e Credit (Rp) 4. 800. 000 13. 200. 000 16. 200. 000

(in Rp) Date Salaries Expense Description 2008 Aug 15 per Cash 30 per Cash 2 3 1. 500. 000 Balance Debit (Rp) Credit (Rp) 1. 500. 000 3. 000 Advertising Expense (in Rp) Date Ref Debit (Rp) Credit (Rp) No : 51 Description 2008 Aug 7 per Cash Ref Debit (Rp) Credit (Rp) 1 240. 000 No : 56 Balance Debit (Rp) Credit (Rp) 240. 000

Utilities Expense (in Rp) Date Description 2008 Aug 29 per Cash 3 260. 000 Utilities Expense (in Rp) Date Ref Debit (Rp) Credit (Rp) Description 2008 Aug 30 per Cash Ref. Debit (Rp) Credit (Rp) 3 150. 000 No : 57 Balance Debit (Rp) Credit (Rp) 260. 000 No : 58 Balance Debit (Rp) Credit (Rp) 150. 000