Portfolio Selection with Support Vector Regression Henrique Pedro

. Stock selection using support vector")

- Slides: 10

Portfolio Selection with Support Vector Regression Henrique, Pedro Alexandre University of Brasilia, Brazil

WHY SVM? • Machine Learning • SVM & SVR • Stocks selection Chih-Chung Chang and Chih-Jen Lin, LIBSVM : a library for support vector machines, 2001. • Multiple dimensions From Dr. Sead Sayad web site -Support Vector Machine - Regression (SVR) Expand the information from the variables The importance of choosing Kernel

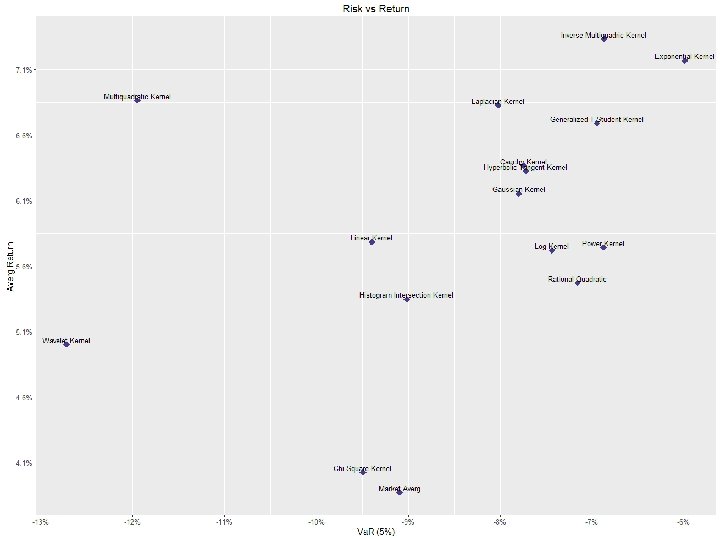

APPLICATION • SVR – Support Vector Regression • Test different 15 Kernels for portfolio selection to beat the market The dual function: Kernel ( Multi dimensional mapping) Predict function. Gaussian Radial Basis Kernel:

WORKFLOW • S&P 100 – from 06/30/2014 • Fundamental data from 06/29/1990 to 06/30/2014. • Fundamentalist analysis • Feature Selection • From 127 down to 24 features Cross Validation Training Validation 52, 5% Random Selection Test 22, 5% 25%

STRATEGY • Forecasting the quarterly return of the stocks for the Portfolio Selections. • 15 portfolios - weighted by the forecast return • Benchmark for the portfolios: • Equal weighted portfolios with the 100 stocks.

RESULTS

374, 40% 192, 65%

RESEARCHERS IN PROGRESS • Machine per sector • Other inputs • Kernel combination • SVM with risk management tools

THANK YOU! Fan, A. , & Palaniswami, M. (2001). Stock selection using support vector machines. Paper presented at the Neural Networks, 2001. Proceedings. IJCNN'01. International Joint Conference on. Marcelino, S. , Henrique, P. A. , & Albuquerque, P. H. M. (2015). Portfolio selection with support vector machines in low economic perspectives in emerging markets. Economic Computation & Economic Cybernetics Studies & Research, 49(4). Huerta, Ramon, Fernando Corbacho, and Charles Elkan. "Nonlinear support vector machines can systematically identify stocks with high and low future returns. " Algorithmic Finance 2. 1 (2013): 45 -58. Emir, S. , Dinçer, H. , & Timor, M. (2012). A Stock Selection Model Based on Fundamental and Technical Analysis Variables by Using Artificial Neural Networks and Support Vector Machines. Review of Economics & Finance, 106 -122. Packages: Robustbase Performance. Analytics Ggplot 2 robustbase Dplyr Scales Kernlab Fselector Mlbench Foreach do. Parallel do. SNOW rgl Pedro Alexandre M. B. Henrique. pedroalexandre. df@gmail. com