Personal Banking Services Deposit Accounts Deposit accounts offered

Personal Banking Services Deposit Accounts Deposit accounts offered by commercial banks help their customers in settling daily transactions and saving money to earn interest. They are current accounts and deposit accounts in various maturity terms and currency. Some are linked with equity or foreign exchange having higher risk in the movement of the price or rate of the underlying shares or foreign currency.

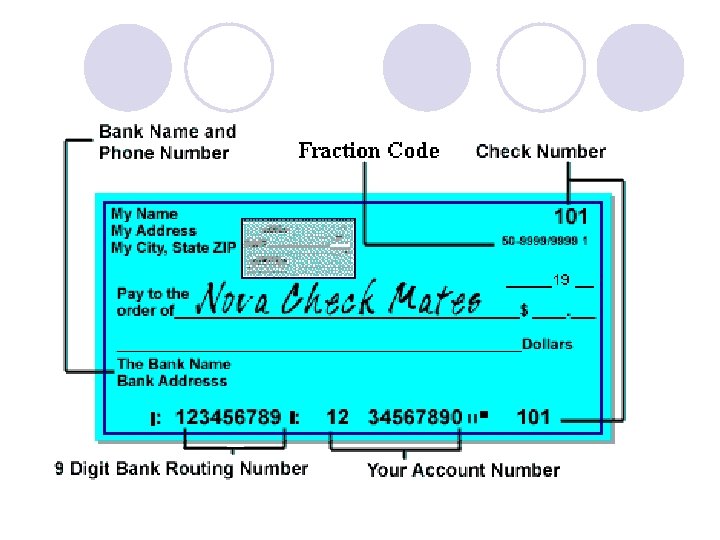

Hong Kong Dollar Deposit Accounts Current Accounts l It is previously a non-interest bearing account, which serves the purpose of paying or settling day to day monetary transactions of the customer by cheques. After the removal of the interest rate agreement of the Hong Kong Association of Banks, commercial banks have started paying interest to holders of current accounts with certain required credit balance. The holders of current accounts can withdraw or transfer funds from the accounts at any branches without giving prior notice to the bank. Cheques can be drawn for settling trade transactions or personal debts.

Hong Kong Dollar Deposit Accounts Current Accounts l A current account should always be maintained in credit balance unless an overdraft arrangement has been previously made so that there is an agreed limit up to which the customer can draw on the account. Subject to the bank’s assessment of its customer’s creditworthiness and/or security offered, an overdraft limit can be agreed within which cheques will not be returned unpaid even though the account is in debit balance.

Hong Kong Dollar Deposit Accounts Current Accounts l Payable interest is calculated on the amount of the overdraft on a daily basis and charged to the account monthly at an agreed interest rate. Such overdraft facility of bank has an advantage that the customer need not pay any interest unless overdraft is incurred. However, commitment fee and annual review fee are usually charged by bank. l Periodic, normally on monthly basis, statements are provided by the bank for customer’s record and reconciliation.

Hong Kong Dollar Deposit Accounts Savings Accounts l It is an interest bearing account. The interest earning system is based on the daily balance and is credited to the account either monthly or semi-annually. The customer can withdraw funds at any time with the passbook without giving prior notice to the bank. Savings account without a passbook is usually called statement savings account. This type of savings account has the convenience that money can be withdrawn without bringing the passbook. Details of each transaction are printed on monthly statement and mailed to customers. Such accounts can be maintained in Hong Kong dollars, any major currencies, or multi-currency.

Hong Kong Dollar Deposit Accounts Time Deposits l It is also called Fixed Deposit in Hong Kong. A deposit tenor ranging from 1 day, or 1 week, or 1 month to a year is agreed between the bank and its customers. The interest rates are higher than that of the Savings Account. But the customer usually cannot withdraw the money before the due date of the agreed tenor, although some banks allow such beforematurity withdrawal with interest forfeiture and even adding a penalty.

Hong Kong Dollar Deposit Accounts Call Deposits l A call deposit is one, which requires the customer to give a certain period of time of an advance notice for withdrawal of funds. Such required period of time ranges from 24 hours to 7 days. For instance, a 24 -hour call deposit requires one day’s advance notice to the bank when funds are to be withdrawn from the account. The interest earned is less than a time deposit but a bit more than savings account.

Hong Kong Dollar Deposit Accounts Target Deposits l It is also called Installment Deposit. This is a time deposit account whereby the customer sets a target amount of funds to be saved in a selfdetermined period of time. Different banks have different levels of pre-set minimum deposit amount. The customer then regularly, say on monthly basis, deposits the pre-set amount of money on an agreed date of a month. At the end of the pre-determined time period, the saved funds and the interest earned can be withdrawn. The interest rate is higher than that of savings deposit because the funds are locked in the bank for a longer time from one year to three years.

Foreign Currency Deposit Accounts Savings Account l Similar to the Hong Kong dollar Savings Account, there is no pre-set minimum deposit limit and the customer can withdraw funds at any time with the passbook and without giving prior notice to the bank.

Foreign Currency Deposit Accounts Time and Call Deposits Foreign currency time and call deposits give the customer the opportunity to take advantage of the higher interest rate of certain foreign currencies but run the risk of the relative exchange rate fluctuation.

Foreign Currency Deposit Accounts Swap Deposit It is designed to help foreign currency depositors to eliminate or minimize the exchange rate risks. It is a foreign deposit plus a forward contract to sell the foreign currency at a predetermined exchange rate on a particular future date. It has been a Hong Kong dollar deposit, in reality, which dispenses with the Interest Rate Agreement of the Hong Kong Association of Banks.

Other Deposit Accounts Paper Gold Deposit The depositor who places funds with a paper gold deposit does not hold any physical amount of gold, but in terms of their market value, the value of gold is then represented in terms of US dollar, which in itself can be remitted in Hong Kong dollars.

Other Deposit Accounts Deposit linked with investment of share or foreign currency l It combines the benefit of a time deposit and an investment. The bank customer is actually buying or selling a share, currency or Hang Seng Index option. The option premium is paid to the bank customer as interest of the deposit. If the underlying asset is more volatile, the option premium is higher and so the interest of the deposit to be paid. So such deposit is always termed as high yield deposit by banks.

Other Deposit Accounts Deposit linked with investment of share or foreign currency l If the price of the underlying asset moves unfavorably to the depositor, i. e. the option buyer will exercise the option right, the depositor will have to receive the underlying assets at the price pre-determined upon placement of the deposit, instead of receiving the deposit principal in original currency. For example, the depositor will receive a number of shares or a certain amount of foreign currency at the predetermined share price or exchange rate. Therefore, the depositor takes such risk of share or currency price fluctuation in return of gaining higher interest.

Lending Services Personal loans l Personal loans are mostly offered in the form of installment loans, which are granted by banks to their customers over fixed periods of time. The repayment schedule of a personal loan is usually fixed in amount and time. The most popular repayment schedule would be monthly or semi-monthly and the amount would be spread in equal installments over the whole term of the loan. The bank usually does not have the right to demand early repayment unless the customer fails to meet the agreed repayment schedule.

Lending Services Personal loans l The purpose of a personal loan may be to finance a vacation or to make a tax payment, depending on the needs of the customer. Personal loans are normally unsecured. An unsecured loan usually carries a high risk to the bank, thus the borrower is required to pay a higher rate of interest on the amount borrowed. Usually unsecured personal loans are for shorter periods of time and for smaller amounts. A personal loan may be supported by a third party guarantee. It is still treated as unsecured unless the guarantee is supported by property. If a personal loan is secured, a longer period of loan, larger amount and lower interest rate may be agreed by the bank.

and EFTPOS The introduction of")

Debit Card and Payment Services Automated Teller Machine (ATM) and EFTPOS The introduction of ATMs by the banks has been a most significant development in the recent banking history in Hong Kong. There are 2 main local ATM networks in Hong Kong, the “ETC” of the HSBC bank group and the “JETCO” – Joint Electronic Teller Services Co. Ltd. jointly owned by around 40 banks in Hong Kong.

and EFTPOS ATMs are usually")

Debit Card and Payment Services Automated Teller Machine (ATM) and EFTPOS ATMs are usually located at the bank’s premises or some busy places such as shopping centers and transportation depots. Customers can access to their accounts for cash withdrawal, balance checking, payment of bills, account transfers, cash deposit, and request for cheque book, without going into the banks’ offices. Each customer is issued a card with a personal identity number (PIN) to use the ATM.

and EFTPOS A bank customer")

Debit Card and Payment Services Automated Teller Machine (ATM) and EFTPOS A bank customer can obtain the following benefits using an ATM cards: l 24 -hour availability of cash l convenient location of ATMs l payment of bills after office hours l perform banking transactions after office hours, such as account transfer and depositing cash to bank account l cash can be obtained in overseas countries via international ATM networks

Debit Card and Payment Services Customers with ATM cards may also use their cards to access the Easy-Pay-System (EPS). EPS developed by a company in the HSBC group is a computer system allowing electronic funds transfer at point of sales (EFTPOS). There around 40 banks in Hong Kong which have joined this network, and their customers can pay electronically for purchases by directly transferring money on line from bank accounts to the accounts of the retail outlets.

Debit Card and Payment Services The customers simply key in the PIN with his card at the cash check point, funds are automatically transferred by debiting his bank account and crediting the retailer’s bank account for the amount of the purchase. The EPS provides convenience to the customer who does not have to carry any cash.

Debit Card and Payment Services Global ATMs have become available which enable customers to withdraw and inquire balance in overseas countries. There are two large international ATM networks, the PLUS and the CIRRUS. Unlike local networks, cardholders are charged a fee of around HK$25 and $5 for each withdrawal and balance inquiry transaction respectively.

Credit Card, Debit Card and Electronic Payment Services It is common that a plastic card incorporating 3 types of services – ATM, EPS and credit card.

Hire Purchase Hire purchase is indeed a kind of loan arrangement in that the acquisition of an asset is completed by way of installment finance. This financing method is usually used for purchase of consumer goods, such as electrical appliances and furniture. The retailer sells the goods while a bank/finance company provides the financing via a hire purchase scheme.

Hire Purchase The buyer of goods, the hire purchaser, can obtain use of the goods immediately by paying a down deposit of around 10% to 20% of the total value of the goods. The remaining balance will be paid later by a number of installments. It is quite often paid by 12 to 24 monthly installments. The installments cover repayment of both the cost price and interest plus profit.

Hire Purchase In most hire purchase agreements, the ownership of the goods sold does not pass the title to the user until the last payment is made. In other words, the hirer (i. e. the finance company offering the hire purchase scheme) is the legal owner of the goods in the hire purchase period.

Hire Purchase Hire purchase is a high risk business. In case of default, recovery of the asset may prove difficult. Even if recovered, the asset cannot always be resold easily and the resale price is almost invariably lower than the current book value. The risk of obsolescence is borne by the hire purchase company.

Credit Cards Nowadays many people use credit cards to purchase goods and services at retail outlets where the cards’ signs or logos are displayed, which mean that the retail outlets are members of the credit card companies.

Credit Cards Every time a cardholder uses his credit card to make purchase, he signs the sales slip in the presence of the seller. A dispensing machine records the sales, the amount, the date of transaction and the card’s account number. The vendor will then claim reimbursement from the card company and pay a service commission ranging from 1. 5% to 5% of the sales value.

Credit Cards The card holder will receive from the credit card company a monthly statement describing the purchase records over the previous month, the amount paid by the customer in last month and the amount owed up-to-date. The card holder has the option of paying the total amount due before a deadline or paying a minimum amount. If the cardholder opted for the latter, he would have to pay interest on the amount outstanding.

Credit Cards Most credit cards have a credit limit revocable on a monthly basis and the credit limit depends on the income, the profession and the spending habit of the cardholder.

Advantages to a credit card holder Credit limit is allowed. l Credit cards are accepted in millions of outlets worldwide. l Interest free credit period from normally 45 days to even 60 days. l A secure way to carry money in Hong Kong or abroad. l

Disadvantages to credit card holder l l l Cash advances on a credit card are expenses. Cardholder has to pay relatively high interest unless payment of card debts is made on time. Impulse spending can get out of hand, leading to repayment problem. If payment is made overseas, the Hong Kong dollar equivalent is not fixed until the voucher is processed by the credit card company. More money has to be paid if Hong Kong dollars are depreciating.

Advantages to retailers Accepting credit cards may attract more sales. l It may produce an image that the company is selling goods of upper market. l Payment guaranteed by credit card company. l Security will be better for accepting fewer cash. The expense of delivery of cash is also reduced. l

Disadvantages to retailers Commission of 1. 5% to 5% is paid to the credit card company. l Investment of equipment may be required. l Money is to be credited to account one or two days after submitting vouchers. l

Debit Card vs Credit Card l There is a variation of the credit card, whereby the cost of purchases is charged directly to a cardholder’s account, such as a savings account or current account, maintained with a bank. Hence, it could be more accurately described as a “debit card”. The operations of such card resemble very much that of a credit card. The cardholder is required to sign voucher, which is also required to be submitted by the retailers to the card company. The only difference of using a debit card is that the cardholders’ account are debited on line instantly whereas a debit note will be issued to cardholder for payment if a credit card is used.

Foreign currency exchange l When you travel abroad, you will find it convenient to take some foreign currency, even if you also take travellers’ cheques or credit card etc. , as you may arrive on a public holiday in the evening or at a weekend and thus unable to cash travellers’ cheques immediately. Banks therefore sell the most common foreign currencies notes (e. g. UD dollars, Euro, Japanese Yen etc. ) on demand at branches to customers.

Foreign currency exchange l While taking foreign currency abroad has the advantage that it can be used immediately upon arrival and must be accepted by shops and restaurants, there is a risk of theft or loss. It is also bulky to carry in large quantities. In some countries with exchange control, the traveller may be forbidden to take enough cash into the country. Therefore it is usual that travellers’ cheques, credit card, or ATM card will also be brought along when travelling abroad.

Foreign currency exchange l Banks not only provide exchange at the bank’s counters for travel purpose but also offer deposit accounts on foreign currencies, both for savings and fixed deposits. Placing foreign currency deposits will earn interest as well as principal gain if the currency will appreciate against Hong Kong dollars. But it will turn to a loss if the currency rate move the opposite direction. The depositor should know that he runs the exchange risk if he saves or invests in foreign currency deposits.

Foreign currency exchange Moreover, customers can participate in foreign exchange forward contract via banks in the foreign exchange market. A forward exchange contract is: l a fixed and binding contract between the bank and its customer, l to buy or sell a specified foreign currency, l at an exchange rate fixed at time of making the contract, and l will be delivered at a fixed or determinable date. l Such contract can help the bank customer hedge the exchange risk.

Traveller’s cheques allow users to have the same advantage of holding cash. They are popular because travellers’ cheques are less bulky and more secure than taking currency notes. Travellers’ cheques in most common currencies and a wide variety of denominations are available to customers from banks. American Express, Visa and Mastercard are examples of large issuer of travellers’ cheques. You can purchase cheques issued by them from a bank where their logo is displaced at counter. The bank charges 0. 5% to 1% commission on the amount of cheques sold.

Traveller’s cheques When the cheques are issued to a customer, the bank will require the customer to sign the cheques. The traveller should ensure that the cheques are kept safely, as otherwise he may not be able to claim a refund in the event of loss or theft, thus losing one of the major advantages of travellers’ cheques. Assuming that the issuer does not feel that the conditions of issue have been breached, a full refund will be made if the cheques are lost or stolen within a short period of time. Some issuers require the traveller to report lost of the cheques immediately and quote the serial numbers to obtain a refund.

Traveller’s cheques When the customer is cashing the travellers’ cheques at a bank or using them at a purchase point, he has to countersign the cheques with the same signature in front of the cashier. The signature is then compared with the first one above; thus, only the owner of the cheques or a skilled forger should be able to cash the cheques. In view of such cashing procedures, it is prudent for the purchaser to sign in the first signature space at once when the cheques are purchased.

Advantage of taking travellers’ cheques abroad l l l They are easy to obtain. Most banks sell travellers’ cheques through their branch network. There is a choice of many currencies. They are secure and convenient to carry around. They are widely accepted for encashment from banks and hotels and for purchase from department stores etc. There may be automatic refunds incase of lost or stolen.

Disadvantages of taking travellers’ cheques abroad l l They usually have to be cashed at a bank, so there are problems with bank opening hours. They cannot usually be used to pay directly for goods or services and so the traveller has to make time to go to a bank. The traveller has to keep a record of the serial numbers to get a refund. Payment must be made before the start of the trip. As opposed to using credit card, payment is to be made after coming back from the trip. There may be a loss of interest.

Disadvantages of taking travellers’ cheques abroad Unused cheques have to be converted back into local currency. A loss in the exchange may be incurred. l Commission is charged on issue. l Traveller has to take time to purchase and collect the cheques from a bank before departure. l

- Slides: 52