Part II Business Level Strategies Cost Leadership WalMart

Part II Business Level Strategies Cost Leadership

Wal-Mart • Growth • The dark side

• Product differentiation (Chapter 5)")

Two Generic Strategies • Cost-leadership (chapter 4) • Product differentiation (Chapter 5)

Other cost leaders • BIC • Timex • Casio

Sources of Cost Advantages • Size differences and economies of scale example: ATM – With higher production volume • Firms can use specialized machines • Firms can build larger plants – Process manufacturing • Firms can increase employee specialization • Firms can spread overhead cost across more units produced

Sources of Cost Advantages • Size differences and Diseconomies of scale example: Oregon mills – Physical limits to efficient size – Managerial diseconomies – Worker de-motivation – Distance to markets and suppliers

Sources of Cost Advantages • Experience differences and learning -Curve Economies – The learning curve • Each time production doubles average labor costs go down by a certain percentage • The learning curve and Competitive advantage example: Texas Instrument – Doesn’t always happen Beer Industry

Sources of Cost Advantages • Differential Low-cost access to Productive inputs – Productive inputs • • Land Labor Capital Raw Materials

Ethics The Race to the Bottom

• Nike • Response

Sources of Cost Advantages • Technological Advantages independent of scale – Technological Hardware – Technological Software

Sources of Cost Advantages • Policy Choices • HP wanted a $49 printer to compete with Lexmark • 43% of sales and 65% of profits

Cost Leadership and… • • • The Threat of Entry The Threat of Rivalry The Threat of Substitutes The Threat of Suppliers The Threat of Buyers

Cost Leadership & Sustained Competitive Advantage

Entrepreneurship • Oakland A’s – – Small Market Second most wins Evaluate players Batters • OBP & Total Bases – Pitchers • First pitch strikes & speed of fast ball – Consistency in farm system

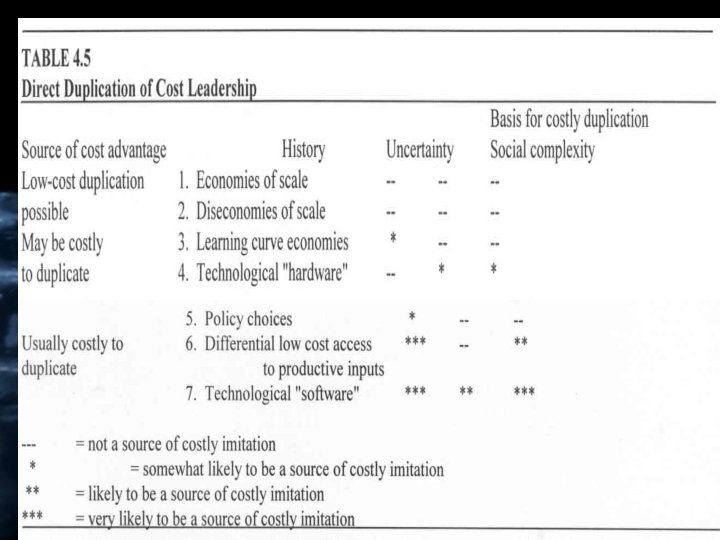

The imitability of sources of Cost Advantage • Easy to duplicate – Economies and Diseconomies of scale • Costly to duplicate – Learning curve? – Differential low-cost access

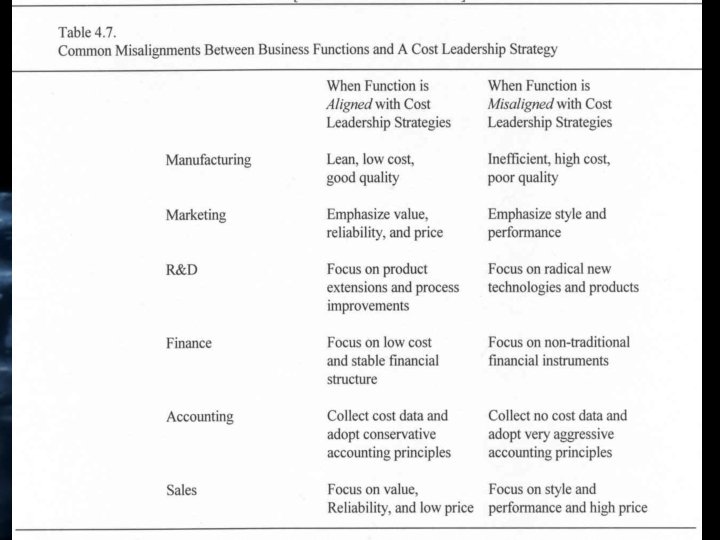

Organizing for cost leadership

- Slides: 20