PARENTS DIC BY JERRY PARENTS DIC Parents DIC

PARENTS DIC BY JERRY

PARENTS DIC • Parents' DIC is a tax-free, income-based monthly benefit for the parents of a military service member or veteran who has died from: • A disease or injury incurred or aggravated while on active duty or active duty for training • An injury incurred or aggravated in line of duty while on inactive duty for training • A service-connected disability

PARENT'S DIC ELIGIBILITY • The term "parent" includes a biological, adoptive, and foster parents. For these purposes, a foster parent defined as someone who stood in the relationship of a parent to the veteran for at least one year before the veteran's last entry into active duty. • Parents must have an income below a certain level. The DIC is based on the income level. • Both of these must be true: • You’re the biological, adoptive, or foster parent of the Veteran or service member, and • Your income is below a certain amount

PARENTS DIC • Needs based program • Based on Income not net worth, all sources of income are considered (income exceptions are the same and NSC and Death Pension) • Parents Dependency and Indemnity Compensation (DIC) is calculated on a calendar-year basis • Note: This is true regardless of when the Department of Veterans Affairs (VA) receives the claim. There is no “initial year” for Parents’ DIC as there is for pension.

THE FOLLOWING TYPES OF INCOME CONSTITUTE COUNTABLE INCOME FOR PARENTS’ DIC PURPOSES: • total income from employment, business (minus operating expenses), investments, interest, or rents • income of a parent’s spouse with whom the parent lives • inheritances of money (but not property) • gifts of property or money, including contributions from adult children • unemployment compensation • retirement type benefits are counted at the rate of 90 cents on the dollar • life insurance proceeds and the proceeds of commercial annuities are counted at the rate of 90 cents on the dollar, and compensation for injury or death is countable. • Social Security, Railroad Retirement, Civil Service Annuity, military retired pay and other public or private retirement benefits are all counted at the rate of 90 cents on the dollar

THE FOLLOWING TYPES OF INCOME ARE NOT COUNTABLE FOR PARENTS’ DIC PURPOSES: • income of children (children are not dependents on Parents’ DIC awards) • inheritances of property (as opposed to money) • the value of maintenance by a relative, friend, or organization • Welfare and Supplementary Security Income (SSI) • VA pension or compensation benefits • Servicemembers’ Group Life Insurance (SGLI), United States Government Life Insurance (USGLI), and National Service Life Insurance (NSLI) proceeds

payments of a bonus or similar cash gratuity by any State based upon service in the Armed Forces proceeds of cashed-in savings bonds proceeds of cashed-in life insurance policies Social Security lump-sum death benefit payments received under the Radiation Exposure Compensation Act (RECA), Public Law (PL) 101 -426 payments under section 103(c)(1) of the Ricky Ray Hemophilia Relief Fund Act of 1998 payments under the Energy Employees Occupational Illness Compensation Program payments to certain eligible Aleuts under 50 U. S. C. 4236 the value of an increase of stock inventory of a business an employer’s contributions to health and hospitalization plans for either an active or retired employee payments received from the Coronavirus Aid, Relief, and Economic Security Act of 2020, and any other payment excluded by statute.

DEDUCTIBLE EXPENSES • Unreimbursed medical expenses that exceed 5 percent of reported annual income can be deducted under 38 CFR 3. 262(l). • Important: Reported annual income refers to all countable family income before the 10 -percent reduction for retirement income. Reported annual income does not include any income that is not countable for Parents’ DIC purposes. • Count medical expense the same as NSC or Death Pension (Payments for such medical expenses must be unreimbursed to be deductible from income) • Some legal expenses can be deducted.

PARENTS DIC AND AA • Aid and attendance. The monthly rate of DIC payable to a parent under this section shall be increased by the amount specified in 38 U. S. C. 1315(g), as increased from time to time under 38 U. S. C. 5312, if such parent is: • (1) A patient in a nursing home, or • (2) Helpless or blind, or so nearly helpless or blind as to need or require the regular aid and attendance of another person.

Your total")

HOW PARENTS DIC IS CALCULATED Yearly income limit (in U. S. $) Your total income for the year must be less than or equal to this amount Beginning monthly rate (in U. S. $) Rate of decrease (also called a $1 decrement) $7, 000 $23 . 08 7, 100 15 . 08 7, 200 7 . 08 7, 224 5. 08

HOW TO USE THE RATE TABLES TO CALCULATE YOUR DIC PAYMENTS • Find your beginning monthly rate in the table above that applies to you. To do this, find the yearly income limit amount in the first column that’s closest to your income when rounded up. The amount listed to the right, in the middle column, is your beginning monthly rate. • For example: Let's say you're the eligible parent, living with the Veteran's other parent or a current spouse. For this example, click on the $7, 000 or more income range directly above. If you earn $7, 153 a year, you make more than $7, 100, and less than $7, 200. So you would use the $7, 200 income limit. Your beginning monthly rate would be $7. • Calculate the difference between your actual income and the income limit that's closest to your income when rounded down. To do this, find the income limit in the first column that's closest to your income when rounded down. Subtract this income limit from your actual income. • Using our example: $7, 153 (actual income) - $7, 100 (income limit closest to your income when rounded down) = $53

HOW TO USE THE RATE TABLES TO CALCULATE YOUR DIC PAYMENTS • Multiply this amount by the rate of decrease. The rate of decrease is the decimal listed in the last column. It helps us adjust your rate to match your actual income level. • Using our example: $53 X. 08 (rate of decrease) = $4. 24 • Add this amount to your beginning monthly rate. The total is your monthly payment. • Using our example: $4. 24 + $7 (beginning monthly rate) = $11. 24 (monthly payment) • If you're eligible for Aid and Attendance, add $364. The total is your monthly payment with Aid and Attendance. • Using our example: $11. 24 (monthly payment) + $364 (Aid and Attendance) = $375. 24 (monthly payment with Aid and Attendance)

PARENTS DIC HOW TO APPLY • File using a 21 -535 • 21 -2680 for AA • Provide financial evidence similar to NSC or Death Pension • Provide Medical Expenses similar to NSC or Death Pension

QUESTIONS • From what I could find there is no limit on Net worth for Parents DIC • There are income limits if you are over the income limit you will not qualify • Medical expense can be counted as an offset • Aid and Attendance can be added to Parents DIC • This M-21 reference will tell you all the details of Parents DIC: • M 21 -1, Part V, Subpart iii, Chapter 1, Section D - Parents’ Dependency and Indemnity Compensation (DIC)

DEPENDENCY AND INDEMNITY COMPENSATION • A tax free monthly benefit paid to eligible survivors of military Servicemembers who died in the line of duty or eligible survivors of Veterans whose death resulted from a service-related injury or disease. • To qualify for this benefit, the claimant(s) must be the eligible surviving spouse or dependent child of a military Servicemember or Veteran who: • Died while serving on active duty, active duty for training, or inactive duty training, OR • Died as a result of a service-connected injury or disease, OR • Died as a result of a non-service-connected injury or disease, and who was totally disabled from his/her serviceconnected disabilities for • at least 10 years immediately preceding death, OR • since the Veteran's release from active duty and for at least five years immediately preceding death, OR • at least one year immediately preceding death if the Veteran was a former prisoner of war.

DEATH INDEMNITY COMPENSATION FORMS TO USE • 21 -534 Ez • 21 -2680 • And then all the other supporting docs such as death cert and medical records if needed etc.

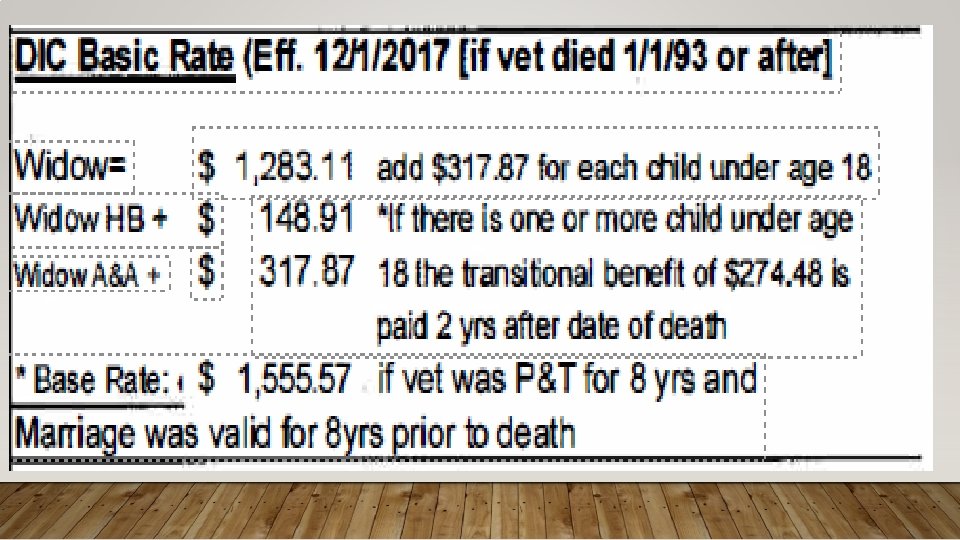

DEATH INDEMNITY COMPENSATION THINGS TO REMEMBER • If a vet was service-connected PT for 10 years, it doesn’t matter why they died • If the Surviving Spouse was married to the veteran for 8 years while he was PT and he died of a SC condition or was PT for 10 years she will get what we call 8 and 8. • There is an additional amount paid for House bound and Surviving Spouses who require AA • Also, if a Surviving Spouse has children under the age of 18 there is an additional amount paid • DIC can be paid to children of veterans also • Champ VA awarded • Tax Relief for Surviving Spouse

- Slides: 18