Overview of Financial Markets Primary Markets versus Secondary

")

")

Users of")

")

")

– Cash management – Assisting with mergers and acquisitions – Back-office")

• Increases in holdings of fixed-income trading • Pretax profits soared to")

- Slides: 70

Overview of Financial Markets • Primary Markets versus Secondary Markets • Money Markets versus Capital Markets • Foreign Exchange Markets

Money Market Instruments Outstanding, 1990 -2001 ($Bn)

Capital Market Instruments Outstanding, 1990 -2001 ($Bn)

Flow of Funds in a World without FIs: Direct Transfer Financial Claims (Equity and debt instruments) Suppliers of Funds (Households) Users of Funds (Corporations) Cash Example: A firm sells shares directly to investors without going through a financial institution.

Flow of Funds in a world with FIs: Indirect transfer FI (Brokers) Users of Funds Cash Suppliers of Funds FI (Asset transformers) Financial Claims (Equity and debt securities) Cash Financial Claims (Deposits and insurance policies)

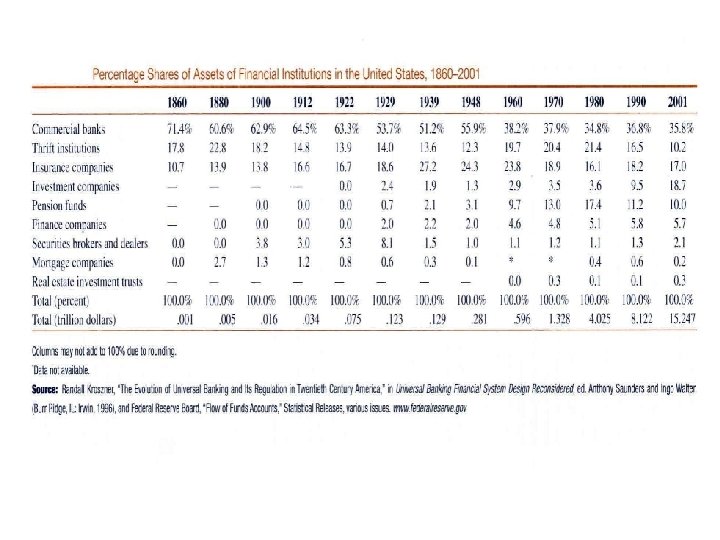

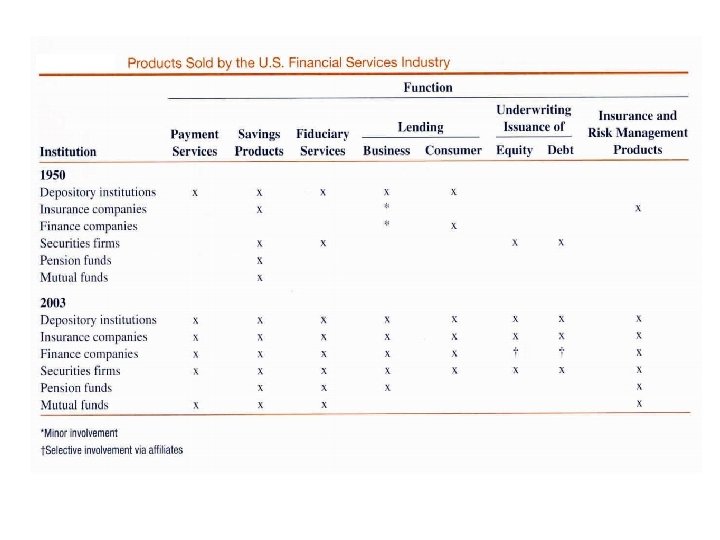

Types of FIs • Commercial banks • Thrifts • Insurance companies (continued)

• Securities firms and investment banks • Finance companies • Mutual Funds • Pension Funds

Services Performed by Financial Intermediaries • Monitoring Costs • Liquidity and Price Risk (continued)

• Transaction Cost Services • Maturity Intermediation • Denomination Intermediation

Services Provided by FIs Benefiting the Overall Economy • Money Supply Transmission • Credit Allocation (continued)

Services Provided by FIs Benefiting the Overall Economy • Intergenerational Wealth Transfers • Payment Services

Risks Faced by Financial Institutions • • • Interest Rate Risk Foreign Exchange Risk Market Risk Credit Risk Liquidity Risk Off-Balance-Sheet Risk Technology Risk Operational Risk Country or Sovereign Risk Insolvency Risk

Globalization of Financial Markets and Institutions • Financial Markets became more global as the value of stocks traded in foreign markets soared • Foreign bond markets have served as a major source of international capital • Globalization also evident in the derivative securities market

Factors Leading to Significant Growth in Foreign Markets • The pool of savings from foreign investors has increased • International investors have turned to U. S. and other markets to expand their investment opportunities • Information on foreign investments and markets is now more accessible (e. g. internet) • Some mutual funds allow ability to invest in foreign securities with low transaction costs • Deregulation has enhanced globalization of capital flows

Economies of Scale and Scope • Economies of scale • Economies of scope • Megamerger • X efficiencies

Measuring Economies of Scale ACi = TC i Si Where: ACi = Average costs of the ith bank TCi = Total costs of the ith bank Si = Size of the bank measured by assets, deposits or loans

Economies of Scale and the Effect of Technology Improvement Average Cost Old Technology AC 1 New Technology AC 2 0 Size

Economies of Scope • By offering more services to a given customer: • Cost economies of scope • Revenue economies of scope

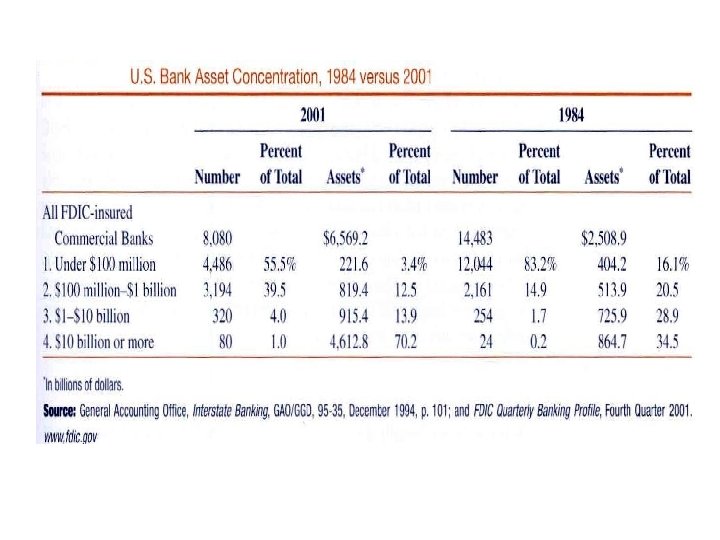

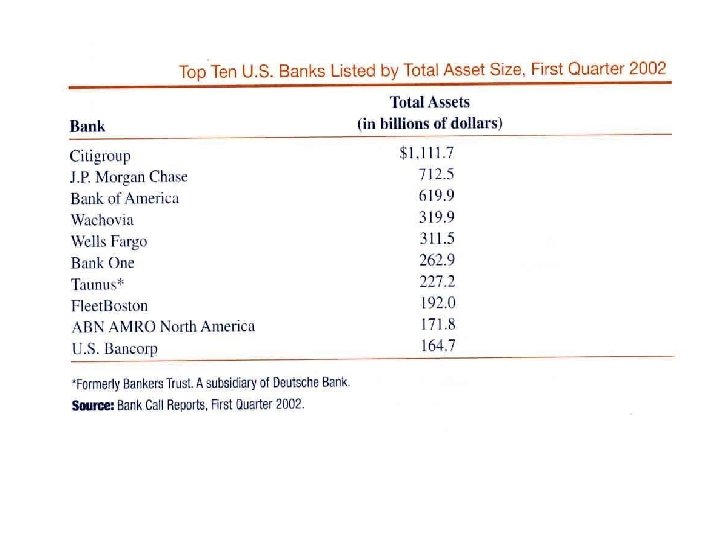

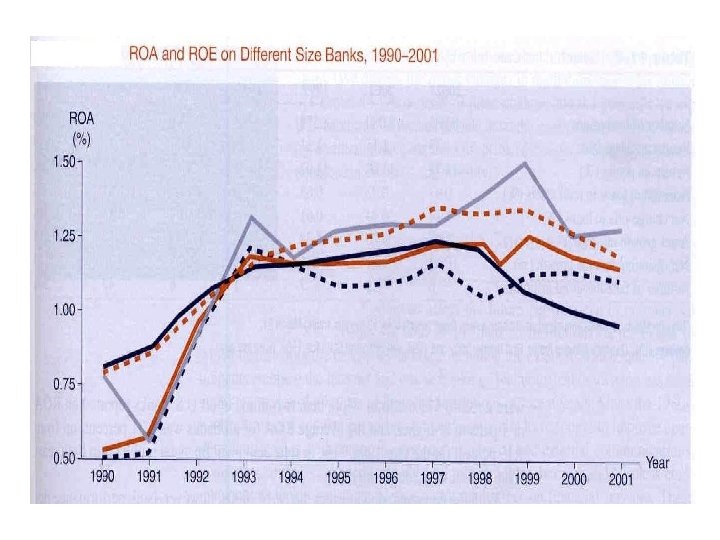

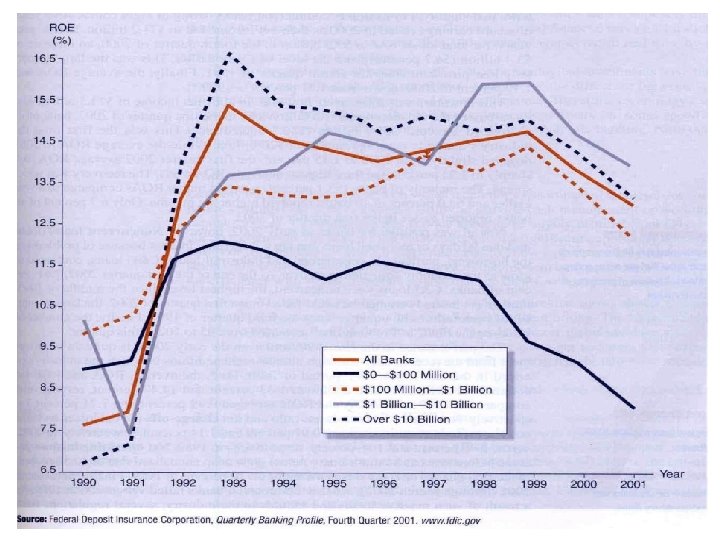

Bank Size and Activities • Large banks have easier access to capital markets and can operate with lower amounts of equity capital • Large banks tend to use more purchased funds (such as fed funds) and have fewer core deposits • Large banks lend to larger corporations which means that their interest rate spread is narrower – the difference between lending and deposit rates • Large banks are more diversification and generate more noninterest income

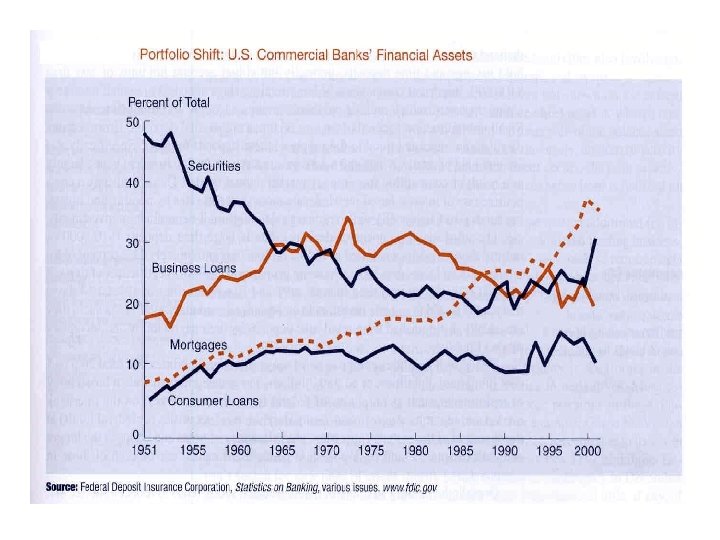

Balance Sheet and Trends • Business loans have declined in importance • Offsetting increase in securities and mortgages • Increased importance of funding via commercial paper market • Securitization of mortgage loans

Off-balance sheet activities • Heightened importance of off-balance sheet items

Other Fee-generating Activities • Trust services • Correspondent banking

1999 Financial Services Modernization Act • Financial Services Modernization Act – Allowed banks, insurance companies, and securities firms to enter each others’ business areas – Provided for state regulation of insurance – Streamlined regulation of BHCs – Prohibited FDIC assistance to affiliates and subsidiaries of banks and savings institutions – Provided for national treatment of foreign banks

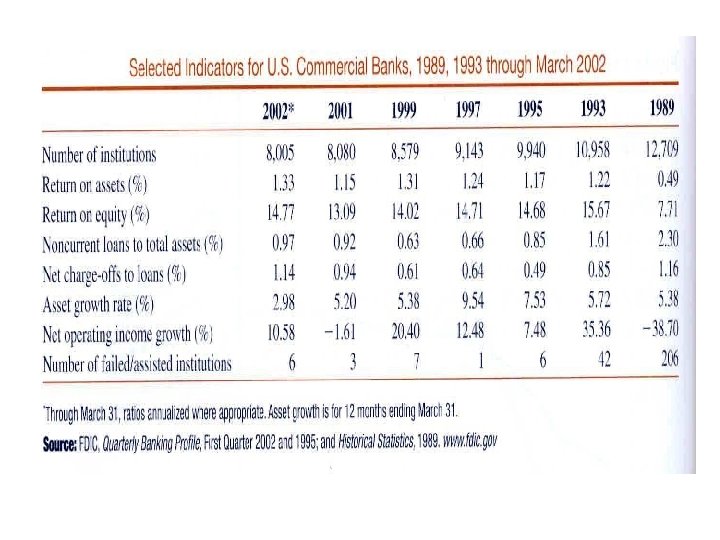

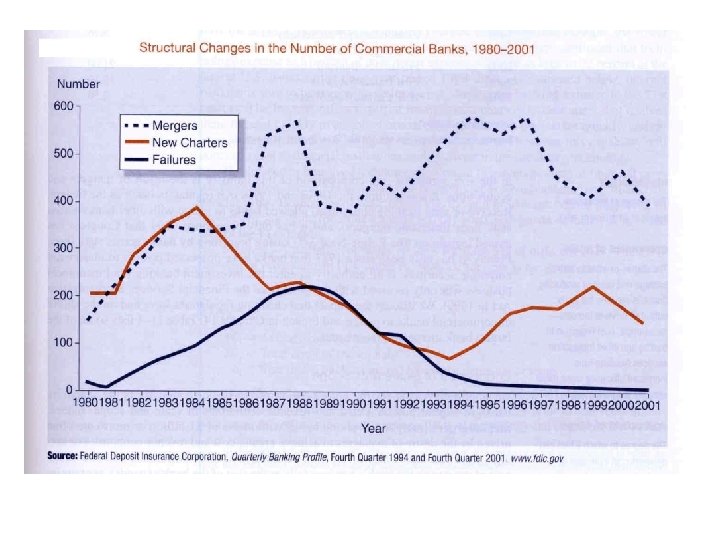

Industry Performance • Economic expansion and falling interest rates through 1990 s • Downturn in early 2000 s • Only 6 failures in 2000 versus 206 in 1989

Savings Institutions • Comprised of: • Savings and Loans Associations • Savings Banks – Effects of changes in Federal Reserve’s policy of interest rate targeting combined with Regulation Q and disintermediation. – Effects of moral hazard and regulator forbearance. – Qualified Thrift Lender (QTL) test.

Savings Institutions: Recent Trends • Industry is smaller overall • Intense competition from other FIs – mortgages for example • Concern for future viability

Credit Unions – Nonprofit depository institutions owned by member-depositors with a common bond. – Exempt from taxes and Community Reinvestment Act (CRA). – Expansion of services offered in order to compete with other FIs. – Approximately 2/3 federally chartered and subject to NCUA regulation.

Insurance Companies • Differences in services provided by: – Life Insurance Companies – Property and Casualty Insurance

Life Insurance Companies • Life Insurance Products: – Ordinary life – Group life – Industrial life – Credit life

Other Life Insurer Activities – Annuities – Private pension funds – Accident and health insurance

Balance Sheet – Long-term liabilities – Long-term assets

Property and Casualty Insurance • Size and Structure • Balance sheet

Property-Casualty • Changing composition of net premiums written – decline in fire insurance and allied lines since 1960 – Homeowners MP: – Commercial MP: – Auto L&PD: – Other liability:

Loss Risk – Underwriting risk may result from – Property versus liability:

Loss Rates – Severity versus frequency: • Loss rates more predictable on low-severity, highfrequency lines (such as fire, auto, homeowners peril) than on high-severity, low-frequency lines (such as earthquake, hurricane, financial guaranty). • Claims in high-severity, low-frequency lines may not be independent. • Higher uncertainty forces PC firms to invest in more short-term assets and hold larger capital and reserves than life insurance firms.

Recent Trends • PC industry was not very profitable during 1987 - 2000. • Reasons:

Global Issues • Insurance industry becoming more global

Securities Firms and Investment Banks • Nature of business: – Underwrite securities. – Market making. – Advising • Growth in mergers and acquisitions:

The Largest M&A Transactions

Key Activities – Investing – Investment banking – Market making – Trading

Key Activities (continued) – Cash management – Assisting with mergers and acquisitions – Back-office and service functions.

Trends • Decline in trading volume and brokerage commissions • Decline in underwriting activities over 198790. • Resurgence in activity and profitability 19912000.

Trends (continued) • Increases in holdings of fixed-income trading • Pretax profits soared to $21. 0 billion in 2000 • 1987: Federal Reserve allowed BHCs to expand securities underwriting.

Balance Sheet • Key assets: – Long positions in securities and commodities. – Reverse repurchase agreements. • Key liabilities: – Repurchase agreements major source of funds. – Securities and commodities sold short. – Broker call loans from banks • Capital levels much lower than levels in banks

Regulation • Primary regulator: SEC • Day-to-day trading practices regulated by the NYSE and NASD.

Mutual Funds • Open-ended • Closed-end • End of 2000:

Size, structure and composition – First mutual fund: Boston, 1924. – Slow growth, initially. – Advent of money market mutual funds, 1972. • Regulation Q. – Total assets in stock and bond mutual funds:

Size, Structure and Composition – By asset size, mutual fund industry second most important FI group. – Recent inroads by commercial banks and insurance companies

Types of Mutual Funds • Long-term funds – Bond and income funds. – Equity funds. – Hybrid • Short-term funds – Taxable and tax-exempt MMMFs – Generally higher returns than bank deposits but uninsured.

Types of Funds – Open-ended funds: – Closed-end investment companies: – Fixed number of shares – Load versus no-load funds.

Global Issues • Worldwide growth in mutual fund investment not as great as in the U. S.

Hedge Funds* • Not technically mutual funds • High returns in 1990 s • Near collapse of Long-Term Capital Management – $3. 6 million bailout

Finance Companies – Activities similar to banks, but no depository function. – May specialize in installment loans (e. g. automobile loans) or may be diversified, providing consumer loans and financing to corporations, especially through factoring. – Commercial paper is key source of funds. – Captive Finance Companies: e. g. GMAC

Major Types of Finance Companies – Sales finance institutions – Personal credit institutions – Business credit institutions

Balance Sheet and Trends – Business and consumer loans are the major assets – Increases in real estate loans and other assets. – Growth in leasing

Business Loans – Business loans comprise largest portion of finance company loans. – Advantages over commercial banks:

Business loans • Major subcategories: – retail and wholesale motor vehicle loans and leases – equipment loans – other business loans.

Liabilities • Major liabilities: commercial paper and other debt • Finance firms are largest issuers of commercial paper – Commercial paper maturities up to 270 days.

Regulation of Finance Companies – Federal Reserve definition of Finance Company – Subject to state-imposed usury ceilings. – Much lower regulatory burden than depository institutions.

Regulation – With less regulatory scrutiny, finance companies must signal safety and soundness to capital markets in order to obtain funds. – Lower leverage than banks – Captive finance companies may employ default protection guarantees from parent company or other protection

Global Issues • In foreign countries, Finance companies are generally subsidiaries of commercial banks or industrials • In Japan, ownership of finance companies by banks created opportunities when banks hit by increase in nonperforming loans