OUR JOURNEY TO A BETTER GAUTENG Gauteng Rapid

OUR JOURNEY TO A BETTER GAUTENG Gauteng Rapid Rail Integrated Network – GRRIN Tshepo Kgobe 10 July 2018

Contents 1. 2. 3. 4. 5. 6. 7. TMR & PPP Framework Lessons Learnt The challenge & Planning Modelling a Future Network The Routes and Phasing Socio-Economic Development Conclusions and Next steps

TMR & PPP Framework

A new modern Gauteng is in the making • Gauteng Premier’s first State of the Province Address • (27 June 2014 in Thokoza, Ekurhuleni) – Radically modernise the way Gauteng residents live and work – Ten pillars of radical transformation • Gauteng has a 25 year Integrated Transport Master Plan (GITMP) with Rail as its Public Transport backbone • Public transport as an economic growth stimulant • The GRRIN project is a key part of the 8 th pillar of the premier’s vision for the modernisation of public transport and other infrastructure thereby helping the economy of the province and the country

Gauteng’s Future Transport planning 1. Car/ vehicle growth and Road Congestion 2. Travel speeds without GRRIN 3. Travel time savings if GRRIN implemented 4. Population Growth and land use 5. Connectivity Challenges in Jhb North Western Sector

Dreaming Of a World-class Rail System To Connect Our People throughout Gauteng • Integrated public transport • At its core a rapid rail link system • Increased infrastructure investment • Spatial Development Initiatives to stimulate economic growth and job creation

Lessons learnt

Gautrain Key Success Factors 1. Political leadership and will 2. Build on Gautrain lessons learned – what worked and what didn’t 3. Stick with PPP but adapt the model 4. Partner with the best 5. Lead the economic development and public transport integration as a Province 6. Follow PFMA 7. Continue economic and socio economic development

Gautrain Lessons learnt • • Greenfields project risk vs Brownfields extension Theoretical vs actual data PPP Structure could do with some amendment GMA has excellent data on ridership, operations, Capex and Opex from Gautrain 1 Lower IRR’s should be applicable in future The Demand Modelling should be improved. Socio economic impacts are significant Public transport as a catalyst for economic change

Important drivers Project to be managed in such a manner that it is institutionally and commercially structured to attract interest, support and private sector participation

(What")

PPP Requirements • Feasibility – Value for money • Public Sector Comparator (PSC) (What will it cost if Government does the work through normal procurement process; and including completion and integration risk and cost) – Affordability – Total cost of project, expressed in Net Present Value (NPV) – Yearly cost to the province (contingent liability) – Maintain a prescribed ratio in social vs. . rest split in budget – Risk transfer • Identify, cost and allocate risks to the role players best equipped to mitigate and manage them

The PPP Feasibility study process

GAUTENG ON THE MOVE Feasibility Study Governance

The Challenge & Planning

External")

Transport Planning Major Interventions* or “do nothing”* Population Growth – (Number of workers) External Factors** Current – Status Quo 2016 Economic Growth – (type, location, labour requirements) Land-use Patterns – (Where will the People live) Enablers*** or “do nothing” Predicted – Future State 2037

1. Car growth and Congestion in Gauteng • 3, 9 million 2014 to 8, 6 million 2037 • Cars/1000 population Gauteng – 300/ 1000 (2014) to 450/1000 (2037) • Significant car growth • Congested road network Growth/congestion 800 600 450 300 160 SA general Gauteng 2014 Gauteng 2037 EU Cars per 1000 population US(cities)

2. Travel speeds without GRRIN 2025 • Existing road network is operating close to capacity • Current average network speed 41 km/h (peak and contra-peak directions) • Will reduce to 26 km/h in 2025 with an key road journey time 1 - 3 hours.

2. Travel speeds without GRRIN 2037 Peak Hour Road Traffic • Assume • • 1 000 km additional freeway capacity 1 500 km additional dual carriageway capacity • All road improvements currently planned are built • Average key road network speed reduces to 23 km/h (peak and contra-peak directions) spread over 3 hours • 10 km/h in peak hour if no peak spreading

4. Population Growth • Gauteng’s population is estimated to increase by 48% by 2037 Population 25, 000 19, 143, 438 20, 000 16, 797, 806 15, 000 12, 952, 631 10, 000 5, 000 0 2014 2025 Total Population 2037 Source: GRRIN Transport demand model : Land use projections from Metro land use data

")

Population (Potential Users 2025)

")

Jobs (all 2025)

Job Opportunities: 2037

“The Cost of Doing Nothing”

“The Cost of Doing Nothing” 2025 Demand on Base Year Network Base Year 7% 2037 Demand on Base Year Network 9% 9% 11% 23% 0 - 20 km/h 39% 48% 53% 20 - 40 km/h 30% 31% 22% 40 - 60 km/h 17% Source GITMP 25 > 60 km/h

Conclusions : ”The Cost of Doing Nothing” • Analysis of the transport situation in 25 -years’ time, shows that the consequences of “doing nothing” will be severe, i. e. if current trends continue • Vehicle population predicted to grow from 3. 9 mil. to 8. 6 mil. • Peak hour person trips to grow from 2. 0 mil. to 3. 2 mil. • Average peak hour road network speed will reduce from 41 km/h to 26 km/h in 2025 • Average peak hour road network speed will reduce from 41 km/h to 23 km/h in 2037 over a spread 3 hour peak • Congestion, with the transport network, the economy and the natural environment choking • Major interventions are required to avoid this scenario

Modelling a Future Network

Existing Rail in Gauteng & un-serviced areas Lanseria & Jhb NW Tshwane East Rand Mall / Midfield Terminal Un-serviced rail areas

Future Rail in Gauteng • Metrorail/PRASA • & Gautrain – Rail as the backbone of public transport • Integrated to BRT and Taxi

2")

Rapid Rail GRRIN interaction with other modes Passenger per hour Travel Distance (km) 2 000 4 000 6 000 8 000 10 000 12 000 14 000 16 000 18 000 20 000 30 000 40 000 10 20 30 Bus Minibus BRT 40 50 60 70 80 90 Monorail 150 900 Long Distance Commuter Metro Rail Tram Rapid Rail Commuter Metro Rail HIGH SPEED/ INTERCITY/ LONG DISTANCE RAIL

")

GRRIN Transport Demand Model DATA INPUT MODEL PROCESS DATA INPUT Census 2011 Landuse (2014) GITMP 25 Model Study Area & Zones GITMP 25, RISFSA, Capacity, Speeds Road & PT Network Census 2011 UPDATED TO 2014 Trip Generation HTS 2013 PT Routes Trip Distribution Road Network Generalised Costs Stated Preference Surveys Mode Choice Generalised Costs ACSA Data Road Network Speeds, Capacity, Costs Assignment PT Routes, Speeds, Capacity, Costs HTS 2013 Travel Time Surveys Calibration & Validation Traffic Counts PT Counts Routes, Timetables, Routes, PT Fares, Timetables, Patronage (Taxi, Bus, BRT, Rail, Capacity, Fares Gautrain)

Model meets")

GRRIN Transport Demand Model • • Model calibrated to international standards (UK) Model meets criteria for: – – – • Signed off by international reviewer – – • • • Traffic Flows; Traffic Screenlines & Cordons Journey Times; Trip Patterns; Passenger Flows High level of confidence in Car Traffic & Gautrain Other Public Transport adjusted and calibrated to counts and information available Road network was expanded based on Gauteng’s Strategic Road Network plans for 2025 and 2037 Gautrain bus headway to match train headways Park & Ride facilities at all new stations

Feasibility Progression Technical Summary Economic International Review Demand GRRIN Transport Demand model Demand Model Revenue Phasing Fare Box SED Financial Model Phasing Technical Phasing Routes, Stations, Capex, Opex & Costs Project Structure Funding Structure Risk Feasibility Study

The Routes and Phase

GRRIN full network Capex • Attached cost categories used • Over R 111 billion (Capex only) • Subject to funds availability • Phased over 25 years LAND ACQUISITION All land acquisition related to track, stations and depots MAINLINE RAILWAY Costs related to railway line infrastructure including related professional fees Project broken down into individual line elements RELOCATION SERVICES OF Relocation of services crossed by lines and stations STATIONS Station capital costs including access roads MOVABLE ASSETS Rolling stock and Buses OVERALL SYSTEM System elements such as signalling control systems and rolling stock DEPOT Depot costs O&M EQUIPMENT Track and rolling stock operations and maintenance equipment CLIENT AND PROFESSIONAL FEES Service fees related to either mainline railway and station elements as above or related to overall system components.

GRRIN Extensions Phasing Phase 1 MAMELODI LEGEND HAZELDEAN HATFIELD North – South Commuter TSHWANE EAST PRETORIA East – West Commuter IRENE Airport CENTURION Phase 1 SAMRAND Metrorail OLIEVENHOUTSBOSCH MIDRAND SUNNINGHILL RHODESFIELD LANSERIA O. R. TAMBO FOURWAYS MODDERFONTEIN COSMO LITTLE FALLS SANDTON RANDBURG MARLBORO EAST RAND MALL SANDTON 2 ROODEPOORT JABULANI ROSEBANK PARK BOKSBURG

Phase 2: Soweto link MAMELODI North – South Commuter East – West Commuter TSHWANE EAST PRETORIA IRENE Airport Service Metrorail integration Phase HAZELDEAN HATFIELD CENTURION SAMRAND OLIEVENHOUTSBOSCH MIDRAND RHODESFIELD SUNNINGHILL LANSERIA O. R. TAMBO FOURWAYS CRADLE MODDERFONTEIN COSMO SANDTON ROODEPOORT JABULANI MIDFIELD TERMINAL RANDBURG LITTLE FALLS MARLBORO SANDTON 2 EAST RAND MALL ROSEBANK PARK BOKSBURG

GRRIN Extensions: All Phases MAMELODI LEGEND HAZELDEAN HATFIELD North – South Commuter TSHWANE EAST PRETORIA East – West Commuter IRENE Airport CENTURION Phase 3 - 5 SAMRAND Metrorail OLIEVENHOUTSBOSCH MIDRAND RHODESFIELD SUNNINGHILL LANSERIA O. R. TAMBO FOURWAYS MODDERFONTEIN COSMO CRADLE SANDTON LITTLE FALLS ROODEPOORT JABULANI MIDFIELD TERMINAL RANDBURG ROSEBANK PARK MARLBORO EAST RAND MALL SANDTON 2 BOKSBURG

Why Phase 1? Freeway crossings Other road crossings • Highest transport model demand • Unserved by any rapid public transport (BRT) • Un-serviced by rail public transport mode • Congestion (see current google plot*) • Key connectivity challenges • Key economic nodes are located within the N 1/N 3/N 12 ring road • Links with Co. J development planning • Many high density residential nodes are located outside of the N 1/N 3/N 12 ring road • Limited freeway and road crossings in NW quadrant (12) • *Source: Google Maps (AM Peak Hour Traffic)

Socio-Economic Impact

Socio Economic Benefit potential of GRRIN • National Revenue: • • Job creation: • • • Total Jobs: Estimated over 200 000 jobs will be created. For every R 1 million of operational expenditure, 4 jobs will be sustained per year Maintenance & Operations: • • For every R 1 spent on operating the Gautrain, an additional 24 cents is added to the national government revenue For every R 1 spent on operating the Gautrain, the provincial economy gains 96 cents Rolling Stock • Industrialization through maintenance in SA

Socio-economic Impacts from the Extensions not often fully appreciated • • Decrease in road expansion and maintenance programs – Even if the introduction of the GRRIN has only the effect of postponing the roads programme, it means extra money in the pockets of tax payers. Concentrated development around railway stations – The establishment of a railway station has the effect of drawing businesses to establish around the station. This agglomeration leads to additional productivity, which ultimately leads to additional growth and development. Reduced risk of unforeseen delays on roads – Some road users will not use the train as a day-to-day form of commute, however it gives them an alternative opportunity to ensure that they reach a destination timeously. Increased perception of safety as opposed to road transport – Especially for women and children, the train ensures a safer transport environment when needed.

GRRIN Expected Benefits to Key Stakeholders Gauteng Province — Less traffic congestion — Carbon emission saving — Reduced accidents/fatalities — Job creation Commuters — Safe, reliable mode of public transport — Time saving — Carbon emission saving — Dedicated right of way

— Less")

GRRIN Expected Benefits to Key Stakeholders Local authorities (Surrounding GRRIN Station Nodes) — Less traffic congestion — Increased rates and taxes revenue, due to real increases in property prices — Increase in Local authorities “brand value” due to a the presence of a dependable public transport solution — Carbon emission saving — Transit Orientated Development (TOD), and economic growth Property Owners and Developers — Increase in property demand around GRRIN nodes — Increased value, densification and occupancy rates — Resultant capital and income gains from an increase in property demand Business Owners — Increased revenue from higher densities of customers close to GRRIN station nodes

Commercial Structuring & Funding

Gautrain I Contract Basis • Gautrain I - Single PPP contract – Train operations & maintenance – Rail infrastructure & maintenance – Rolling stock & maintenance. • Patronage guarantee to the Bombela Consortium based on a pre-agreed equity IRR return. • Patronage Guarantee based on the Greenfield nature of the project Gautrain Management Agency Government Funding: Patronage Guarantee Patronage guarantee Fully inclusive rail service Servicing of debt Equity providers Equity ≈ 2% Debt ≈ 10% Bombela Equity returns Train Operations Debt providers Infrastructure Rolling Stock Government Funding – Infrastructure ≈ 88%

Gautrain Funding Structure • The three spheres of Government ≈ 88% • National Do. RA: 48. 5% • Provincial MTEF: 21. 1% • Provincial Borrowings: 18. 6% • Remainder of CAPEX/Infrastructure funded through equity and debt ≈ 12% – Long-term Debt: 10% – Equity: 2% • Shortfall of Patronage Guarantee covered by Provincial MTEF funding Gautrain I Funding Split Equity, 2. 00% LT Debt, 10. 00% Provincial Borrowing, 18. 60% MTEF, 21. 10% Do. RA, [VALUE]

GRRIN Extensions Basis & Structure

Funding Structure – Default Option • The outcome of the GRRIN PPP feasibility study derived an anticipated infrastructure funding split: default funding infrastructure split – Government Capital contribution ≈ 67% • National Do. RA: 40% • Provincial MTEF Funding: 27% – Private Sector funding of ≈ 33% • Debt • Mezzanine Funding • Pure Equity • • This option does not consider additional ‘alternative’ funding sources that would further reduce the required government capital contribution Proportion of the government capital contribution possibly funded via ‘alternative’ sources of revenue Private Sector, 33% Provincial MTEF, 27% National Do. RA, 40%

Gautrain /GRRIN comparison • The accompanying chart quantifies the change from Gautrain to GRRIN funding sources on the project funding/financing split Private Sector, 12% Provincial MTEF, 40% National Do. RA, 49% Private Sector, 33% Provincial MTEF, 27% National Do. RA, 40%

Alternative Funding Analysis • Additional sources of Alternative funding were identified per the DBSA report (“Gauteng Rapid Rail Network Extension (GRRNE) Funding Options Analysis”) • The potential categories of “Alternative” revenue/funding are as follows: – – – – Tax Increment Financing (TIR) (New & existing stations) Special Rating Areas (SRA) (New & existing stations) Vehicle License Fee Airport Tax Sales Tax - VAT Property Asset and Management Agency (Property Development) Station Auctioning

Alternative Funding Analysis • The accompanying charts quantify the impact of ‘Alternative’ funding sources on the project funding/financing split default funding infrastructure split Private Sector, 33% Provincial MTEF, 27% National Do. RA, 40% alternative funding Infrastructure Split Provincial MTEF, 12% Alternative Funding, 38% National Do. RA, 17% Private Sector, 33%

Alternative Funding Analysis Alternative Funding - DBSA Report 4, 000 3, 500 3, 000 Station Auctioning PAMA (Property development) Sales Tax 2, 000 Airport Car License (Affected Munics) 1, 500 SRA TIF 1, 000 500 25 20 26 20 27 20 28 20 29 20 30 20 31 20 32 20 33 20 34 20 35 20 36 20 37 20 38 20 39 20 40 20 24 23 20 22 20 21 20 20 20 19 20 18 20 20 17 20 ZAR Real (RM) 2, 500

Alternative Funding Source TIF Existing Stations SRA Existing")

Alternative Funding Analysis (2017 – 2034) Alternative Funding Source TIF Existing Stations SRA Existing Stations Car License (Affected Munics) Airport Sales Tax Total Real (Rm) 579 1 157 4 379 23 424 454 PAMA (Property development) 2 116 Station Auctioning 1 930 Total 33 585 *Source: Table 6. 4 DBSA report converted to real 2016 figures

Conclusion

Conclusions • • The Gautrain has already contributed to some of the NDP milestones and will continue to be a major player in shaping the economy of Gauteng, more so if its network expands beyond the current capacity GRRIN can fulfill the criteria of a catalytic and transformative infrastructure project that would lift socio-economic development in the Gauteng region onto a higher, and more sustainable growth trajectory. GRRIN can facilitate Radical spatial, social and economic transformation in the GCR, thereby promoting a more equal society through better access to economic opportunities to benefit Gauteng’s residents GRRIN contributes to the Premier’s 10 pillar programme (See detailed slides as annexure if required)

• Feasibility Study – Project is technically, economically, financially")

Conclusions PPP Requirements (Phase 1) • Feasibility Study – Project is technically, economically, financially feasible as default option • Value for money – More viable Vf. M than Gautrain 1 due to experience, brownfield nature and lessons learnt – Risk adjusted PPP reference model (NPV) is lower than Risk adjusted PSC – Significant socio economic and economic impact (BCR, EIRR and SED figures) • Risk transfer – Operator PPP Revised project structure results in significant risk mitigation • Affordability – The project is affordable subject to the relevant funding being approved by government. – With alternative funding it is more affordable.

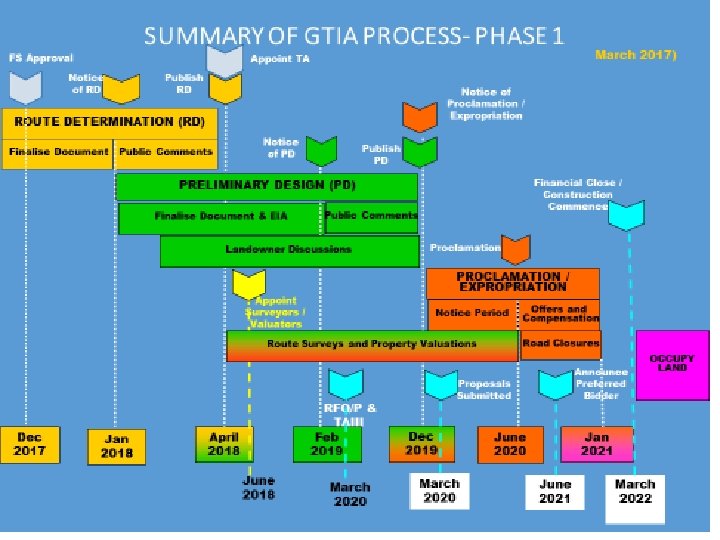

Way forward Pre construction activities • Various preparatory work packages required: – Appointment of the PIMO and the Procurement Transaction Advisors – RFQ, RFP development for Operator PPP – Baseline preliminary design, – geotechnical investigations, – land survey, – environmental authorisations(EIA) including heritage(HIA), – land proclamation and acquisition, – public participation and communications, – stakeholder engagement and – Civils contracts • A programme has been developed for all the different components.

Thank You Tshepo Kgobe Tshepok@gautrain. co. za www. gautrain. co. za

- Slides: 59