OIDD Technical Assistance Institute State Councils on Developmental

is a secure, online payment platform, developed by")

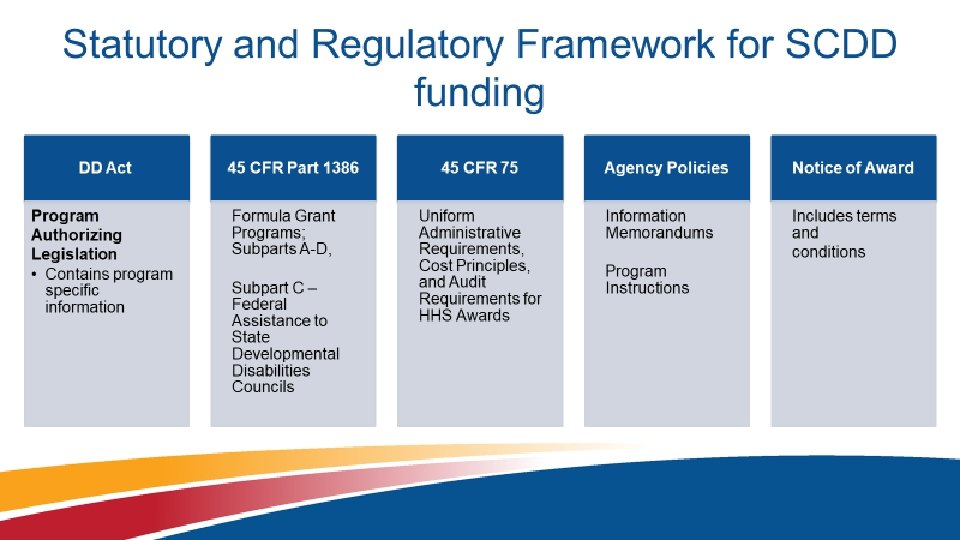

Statutory Requirements • Costs")

- Slides: 18

OIDD Technical Assistance Institute State Councils on Developmental Disabilities 1

Select topics for discussion • • • OGM Role and Primary Activities Review statutory/regulatory framework Match Budget Personnel documentation Federal reporting – SF-425 • Obligation/Liquidation – Broadly – COVID-19 Grant Flexibilities

OGM Role and Primary Activities To coordinate ACL's administration of grants and cooperative agreements Primary Activities include: • providing grants policy oversight; • ensuring compliance with statutory, regulatory, and administrative policy requirements; • and performing business review and cost/budget analysis for discretionary grants.

Match – topics to cover • Match Requirements • Calculating – Aggregate and Individual • Reporting – SF-425 – Detailed spreadsheet • Non-federal share – Cash – In-kind • How to determine the share 5

Non-federal share and aggregate • Councils should have a system in place to look at match at a project by project level in order to determine the overall match; – Councils must be able to look at match project by project with the appropriate required match to determine if there is match, overmatch, or undermatch • Councils have until the end of each project period to reach match; • Detailed documentation for each fiscal year must be provided when submitting the annual SF-425 6

Documenting and reporting match • 45 CFR 75, Subpart C, § 75. 306 – – Verifiable from non-Federal entity’s records Are not included as contributions for other Federal awards Are necessary and reasonable for the accomplish of project or program objectives Are allowable under subpart E • Internal documentation is needed to ensure match requirements are met. • Match is reported on the SF‐ 425. • A variety of methods are used by DD Councils to document match 7

PMS • PMS (Payment Management System) is a secure, online payment platform, developed by the PSC (Program Support Center) which provides awarding agencies and grant recipients/customers with grant payments, cash management, and grant accounting support services. • HHS Grant recipients use PMS to drawdown grant funds, and to report financial activity. • The PMS website is located at § https: //pms. psc. gov/ 8

PMS • Grant recipients are required to submit their financial reporting to PMS on a quarterly basis, using the Federal Cash Transaction Report (FCTR, SF 272). • As of April, 2020, grant recipients are required to submit their SF 425 (FFR) to PMS electronically, using PMS’ online FFR reporting system. • Online FFR reporting is required for all new grants awarded in FY 2020 and beyond. • For grant recipients who have received training on use of the online FFR system, training for use of the system is currently being provided by PSC. • Upon submission, the FFR must reconcile with the FCTR (SF 270) at the time that it’s entered; if there any mismatches or discrepancies, the reporting system will reject the FFR. This feature provides an additional layer of security, ensuring that the FFR and FCTR reconcile. 9

PMS • Representatives from HHS awarding agencies use PMS to verify a grant recipient’s financial activity (reported disbursements & drawdown of grant funds) and to reconcile the FFR (SF 425) with the PMS reporting (disbursements & drawdowns). • FFRs are reconciled using one of the following PMS Adhoc Inquiries: § Doc- E (Document Summary Extended) § This is a detailed inquiry report that displays authorization, disbursement, charged advance data for an individual grant or for all grants posted to a specific Payee Account Number. § FCO (Document Data w/FCO Segments) § This is an inquiry report that displays a grant award's authorization, disbursements, and charged advances at the fiscal year (FY), Common Accounting Number (CAN), and object class (OC) level. § FCO-E (Document Data w/FCO Segments Extended) § This is a more detailed version of the FCO. It includes an award's beginning and ending dates, and applicable subaccounts. In addition, a brief summary is included in the data output. 10

PMS • The reconciliation of the FFR with the PMS reporting is done by comparing the following entries from both reports to ensure that they match: § Line 10 d of the FFR against the Authorized amount from the PMS Inquiry report § Line 10 g of the FFR against § Snapshot disbursements for awards issued under a G account (Pooled Account) § Snapshot Charges for awards issued under a P Account (Sub-account) § Line 10 h of the FFR should amount to the difference between the Authorization column minus either the Snapshot Disbursement column or the Snapshot Charge column, depending on the type of account the grant was funded from (G or P). § If the differences do not match, the recipient must be informed of the discrepancy and they must revise their reporting. • The ACL GMS generates a copy of the online FFR to verify the reconciliation of the reporting. 11

Budgets • Councils must use not less than 70% of their funds for activities related to the State plan goals (direct costs). • Operational or “general management” costs cannot exceed 30% of the annual amount provided to the Council (indirect costs). 12

Council budgets State plan projects/activities Administrative budget (general management operations) Statutory Requirements • Costs that can be identified specifically with a particular subaward, project or program, service, or other organizational activity or that can be directly assigned to activities in the 5 year State plan with a high degree of accuracy. • Costs that support the Council as a whole; support multiple cost objectives • Examples: • Rent and utilities; Some staff salary and benefits; travel, supplies, liability insurance, • No less than 70% of the annual grant award can be spent on activities of the State plan; • No greater than 30% of the annual grant award can be spent on Administrative costs • - This includes the DSA reimbursement of 5% of the annual grant award or $50, 000 whichever is less 13

Direct vs. Indirect costs • Direct costs are those that can be easily and directly assigned to a state plan goal/objective activity. • Indirect costs are those that apply to more than one Council activity – Examples – Council meetings, Council member travel, rent, utilities, office supplies • 45 CFR 75; § 75. 412 14

Personnel expenses • Documentation is required – Council staff – Council grantees (if sub-recipient has personnel costs). • If Council staff are performing tasks Regulatory information: 45 CFR 75 § 75. 430 (i) Standards for documentation of personnel expenses 15

Staff Allocation documentation In general – personnel expenses must be based on records that accurately reflect the work performed. • Time and attendance or equivalent records for all employees. • Time distribution records for employees whose compensation is chargeable to more than cost objective (administrative and state plan activity). – Percentages from position audit or time study applied to timesheet or online payroll system – (coding to each area) § Not a slip of paper in a file drawer with the percentage noted Reference: 45 CFR 75 § 75. 430 (i) Standards for documentation of personnel expenses 16

Federal reporting • Where to submit SF-425 – FY 2020 shall be submitted in the Payment Management System (PMS) – FY 2019 – FY 2018 17

Questions and Comments 18