Off the balance sheet II SWAP Loan sales

Off the balance sheet II ØSWAP ØLoan sales ØSecuritization

Ø Currency SWAP Ø Interest rate")

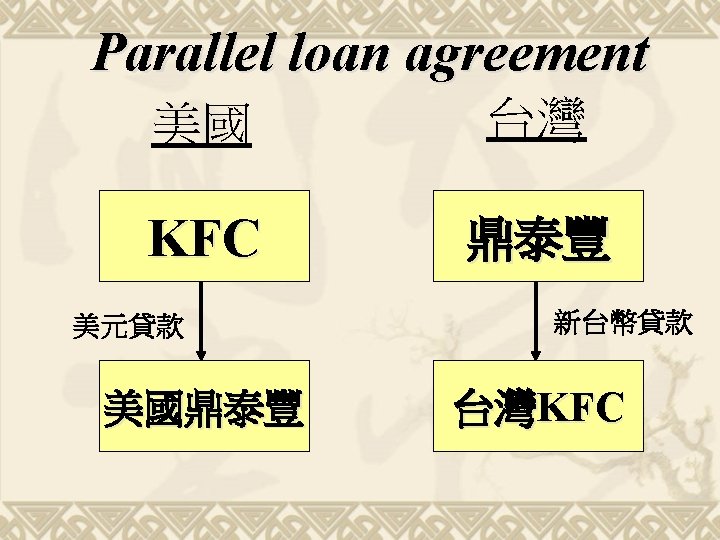

SWAP Ø Parallel loan agreement(back to back loan) Ø Currency SWAP Ø Interest rate SWAP Ø Basis SWAP Ø The optimal notional value of swap Ø Pricing an interest rate swap Ø Inverse floater swap

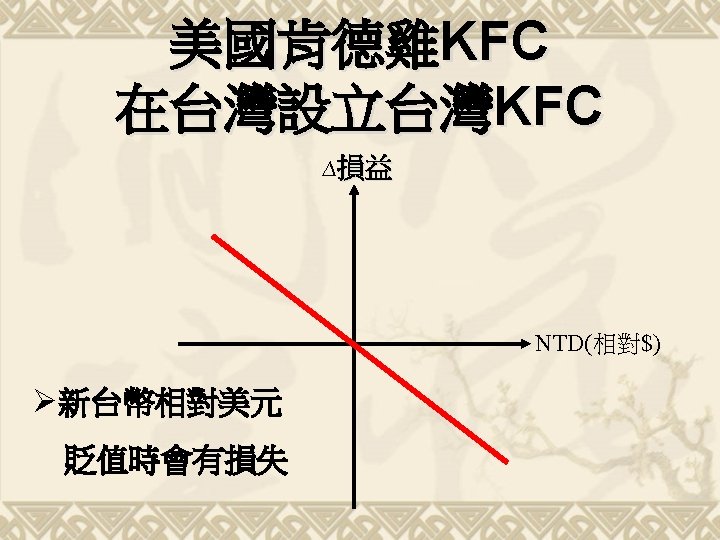

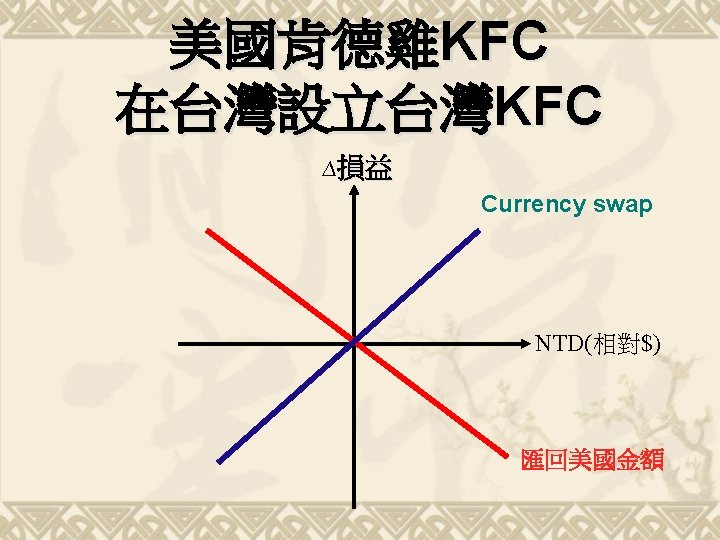

Currency swap A swap used to hedge against exchange rate risk from mismatched currencies on assets and liabilities.

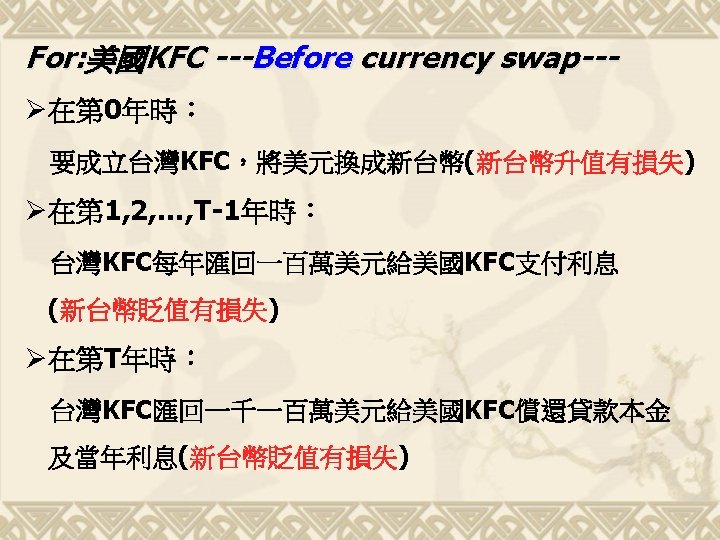

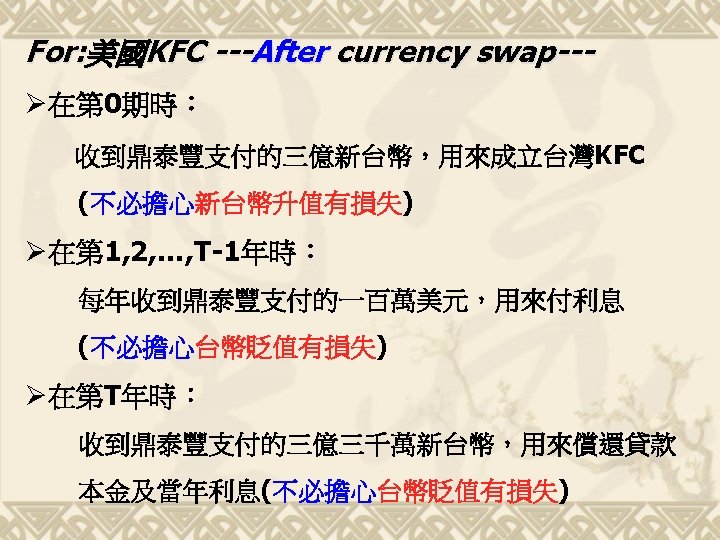

Currency swap 美國KFC NTD US US $1 m $1 m US $11 m 300 m US NTD $10 m 0 NTD NTD 30 m 30 m 1 2 3 台灣鼎泰豐 330 m T(year)

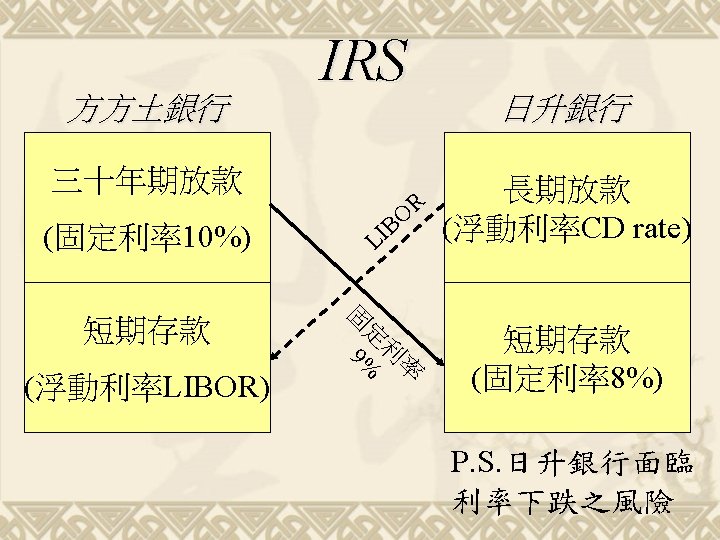

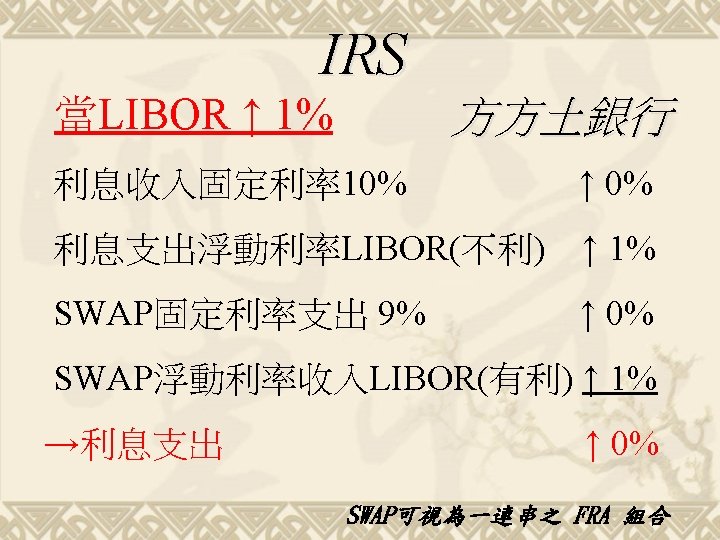

Interest rate SWAP An exchange of fixed interest payments for floating interest payments by two counterparties. 歐董來電!

Swap Basis swap 收 9% B/S 付 8% 日升銀行 付LIBOR 收LIBOR

Swap Basis swap B/S 付 8% 收 9% 日升銀行 付LIBOR 收CD rate ØCD rate – LIBOR = ?

Basis swap A swap in which both parties make payments at different floating rate.

+(LIBOR-CD)=0 歐董這麼做!")

Basis swap 收LIBOR 日升銀行 士心銀行 付CD 付LIBOR 收CD Ø(CD-LIBOR)+(LIBOR-CD)=0 歐董這麼做!

*A * ∆R/(1+R) ∆S=-(Dfixed –Dfloat)*NS *")

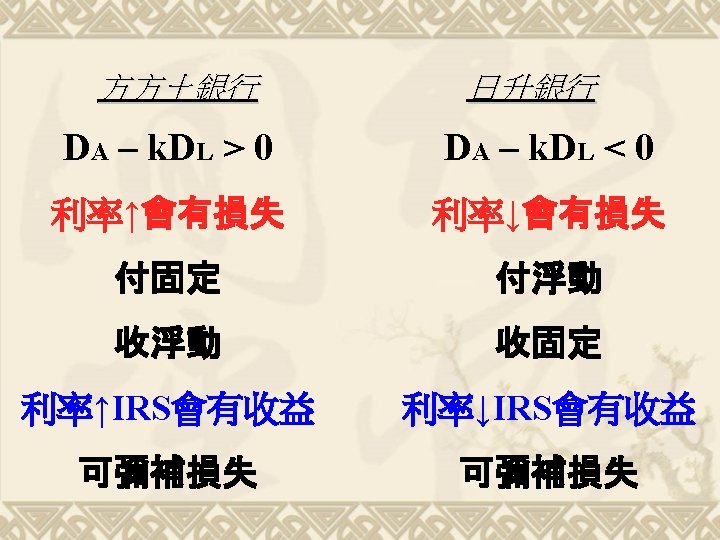

The optimal notional value of swap ∆E=-(DA –k. DL)*A * ∆R/(1+R) ∆S=-(Dfixed –Dfloat)*NS * ∆R/(1+R) Dfixed : 與swap具相同maturity, fixed coupon rate的政府債券之Duration Dfloat : 與swap具相同maturity, float coupon rate的政府債券之Duration 令∆S= ∆E 解得NS= (DA –k. DL)*A / (Dfixed –Dfloat)

The optimal notional value of swap ØEx: DA=5 , DL=3, k=0. 9, A=$100, 000 Dfixed =7, Dfloat=1 NS= (DA –k. DL)*A / (Dfixed –Dfloat) =$230, 000/(7 -1)=$38, 333 課本p 697

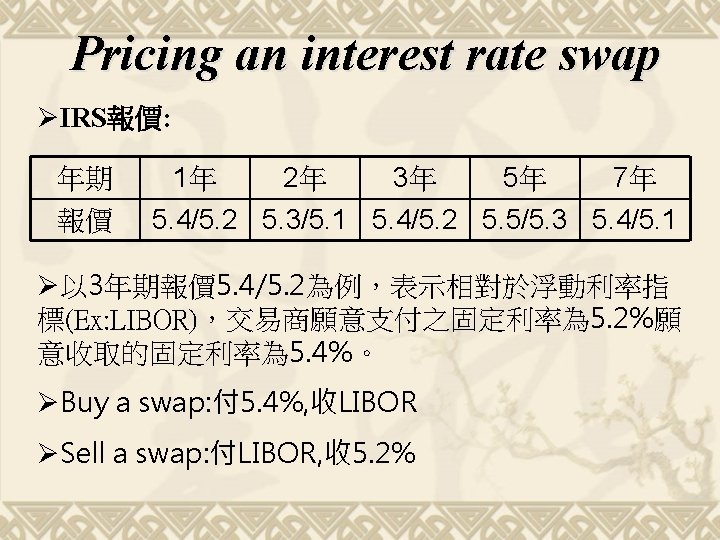

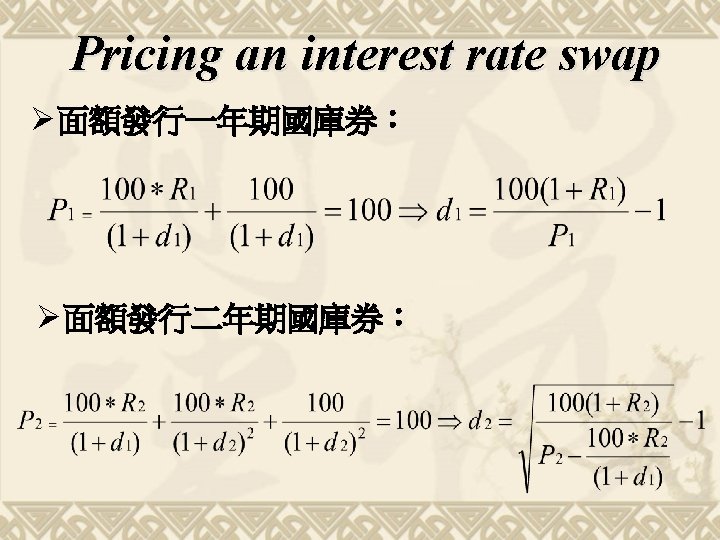

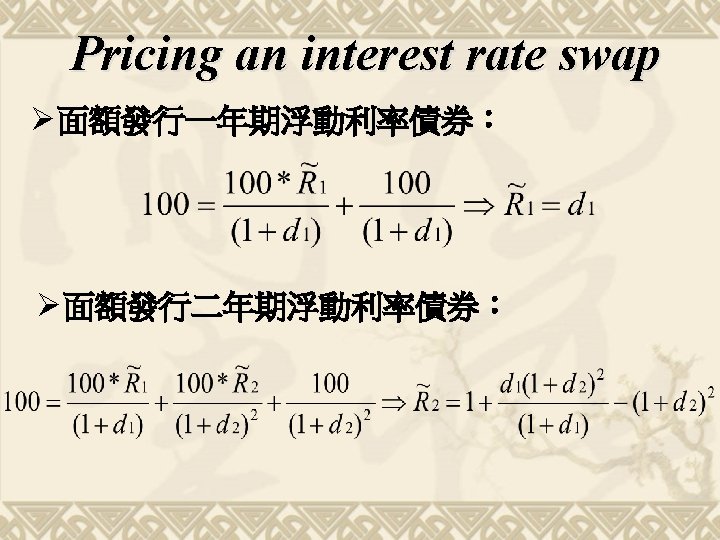

Pricing an interest rate swap ØNo-arbitrage condition: Expect fixed-payment PV = Expect floating-payment PV Ø則對一個名目本金為P,每期固定利率 、浮動利率 , n 期,各期折現率di 之IRS可用下式表示:

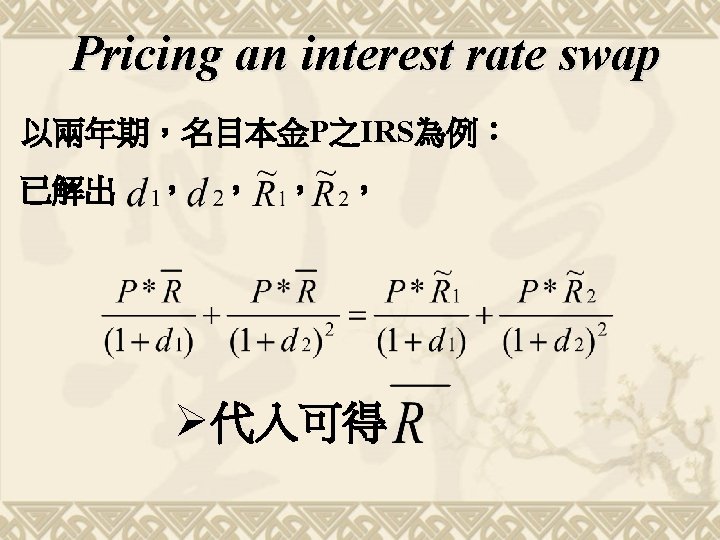

Pricing an interest rate swap Ø 以兩年期,名目本金P之IRS為例: Expect fixed-payment PV = Expect floating-payment PV Ø如何求得 ?

")

Pricing an interest rate swap 面額發行國庫券利率 R 2 R 1 1 2 到期期間(年)

Inverse floater swap Fixed-rate bond Floating-rate bond Inverse floating-rate bond Ex: 10 -year 15% bond ($100 million) Floater coupon: reference rate + 1%($100 M) Inverse floating coupon: 14% - reference rate ($100 M)

Inverse floater swap Swap FI Dealer 7%-LIBOR Note coupon Government Agency 7%-LIBOR Investor LIBOR Ø由面對利率下降之風險 面對利率上升之風險? Ø預期利率下降? Ø發行100 M逆浮動債券, 同時進行50 M之inverse floater swap Ø -100*(7%-LIBOR)+50*(7%-LIBOR)-50*LIBOR=50*7% Ø每期票息等於發行100 M固定利率3. 5%之債券 =100*3. 5%

Loan sales

Loan sales p Sale of a loan originated by an FI with or without recourse to an outside buyer.

Note:A FI Shorts a put when selling Loan Sales with recourse.

Types of Loan Sales v Traditional Short Term v HLT Loan Sales

Traditional Short Term v Secured by assets of the borrowing firm. v Made to investment grade borrower or better. v Issued for a short term (90 days or less). v Yields closely tied to a commercial paper rate. v Sold in units of $1 million and up.

. v They are secured by")

HLT Loan Sales v They are term loans (TLs). v They are secured by assets of the borrowing firm (usually given senior secured status). v They have a long maturity. v They have floating rates tied to LIBOR. v They have strong covenant protection.

Types of Loan Sale Contracts v v Participations: Buying a share in a loan syndication with limited, contractual control and rights over the barrower. Assignments: Buying a share in a loan syndication with some contractual control and rights over the borrower.

The buyers of Loan Sales v Investment Banks v Vulture Funds v Other Domestic Banks v Foreign Banks v Insurance companies and Pension Funds v Closed- and Open-End Bank Loan Mutual Funds v Nonfinancial Corporations

The sellers of Loan Sales v Major Money Center Banks v Good Bank - Bad Banks v Foreign Banks v Investment Banks v The U. S. Government and its Agencies

Why Banks and Other FIs sell Loans v Reserve Requirements v Fee Income v Capital Costs v Liquidity Risk

Fee Income vs. Accrued Revenue

Factors Deterring Loan Sales Growth in the Future v Access to the Commercial Paper Market v Customer Relationship Effects v Legal Concerns

Factors Encouraging Loan Sales Growth in the Future BIS Capital Requirements v Market Value Accounting v Asset Brokerage and Loan Trading v Government Loan Sale v Credit Ratings v Purchase and Sale of Foreign Bank Loans v

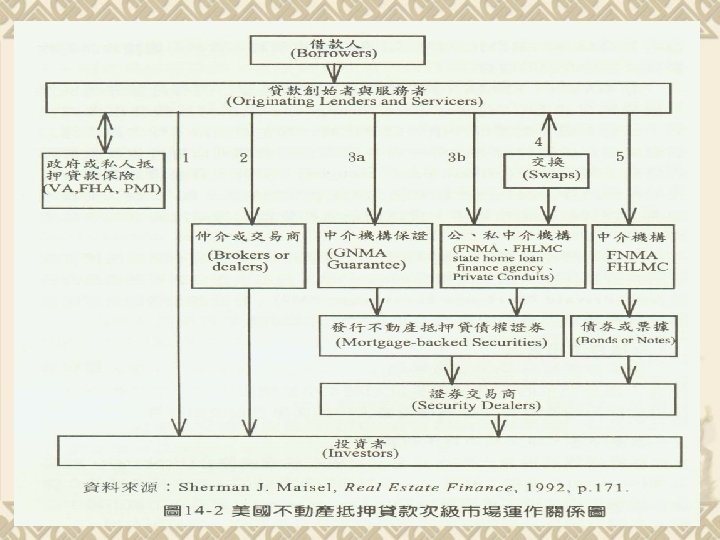

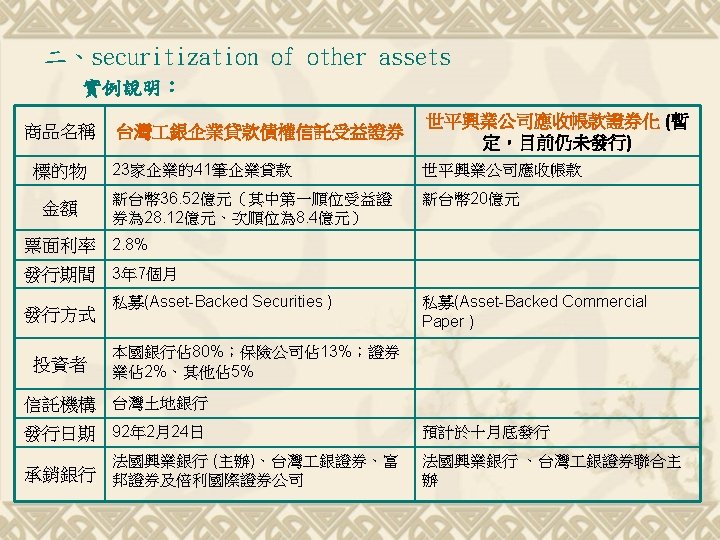

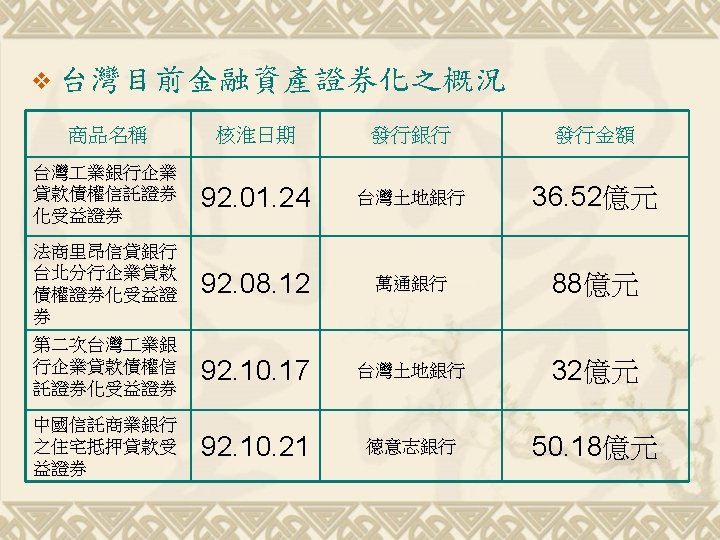

Securitization

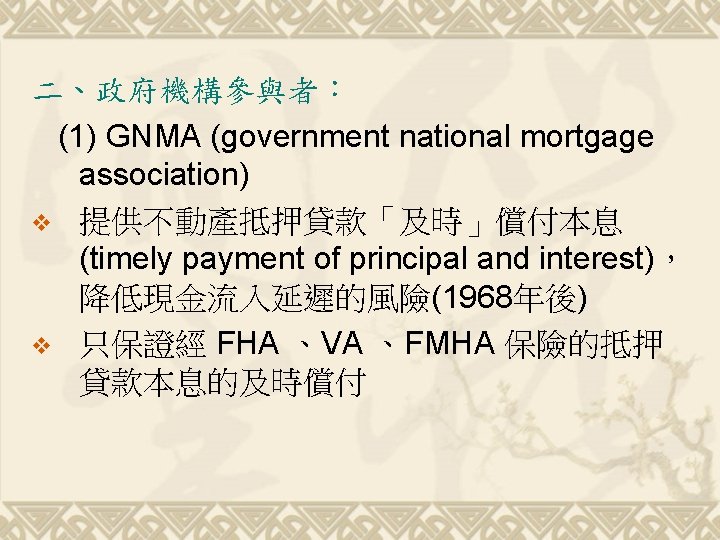

FNMA (federal national mortgage association) v 主動向銀行購買抵押貸款,來創造MBS v 提供及時償付本息的保證(80年代後) (3)FHLMC (federal home loan mortgage")

(2)FNMA (federal national mortgage association) v 主動向銀行購買抵押貸款,來創造MBS v 提供及時償付本息的保證(80年代後) (3)FHLMC (federal home loan mortgage corporation) v 對未經FHA 、VA 保險過的傳統貸款 (conventional loan)提供及時償付本息 v 其他業務與FNMA相同

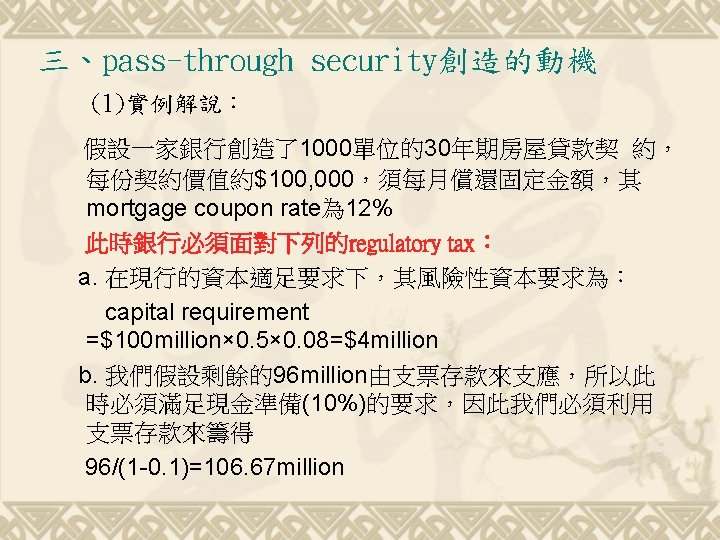

× 0. 0027=$288, 000 d. 結論: the bank with mortgage portfolio")

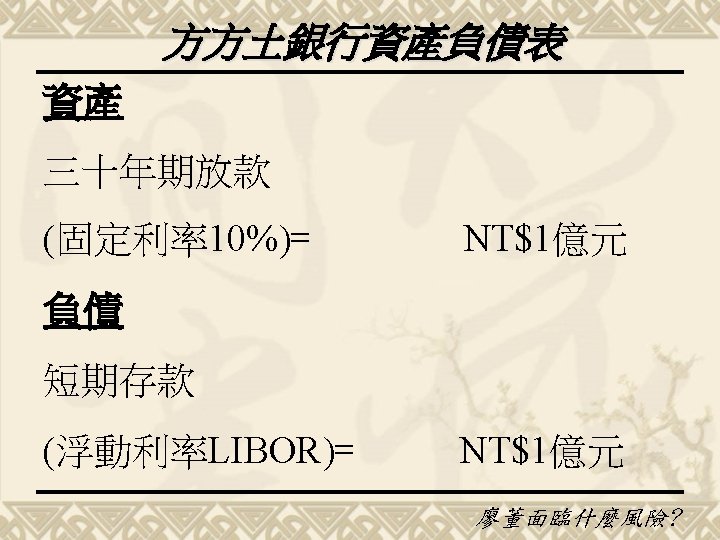

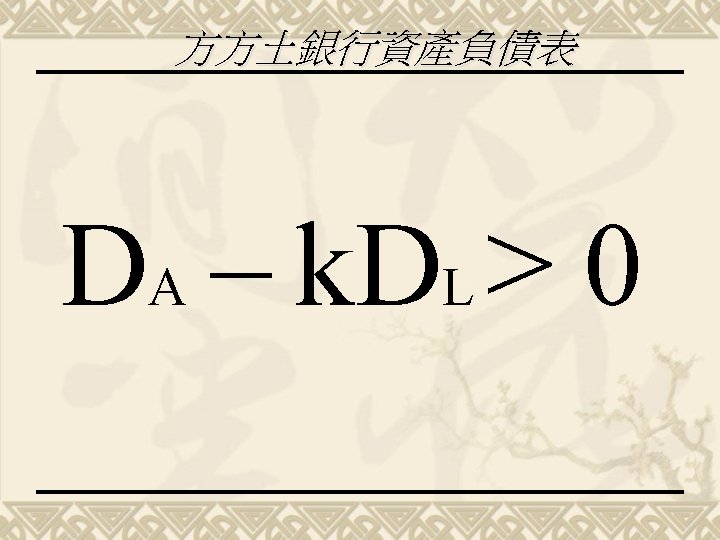

c. 存款保險費的支付 106. 67(m)× 0. 0027=$288, 000 d. 結論: the bank with mortgage portfolio faces three level of regulatory taxes: capital requirement reserve requirement FDIC insurance premium (2)持有mortgage portfolio的risk exposure a. gap exposure (or D A>k × D L) b. illiquidity exposure

消除風險的方法: a. lengthen the bank’s on-balance-sheet liability by issuing longer-term deposits or other liability")

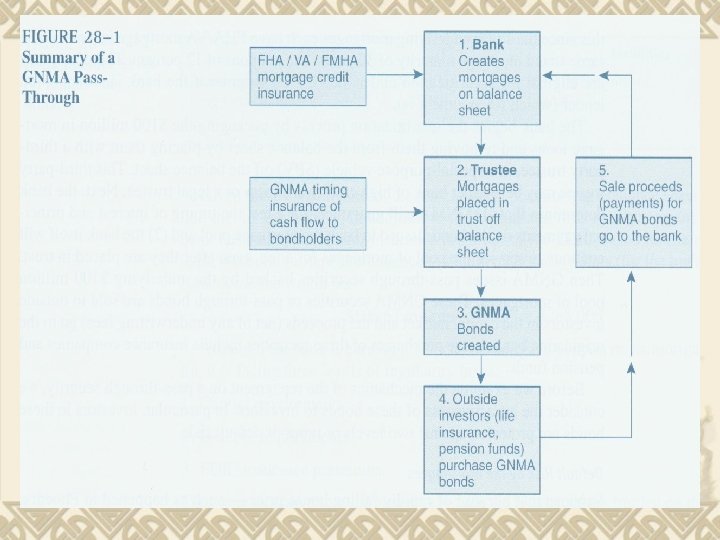

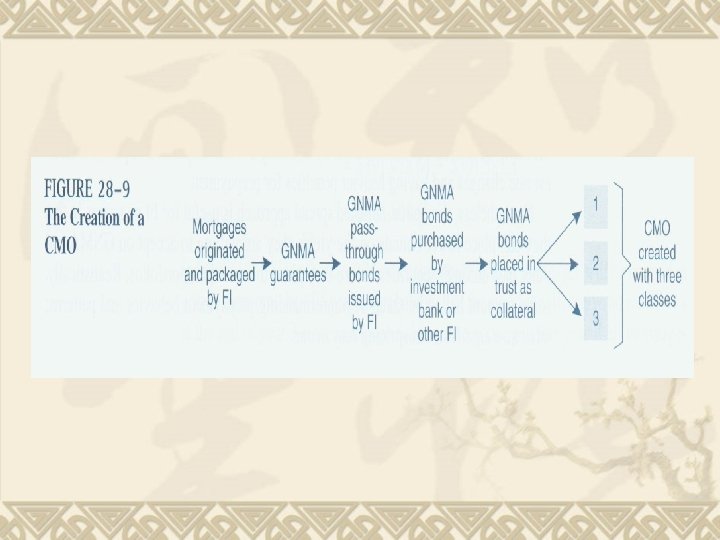

(3)消除風險的方法: a. lengthen the bank’s on-balance-sheet liability by issuing longer-term deposits or other liability claims b. engage in interest rate swap to transform the bank’s liabilities into those of a long-term , fixed-rate nature. c. creating GNMA pass-through securities 四、創造pass-through security的過程 GNMA將保證利息與本金按時支付給投資人 銀行仍將對房屋貸款者提供服務,以賺取手續費

五、使用pass-through security對FI的影響 Prior to use of pass-through security Asset Cash reserves Long –term mortgages $10. 67 100. 00 Liability Demand deposits Capital $110. 67 After use of pass-through security Asset Cash reserves $10. 67 Cash proceeds from mortgage securitization 100. 00 $110. 67 Liability Demand deposits Capital $106. 67 4. 00 $110. 67

default risk by mortgagers (2) default risk by bank 七、pass-through security的實際報酬 Mortgage")

六、對投資人的吸引力 (1) default risk by mortgagers (2) default risk by bank 七、pass-through security的實際報酬 Mortgage coupon rate =12% Minus Serving fees =0. 44 Minus GNMA insurance fee =0. 06 GNMA pass-through bond coupon =11. 5%

八、證券化對金融機構的意義 asset transformer asset broker interest spread dependent fees dependent 九、Prepayment Risk on pass-through securities (1)風險來源: 1. refinancing 2. housing turnover (2) Good news effects (3) Bad news effects

PSA model 在此PSA假設第一個月的prepayment rate為 0. 2%,之後 的29個月每個月遞增 0. 2%,直到annualized prepayment rate達到")

十、prepayment models (1) PSA model 在此PSA假設第一個月的prepayment rate為 0. 2%,之後 的29個月每個月遞增 0. 2%,直到annualized prepayment rate達到 6%,且之後每個月的prepayment rate皆為 6%

empirical models (3) option model PGNMA= PTBOND- PPREPAYMENT OPTION YGNMA= YTBOND- YPREPAYMENT OPTION 實例解說:")

(2)empirical models (3) option model PGNMA= PTBOND- PPREPAYMENT OPTION YGNMA= YTBOND- YPREPAYMENT OPTION 實例解說: The mortgage have a three –year maturity and pay principal and interest only once at the end of each year. The mortgage coupon rate is 10% on an outstanding pool of mortgages with an outstanding principal balance of $1, 000(current mortgage rate of 9%) 每月償付額=$402, 114

Assumption: Mortgager do not begin to prepay until mortgage rate , in any year, fall 3 percent or more below the mortgage coupon rate for the pool (10%) P=0. 125 11% P=0. 25 P=0. 125 10% P=0. 5 P=0. 25 12% 9% P=0. 25 10% 9% P=0. 25 8% 7% P=0. 125 8% P=0. 25 P=0. 125 6%

v v v end of year 1 interest payment =1, 000× 10%=$100, 000 principal payment =402, 114 -100, 000=302, 114 outstanding principal balance in the end of year 1 =1, 000 -302, 114=$697, 886 end of year 2 interest payment =697, 866× 10%=$69, 788. 6 principal payment =402, 114 -69, 788. 6=332, 325. 4 outstanding principal balance in the end of year 1 =697, 886 -332, 325. 4=$365, 560. 6 PMT + Principal balance outstanding at the end of year 2 =402, 114 + 365, 560. 6 = $767, 674. 6 CF 2=0. 25 × $767, 674. 6 +0. 75 × 402, 114 = $493, 504. 15 CF 3=0. 25 × 0 +0. 75 × 402, 114 = $301, 585. 5

v 如何計算OAS P = Price of GNMA d 1=discount rate on one-year, zero-coupon Treasury bonds d 2=discount rate on two-year, zero-coupon Treasury bonds d 3=discount rate on three-year, zero-coupon Treasury bonds OS=Option-adjusted spread on GNMA

v Assume that T-bond yield curve is flat, so that d 1= d 2 =d 3=8% Solving for OS, we find that: OS=0. 96% YGNMA=YTBOND+OS=8. 96% v OAS的用途 The OAS approach is useful for FI managers in that they can place lower bounds on the yields they are willing to accept on GNMA and other pass-through securities before they place them in their portfolios.

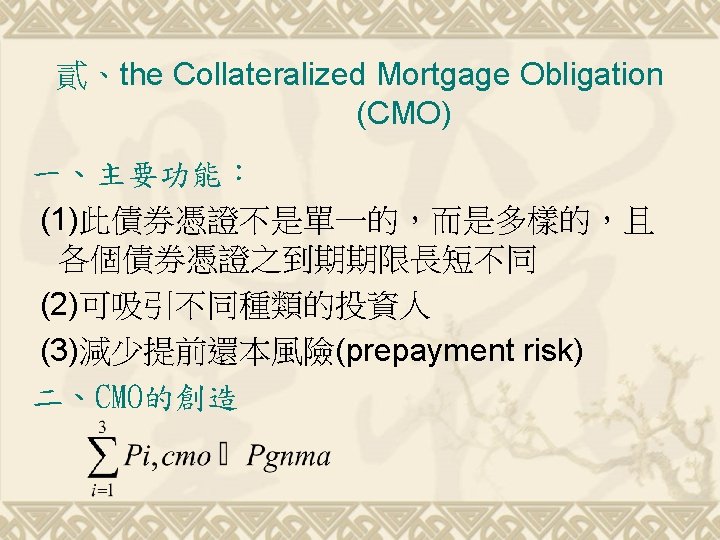

實例解說 Suppose an investment bank buys a $150 million issue of GNMAs and places them in trust as collateral. It then issues a CMO with these three classes: v v v Class A: annual fixed coupon 7 percent , class size $50 million Class B: annual fixed coupon 8 percent , class size $50 million Class C: annual fixed coupon 9 percent , class size $50 million

三、class A、B、C bond buyers Class A Class B Class C 存續期間 1. 5 -3年 5 -7年 20年 投資者類型 Depository institution pension fund insurance company and pension fund 等級 項目 四、other CMO classes (1)class Z (2)class R

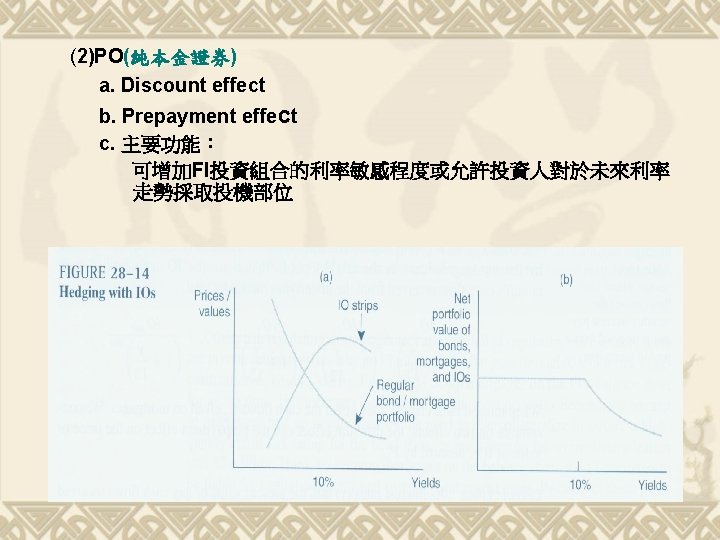

IO(純利息證券) a. Discount effect b. Prepayment effect")

肆、Innovation in securitization 一、Mortgage passthrough strips (1) IO(純利息證券) a. Discount effect b. Prepayment effect c. 主要功能: 由於其具有negative duration,故可做為一 般金融機構的良好避險 具,特別是持有一般 債券投資組合時

伍、can all assets be securitized 一、證券化的優缺點: Benefit Cost New funding source Cost of public/private credit risk insurance and guarantee Increases liquidity of FI loans Cost of over-cllateralization Enhanced ability to manage the duration gap Valuation and packaging costs If off balance sheet , the issuer saves on reserve requirements, deposit insurance premiums, and capital adequacy requirements

the relative degree of heterogeneity (2) credit quality of an asset type")

二、資產選擇證券化前須考慮的要點: (1) the relative degree of heterogeneity (2) credit quality of an asset type or group

p Scale and scope economic at large banks: Including offbalance sheet products and regulatory effects (1984 -1991)

requirements on bank")

Abstract This paper examines the impact of the risk-backed capital (RBC) requirements on bank cost efficiencies. It takes into consideration both on- and offbalance products and allow product mixes to differ across banks and to vary over time.

Technological")

Methodology p p p The Translog cost function. Expansion path scale economics. (EPSCE) Technological expansion path scale bias. (TECHEPB) Expansion path subadditivity. (EPSUB) Technological expansion path subadditivity bias. (TECHSUB)

Data It utilizes data from the quarterly Call Report over the period 1984 -1991. Sampled banks include the largest 120 banks in the u. s. After dropping those banks that merged with or were acquired by other banks during the period, its final sample includes 91 banks.

Empirical results p Large Banks EPSCE TECHEPB EPSUB TECHSUB Pre-RBC Announcement Implementation <1 <1 >1 insignificant >0 >0 <0 insignificant >0

Empirical results p Small Banks Pre-RBC Announcement Implementation EPSCE insignificant TECHEPB insignificant >0 >0 insignificant EPSUB TECHSUB

Conclusion v v v 規模經濟For large banks, after the RBC implementation, the index change from EPSCE<1(economies) to EPSCE>1(diseconomics), implying that large banks were too large to be efficient after the RBC implementation. 範疇經濟For large banks, after the RBC implementation, the index change from EPSUB>0(economies) to EPSUB<0(diseconomics), implying that large banks were too large to be efficient after the RBC implementation. Banks did not seem to have reduced production overall (particularly OBS products) in response to the regulatory tax imposed by the RBC requirements. This implies that the imposed regulatory tax may be too small. Another possible explanation to our results is that banks may in fact be revenue efficient rather than cost efficient

- Slides: 92