New UK Accounts Taxonomies Overview Peter Calvert XBRL

New UK Accounts Taxonomies - Overview Peter Calvert XBRL UK – ICAEW Seminar – 19 May 2014

Why new taxonomies? § New accounting regulations § Improvements in the light of experience § New requirements for XBRL tagging § New ownership and organisational structure behind the taxonomies

The new taxonomies § Full IFRS for UK companies § FRS 101 (reduced disclosure framework) § FRS 102 (Financial Reporting Standard for UK and Ireland) § Application of the standards § Similarities and differences

The development project § Development team under FRC auspices – Accounting specialists – Taxonomy developer and coordinator – FRC project manager § Technical infrastructure § Oversight: – Governance Committee; Technical Task Force; Closed User Group review § Timescales: March 2013 – Sept 2014

What happens next? § Public review of the taxonomies began on 8 May and will last for two months § Ends Tuesday, 8 July 2014 § Feedback via comment letter or via ‘Yeti’

What happens next? § Public review of the taxonomies began on 8 May and will last for two months § Ends Tuesday, 8 July 2014 § Feedback via comment letter or via ‘Yeti’ § Complete taxonomies in light of feedback § Release with supporting documents by or before September 2014 § Implementation

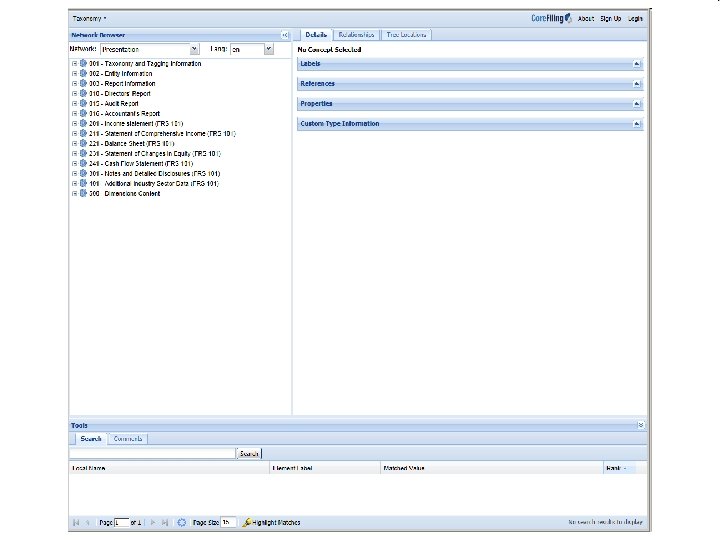

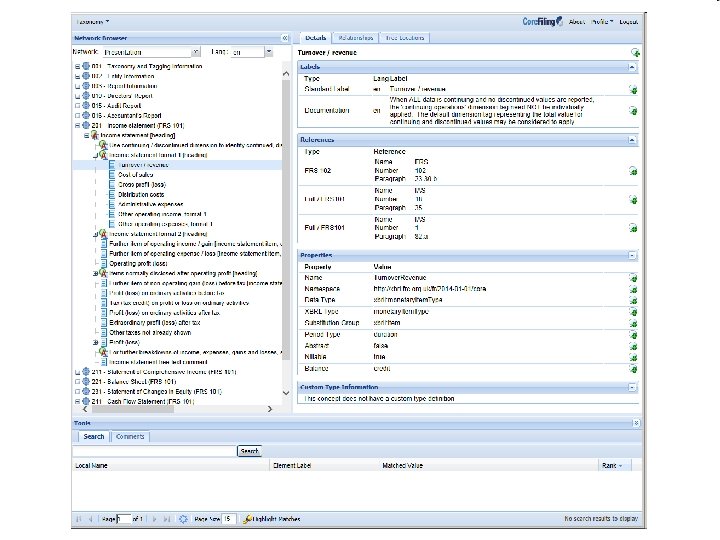

Aims and requirements § General aims: – Accurate, clear – Cover data which is useful for analysis, comparison and review by consumers – Easy and efficient to use – Provide unambiguous and consistent tagged data for consumers § Completeness requirement: – Financial data – Textual information

Broadening use of XBRL § HMRC: – Tax risk analysis, policy and planning § Government departments: – Policy, statistics and other purposes § Companies House: – Public and private consumers; investors; information companies; credit rating agencies; banks § Company financial info in digital format

Demands on taxonomies § Support more effective use of XBRL by a broader range of consumers § Support improved quality of tagging § Limit and ease the burden on preparer community § Meet the needs of 2016 and beyond Þ Range of design and content decisions

Main taxonomy features - 1 § Stability decision – Basic ‘look and feel’ and many features unchanged § Careful focus on content and user – Clarity of presentation and organisation – Consistency of approach § Built-in guidance – Guidance tags, cross-references, supporting information in ‘documentation’ labels § Accounting references

Main taxonomy features - 2 § Simplification of textual tagging § Greater use of dimensions, where appropriate § Introduction of ‘typed’ dimensions: – ‘Analysis’ items – Groupings – replacement of tuples § Covered in FRC Accounts Taxonomies Design document

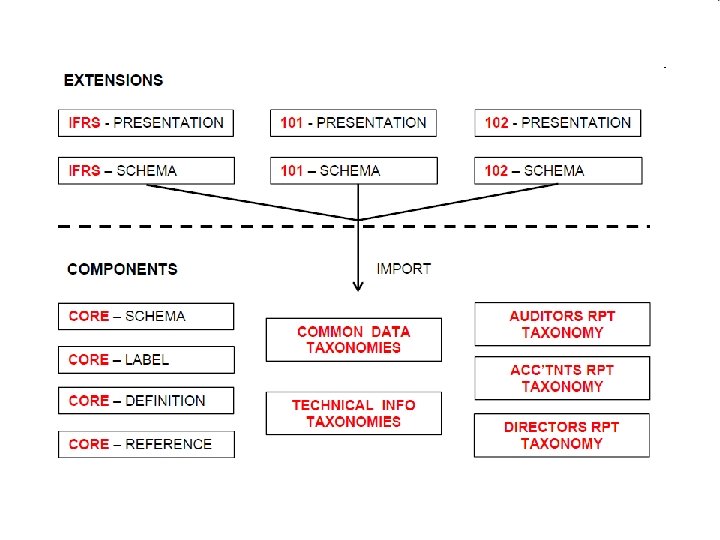

Structure of the taxonomies § Same underlying accounting base: IFRS published by IASB § Broad range of taxonomy content is the same across the accounting frameworks Þ Common ‘Core taxonomy’ Þ Extensions to core taxonomy to create individual taxonomies for Full IFRS, FRS 101 and FRS 102

Summary § § § § Reasons for new taxonomies General aims List of new features Timescales Providing feedback Next presentations Questions?

- Slides: 16