NATIVE AMERICAN INCOME What is this income Isnt

§ § § 70 years old, living alone Indicates he")

- Slides: 28

NATIVE AMERICAN INCOME

What is this income? Isn’t it all excluded? Some Native American/Alaska Natives receive funds from their tribes which may/may not be countable unearned income- examples: -Tribal casino/gaming money -Per capita/ dividends -General Assistance (GA) -Elder pay -Timber/mineral revenue

o t t a h w d n a s r o t a c i d n I ask

Each DHS application addresses Racial Heritage. This does not always mean that there is tribal income. However a good indicator that you should as a few questions. 539 A ERDC de 7476 415 F ERDC de 7470

Is there anywhere else on the applications to check?

415 F 539 A

What are some kinds of countable payments that Native American/Alaska Native receive? Elder Payments Per Capita General Assistance Gaming/Casino Dividends

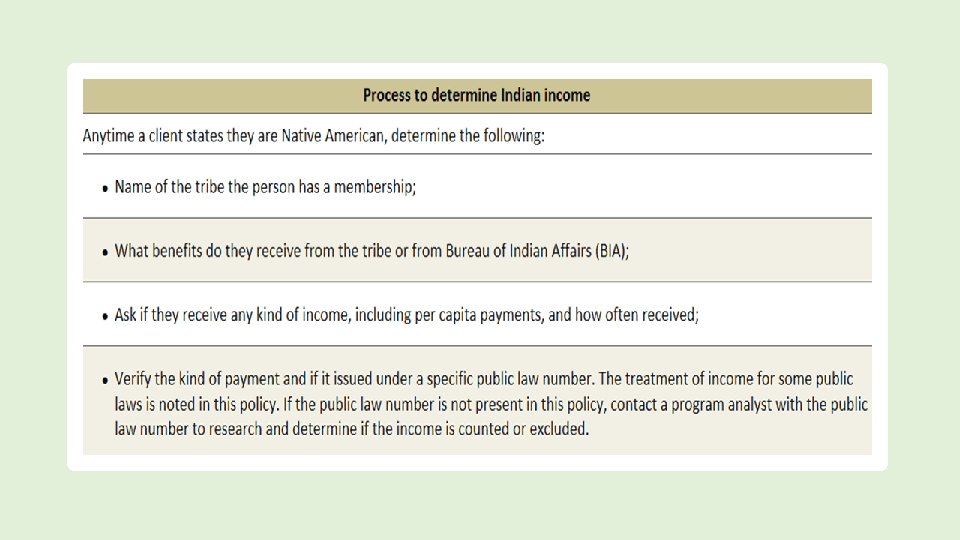

What is a public law? Also called public act, public statute. a law or statute of a general character that applies to the people of a whole state or nation. Many tribes or bands have received judgements or settlements under public law or a treaty with the United States.

PUBLIC LAW -Look to see if you can find the name of the tribe in Counting Client Assets. You will need to determine if the benefit received is covered under Public Law. Make sure to narrate the Public Law number. Most often this benefit is not countable, OR may only have that paid over $2000, countable, but your best practice is to make sure to check CCA #37 for how to treat the income with each program you are determining eligibility for--

For all programs, count as unearned income any payments distributed by the tribe or band, which is not excluded under public law. This can include profit share or per capita income from tribal casinos, timber sales or sale of oil reserves. Payments made to tribal members from these profits are counted if the income is anticipated to be recurring (monthly, quarterly, semi-annually or once a year). One time payments are nonrecurring and are counted as lump sum income (CA-A. 6). Treat recurring payments received less often than monthly as periodic income. (CA-A. 7).

EXAMPLES of Native American Benefits • Elder Pay/Pension • Monies paid to a person that is over a certain age (normally over 65). This income is a completely separate payment from any other tribal benefits and is paid at the discretion of the tribe with regards to amount and payment dates (monthly, quarterly, semi-annual, or annual). • Some tribes pay, while others do not, • Not to be confused with Old Age Assistance Claims Settlement Act payments

Old Age Assistance Claims Settlement Act Payments made under the Old Age Assistance Claims Settlement Act (P. L. 98‑ 500, Section 8) to heirs of deceased Indians are excluded except for per capita shares in excess of $2, 000. The first $2, 000 of each payment is excluded as income and as a resource. Count the remainder as lump sum income General Assistance ~ For all programs except SNAP, exclude Bureau of Indian Affairs (BIA) General Assistance program payments. Count as unearned income for SNAP. ~ Some tribes use tribal funds for general assistance programs. The payments received under general assistance programs funded by the tribe are counted as unearned income.

Per Capita Some per capita payments for timber or mineral sales may be counted while others are excluded. The tribal office will know if any part of the per capita payment was from lands held in trust. Gaming/ Casino Dividends These payments are not excluded under public law. Recurring payments received monthly, quarterly, semi-annually, or annually. Determine the last full years income and divide by 12 months to get monthly amount to count. NOTE- children that are eligible for these payments may have all or part deposited to a trust account. Contact the tribe issuing the payment to determine if the parent/guardian can access any part of the payment, and if the parent/guardian has done so. If the parent/guardian has accessed that portion available, that income is averaged per month and is considered countable income to that child.

Timber Sales, Oil/Mineral Reserves Payments for timber or mineral sales may be counted while others are excluded. They are excluded only if the sales are off lands held in trust by the Secretary of the Interior. The tribal office will know if any part of the per capita payment was from lands held in trust. Alaska Native Claim Settlement Act (ANCSA) The Alaska Native Claim Settlement Act (ANCSA) established Alaska Native claims to the land by transferring titles to 13 Alaska Native regional corporations and 200 local village corporations. ~ Exclude the value of stock, partnership interest, land or interest in land an interest in a settlement trust. ~ Exclude the first $2, 000 of each per capita payment per financial group member receiving such payment per year. ~ Count the amount over $2, 000 as lump sum income (CA-A. 6).

What can the worker use to verify this income? -stubs, statements from the tribe or BIA -tax statements/1099’s -the worker can contact the tribe

Is this verification enough?

SCENARIOS!

GABE- CAPI application § Single adult male § Living in Portland § Has income of $150 § Is native American/native Alaskan § Has no earnings (earned or unearned

Case Example : Gabe –

Notice the Race section is coded with ‘I’. This is another indicator to ask about Indian ‘Native American’ Benefits. Worker was able to gather information on Odd jobs as SEN during interview.

RAY- 539 a (APD) § § § 70 years old, living alone Indicates he is native American Getting SSB=$500/month Getting Tribal pension of $500/month Getting the tribal casino payments Has no verification with him

Charlie and Edith § Just moved to Oregon from Alaska § -both are US Citizens, Age 61 and unemployed § They are living with their son and his family § Charlie is receiving veterans benefits of $1500/month § Charlie is noted as Alaskan Native and Edith is Asian § Charlie states he is getting payments from Bristol Bay Native Corporation

Bristol Bay is one of the 13 major regional corporations established under the Alaska Native Claim Settlement Act (ANCSA) and is covered under Public Law #100 -241. The worker researches the manual and finds that under this PL, the first $2000 of each per capita payment per financial group member, per year, is excluded. The income is narrated, but it is not coded to the case, as it is under the $2000. Only the VET income is coded. $500 x 2 payments/year= $1000. 00, UNDER THE $2000 limit, no countable income.

Cathy and 4 children: • Cathy- Yakima enrolled: $125/month • Child One- CTUIR= all goes into a trust account • Child Two-Seminole= $6000/year • Child Three- native Hawaiian, no income • Child Four- Yakima = $125/month

Child Two-$6000/year income § Different sources of income and countable income: § $4000 goes into a trust account held by the tribe for the child from which she can not access until she is no longer a minor. § $1000 is paid to Cathy, but is covered under a Public Law and is not countable § $1000/year is from tribal casino gaming dividends and is paid directly to Cathy for the benefit of the child § Of all of this income, only the $1000/year of the casino dividends is countable to the child/household. § THE WORKER IS CALCULATES: $1000/12=$83. 34/MONTH AND CODES THIS TO THE CASE

Code the case with unearned income as follows: Cathy- IND $125/month Child Two- IND $83. 34/month Child Four- IND $125/month The other two children do not have any countable unearned income for SNAP.

Questions?