NAD Planned Giving and Trust Services Certification Course

• Established in 1862 by President Abraham Lincoln •")

- of the")

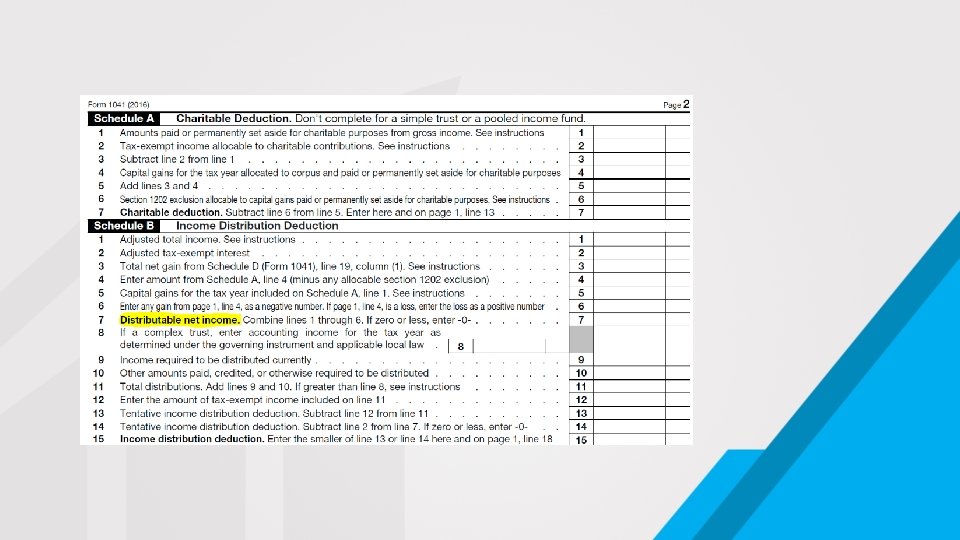

• DNI is a very important concept in trust taxation")

Deductions $ XXX • (Equals)")

- Slides: 31

NAD Planned Giving and Trust Services Certification Course Fiduciary Income Tax Reporting #1 May - 2017

Who is the IRS and why are they so important to you?

The Internal Revenue Service (IRS) • Established in 1862 by President Abraham Lincoln • IRS is an agency that operates under the US Department of the Treasury • Purpose: • To devise a method that captures any income, capital gains, and other revenue that’s earned or a cause of an event (i. e. when a person dies) • To enforce the tax code

Main tax forms the IRS will be looking for as it relates to income: 1040 – Individual Income Tax return 1041 – Federal Estate & Trust Tax return 5227 – Split-interest Trust Information Tax return 8283 – Non cash charitable contribution 8282 – Tattletale form 706 – Estate Tax return

State Tax Returns • Income tax returns • Estate tax returns • Inheritance tax returns * Call or go to your State Department of Revenue’s web site to determine what return/s need to be filed

There’s Always a Taxpayer • The personal representative (that’s the IRS term)- of the deceased person must file a personal income tax return for the year in which the settlor died. This person is responsible for distributing the settlor’s property • If no trust, the executor of the will distribute the property and pay the taxes. However, if there is a trust, and the incomes from the trust, the trustee will take over

There’s Always a Taxpayer • The trustee – is responsible for reporting income earned and paying the taxes. They are also responsible for distributing the property and closing the trust • The beneficiaries – usually file their own returns that includes inherited income from trust property earned • The Remaindermen – is the person who receives what’s left of the trust’s property when it ends

Example Jill is the successor trustee of her brother Joe’s living trust. He dies on March 10, 2015. She distributes all of the trust assets to the beneficiary, Joe’s son Jed, by December 31 of that year

You could be personally liable! • Taxes are paid out of the deceased person’s assets, unless you are the surviving spouse and are personally liable for the taxes due • If you: • Fail to file the tax returns required for the trust • Don’t pay the tax due for the trust • Fail to adequately investigate and determine how much tax the trust owes and distribute the trust’s assets even though you know that you haven’t paid all the tax due, • Could be personally liable for the trust tax bill, plus the penalties and interest

You could be personally liable! • Good news: Your liability is limited to the amount that would have been available to pay the tax, plus penalties and interest • Yes, you are on the hook for what the trust should have paid before the assets were distributed. • Forget or pay the tax late: • Interest accrues at 4% per year • Two different penalties may be imposed: • Failure to file – 5% charge of the tax due for each month the return is late, up to a max of 25% of the total • Failure to pay the tax -. 5% penalty for each month the tax isn’t paid - no maximum

Grantor v. Non-grantor Trust • The relationship of the grantor to the other individuals involved in the trust determines whether a trust is a grantor trust or a non-grantor trust • Grantor Trust • All revocable trusts are grantor trusts • Irrevocable trusts may be grantor trusts if: • Income is distributed to and administrated by the grantor • Reversionary interest of 5% or more of principal Example: If a grantor puts $100, 000 into an irrevocable trust, but the grantor retains the right to receive at least $5, 000 of that money back at some point in the future – Section 673 IRS code

Difference between a Grantor and Non-grantor trust • Grantor is usually the trustee and beneficiary over the trust’s income and principal • Retains certain powers over the trust administration • Power to revoke (amend or terminate) the trust • Keeps control over the property inside the trust • Items of the income and deduction are generally declared on the grantor’s income tax return • May not need a Tax Identification Number (TIN)

Non-grantor Trust • Grantor has given up all right, title, and interest in the principal • Only the trustee may revoke or terminate the trust • Grantor cannot be named as a trustee, beneficiary, or a remainderman • Grantor trust becomes non-grantor trust when grantor dies • Need a Tax Id Number (TIN) and file the 1041 every year the trust is open

Simple v. Complex Trust • Simple Trust • Is required to distribute all of its income currently • Does not provide for any income amount to be paid to, or set aside for, a charitable purpose • Does not have any amounts other than income paid out during the current year • Principal can not be distributed • May still be a simple trust if capital gains or losses are allotted to income under the governing instrument or local law

Simple v. Complex Trust • Is any trust that is not a simple trust or a grantor trust • Any year that the trust distributes principal is a complex trust • A trust may be a simple trust one year and a complex trust another Example: the trustee is required to pay out the interest and has discretion to pay out principal • A trust will never be a simple trust in the year in which it is closed, since the principal is distributed to close the trust • Estates are treated like complex trusts

Distributable Net Income (DNI) • DNI is a very important concept in trust taxation as it limits two important amounts: • DNI is the maximum amount of distributions to beneficiaries that the trust can deduct from its gross income • DNI is also the maximum amount of trust income that the beneficiaries must include in their gross income • Where there is more than one beneficiary, each will report his/her share of trust income, up to his/her pro rate share of the DNI • DNI is a concept that also applies to income taxation of estates • A trust will not include in DNI any extraordinary dividends or taxable stock dividends that are allocated to the principal

Calculating DNI • Gross Income $ XXX • (Minus) Deductions $ XXX • (Equals) $ XXX • (Plus) Personal Exemption $ XXX • (Plus) Distribution Deduction (May be the most important deduction) • (Plus) Net Capital Losses (unless charged to income) • (Plus) Net Tax Exempt Interest $ XXX • (Minus) Net Capital Gain (unless allocated to income) • (Equals) DNI $ XXX

Final Tax Returns • Personal representative needs to file the deceased person’s final 1040 tax return • Need to state “Deceased” with the date of death on the top of the form • Need to check “Final Return” • Income/expense should be included until date of death. • If you are the surviving spouse, you can still file this final return as married, filing jointly – “filing as surviving spouse” • If not required due to minimum income thresholds, it’s a good idea anyway as there may be a refund

Final Tax Returns • File IRS Form 56 to let the IRS know who you are – Trustee • It may require you to provide proof of your authority to act for the deceased person – such as a statement under oath that there’s no probate proceeding and that the trust is the beneficiary of the will • If prior year 1040 returns have not been filed, it is your job to file them. Remember, the IRS may hold you responsible for any taxes due

Final Tax Returns • Track all income before filing • W-2 - salary, interest, dividends, rental property income, royalties, profits from business, retirement distributions, pensions and tax refunds (Federal, State, and City) • For more information regarding IRS Taxes see – IRS Publication 17 • Due by April 15 of the year following the death – Pay Taxes! • If you are filing as the trustee, sign the last return yourself and write “filing as the Personal Representative for the Estate of _________, Deceased. ” • If you file an extension and you know that taxes will be due, estimate the taxes due and pay it!

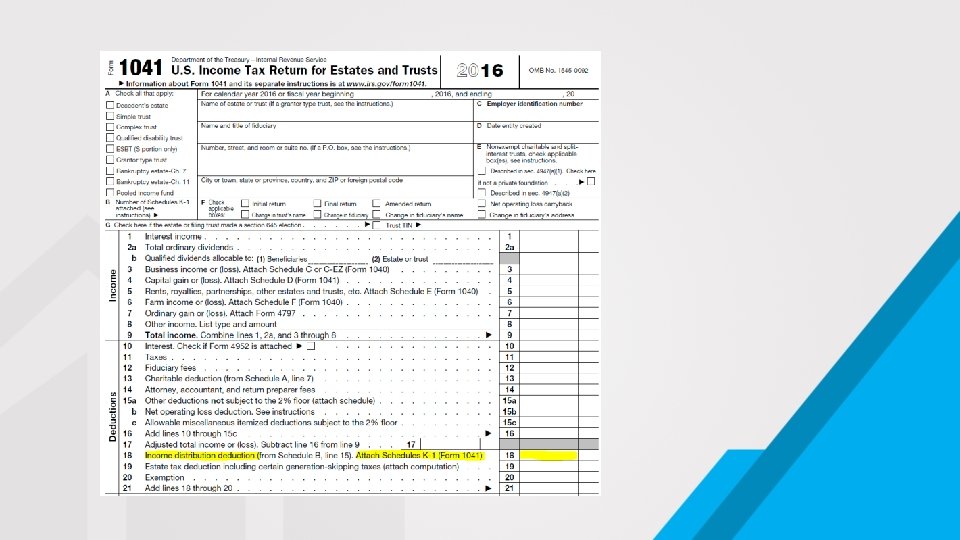

Estate or Trust Income Tax Return: IRS Form 1041 • Get expert help • If settlor’s estate or trust has gross income of more than $600, or any taxable income – you must file the 1041 • You can’t report trust/estate income under the deceased person’s Social Security number • Get a Taxpayer ID Number - Employer Identification Number (EIN)

Estate or Trust Income Tax Return: IRS Form 1041 • File IRS SS-4 form. • Example: xx-xxxxxxx (9 digits) • File date: April 15 – Pay taxes! • If you file an extension and you know that taxes will be due, estimate the taxes due and pay it! • For the first two years of trust administration, you aren’t required to file quarterly estimated taxes • After that, if trust earns more than $1, 000 in a year, you need to pay quarterly estimated taxes • If beneficiaries are to receive taxable income from the trust, IRS Section 6034 requires that beneficiaries be informed of any trust income that should be taxed to the beneficiary. • Send K-1 to beneficiary prior to April 15. Best practice: send K-1 by February 15

IRS likes consistency • Once you request an EIN Number, you have put the IRS on notice that an entity may have income • Once a 1041 has been filed, the IRS looks for it until you check the Final Return box • Even though in a particular year a trust does not have required income to file, it’s a good idea to file anyway as you may hear from the IRS

Example The Jane Simple Trust has investment income that requires the trustee to file a 1041 for the last five (5) years. In year 6, the investment income was only $300. Since the income was below the $600 gross income requirement, the trustee decided not to file the 1041.

Remember There May Be Other Taxes Due • Federal Estate Taxes – IRS Form 706 with estates over $5, 450, 000 (2016) that graduates due to inflation • State Income Taxes – Know your state or the state the trust/estate is in • State Estate Taxes • Inheritance Taxes • Real Estate taxes • Business taxes

Example On July 8, of year 7, the IRS writes a letter to the trustee asking why they didn’t receive the 1041 tax return. It is the trustee’s responsibility to respond to all IRS questions as the responsible party.

Example On August 5, of year 7, the trustee responds to the IRS that the trust only had income of $300 before the exemption deduction of $300 giving a zero ($0. 00) tax liability

Example On April 15, 2016, she files a form 1040 individual tax return for her brother, covering his income from January 1, 2015 until his death on March 10, 2015. She also files Form 1041, Income Tax Return for Estates and Trusts, to report the trust’s income from March 10, 2015 to December 31, 2015.

Example Once Jed owns the trust assets, he is responsible for paying tax on any income they produce