n n n Guarantee pension Income pension Premium

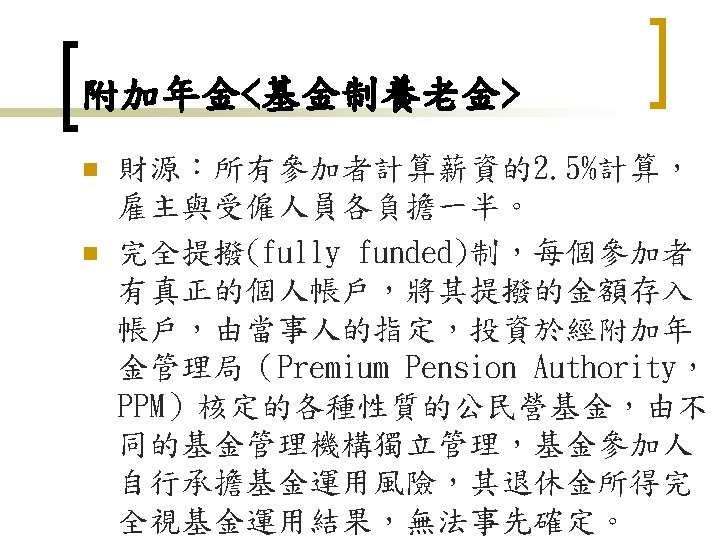

所得年金(Income pension) 附加年金 (Premium reserve pension) 職業年金 私人養老金")

保障私部門白領 階級勞 2. Occupational Pension Scheme for")

Population")

b. is fully funded and")

- Slides: 32

現行制度 n n n 保障年金(Guarantee pension) 所得年金(Income pension) 附加年金 (Premium reserve pension) 職業年金 私人養老金

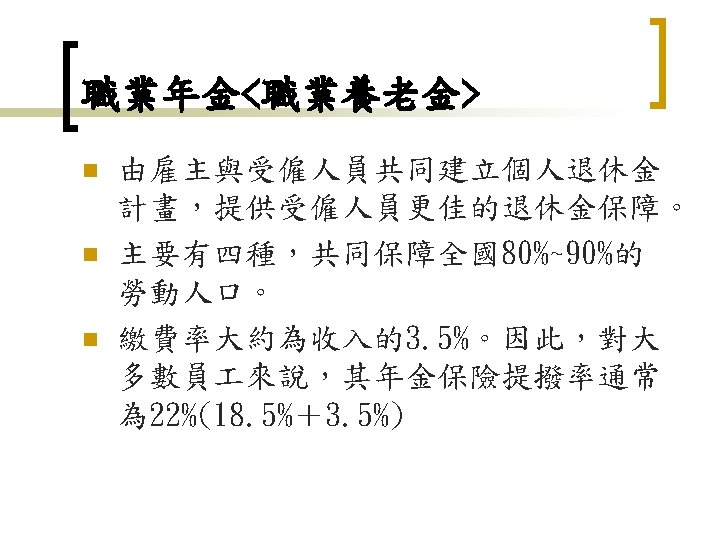

職業年金<職業養老金> 1. Occupational Pension Scheme for Whitecollar Employees(ITP)保障私部門白領 階級勞 2. Occupational Pension Scheme for Workers (STP)保障私部門藍領階級勞 3. Occupational Pension Scheme for Local Government Employees(KPA)保障縣市、 自治區等地方政府員 4. Occupational Pension Scheme for Central Government Employees(SPV)保障中央政 府公務員和其他省政府員

Replacement Rate 資料來源: PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES

Sources of Net Replacement Rate 資料來源: PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES

Tax n n EET:Exempt contributions, Exempt investment income and capital gains of the pension institution, Taxed benefits ETT:Exempt contributions, Taxed investment income and capital gains of the pension institution, Taxed benefits 資料來源: Economic Globalisation and Swedish Pensions

資料來源 n n n n 瑞典年金制度介紹 , 台灣老年學論壇第 4 期 , 2009 瑞典實施NDC年金制度之研究 , 行政院經建會 , 2010 我國退休基金管理制度之研究 , 行政院經建會 , 2010 Economic Globalisation and Swedish Pensions , Peter A. Diamond , 2009 PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES , OECD , 2011 The Swedish Pension Reform Model: Framework and Issues , Edward Palmer 瑞典國家統計局網站(http: //www. scb. se) http: //nordsoc. is/en/Sweden/

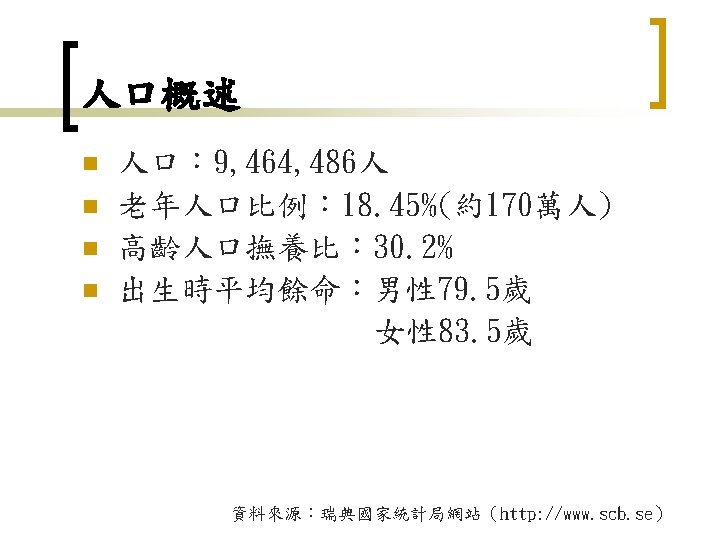

Indicators n n n Population : 5, 579, 204 (around 5. 6 million) Population over age 65 : 26. 8 % of working age population Life expectancy : 78. 3 at birth 82. 6 at age 65

Multi-pillar structure public pillar : social pension + ATP n second pillar: occupational pension plans + three supplementary pension schemes (part of ATP & LD ) n third pillar: voluntary personal pension plans n

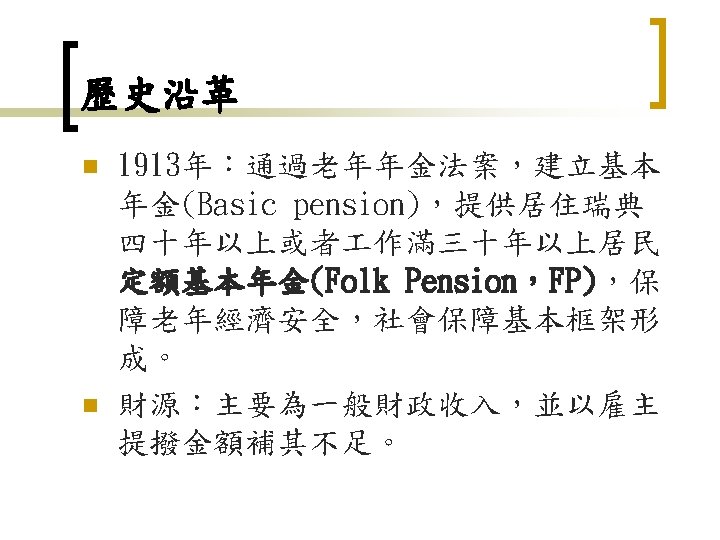

public pillar - social pension a. b. c. Legislation for people over 65. unfunded and financed from general tax revenues (pay-as-you-go) Public pension spending : 5. 6 % of GDP Flat benefits+ Earnings-related benefits Flat benefits: universal pension residency test &proportionality rule fraction of the years against 40 ≧ 40 years : full public old-age pension Earnings-related benefits: employment earnings test will be reduced by 30% if work income ≧ ¾ average wage + a supplement (income test is qualified , where income including ATP and occupational pensions)

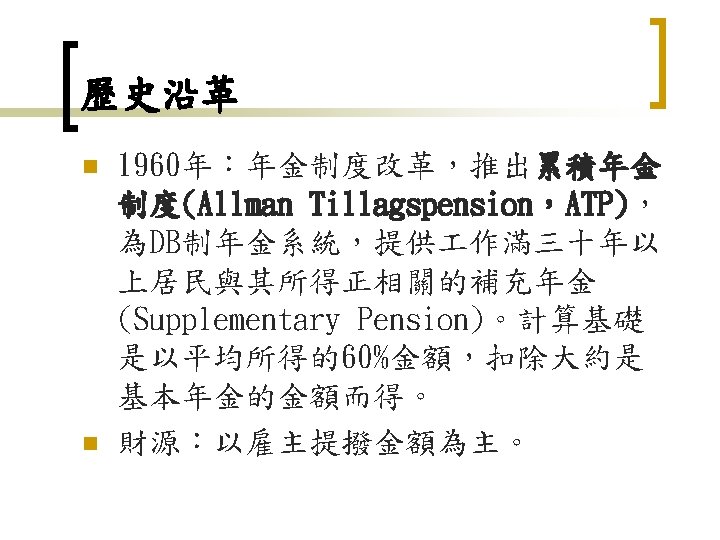

public pillar - ATP Labor Market Supplementary Pension (ATP) b. is fully funded and (a DC plan) contributions are split, with two-thirds paid by employer and onethird by employee (or the government for unemployed workers) c. Less than 0. 9 percent of the average wage (adjusted from time to time. ) it was established by law and entails social security features a.

ATP conti. d. The contribution is a fixed amount – as opposed to a percentage of income – varied only against the number of hours worked (have no income redistribution)

second pillar: occupational pension n n a. b. c. quasi-mandatory and nearly universal Because social pension scheme and ATP pay modest benefits, effectively imposed by collective labor agreements is not enacted a mandatory occupational pension pillar, but coverage is extensive and reaches almost 80 percent of the wage earners managed by (1)life insurance companies, (2)multiemployer pension funds and (3)corporate pension funds & (4)banks on a small scale

second pillar: d. e. majority DC plan On average, the contribution rate amounts to 15% of income with the employer contributing 2/3 of that rate source from : The World Bank Group & http: //www. pensionfundsonline. co. uk

second pillar: three supplementary pension schemes a. b. All are DC plans two of them are managed by ATP (SP & SUPP) the last is managed by LD Pensions (Employees Capital Fund) since 1980 aimed at adjusting cost of living increase lump sum

third pillar : voluntary personal pension plans Life insurance and pension companies banking institutions (1)Not offer annuity products (2) lump sums and phased withdrawals

n sources from : http: //www. socialprotection. eu/files_db/889/asisp_ANR 10_Denmark. pdf

Replacement Ratios n n n Less educated Skilled Highly educated The blue part is public pension and the pink part is private pension. Source: Ministry of Economic and Business Affairs (2003).

資料來源 n n http: //issuu. com/world. bank. publications/docs/ 9780821385739 (Annuities and Other Retirement Products published by world bank) http: //www. oecd. org/document/46/0, 3746, en_ 2649_34853_36091822_1_1, 00. html Pension Reforms in Denmark Peter Abrahamson & Cecilie Wehner Department of Sociology University of Copenhagen November 2003 Pension Institutions and Annuities in Denmark