Micro Small and Medium Enterprises Understanding Constraints to

Total Interest Income (1000 s, Pesos) Total Profits (1000")

- Slides: 49

Micro, Small and Medium Enterprises: Understanding Constraints to Growth Dean Karlan Yale University Innovations for Poverty Action M. I. T. Jameel Poverty Action Lab Financial Access Initiative

Analytical Framework �Three questions �What is the market failure? �Does a particular intervention help solve a market failure? �What is the welfare change?

Constraints to Growth �Subtitle: what are the market failures? �Information �Market relationships �Trust? Knowledge of networks? �Risk �Judicial processes �Credit (screening? enforcement? ) �Human capital �Managerial capital �Transaction costs (i. e. , price)

Impact Evaluation Design Themes 1. Search for the resource constraint �Nobody has unlimited money �Not everyone can get services �Two basic approaches: � If more eligible applicants than slots: � Randomize which get treatment � If program can service all eligible applicants: � Randomize information campaign to generate interest � Nice advantage: learn how to promote the program! 2. Answer questions for operations too �Not just impact of program versus nothing �Ideally, deliver lessons for how to improve a program

Access to Finance 1. Are there market failures (and what is the underlying mechanism? ) � Does expanding supply more credit? � First stage of credit impact studies � Does judicial reform lead to more contracts? � Does introduction of insurance increase investment?

What innovations solve market failures? � Microenterprise popular solution: Joint liability � Improved screening, monitoring, enforcement? � Training: Case study #1 � Small/medium enterprise: � Mentoring/consulting: Case study #2 � Market linkages: Case study #3 (agriculture) � Price: Case study #4 (price) � Credit scoring: Case study #5 � Embedded in these: What is the welfare improvement?

Outline �Five specific projects to describe �Business Training for Microentrepreneurs � Peru �Small/medium enterprise mentoring/consulting � Mexico �Market linkages for horticultural crops � Kenya �Price: expanding access to credit � South Africa and Mexico �Credit scoring to measure impact of loans � Philippines and South Africa

Peru Business Training: The Intervention �We add business training sessions to a microfinance group banking program in urban and rural areas in Peru �We worked with FINCA-Peru, a self-sustainable MFI � 12 years of experience promoting village banks for female microentrepreneurs in Ayacucho and Lima, Peru � 273 village banks � 6, 429 clients, 96 percent of which were women �Total savings: $1, 630, 823 �Loan portfolio: $821, 172

The Training � Two different set of materials for the two locations because of differences in literacy and language � Lima: Atinchik – spanish – written aids and homework � Ayacucho: Freedom from Hunger – quechua – visual aids � Two modules � Module 1: introduced attendees to what a business is, how a business works, and the marketplace (identify their customers, competitors, and the position of the business in the marketplace and then learned about product, promotional strategies and commercial planning) � Module 2: how to separate business and home finances, differences between income, costs, and profit, calculate production costs, and product pricing.

Experimental Design �Program had 300 village banks �Each village bank had about 20 women �Each village bank met weekly or monthly to make loan payments �All credit officers trained in how to deliver business training �Each credit officer handled 12 village banks. � 8 were assigned to treatment, randomly chosen � 4 were assigned to control, randomly chosen

Impacts �Weak evidence, but positive benefits for clients �Strongest result: business knowledge indices increased, and revenues in bad months increased �For microfinance institution: lowered default and increased client retention �Implication: cost effective, given very low cost �But much remains to be improved. �Results weak compared to incoming studies on mentoring/consulting

Mentoring/Consulting Project �Run by Mexican state government �Firms apply for grants for consultants/mentors from consulting firms in Puebla �Limited supply of grants for eligible firms �Thus randomization good for two reasons: � 1) Helped solve political problem, by choosing randomly no complaints of favoritism when allocating a scarce resource � 2) Provides powerful impact evaluation by independent researchers to help strengthen future policy discussions �Fairly small sample, 433 firms

Results �After one year �Monthly firm sales & profits up 78% and 110% respectively �Productivity increased �Productivity defined as profits unexplained by assets

DN Program • Drum. Net is an NGO that encourages the production of an export oriented crop through a cashless micro-credit program by linking directly commercial banks, smallholder farmers, retail providers and exporters. • Solves trust problems found in contract farming. • Information • Credit

Drum. Net Program • A farmer that wants to be a member of Drum. Net has to: – Be a member of a registered SHG. – Express an interest export crop French beans. – Have irrigated land. • Upon registration, Drum. Net members – Receive a 4 week orientation on Good Agricultural Practices and EUREPGAP requirements. – Open a personal savings account with local bank. – Make a cash contribution of USD 10 that will serve as collateral for a line of credit of up to 4 times that amount to purchase inputs (seeds and fertilizer).

Drum. Net Program • Farmers are organized into groups of 5 who are jointly liable for the loans taken out. • At harvest time, Drum. Net negotiates a price with the exporter and arranges for the produce pick-up at pre-specified collection points. • A transaction agent is appointed in each collection point to serve as liaison between Drum. Net and the farmers. • At these collection points, farmers grade their produce and package it, although exporter has the final word on the grading. • Once the produce is delivered to the exporter, the exporter pays Drum. Net who in turn deducts any loan repayment and credits the rest to the member bank account.

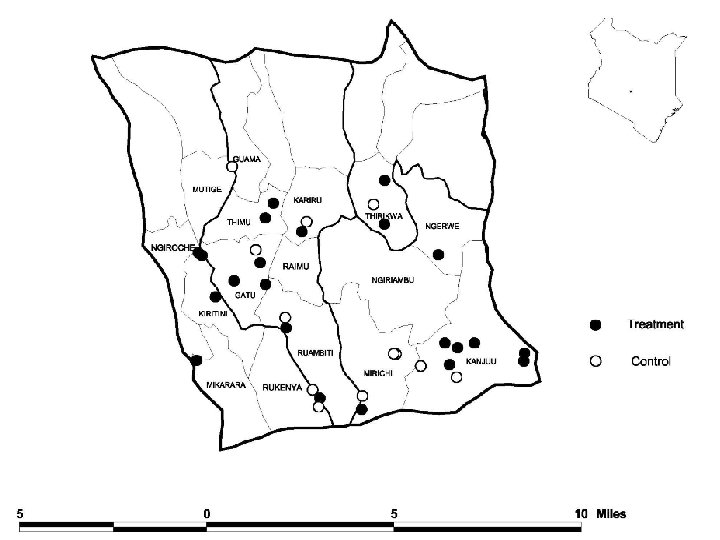

Experimental Design Location • Gichugu division in the Kirinyaga district. It was chosen because of its agroclimatic conditions (similar to original DN locations) and because the clustering of participants was feasible logistically. Sample Framework • • Original sample of 96 registered SHGs including disbanded groups. Run a “filter” survey to find out the status. Final sample of 36 SHG whose combined number of members reached the target Drum. Net capacity of 750 individuals (20 -40 members in a group). Randomization of SHGs • • • 12 got all services except for credit 12 got all services including credit 12 Control – All analysis will cluster standard errors within SHG

Experimental Design 36 SHG April 2004 June 2004 September 2004 Baseline Drum. Net starts Orientations Survey orientation of 24 finish SHG May 2005 Follow-up Survey

Demand Elasticities �Large-scale experiment in Mexico, Compartamos Bank �Randomized over branches spread throughout entire country �Incorporates general equilibrium effects

Price Huge variance in rates around the world Huge variance in depth of outreach Significant debate, especially in high rate countries Two sides to the calculation Costs Demand Most of the data/analysis/discussion is on costs For years, World Bank (CGAP) and others pushed to raise rates, to get to sustainability

Existing Evidence �First experimental study from South Africa � 58, 168 direct mail letters to prior clients �Most received lower rates, some higher �One time offer, with about one month window to apply

Direct Mail Example Letters �Add example of marketing letters here

Existing Evidence �Direct mail: �Limited exposure (i. e. , probably low ‘gossip’ to spread the word) �To those paying attention to mail � Note: high sensitivity to marketing on the same letters � Photo of a woman same effect on take-up as dropping the interest rate by 4. 3 percentage points �Not long term �Unlikely general equilbrium effects

Compartamos experiment �Key differences �Randomization at branch level �Data collected over 19 months �Two “take-up” sets of data � Specific face-to-face marketing � Natural over time process, i. e. , branch level outcomes with normal marketing, growth, gossip and general equilibrium effects

Experimental Design “Crédito Mujer” village banking loan product only for women Bank branches grouped into 80 geographic clusters across Mexico Half assigned “high” rate Half assigned “low” rate

Branch Locations “high” rate “low” rate Final sample included 132 branch offices in 80 geographic clusters across Mexico

Terms of the Loan Borrowers may already have a business or plan to start one Loans from 1, 000 to 20, 000 pesos (≈ $75 -$1500 USD). Average loan size 7, 365 pesos (≈ 550 USD). 16 weekly payments Group meetings and group liability

Interest Rates Offered "Low" Scenario Level Gold Silver Bronze q. Clients % of Clients Annualized 22% 27% 51% 62. 63% 72. 54% 82. 35% Flat Monthly 3. 0% 3. 5% 4. 0% assigned to one of three rate levels based on their borrower profile q“Low” scenario branches: approximately 10% lower annualized to clients with same profile "High" Scenario Annualized 72. 54% 82. 35% 91. 34% Flat Monthly 3. 5% 4. 0% 4. 5%

Data Sources Administrative Data: Compartamos’ client records Take up: Loan officers kept logs during direct loan promotion activities to report outcome of their efforts Competition: Branch managers of study branches were asked to report rates of their top three competitors Credit Bureau: Data report from Mexico’s largest Credit Bureau on municipalities served by study branches Government Loan Data: National Banking and Securities Commission report on lending data from financial entities in municipalities served by study branches

Results: More Clients 6000 Total Number of Clients per cluster per month 5000 4000 3000 2000 1000 0 Low Rate High Rate Total Clients

Results: Larger Loan Portfolio 40000 Total Loan Amount per cluster per month (1000 s, Pesos) 35000 30000 25000 20000 15000 10000 5000 0 Low Rate High Rate Total Loan Amount

All together for Compartamos �Compartamos is a for-profit �Impact on society important �Promise to investors of course is that helping society can be profitable. �Revenues increased by about 11% �Costs did too �Net impact on profits: up about 3% �Statistically same as before

Costs, Income, & Profit (1) Total Interest Income (1000 s, Pesos) Total Profits (1000 s, Pesos) 167. 094 (139. 784) 32. 070 (102. 520) Yes Yes 521. 216 80 1474. 239 80 953. 022 80 Total Costs Dependent Variable: (1000 s, Pesos) Panel A: December 2008 Report Low Interest Rate 94. 700** (46. 349) Quintile of Baseline Dependent Variable Mean of dependent variable for high interest rate cluster N

Pending issues �Clearly one parameter not right for the whole world �Key is to understand the heterogeneity �Competitive landscape �Returns to capital (discount rate) �Financial literacy �Disclosure policies and practices �Replication sites �Rural peru, urban Manila, urban Ghana, rural Philippines

Expanding Microenterprise Credit Access: Using Randomized Supply Decisions to Estimate the Impacts in Manila Dean S. Karlan Yale University Innovations for Poverty Action M. I. T. Jameel Poverty Action Lab Jonathan Zinman Dartmouth College Innovations for Poverty Action M. I. T. Jameel Poverty Action Lab

Motivation �Microcredit certainly a “big” idea in development policy �One key premise underlies the movement: � Credit market failures exist � Specifically, “microcredit”, by lowing transaction costs or removing information asymmetries, removes credit constraints for the poor �Countless key implications argued: � As credit constraints relaxed, impacts spread through all facets of business, consumption, health, education, etc. � Even on to informal institutions, trust, political participation, household bargaining, the list of “theories” goes on…. �Of course some argue this could be too much debt � Consumer disclosure issues � In USA…. debt is now the culprit, not the savior…

Experiments to measure impact �Impact studies of microcredit have been done �and done… �Questions linger regarding identification �Basic selection problems: �Who chooses to borrow? � Entrepreneurial spirit? Resourceful individuals? �Who do MFI’s agree to lend to? �Program placement: MFI’s target growing areas

Microcredit Randomized Trials � Now we are beginning to see a wave of them � South Africa: urban/peri-urban, for-profit, individual lending, formal sector employed individuals (Karlan and Zinman, 2008) � Philippines: urban Manila, for-profit, individual lending (Karlan and Zinman, 2009) � India: Spandana, urban Hyderabad, for-profit, group lending (Banerjee, Duflo, Glennerster and Kinnan, 2009) � Peru: Arariwa, rural, village banking, non-profit (Karlan and Zinman, 2010? ) � Mexico: Compartamos, peri-urban/urban, village banking, for-profit (Angelucci, Conley, Karlan and Zinman, 2011? ) � Morocco: Al-Amana, rural, village banking, non-profit (Crepon, Duflo and Pariente, 2010? ) � Philippines: FICO and First Valley (getting under way, 2012? ) � Bosnia: for-profit, individual liability, urban and rural (Augsburg, de Haas, Hamgart and Meghir, 2011? )

Simple but critical test �One theory: markets are actually complete. �High prices for informal credit �Incomplete credit markets? �Or higher price for better service? �Will increased loans higher debt or change in debt composition? �If so, prima facie evidence for credit constraints

Basic Methodology 1. Lender randomizes marginal loan applicants: 1 – 30 Auto reject 31 – 45 Randomly 46 – 59 Randomly approve 60% approve 85% 60 – 100 Auto approve 100 -point credit scorecard based on applicant’s: • Business capacity • Personal financial resources • Outside financial resources • Personal and business stability • Demographic characteristics

Basic Methodology 2. Follow-up with household survey that measures: • • Borrowing, broadly defined Business income, expenses, and profits Investments, broadly defined Psychological and political outlook Surveyors completed 1, 114 of 1, 601 in sample for 70% response rate. Number of days between treatment and follow-up: Mean Median Standard Dev. 411 378 76

Why did the bank do this? Weekly credit committees: slow, costly, subject to inconsistencies of subjective scoring. Computerized credit scoring fast (loan decision in 1 hour!) and quantitatively-based. Future scorecard revision requires data points on “below the line” applicants.

Market Settings Small-business Microloan market in Philippines: • • For-profit rural bank Regulated but no viable credit bureau Unsecured Individual liability High-risk Short-term (13 weeks), fixed repayments Expensive by many international standards (63% APR)

Results �Loan use increases: 9. 6% more likely to have a loan �Evidence of market failure being solved

Impacts �A lot of non-results �To address multiple outcome issues, we compute indices, and several are consistent and statistically significant. �Key results: �Profits go up for men, but not women (consistent with de Mel et al capital drop experiment in Sri Lanka) �Cut back in firm investments and cutback in formal insurance �Increased education for families of male borrowers �Increased access to informal credit �Increased trust in community �Increased stress (consistent finding in South Africa)

South Africa �Similar study �Consumer lending �Found increase in employment after getting a loan �Net impact: 8 percentage point reduction in poverty headcount ratio

Further research �What are patterns of impact? �When should credit be increased? �Who should lenders (and their funders) target? �Replication needed to further answer these questions. No one study can satisfy the policy questions being posed. �Need varying competitive settings �Need varying cultural and economic conditions.

Thank you! dean. karlan@yale. edu http: //karlan. yale. edu http: //www. poverty-action. org http: //www. povertyactionlab. org