MFF MIDTERM REVISION PROSPECTS FOR THE EU BUDGET

MFF MID-TERM REVISION PROSPECTS FOR THE EU BUDGET FOR THE SECOND HALF OFMFF Jacek Dominik European Parliament Committee on budgets Public hearing 17 March 2016

Article 2 -")

Outline • Review or Revision (article 2 of MFF Reg. ) Article 2 - Mid-term review/revision of the MFF By the end of 2016 at the latest, the Commission shall present a review of the functioning of the MFF taking full account of the economic situation at that time as well as the latest macroeconomic projections. This compulsory review shall, as appropriate, be accompanied by a legislative proposal for the revision of this Regulation in accordance with the procedures set out in the TFEU. Without prejudice to Article 7 of this Regulation, preallocated national envelopes shall not be reduced through such a revision • • Duration of MFF (5 or 5+5 or 7 years) Revenues Expenditures Backlog, RAL, Flexibility

Revenues • New OR – but the same ceiling • Can it solve the problem of the under-funding of the EU budget? • Bigger visibility for EU citizens – bigger support for the European integration? • Rabates – can we get rid of them by introducing genuine own resources?

Expenditures • Challenges: Ø Growth and jobs – Investments Ø Migrations Ø Security Ø Energy and Climate Ø etc • Tools Ø Financial instruments • MFF 2014 -2020: Ø Cellings (in comparison with 2007 -13) Ø Conditionalities Ø Cohesion policy

EUR billion, 2011 prices 150 140 130 Contingency margin 120 2015 revision 110 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Expenditures - Conditionalities Performance improvements in the new MFF 20142020: • Higher amounts in key growth and competitiveness areas • Multiple objectives: example climate mainstreaming • Higher leverage for EU money • Reinforced link to economic governance • Programme performance framework + performance reserve • Simplified delivery system

Financial Instruments In this MFF we can see shift from grant financing towards greater use of financial instruments There are natural constrains to go further along this path. Commission cannot be turned into the giant banker (this could crowed out private financial system). Financial instruments can be applied only to revenue generating projects. There are plenty of areas where the EU projects contribute to economic development or wider societal goals, for instance training to young unemployed, but where generating financial returns is impossible or impractical

Flexibility • We need increased room for maneuver but not at the expense of EU budget’s predictability and legal certainty • It’s been only 2 years since current MFF’s startup – it is too early for another rearrangement and transfers between budget headings • „Satelite instruments” outside EU budget (e. g. Turkey Facility) as a consequence of lack of appropriations and time constraints

Not sufficient payment appropriations in adopted budgets After temporary decline backlog in years 2015 -2017 is expected to mount up (from 2018) as a consequence of n+3 rule in Cohesion Policy Flexibility instruments (e. g. Contingency Margin) are already nearly fully exhausted

in Cohesion Policy The backlog of outstanding payment claims at")

Mainly (more than 90%) in Cohesion Policy The backlog of outstanding payment claims at year-end for the 2007 -2013 Cohesion Policy programmes (EUR billion) Amending Budgets (not only in Cohesion) 2012 -2014 ‚fresh money’ – more than 20 bln EUR: • 2012 – 7, 5 bln EUR • 2013 – 11, 2 bln EUR • 2014 – 3, 5 bln EUR

RAL After artificial decrease in RAL at the end of 2014, its level increased significantly in 2015 as a natural consequence of the full implementation of EUR 32 billion of differentiated commitment appropriations, either reprogrammed or carried over from 2014. In 2016, due to a difference of over EUR 10 billion between budgeted commitment and payment appropriations, a further increase of RAL is expected.

RAL • RAL end of 2003 – 102 bln EUR

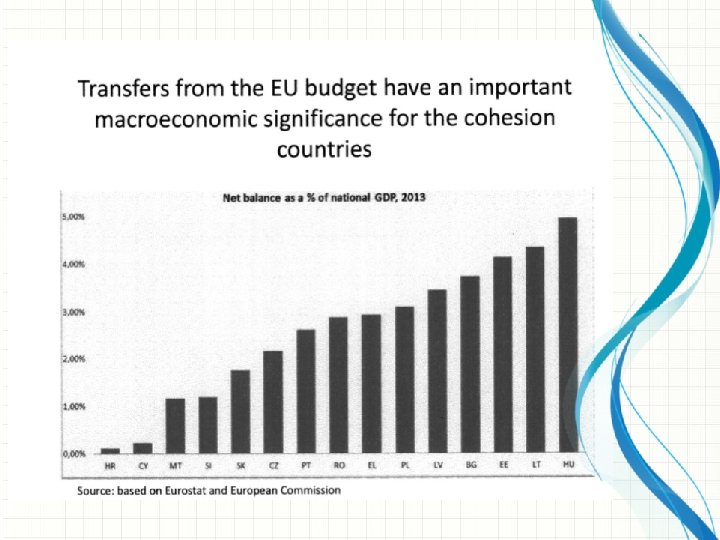

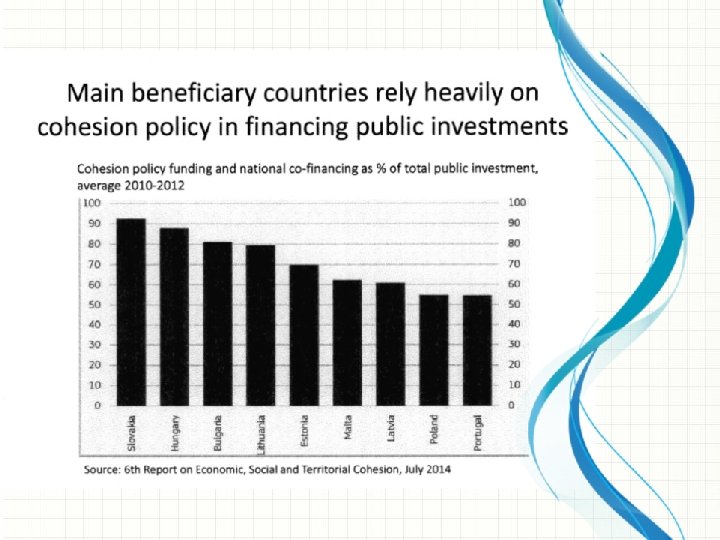

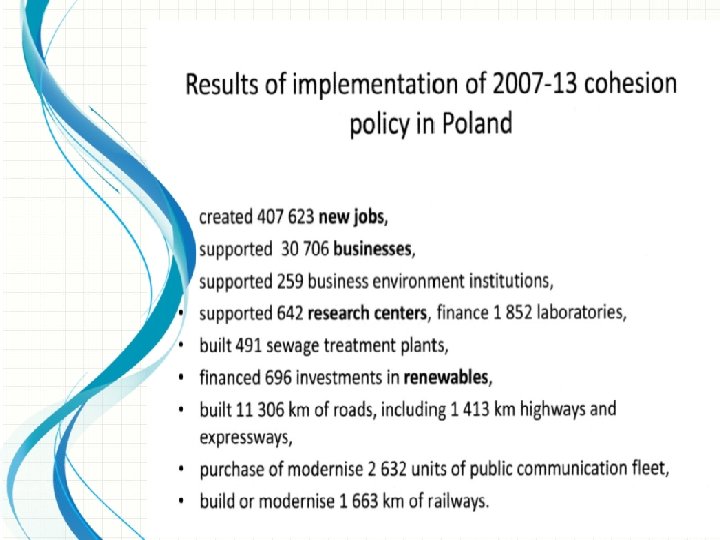

• EU funds have continued to play a key role in a number of Member States. In Bulgaria, the Czech Republic, Estonia, Croatia, Latvia, Lithuania, Hungary, Malta, Poland, Portugal, Romania, Slovenia and Slovakia, EU funds account for a large share of investment Positive, countercyclical impact on MS economies Contributes to achievement of Europe 2020 goals Increasing role in economic governance, macro-economic conditionalities Links with CSRs

European Added Value • Definition – what is EAV – No usiversal definition • How to measure? Different attitude • Limitations • Centralised vs shared implementation – more contitionality in shared management

Thank you

- Slides: 20