Medicare Parts A B 2021 What is Medicare

Medicare Parts A & B 2021

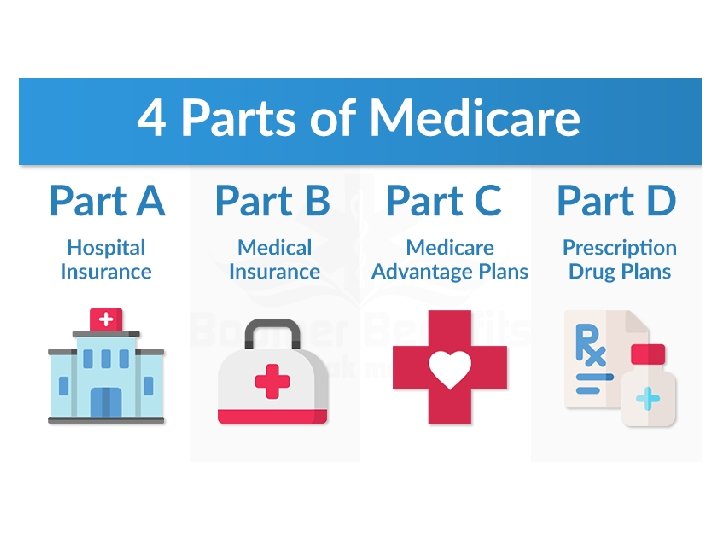

What is Medicare? Federal health insurance program for: • People who are 65 or older • Certain people < 65 with disabilities • People with End-Stage Renal Disease (ESRD)

Roadmap • Part 1: Enrollment and Eligibility • Part 2: Benefits and Cost Sharing • Part 3: Coordination of Benefits

Medicare Enrollment & Eligibility

Enrollment Periods • Initial Enrollment Period • General Enrollment Period • Special Enrollment Period • Enroll via Social Security Administration

Initial Enrollment Period • 7 -month window when first eligible – 3 months before 65 th birthday – The month first eligible (age 65 or 25 th SSDI payment) – 3 months after 65 th birthday/25 th SSDI payment

When does Coverage Start? If you sign up for Part A (if you have to buy it) and/or Part B in this month: Your coverage starts: The month you turn 65 1 month after you sign up 1 month after you turn 65 2 months after you sign up 2 months after you turn 65 3 months after you sign up 3 months after you turn 65 3 months after you sign up *Watch out for first of the month birthdays! Those IEPs will start one month earlier.

General Enrollment Period • Those who did not sign up for Medicare during their IEP can sign up from Jan. 1 - March 31 of each year • Part A coverage starts: – July 1 if not premium-free – Up to 6 months retroactive for premium-free • Watch out for clients with HSAs! • Part B coverage starts July 1 • Late enrollment penalties may apply!

through current employment")

Special Enrollment Period • Individuals with employer group health plan (EGHP) through current employment (or spouse’s current employment) may choose to postpone enrollment without penalty unless they have ESRD – Retiree health insurance and COBRA does not count! • SEP exists: – While still covered by the employee-sponsored plan – During the 8 -month period that begins the month after the employer coverage ends • Coverage starts the month after the month of enrollment – Premium-free Part A will be retroactive up to 6 months – watch out for clients with HSAs!

Part A Enrollment: 65 and over, Premium-free • Automatically enrolled in premium-free Part A and Part B if age 65 and receiving Social Security or Railroad Retirement Benefits • Can enroll at any point after age 65 for premium-free Part A if eligible for retirement benefits but not yet receiving them – Need 40 work quarters; $1, 470/work quarter in (2021) – Coverage will backdate up to 6 months

Medicare Part A Enrollment: Under Age 65, Premium-Free • Disabled and 24 months of disability payments – Waiting period is actually 29 months from date of disability because of 5 months’ waiting period for cash benefits after onset date; enrollment in Parts A & B will be automatic – Includes SSDI and disabled widow’s benefits – Some individuals are eligible for Medicare without the 29 month waiting period (e. g. , ALS) • ESRD – Coverage starts 4 th month of dialysis or month admitted to hospital for transplant; might be retroactive in some situations – Contact BSSA as start dates and enrollment periods can get tricky!

Medicare Part A Enrollment: Age 65 and over, Premium • Individuals 65 and over, not entitled to Social Security or Railroad Retirement benefits can purchase Part A coverage when they sign up for Part B • Must enroll in IEP or GEP (may have LEP) • Premiums calculated by work quarters -30 -39 work quarters: $259/month (2021) -< 30 work quarters: $471/month (2021)

Medicare Part B: Enrollment • If not automatically enrolled during IEP or automatic enrollment was declined at that time, can only enroll during General Enrollment Period or Special Enrollment Period – Individuals who become entitled to Medicare due to disability or end stage renal disease can enroll in Medicare Part B when they are eligible for Part A

Late Enrollment Penalties • Does not apply to individuals with SEP • Part A LEP – Part A premium is increased by 10% if an individual did not enroll when first eligible; penalty lasts for twice the number of years the individual could have had Part A but didn’t sign up. Does not apply to premium-free Part A. • Part B LEP – Part B premium is increased by 10% for each full 12 months that an eligible individual could have enrolled but did not; penalty lasts as long as individual has Part B • If an individual failed to enroll because of governmental error, misrepresentation, or inaction, individual may be entitled to equitable relief – contact BSSA

Medicare Eligibility for Non-Citizens • Eligible if lawfully present and qualified to receive or currently receives Social Security retirement benefits, Railroad Retirement Benefits (RRB), or Social Security Disability Insurance (SSDI) – Will qualify for premium-free Part A in any of these situations • Any U. S. citizen or permanent resident (for at least 5 years) who is age 65 may enroll in Part B during an enrollment period and purchase Part A at that time

Medicare Part A: Cost Sharing & Benefits

Medicare Part A: Coverage Medicare Part A typically covers: • Inpatient care in hospitals • Skilled Nursing Facility Care • Hospice Care • Home health care

Part A and Inpatient Hospital Care • Inpatient Hospital Care -Benefit • Up to 90 days care per benefit period • 60 lifetime reserve days -Cost-sharing • • • Deductible per benefit period: $1, 484 in 2021 Days 1 -60: $0 coinsurance Days 61 -90: $371 in 2021 Days 91 -150 (60 lifetime reserve days): $742 in 2021 Beyond lifetime reserve days: all costs

Part A and Inpatient Hospital Care • Inpatient Hospital Care – Cost-sharing is determined per benefit period not annually – Benefit period begins with the first day a patient received inpatient care and ends when patient has been out of the facility/not receiving skilled care for 60 consecutive days.

Part A and Inpatient Hospital Care • Benefit Periods: Same Benefit Period – Jane enters the hospital on Jan. 1, transferred to SNF on Jan. 5, discharged home on Feb. 2. – On March 15, she breaks her hip and returns to the hospital. She is still within her previous benefit period, so there is no new deductible and her inpatient hospital days will not start over.

Part A and Inpatient Hospital Care • Benefit Period: New Benefit Period – Jane enters the hospital on Jan. 1, is transferred to SNF on Jan. 7, and is discharged home on Feb. 2. – May 1, she falls, breaks her hip, and returns to the hospital. Because it has been more than 60 days since she was discharged, she is in a new benefit period and must pay a new deductible.

Part A and SNF Care • Skilled Nursing Facility Care - requirements – 3 day inpatient hospitalization prior to admission to the nursing home – Admission to the nursing home within 30 days of discharge from the hospital – Admission to the nursing home for treatment of the same injury or illness that was treated at the hospital – Beneficiary must require and receive skilled nursing or skilled rehabilitation services on a daily basis (5 days/week) • If break in skilled care > 30 days, need a new 3 -day inpatient stay for additional skilled care coverage • If break in skilled care > 60 days, benefit period ends

Part A and SNF Coverage • Up to 100 days of skilled care in a Medicare certified SNF, after discharge from a qualifying hospital stay. • Many SNF stays are not covered because of the strict coverage criteria. – Also a lot of misinformation about coverage rules – talk to BSSA!

SNF Cost Sharing • Cost Sharing per benefit period: – Days 1 -20: Medicare pays 100% – Days 21 -100: Beneficiary pays $185. 50 per day in 2021 – Days 101 +: Beneficiary pays 100%, no more Medicare coverage.

Part A and Hospice • Medicare covers palliative care from a Medicare approved hospice program for beneficiaries with terminal illness – Does not cover treatment intended to cure the condition – Treatment of conditions unrelated to terminal illness may be covered by other parts of Medicare

Part A and Home Health Care • Medicare covers some health care after a beneficiary is discharged from a Medicare covered stay in the hospital or a SNF – Part A covers first 100 days after discharge from 3 day inpatient hospital stay or Medicare-covered SNF stay; Part B covers any additional medically necessary care – Beneficiary must be homebound and need skilled nursing care or therapy on an intermittent basis.

Medicare Part B: Cost Sharing & Benefits

Medicare Part B: Coverage • Services from doctors and other health care providers • Outpatient care • Durable Medical Equipment • Home health care • Some preventative services – “Annual wellness visit” but not yearly physical

Medicare Part B: Coverage • Medicare Part B is not comprehensive, and there are some things which will never be covered no matter how medically necessary. • Non-Covered Services – Custodial care – Hearing aids – Eyeglasses or contact lenses – Routine physical exams – Routine dental care – Stem cell therapy to treat arthritis, ligament tears, degenerative disc disease, and other non-FDA approved uses.

– Beneficiaries with income")

Medicare Part B Premium • Monthly premiums: $148. 50 (2021) – Beneficiaries with income higher than $88, 000/ individual or $176, 000/couple will pay an increased premium (IRMAA). – Beneficiaries who are not protected by the “hold harmless provision” will pay a higher premium than they may have in previous years. The provision does not protect: • • Those not collecting Social Security benefits Those who enroll in Part B for the first time in 2021 “Dual eligibles” Beneficiaries who pay an additional income-related premium

If your filing status and yearly income in 2019")

Income-Related Monthly Adjustment Amount (2021) If your filing status and yearly income in 2019 was: File individual tax return File joint tax return Married, file separate tax return You pay each month (2021) $88, 000 or less $176, 000 or less $88, 000 or less $148. 50 above $88, 000 up to above $176, 000 up $111, 000 to $222, 000 Not applicable $207. 90 above $111, 000 up to $138, 000 above $222, 000 up to $276, 000 Not applicable $297. 00 above $138, 000 up to $165, 000 above $276, 000 up to $330, 000 Not applicable $386. 10 above $165, 000 and less than $500, 000 above $330, 000 and less than $750, 000 above $88, 000 and less than $412, 000 $475. 20 $500, 000 or above $750, 000 and above $412, 000 and above $504. 90

Hold Harmless Rule • The “hold harmless” rule protects people from having their previous year’s Social Security benefit level reduced by an increase in the Part B premium if: – They are entitled to Social Security benefits for November and December of the previous year. – The Part B premium was deducted from their Social Security benefits in November 2020 through January 2021. – They don’t already pay higher Part B premiums because of IRMAA. – They do not receive a Cost-of-Living Adjustment (COLA) large enough to cover the increased premium. The 2021 COLA was 1. 3% of the Social Security benefit. • If hold harmless rule applies, beneficiaries pay a premium increase that is the same dollar amount as their COLA.

• After deductible is")

Medicare Part B: Cost Sharing • Annual deductible: $203 (2021) • After deductible is met, beneficiary is usually responsible for 20% of Medicare-approved amounts of covered service or item – Providers who accept assignment accept the Medicare -approved amount as full payment for covered services • Non-participating providers can charge more, subject to limiting charge of 15%; limiting charge does not apply to DME – Services billed under the Outpatient Prospective Payment System have set co-insurance amounts that are re-determined annually

Part B and Prescription Drugs • Part B covers some drugs: – Immunosuppressants if the transplant was Medicarecovered – Durable medical equipment supply drugs – Parenteral nutrition for individual with non-functioning digestive tract – Infusion/ injectable drugs if administered by a physician – Anti-cancer: • Oral anti-emetics prescribed within 48 hours of chemo if full replacement for IV treatment • Oral anti-cancer • Other Part B covered items: – DME: test strips, lancets, ostomy, etc.

Medicare Coordination of Benefits

Medicare & Employer Group Health Plans • Coverage must be through individual or spouse’s active employment • For individual > 65, if: – Employer has <20 employees, Medicare pays primary, EGHP pays secondary – Employer has 20+ employees, EGHP pays primary, Medicare pays secondary • For individual who is disabled, if: – Employer has 100+ employees, EGHP pays primary, Medicare pays secondary • For individual with ESRD, Medicare pays secondary during first 30 months of eligibility or entitlement to Medicare – contact BSSA!

HSA Warning • To avoid a tax penalty, individuals who enroll in Medicare Part A and/or B must stop contributing money to their health savings account (HSA). – IRS rules say that, in order to contribute to an HSA, the individual cannot have any health insurance other than an HDHP. • Individuals who have an HSA with a high deductible health plan (HDHP) based on their own or their spouse’s current employment who are delaying Medicare enrollment should stop contributing to their HSA 6 months before they apply for Medicare. • Individuals can still withdraw money from their HSA after they enroll in Medicare to help pay for qualified medical expenses.

Medicare & COBRA • Individual is age 65 years or older and covered by Medicare & COBRA: – Medicare pays primary, COBRA pays secondary • Individual is disabled and covered by Medicare & COBRA: – Medicare pays primary, COBRA pays secondary • Individual has ESRD, is covered by COBRA and is in the first 30 months of eligibility or entitlement to Medicare – COBRA pays primary, Medicare pays secondary

Medicare and Retiree Health Plans • Individual is age 65 or older or qualifies for Medicare through disability and has an employer retirement plan: – Medicare typically pays primary, Retiree coverage pays secondary – check plan documents to see whether Medicare enrollment is required!

Liability Insurance & Workers’ Comp • Individual is entitled to Medicare and was in an accident or other situation where no-fault or liability insurance is involved. – No-fault or Liability Insurance pays primary for accident or other situation related health care services claimed or released, Medicare pays secondary • Individual is entitled to Medicare and is covered under Workers’ Compensation because of a job-related illness or injury: – Workers’ Compensation pays primary for health care items or services related to job-related illness or injury claims. • Note: When there is evidence that the no-fault insurer, liability insurer, or workers’ compensation plan will not pay promptly, Medicare may make a conditional payment. The payment is “conditional” because it must be repaid to Medicare when a settlement, judgment, award or other payment is made. • Contact BSSA in these situations!

Role of the Benefit Specialist • Information: Medicare can be very confusing, and you will be the expert in your county! • You will also be instrumental in helping clients understand coverage determinations and assisting them with appeals when necessary. • Enrollment in Part B at the proper time is very important and will continue to be more confusing for eligible beneficiaries as many continue to work past age 65.

- Slides: 42