Master Class Term Structure and Weighted Vega Option

Vega position will benefit with an increase in implied")

For a calculation use:")

X Vega")

")

- Slides: 27

Master Class Term Structure and Weighted Vega Option Pit

Disclosure • • The materials presented from Option Pit LLC are for your informational and educational purposes only. Option Pit LLC nor its employees do not offer investment, legal or tax advice of any kind, and the analysis displayed with various tools does not constitute investment, legal or tax advice and should not be interpreted as such. Using the data and analysis contained in the materials for reasons other than the informational and educational purposes intended is at the user’s own risk. Option Pit LLC is not responsible for any losses that may occur from transactions effected based upon information or analysis contained in the presented materials. Specific trading ideas or strategies discussed in the presentations or materials are entirely illustrative and do not constitute a solicitation of a transaction (or transactions) or a recommendation to execute a particular transaction or implement a particular trading strategy. To the extent that you make use of the concepts with the presentation material, you are solely responsible for the applicable trading or investment decision. Use caution when entering any option transaction and it is recommended you consult with your financial advisor for investment, legal or tax advice relating to options transactions

What you will learn • • • We will talk about the Greek Vega and Theta What is the Term Structure Understanding Vega Weighting Using Forward Volatility in a calculation What does this have to do with VIX and Vol Products?

Easy Greeks – Vega and Theta

What is Vega • The simplest definition of Vega is: – The sensitivity of an options price to change in implied volatility • It is sometimes called an options’ ‘delta’ to implied volatility • Vega measures risk for a change in Volatility

Vega • The Vega S. A. T. question: – Delta is to Change in Price as Vega is to: • • White Castle Sliders Implied Volatility Chevy Camaro IROC-Z Newport Menthol Cigarettes – Vega is tradable • This is central to this class

Vega • A positive (+) Vega position will benefit with an increase in implied volatility • A negative (-) Vega position will be hurt by an increase in implied volatility • Long options have positive Vega (long juice) • Short options have negative Vega (short juice)

Implied Volatility and Vega • In practice Vega really measures changes in Implied Volatility – THUS for every 1% change in implied volatility, the option will change X number of cents per contract • To calculate multiply VEGA*CHANGE IN IV*100 – Thus a 2% increase in IV in an option that has. 20 of Vega would be: • 2*. 20*100, or $40. 00 – The VIX and Vol Products use Vega as a direction

What is Theta • The simplest definition of theta is: it is the rate at which an option’s time premium or ‘fluff’ is disappearing – How quickly is the ‘insurance value’ heading to 0 • The technical definition is the sensitivity of the option to the passage of time • Theta measures TIME RISK

Theta • A positive theta position will benefit with the passage of time (as time passes position MAKES $$$) • A negative theta position will be hurt by the passage of time (as time passes position will lose $$$) • Long options have negative theta • Short options have positive theta

Time and IV • Time and Volatility are factors in the Option Model They do a dance that rules the performance of spreads

Let’s Evaluate Theta and Vega

Term Structure Each month or week has a singular volatility that helps us determine what the market is thinking

Theta and Vega Same option strike different DTE and Vegas

Theta and Vega • Note how Theta and Vega can change in dominance for the risk in a position. – This is the Greeks telling you which one is more important

A Note on Vega and Forward Vol Is the Vega you see? Is the IV you see? • The IV changes do not always move linearly across the term structure – http: //www. optionpit. com/blog/understandingweighted-vega-spx-options

How does Volatility move? ATM volatility moves proportionally to 1/SQRT(t) For a calculation use: Or Vw= SQRT (Tw/T) x V We make the back term vols “look forward” to adjust for time We weight the Vegas to the term

Pricing Weighted Vega For Weighted Vega for standard options: Vw=SQRT(near DTE/Far DTE) X Vega Ex for 01/24/2017 10 SPY Feb 10 2017 226 calls have 205 Vega Now we weight to the Jan 27 term SQRT(3/17) X 205 = 86. 1 Vega – Let’s price a time spread

Comparing two IV’S • Normalize for time • Why do we do this? Because part of each term is shared time. • We want to find the value of the unshared time – =SQRT((T 2*vol 2^2 -T 1*vol 1^2)/(T 2 -T 1))

Creating Forward Vols This helps us assess the forward value of the IV and the value of a time spread. Also, this can measure what we give up or gain in a time spread Courtesy of A. Singh

What term is the VIX? • Now why do we care about Term Structure if we trade the Vol Products and VIX? • VIX prices a very narrow part of time. 30 days out There are lots of different vols short term but VIX cash does not price it -the Weekly futures do

VIX futures trade by the Week

Where the VIX looks

What did we learn? • Not all Volatility is created equal nor is the vega – Time needs to be normalized to get an accurate picture • We now have devices for helping to analyze volatility horizontally • Volatility seeks these numbers We use these techniques through out the course now!

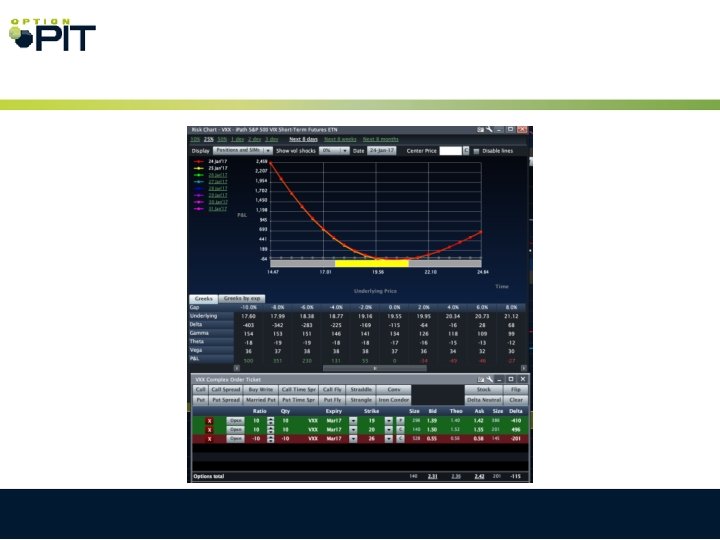

Let’s Create a trade • -5 SPXW JAN 27 2265 at 2. 11 • 5 SPXW JAN 30 2265 FRO 3. 15

Thank you for attending! For question you can contact: mark@optionpit. com andrew@optionpit. com 1(888) Trade-01