MARYLAND MUNICIPAL LEAGUE FALL CONFERENCE MUNICIPAL BUDGETING ALFRED

MARYLAND MUNICIPAL LEAGUE FALL CONFERENCE MUNICIPAL BUDGETING ALFRED E. MARTIN, CPA STEPHANIE WALKER, CPA, CPFO OCTOBER 8, 2020

CLASS OBJECTIVES • Introduce participants to framework and fundamental concepts of municipal budgeting in Maryland • Help participants better understand their municipality’s financial picture • Give participants ideas for how to handle the extraordinary fiscal issues facing municipal governments in these difficult economic times • COVID-19 adjustments

LEGAL FRAMEWORK: MARYLAND LAW • Fiscal Year: July 1 – June 30 (Art. 24, Sec. 1 -102) • Expenditures: must be for public purpose (Art. 23 A, Sec. 2(b)(2)) • Amendments: 2/3 vote required (Art. 23 A, sec. 2(b)(2)) • Constant yield tax rate (Tax-Property Art. , Sec. 6 -308) • Financial reporting (Art. 19, Sec. 35 – Sec. 41) • Audit (Art. 19, Sec. 35 – Sec. 41)

LEGAL FRAMEWORK: FINANCIAL REPORTING Requirements of Manual of Uniform Financial Reporting issued by Department of Legislative Services (DLS): • Submission of annual Uniform Financial Report to DLS • Expenditures must be classified by function or program, at minimum: • • Salaries Other operating expenses Construction Other capital

LEGAL FRAMEWORK: MUNICIPAL CHARTER/ORDINANCES • Responsible person; schedule; required content • Requirement that budget be balanced • Public review, notice, and hearings and adoption process • Amendment procedures • Requirement that unencumbered appropriations lapse

Special Revenue Fund(s) General Fund Debt Service Fund")

COMMON TERMS: FUNDS Capital Projects Fund(s) Special Revenue Fund(s) General Fund Debt Service Fund Utilities

COMMON TERMS: FUND BALANCE / NET POSITION • Accumulation of all previous years’ revenues minus expenditures • Exists within each fund • Nonspendable, Restricted, Committed, Assigned, or Unassigned • Other common names: • • Reserves Undesignated / Unreserved Fund Balance (old terminology) Working Capital Rainy Day Fund

FINANCIAL POLICIES • Fund Balance • Minimums, or targets • Allowed uses for excess • Method for replenishing, if under target • Revenue / Rate setting • Recurring vs one-time • Rate development full cost vs some costs

http: //www. mdmunicipal. org/724/Conducting-Municipal-Business-Duringthe •")

RESOURCES FOR CHALLENGING TIMES • Maryland Municipal League (MML) http: //www. mdmunicipal. org/724/Conducting-Municipal-Business-Duringthe • Government Finance Officers Association (GFOA) https: //www. gfoa. org/coronavirus • International City Managers’ Association https: //icma. org/blogposts/budgeting-during-crisis-four-step-plan-respond-covid-19 recession? _zs=Pdhsb 1&_zl=f 4 Kj 6

BREAK OUT SESSION Group Discussion Questions 1. What financial challenges and uncertainties are your community facing, or expecting to face, this year due to the COVID-19 pandemic? 2. What did you change to cope with these challenges or uncertainties? Please take notes to do a report out after the break.

DEBRIEF FROM BREAKOUT Notes:

DEBRIEF FROM BREAKOUT Reliance on fund balances • Be aware of the long-term impact of using fund balance to balance your budget. • Compare expected new fund balance level to policy • GFOA recommendation no less than 2 months of operating expenditures (likely more depending on each gov’ts unique position)

BUDGETING FOR THE UNEXPECTED Other unexpected costs we face annually: • Unforeseen termination/retirement payouts • Unusual amounts of ice and snow removal • Large equipment/facility failures • Union negotiations / raises • Other emergencies

BUDGET TIPS & TRICKS • Developing current year projections for revenues and expenditures • Compare to actuals (multi-year when possible) • Reduce conservative budgeting and budget pad • Budget postmortem • Salary vacancy

REVENUE: PROJECTION TECHNIQUES

REVENUE: PROPERTY TAX BASICS • Real property • Commercial personal property • Assessments: 100% valuation • Tax rates • Constant yield tax rate

REVENUE: PROPERTY TAX CALCULATIONS How much revenue will a $0. 01 increase in property taxes generate?

REVENUE: OTHER SOURCES • • Admissions and amusements tax Hotel or room tax Grants: Federal, State, or County property tax rebate Recycling collections Ordinance and police fines Licenses and permits Recreation fees Technology / administrative fees Donations Parking permits Utility charges: water, electric, stormwater, sanitary sewer • Sale of capital assets • Debt proceeds / borrowing • •

EXPENDITURES

EXPENDITURES: POLICY QUESTIONS/CONSIDERATIONS Key Questions: • What types of programs and services? • At what spending or service levels? Key Considerations: • Legal authority • Legal mandates • Community characteristics and needs • Goals and priorities • Services provided by other entities • Available revenue

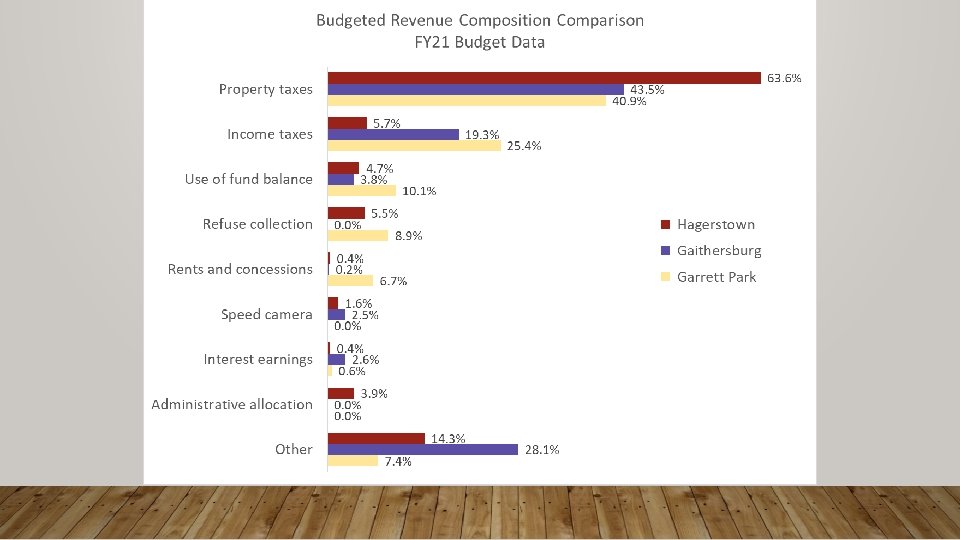

* Note - Garrett Park’s budget is not presented in exactly this manner; presenter judgment was used to present in this categorization

BUDGET AS A PROCESS: STEPS • Preparation • Review and adoption • Implementation • Evaluation

BUDGET AS A PROCESS: PREPARATION • Set fiscal guidelines • Estimate revenues and expenses • Develop proposed budget

BUDGET AS A PROCESS: REVIEW AND ADOPTION • Disseminate information; provide notice as required by State and any local requirements • Conduct presentations and hearings (e. g. , State constant yield tax rate) • Discuss issues • Obtain public comment • Make adjustments • Adopt budget; set tax rate

BUDGET AS A PROCESS: IMPLEMENTATION

BUDGET AS A PROCESS: IMPLEMENTATION • Posting on website and updating accounting system • Identifying your procedures for spending within budget • Regular review of actual compared to budget (and projections) • Budget transfer authority • Amendments

BUDGET AS A PROCESS: EVALUATION • Baseline for budget development • Uniform financial report (UFR) – November 1 • https: //msa. maryland. gov/megafile/msa/speccol/sc 5300/sc 5339/000113/ 012000/012544/unrestricted/20100420 e. pdf • Annual audit of financial statements

www. GFOA. org • Distinguished Budget")

ADDITIONAL RESOURCES • Government Finance Officers’ Association (GFOA) www. GFOA. org • Distinguished Budget Presentation Awards Program: awards criteria • Podcasts, articles and books on budgeting and municipal finance • Best practices on budgeting and financial policies • Maryland Department of Legislative Services • Local Government Finances in Maryland reports www. dls. Maryland. gov look under publications, most recent http: //dls. maryland. gov/pubs/prod/Inter. Gov. Matters/Loc. Fin. Tax. Rte/Local_Government_Financ es_FY_2018. pdf • Other municipalities budgets and policies • City of Hagerstown https: //www. hagerstownmd. org/143/Finance • City of Gaithersburg https: //www. gaithersburgmd. gov/government/budget-strategic-planning

ADDITIONAL RESOURCES Alfred E. Martin, Stephanie M. Walker, CPA, CPFO Retired Finance Director Stephanie. Walker@Walker. Cross. com City of Hagerstown, Maryland (414) 840 -4506 aemartin 24@aol. com (301) 991 -3468

MUNICIPAL BUDGETING: SELF-STUDY See self-study problems 1 -6 in Municipal Budgeting Class Participant Handbook Available online at www. mdmunicipal. org under Conferences & Training

- Slides: 31