Markets Law and Regulations Banking Union Banking Union

Markets Law and Regulations Banking Union

Banking Union Summary • Introduction • Key regulatory initiatives and the Banking Union • The idea of setting up a Banking Union • The four «building blocks» of the BU • The Single Supervisory Mechanism (SSM) • The Single Resolution Mechanism (SRM) • The Bank Recovery and Resolution Directive (BRRD)

Intro – European banking union: why? • In 2007 instability in the subprime mortgage market in the U. S. triggered a crisis that spread through the money markets in the U. S. affecting participating financial institutions. • The crisis worsened throughout 2008, eventually taking with it two large investment banks: (Bear Sterns and Lehman Brothers) • European banks were not immune from these events.

Intro – European banking union: why? • • • Some of them had U. S. mortgage‐backed securities in their balance sheets the value of which decreased as confidence and liquidity dried up in the U. S. markets. Some of the ailing banks held considerable amounts of sovereign debt. In the years that followed (in particular, 2012), many EU MS had to fight the problems that had arisen in their highly interconnected banks using national policy tools. Moreover, the interdependencies resulting from the single currency hindered the capacity of Member States to respond rapidly and effectively. Eventually, some MS ended up requesting financial assistance from outside sources, which put additional pressure on the public finances and boosted public debt to unprecedented levels.

Introduction • The micro‐ and macro‐prudential supervisory remits of competent authorities have been radically re‐arranged recently in Europe, in particular within the Euro area with the establishment of the SSM and the conferral of specific supervisory tasks to the ECB under Article 127(6) TFEU.

Key EU regulatory initiatives and the BU Financial Transaction / Activity Tax SIFI Corporate Governance and Remuneratio n Policies CRD IV/CRR (Basel III) Bank Recovery and Resolution Deposit Guarantee and Investor Compensati on Schemes Consumer Protection Revision of Mi. FID and Market Abuse Directive

The idea of setting up a Banking Union The European Banking Union was born out of a perceived need for a stronger and more centralized system of financial supervision and resolution to restore credibility and stability to the euro area banking system, to break the doom loop between banks and sovereign states, and thereby to help address the fundamental problems of the euro area and of the EU.

More specifically… • • • EBU is intended to set out a supervisory upgrade identified as a necessary precondition for the unlocking of European Stability Mechanism (ESM) funding for direct bank recapitalization. EBU quickly began to acquire concrete shape in the form of the Single Supervisory Mechanism (or SSM), with the ECB as its hub. The legal framework for the establishment of the SSM was agreed in September 2013 and entered into force on 30 October 2013

What is banking Union? • • • Single Supervisory Mechanism* • ECB + NCAs Single Resolution Mechanism Single Resolution Board and Fund + National Resolution Authorities + Single Banking Rulebook (single market) + State Aid rules (single market) + European Stability Mechanism • + Proposed European Deposit Insurance Scheme…. (November 2015 COM proposal) Designed as a euro area mechanism • • SRM/SSM mandatory for euro area Other MS can join on a voluntary basis (‘participating MS’)

Banking Union • The purpose of the European institutions is to take into proper account the challenges that the Economic and Monetary Union (EMU) is facing. • Notwithstanding the 2011 reform (ESRB + ESAs) the Euro area is still diverse and non‐coordinated national policies have effects that “quickly propagate to the euro area as a whole”.

Banking Union In 2012 the Von Rompuy report proposed a “vision” for the EMU based on four pillars: an integrated financial framework to ensure financial stability in particular in the Euro area and minimise the cost of bank failures to European citizens; an integrated budgetary framework to ensure sound fiscal policy making at the national and European levels, encompassing: coordination, joint decision‐making, greater enforcement and commensurate steps towards common debt issuance; an integrated economic policy framework compatible with the smooth functioning of EMU; a higher level of democratic legitimacy and accountability of decision‐making within the EMU

The four building blocks… • … are deemed to be necessary for long‐term stability in the EMU, but of course they require a lot of further work, including possible changes to the EU treaties. • For the time being the instrument through which the goal of greater and better financial integration is pursued is to entrust the prudential supervision of banks to the ECB (on the basis of art. 127, para. 6, TFEU).

: • Art.")

Art. 127 TFUE as legal basis… • For single supervision (on banks): • Art. 127, par. 6. : “The Council, acting by means of regulations in accordance with a special legislative procedure, may unanimously, and after consulting the European Parliament and the European Central Bank, confer specific tasks upon the European Central Bank concerning policies relating to the prudential supervision of credit institutions and other financial institutions with the exception of insurance undertakings”.

… more than just prudential supervision • Supervision is an important first step towards what has been called the “banking union“. However, it requires other two pillars: • the introduction of standard procedures for the resolution of banking crisis occurring in the Euro area; • the creation of a European deposit guarantee scheme;

Banking Union Single Supervisory Mechanism Single Resolution Mechanism Deposit Guarantees Single Rulebook

The first pillar: SSM • The initial package of measures relating to prudential supervision is divided into two proposals for regulations which provide for: • the creation of a single system of supervision under the responsibility of the ECB (Single Supervisory Mechanism or SSM); and for • the necessary amendments to Regulation 1093/2010 establishing the EBA.

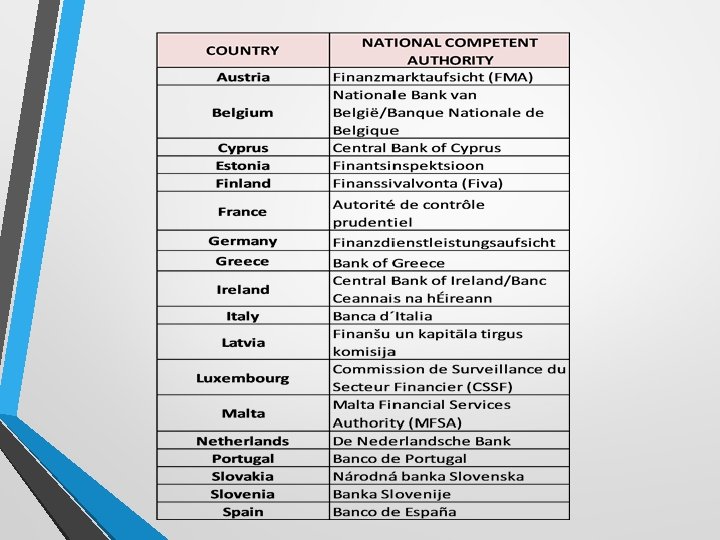

Why a SSM? • The main aims of the single supervisory mechanism is to ensure the safety and soundness of the European banking system and to increase financial integration and stability in Europe. • The ECB has been give the responsibility to ensure the effective and consistent functioning of the single supervisory mechanism, cooperating with the national competent authorities of participating EU countries.

• In 2012 the Commission issued a set of proposals as")

The proposals (2012) • In 2012 the Commission issued a set of proposals as the first step towards an integrated “banking union”. • one regulation giving supervisory powers to the ECB and national supervisory authorities, i. e. the creation of a SSM; • one regulation introducing limited changes to the regulation that had set up the European Banking Authority (EBA) to ensure a balance in its decision making structures in the face of the new SSM; • and a communication presenting a roadmap for the implementation of the banking union, covering the single rulebook, common deposit protection and a single bank resolution mechanism.

• In October 2013, the European Union formally adopted")

SSM: entry into force (2013) • In October 2013, the European Union formally adopted the creation of a SSM by promulgating two Regulations: • One in which the Council agreed to confer specific supervisory tasks to the ECB and • a joint Regulation of the European Parliament and the Council amending the previous Regulation that had established the EBA • In addition, in July 2014, the European Parliament and the Council adopted Regulation (EU) No. 806/2014 establishing the Single Resolution Mechanism (“SRM”) and a Single Resolution Fund (“SRF”)

The SSM: an overview • The SSM is the system of prudential financial supervision of credit institutions in the E. U. composed of • • • the ECB and the National competent authorities of participating Member States. Under the SSM Regulation, “participating Member States” shall mean all Member States whose currency is the euro or any other Member States who establish a close cooperation with the SSM (see Article 7 of the SSM Regulation: opt in mechanism)

The SSM: an overview • Articles 4 and 5 of the SSM Regulation provide for the specific competences to be attributed to the ECB in relation to micro‐ and macro‐prudential supervision, respectively. • In particular, Article 4. 1 expressly refers to the following microprudential tasks: • “[T]o authorise credit institutions and to withdraw authorisations of credit institutions” • the SSM Regulation provides that any application for authorization to take up the business of a credit institution shall be submitted to the relevant NCA. The NCA will submit a draft decision to the ECB, who will be able to adopt it or modify it depending on the circumstances. The article also regulates the process for withdrawing an authorization.

The SSM: an overview • Futhermore: • • • For supervised institutions wishing to establish a branch or provide crossborder services in a non‐participating Member State, to undertake the tasks of the competent authority in the home Member State; to undertake the supervisory tasks of NCAs when a credit institution established in a nonparticipating Member State establishes a branch or provides cross‐border services in a participating Member State; “[T]o assess notifications of the acquisition and disposal of qualifying holdings in credit institutions, except in the case of a bank resolution”

The SSM: an overview • To ensure that supervised credit institutions comply with the ECB’s acts which impose prudential requirements (e. g. capital requirements) • To carry out supervisory reviews, stress test and their possible publication, and to impose any additional measures hat are considered necessary to ensure a sound management and coverage of the risks of the relevant supervised institutions; • To carry out supervision on a consolidated basis over credit institutions’ parents • To supervise recovery plans and early intervention where a credit institution or a supervised group may be likely to breach any applicable requirements, and to supervise any structural changes where expressly stipulated by Union law, excluding any resolution powers.

What makes a credit institution “significant”? • the NCAs’ tasks cover those credit institutions considered to be “less significant” except for authorizations and notifications of the acquisition and disposal of qualifying holdings in credit institutions, while the ECB’s direct exercise of the supervisory tasks will cover those institutions that shall not be regarded as “less significant”. • Deciding on whether credit institutions are significant or not will also be based on: • • the total value of their assets; • • the significance of their cross‐border activities; the importance for the economy of the country in which they are located or the EU as a whole; whether they have requested or received public financial assistance from the European Stability Mechanism (ESM) or the European Financial Stability Facility (EFSF).

Participating countries • Euro area countries participate automatically in the single supervisory mechanism. • Non‐euro area Member States can also choose to participate in the single supervisory mechanism by their national competent authorities entering into “close cooperation” with the ECB (s. c. opt‐in mechanism). • If the ECB agrees, the decision will be published in the Official Journal of the EU.

Non‐participating countries • The ECB and the competent authorities of other EU countries will conclude a memorandum of understanding describing how they will cooperate with one another in the performance of their supervisory tasks. • The ECB will also sign a memorandum of understanding with the competent authority of each EU country that is home to at least one global systemically important institution.

How many credit institutions re directly supervised by the ECB? 129 credit institutions, representing almost 85% of total banking assets in the euro area. All other credit institutions in the participating countries, around 6, 000 in the euro area alone, will continue to be supervised by the national competent authorities. The ECB can decide at any time to exercise direct supervision of any one of these credit institutions in order to ensure consistent application of high supervisory standards.

The impact of the SSM on the existing framework • The SSM introduces a different approach as compared to the one adopted in 2011 by establishing the three micro‐ prudential supervisory (or just regulatory? ) authorities (EBA, ESMA, EIOPA) and ESRB (macro‐prudential) • creation of European system with ECB at its heart, with allocation of supervisory tasks at EU or national level on the basis of systemic relevance

Decision making • SSM decisions are taken by a supervisory board created by the regulation. • • • Draft decisions are adopted unless the ECB Governing Council objects within a period of less than 10 days (endorsement? ). The supervisory board will consist of the chair, the vice chair (an ECB executive board member), four representatives from the ECB and one representative from the supervisory authority of each member state participating in the SSM. Decisions of the supervisory board shall be taken by simple majority of its members, with every member having one vote, except for decisions on regulations adopted by the ECB.

Accountability • The accountability of the ECB in the exercise of its supervisory tasks is broad‐based. • • accountable to the European Parliament and the Council of Ministers for the implementation of the draft regulations regular reporting requirements and the supervisory board chair needs to present the report to the European Parliament and the Eurogroup extended by those ministers of countries participating in the SSM. The chair may also be heard by the relevant committees on the execution of its tasks. Finally, the ECB is also required to answer in writing any questions raised by national parliaments, and national parliaments may invite the chair or any other member of the supervisory board for an exchange of views

")

Issues • • Non‐euro countries stay out of the SSM (save for “opt in”) Furthermore, in the event a non‐Euro Member State decides to opt in, it will have a slightly different position from Euro area Member countries because: • Non‐Euro countries will only have limited rights to participate in the decision‐making process; and • the ECB will keep its power to unilaterally exclude them from the common mechanism of supervision where they do not comply with their obligations.

Issues • risk of overlaps of competences between the ECB and the EBA? • They will play different roles, however it is no coincidence that the European Commission has constantly reiterated that the role of EBA will be similar to its current role, with – apparently ‐ no clashes with the powers granted to the ECB: • “…to avoid fragmentation of the internal market following the establishment of the single supervisory mechanism, the proper functioning of the EBA needs to be ensured. The role of the EBA should therefore be preserved in order to further develop the single rulebook and ensure convergence of supervisory practices over all EU”

- Slides: 33