Market Structures Competition Conditions of Perfect Competition Perfect

- Slides: 29

Market Structures

Competition • Conditions of Perfect Competition – Perfect competition is the goal of economists for a stable free market. – In this situation, there are many sellers, selling identical products, able to enter and exit the market freely, and none of them are large enough to influence prices. – There need to also be many well-informed buyers, all looking for the best prices. This keeps the system in equilibrium.

• This system exists for only some products. Pencils and pens, and paper products come close to this, as do some agricultural products (though many agricultural products come from very large agribusinesses that have a large impact on prices. ) • Many products do not fit into a perfectly competitive system, such as Microsoft in the operating system business, and automobile companies like the big three auto makers in Detroit: Ford, Chevy, GM.

Barriers to Entry • Competitiveness in markets largely has to do with the ease with which new firms can enter the market. • Markets that require a lot of technical knowledge (computer hardware), large amounts of infrastructure (oil, transportation, factories), or difficult to get resources have large start up costs. • In these cases, there remains a relatively few businesses that are in the market, making perfect competition improbable.

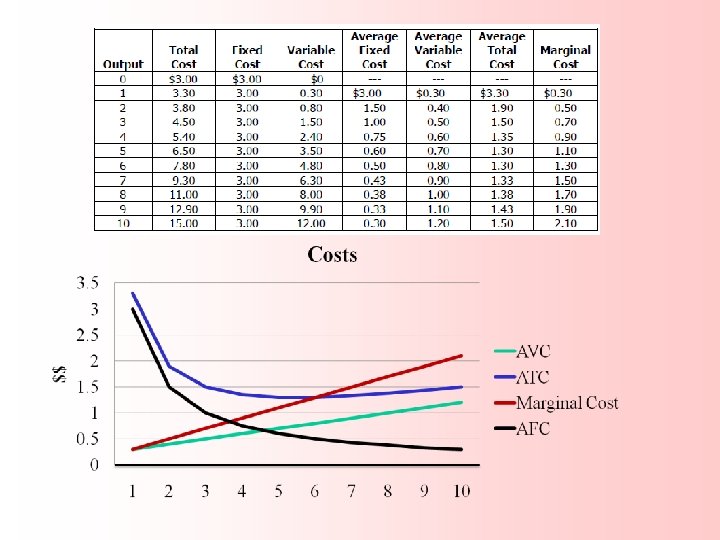

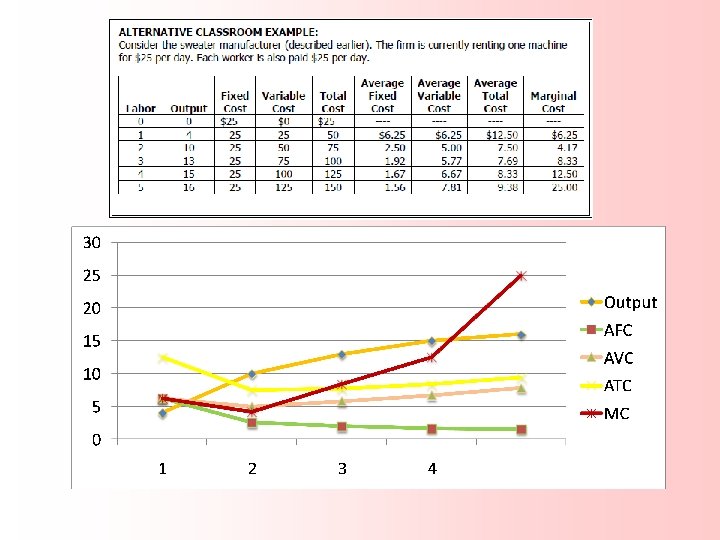

Cost • To have an understanding of how businesses act, it is necessary to understand a few things about costs. • For a normal business, the cost of making something comes from fixed costs (FC) and variable costs (VC). • We can divide the number of products into these costs to get average costs per item, ie. Average Fixed Cost (AFC), Average Variable Cost (AVC). • We can add AFC and AVC together to get Average Total Cost (ATC). • We also want to look at the marginal costs (the amount of difference it takes to make the next item).

Cost Curves for a Typical Firm Marginal Cost declines at first and then increases due to diminishing marginal product. Note how MC hits both ATC and AVC at their minimum points. AFC, a short-run concept, declines throughout. Costs $3. 00 2. 50 MC 2. 00 1. 50 ATC AVC 1. 00 0. 50 AFC 0 2 4 6 8 10 12 14 Quantity of Output

Firm in a Competitive Market • • Because a competitive firm is a price taker, its revenue is proportional to the amount of output it produces. The price of the good equals both the firm’s average revenue and its marginal revenue. To maximize profit, a firm chooses a quantity of output such that marginal revenue equals marginal cost. Because marginal revenue for a competitive firm equals the market price, the firm chooses quantity so that price equals marginal cost. Thus, the firm’s marginal cost curve is its supply curve. In a market with free entry and exit, profits are driven to zero in the long run. In this long -run equilibrium, all firms produce at the efficient scale, price equals minimum average total cost, and the number of firms adjusts to satisfy the quantity demanded at this price. In the short run, an increase in demand raises prices and leads to profits, and a decrease in demand lowers prices and leads to losses. But if firms can freely enter and exit the market, then in the long run the number of firms adjusts to drive the market back to the zero-profit equilibrium.

Example: Competitive Market • At what level should the firm operate to maximize profit?

Monopolies • Monopolies exist when there is a single supplier for a good, and the barriers to entry prevent other suppliers from entering the market. • While monopolies are generally considered to be bad because they can limit the quantity supplied and can charge whatever they want, there are other kinds of monopolies that economists love.

Monopoly Price Making • Because a monopoly is a price maker, rather than a price taker, it can set it’s price at the point of maximum profit. • Profit = (P – ATC) * Q • This means that there is a deadweight loss that occurs where product is not produced because the monopoly sets the price above equilibrium.

Economies of Scale • An economy of scale is where a business’ costs continue to drop with each product made. • Normally after a certain amount, the cost of making each additional product falls for a time (startup costs are large initially, an the cost to make an individual item small), but eventually the cost rises again. • With an economy of scale, the cost keeps dropping, up to the limit of supplying the entire world market. • This is where a single business can produce enough of a good for everyone, and do it cheaply.

Average Total Cost in the Short and Long Run Average Total Cost ATC in short run with small factory ATC in short run with medium factory large factory ATC in long run $12, 000 10, 000 Economies of scale 0 Constant returns to scale 1, 000 1, 200 Diseconomies of scale Quantity of Cars per Day

Natural Monopolies • A natural monopoly is where the ability to provide a good or service is limited by a large infrastructure, like water and electricity. • Because it takes such a large investment to put up the wires, or make the canals and pipes, it is considered foolish to build a second set for each household just for the sake of competition. • In these cases, one firm is allowed to have a monopoly in that area, and the rates it can charge are regulated.

Government Monopolies • The government can allow some businesses to have a limited monopoly in certain cases. • One is for patents, that allows a person or business to have the sole right to produce and sell a particular item, like a new drug. • Government can also permit a particular seller to have a limited franchise within a specific area, like a school or national park, where it is believed good to have some form of business there, but not desirable to have many.

Prices and Monopolies • Monopolies have a greater ability to set prices than does a business that is competing for customers. • In these cases, the monopoly business wants to get the most profit they can, by setting the price at the point of diminishing returns, as opposed to the cost of making the item (which is supposed to be the place where, in perfect competition, the various sellers will sell their products).

Price Discrimination • Monopolies can also take advantage of price discrimination, though many firms practice this as well. • Taking a look at a demand curve, there are people that will pay more for a product than the equilibrium price. • To maximize profit, the seller wants to get those individuals to pay more, and still get the people who don’t want to pay that much, but will still buy at equilibrium.

Example of Price Discrimination • For example, the equilibrium price of a new cell phone may be $100, but there are people willing to pay up to $200 for that phone. • The seller wants to get that $200, even if for only a few of their phones, so it initially sells that phones at $200, then over the next few months, it reduces the price gradually, until it reaches the equilibrium price. • The phone sits at the equilibrium price for a while, then they begin to sell some at a discount, perhaps with a complicated rebate scheme, to get those who want the phone, but not at the equilibrium price. • Using this method, the producers of the phone can get maximum profit from the sale of their phone, by targeting each group that is willing to buy that phone at different prices.

Monopolistic Competition • Monopolistic competition are where there are many firms, barriers to entry are low, there is little control over prices, and there is little variation of goods. • There are many examples of these kinds of businesses, like retail stores, or gas stations. They tend to have some kind of brand image, and differentiate themselves by service, product quality, or features.

Oligopoly • An oligopoly is a situation where there a few firms that produce very similar products, but are different in some variation. Cola companies would fall into this category. • In these cases, people are attached to a brand, like Pepsi, but if the prices rise significantly, they may choose Dr. Pepper instead. • The conditions for an oligopoly are that there a few firms, barriers to entry are high, there is some control over prices, and the products are slightly different.

Price Collusion and Cartels • When there are few suppliers for a good, it is possible for them to get together and set prices for the benefit of all the suppliers. This is called price fixing, and collusion. These practices are illegal, since they undermine competition in the market. • Cartels are a form of open agreement between firms to set prices, such as OPEC (Organization of Petroleum Exporting Countries). While illegal in the U. S. , OPEC countries agree on the limits of each country to pump oil, thus limiting supply and raising prices.

Regulation and Deregulation • Because of the ability of monopolies and oligopolies to have a large control over prices and supply, regulations are instituted to have some control over this. • Much of this is because that it is recognized that where monopolies form, the price goes up, and the quantity supplied goes down, making the market less efficient.

Predatory Pricing • Large firms have the ability to practice predatory pricing to prevent competition. • Because a large firm usually has much lower costs (economies of scale), they are able to prevent new firms from supplying the market by lowering their prices temporarily, thus making it impossible for a new firm to make a profit. • Once the new firm is gone, the prices go back up.

Buy Outs and Mergers • Businesses also tend to buy out their competition, buy offering the owners a lot of money, then either shutting down the operation, or using it to make the buyers product. • This can also happen with mergers. As the number of firms producing a good go down, the supply becomes limited to a few producers, thus limiting supply and increasing the price.

Anti-Trust Laws • Many regulations were put into place over the years to prevent this kind of practice, and to bust up monopolies. These were called Anti-Trust laws. • Over the last few decades however, many of these laws have been repealed or simply not enforced, allowing a few companies to dominate certain businesses. This has been known as De-Regulation. This has allowed for a few companies to now own large part of the newspapers, television, radio, cable market, energy, and other sectors of the market. • The idea was that by de-regulating the markets, it would allow for more competition, and lower prices. The effect has not been what was advertised, and now diversity has gone down, and prices have gone up. The California Energy Crisis is one example of this.

Market Failure • Capitalism is supposed to operate on the principle that the market forces will prove to be superior to decision making by governments and bureaucracies. • In truth, however, unregulated capitalism invariably ends up in the destruction of economies, and again, invariably, regulation and socialism need to rescue capitalism from itself. • On the other hand, when capitalism is regulated and focused on the goals of the society rather that simply profit, the system can work very well, though it still needs rescuing from time to time, and that rescue is always paid for by the taxpayers. • In the current system, profits are privatized, and the costs are socialized, resulting in a massive transfer of wealth from the middle and lower classes to the owner class.