MARKET STRUCTURES AND MARKET FAILURES PERFECT PURE COMPETITION

COMPETITION • A market structure in which producers supply an identical product")

• This")

- Slides: 22

MARKET STRUCTURES AND MARKET FAILURES

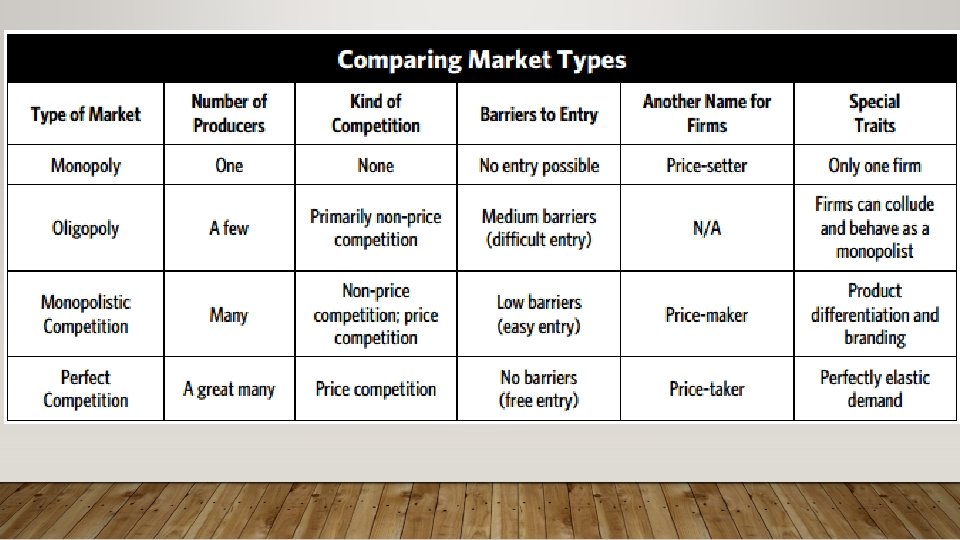

PERFECT (PURE) COMPETITION • A market structure in which producers supply an identical product and no single producer can influence its price. • Prices are set by supply and demand.

MONOPOLY • A market structure in which a single producer supplies a unique product that has no substitutes. • The producer has no competition and alone sets the price.

MONOPOLY EXAMPLES

OLIGOPOLY • A market structure in which a few firms dominate the market and produce similar or identical goods.

MONOPOLISTIC COMPETITION • A market structure in which many producers supply similar but varied products. • Many sellers, low barriers to entry and non-price competition. • i. e. restaurant and hotels.

POSITIVE AND NEGATIVE EXTERNALITIES • One of the reasons why economists value competitive markets is because they seem to lead to an efficient use of resources. All the costs and benefits of a good or service are thought to be reflected in the price of that good or service. • With imperfect competition, though, certain costs or benefits may escape the buyer or seller. • These unaccounted costs or benefits are called externalities or spillovers. They are evidence of market failures.

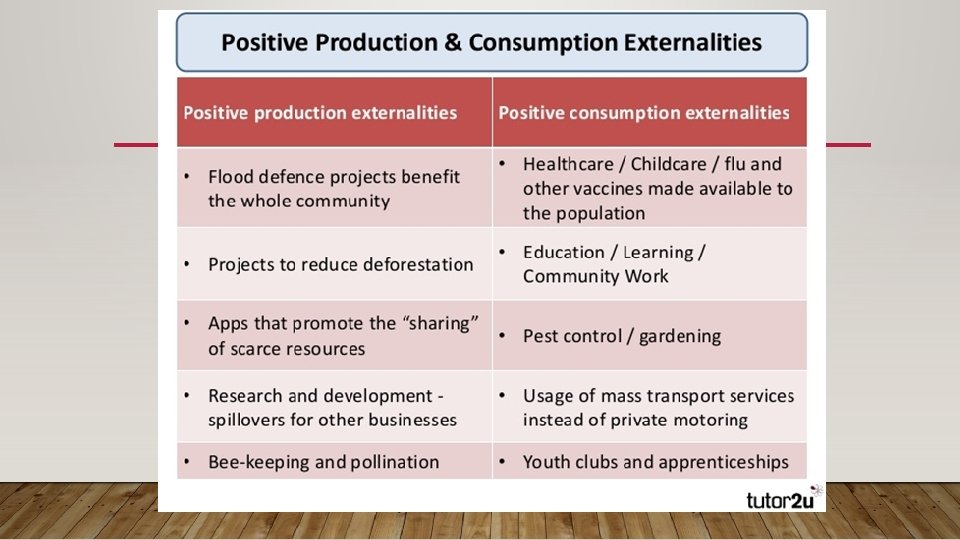

POSITIVE EXTERNALITY • A positive externality is a benefit of production or consumption that falls on someone other than the producer or consumer. It is a positive side-effect of an economic activity that benefits a third party (for instance, society). Education and R & D are typical examples

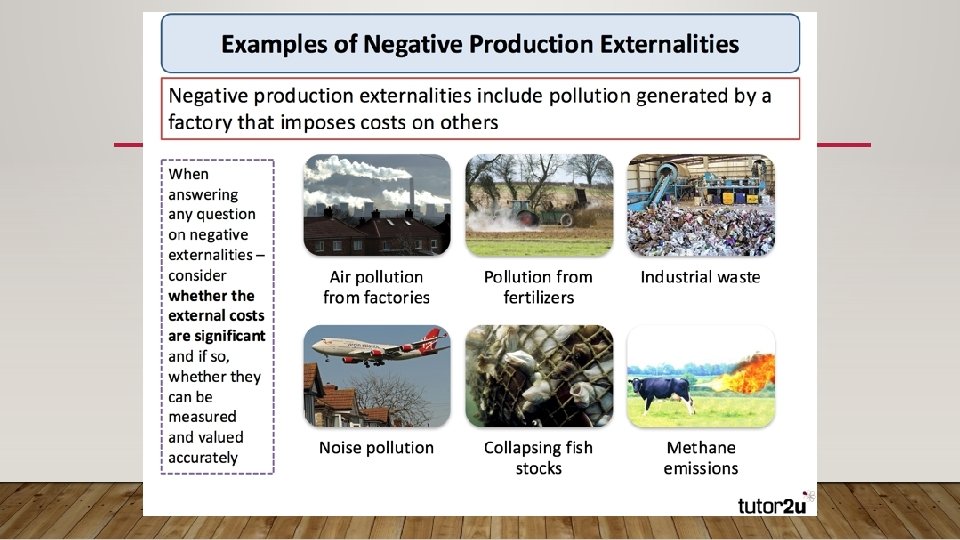

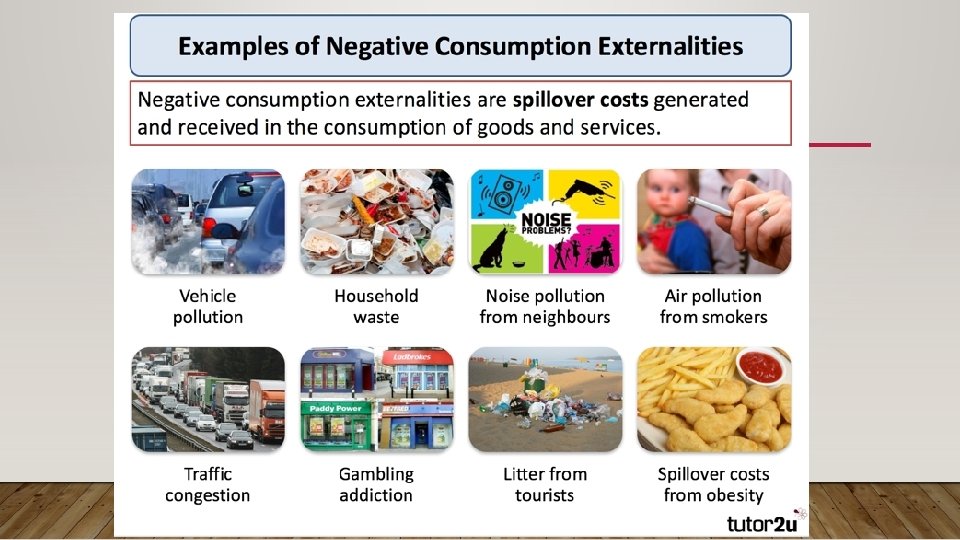

NEGATIVE EXTERNALITY • A negative externality is a cost of production or consumption that falls on someone other than the producer or consumer. It is a negative side-effect of an economic activity. Air or water pollution are examples of a negative externality.

NEGATIVE EXTERNALITY • A negative externality is a form of market inefficiency. We see this in the case of pollution in an unregulated market, where the cost of the pollution is not born by the producer and leads to overproduction

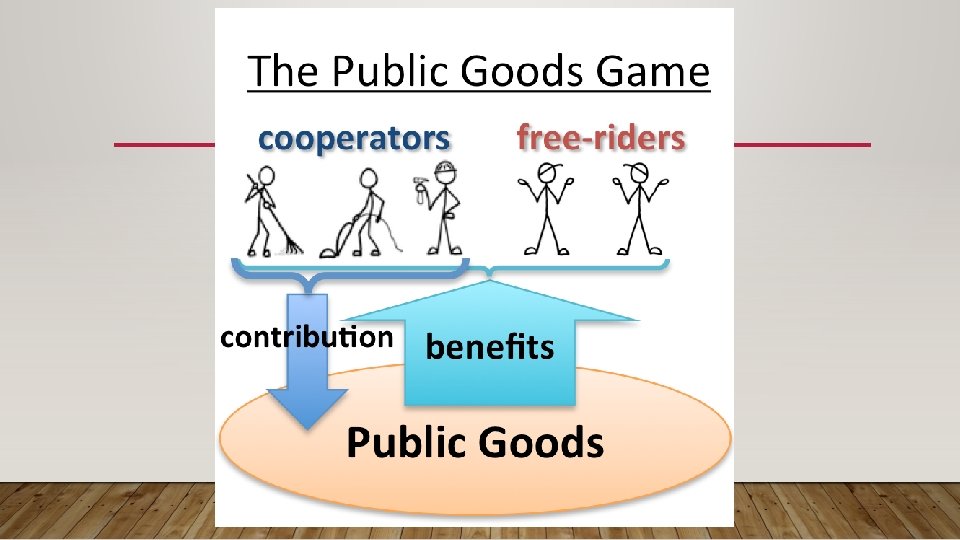

PUBLIC GOODS • Public goods are goods and services that are used collectively and that no one can be excluded from using. Public goods are not provided by markets. Fresh air, national defense, street lights, and lighthouses are all examples of public goods.

THE FREE-RIDER PROBLEM • A free rider is someone who enjoys the benefit of a good or service, such as roads or public schools, without paying for it. Free riding becomes a problem when it leads to the underproduction of that good or service. • An example of a free rider is a worker who does not belong to a union and thus does not have to pay union dues but who would benefit if that union should negotiate a wage increase for all those doing the worker’s job.

TRAGEDY OF THE COMMONS • Tragedy of the commons is a circumstance in which a shared resource is overused or destroyed because users take no responsibility for its preservation. Overfishing and habitat destruction are examples.

COASE THEOREM (FIRST SUGGESTED BY RONALD COASE IN THE EARLY 1960 S) • This theorem states that where externalities are a problem, often a negotiated solution can be found in the market. This is true even in the case of a dispute over who has the right to do something, such as a factory polluting the air. • The key is that the responsibility for these externalities can be identified as well as bought and sold. Transaction costs would also have to be low. If these two conditions can be met, there should be a market solution that can help mitigate the negative effects of externalities.

SUMMARY OF THE DIFFERENT TYPES OF MARKETS