Manufacturing Costs and Job Order Costing Systems UAA

Manufacturing Costs and Job -Order Costing Systems UAA – ACCT 202 Principles of Managerial Accounting Dr. Fred Barbee Chapter

Cost Classifications for Manufacturing Firms

Specify “Tag” the Cost l We C ct ire st o D need to place an adjective (tag) on the cost to identify what it is.

Manufacturing Costs

Manufacturing Costs

General Model of Cost Flow and Accumulation

Cost Flows in a Manufacturing Firm Direct Materials Direct Labor Mfg. Overhead Work-in. Process Finished Goods Cost-of Goods Sold

Cost Flows in a Manufacturing. Costs Firm Manufacturing Direct Materials Direct Labor Mfg. Overhead Costs incurred in the manufacture of goods being produced. Work-in. Process Finished Goods Cost-of Goods Sold • Known as product (inventoriable) costs. • They are expensed when the product is sold.

®Those that become Cost Flows in a materials Manufacturing Firman Direct Materials Direct Labor Mfg. Overhead integral part of the finished product and can be physically traced to the product. ®Those factory labor costs that can be physically traced to. Cost-of the Work-in. Finished Process Goods Sold production of. Goods the finished product. ®All costs associated with the manufacture of a product except direct materials and direct labor.

Direct Materials l DM in Theory l Every l DM component in Reality l Must apply cost-benefit rule

DM – What is Cost? l The invoice price of the raw materials, l Shipping l Import l. A costs, duties, and reduction for any allowable discounts for prompt payment.

MOH – Other Names l Overhead l Burden l Indirect Manufacturing Costs l Factory Expenses

MOH – A Few Examples l Factory Supervision, l Factory Telephone, heat, light, power, l Factory bookkeeping salaries, l Insurance l Depreciation/factory l Indirect equipment materials, labor.

Direct Materials • Known as Direct costs. Period Labor Work-in. Process Nonmanufacturing Costs Cost-of Finished Goods Sold Costs incurred for • They are Mfg. other than production expensed in Overhead old S activities. the period in which they. Sales are Cost of Goods Sold incurred. Income = Gross Margin Statement = Nonmanufacturing Expenses Net Income

®Direct General Materials & Administrative Expenses All executive, organizational, and clerical costs associated with the general Direct Work-in. Finished management Cost-of Labor Goods Sold of the firm. Process ®Mfg. Selling Overhead & Distribution Expenses ld o S customer All costs necessary to secure orders and get the. Sales products/services to the customer. Income Statement = = Cost of Goods Sold Gross Margin Nonmanufacturing Expenses Net Income

Direct Labor Mfg. Overhead Product Costs Direct Materials Work-in. Process Finished Goods Cost-of Goods Sold Sales Income Statement = = Cost of Goods Sold Gross Margin Nonmanufacturing Expenses Net Income Period Costs

Nonmanufacturing Costs

Nonmanufacturing Costs l All costs not associated with the production of goods. l Selling Costs l Administrative Costs

Cost Flows in a Manufacturing Firm

Cost Flows in a Manufacturing Firm Manufacturing Costs DM DL MOH Balance Sheet Unused Used d e i l App WIP DM Inv. Unfinished Fini she d Sales - Income Statement COGS = Gross Margin - S&A = Net Income Sold WIP Inv. FG Inv.

Product and Period Costs

Cost Flows in a Manufacturing Firm Product Costs Manufacturing Costs DM DL MOH Balance Sheet Unused Used d e i l App WIP DM Inv. Unfinished Fini she WIP Inv. d Sales - Income Statement COGS = Gross Margin - S&A = Net Income Sold Period Costs FG Inv.

Cost Flows in a Manufacturing Firm Pro duct Costs Manufacturing Costs DM DL MOH Balance Sheet Unused Used d e i l App WIP DM Inv. Unfinished Fini she d WIP Inv. FG Inv. Sales Product Costs: Costs assigned to products (i. e. , d l COGS So Work in Process Inventory. Income Statement = Gross Margin They “attach” to units of product and - themselves. S&A remain with the product until it is sold. = Net Income

Cost Flows in a Manufacturing Firm Pro duct Costs Manufacturing Costs DM DL MOH Balance Sheet Unused Used d e i l App WIP DM Inv. Unfinished Fini she d Sales - Income Statement COGS = Gross Margin - S&A = Net Income Sold WIP Inv. FG Inv.

Cost Flows in a Manufacturing Firm Sheet Period Costs: Expired non product. Balance costs. Unused DM charged to expense in the period DM Inv. Always in Use d they occur. which Unfinished Used Manufacturing Costs DL MOH d e i l pp WIP Inv. Fini A she d Sales - Income Statement COGS = Gross Margin - S&A = Net Income Sold Period Costs FG Inv.

Product Costs Vs. Period Costs DM, DL, MOH, S&A Costs Product Costs DM, DL MOH S& A Period Costs DM, DL MOH S& A Work-in. Process Finished Goods Selling and Administrative Costs Sale DM , DL MOH Expensed in the current period. Cost of Goods Sold

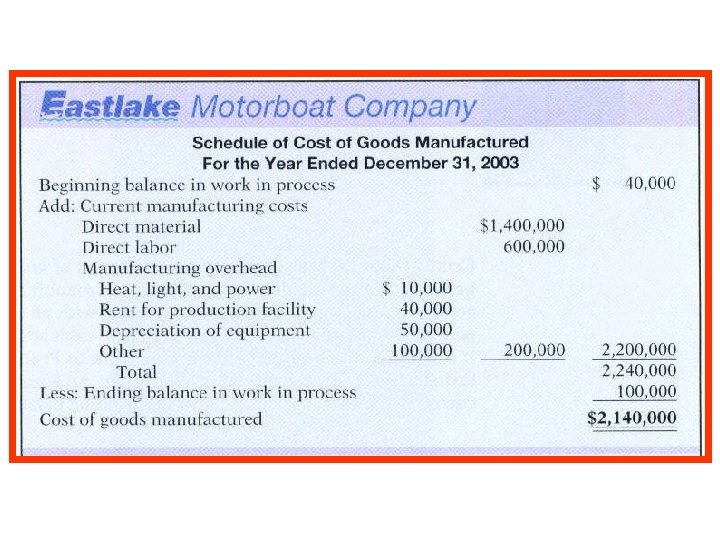

Balance Sheet Presentation of Product Costs

Balance Sheet Presentation

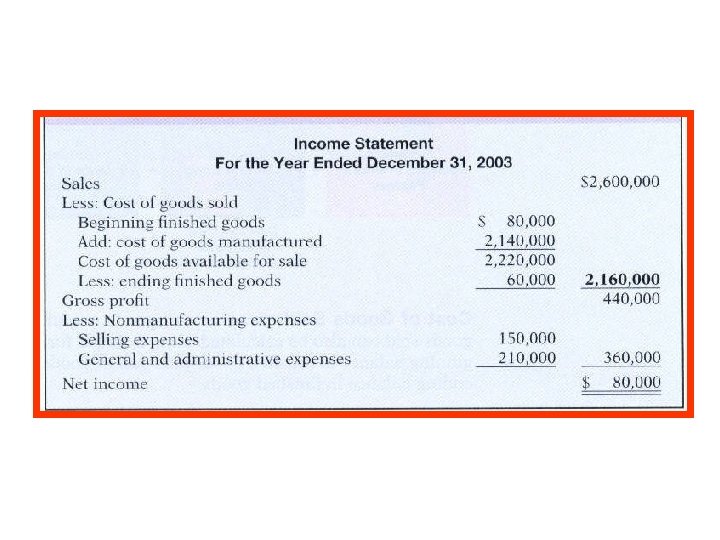

Income Statement Presentation of Product Costs

Income Statement

Direct Materials Used: Beginning inventory Add: Purchases $200, 000 450, 000 Materials available $650, 000 Less: Ending inventory Direct Labor 50, 000 $ 600, 000 350, 000 Manufacturing overhead: Indirect labor $122, 500 Depreciation 177, 500 Rent 50, 000 Utilities 37, 500 Property taxes 12, 500 Maintenance 50, 000 Total manufacturing costs added 450, 000 $1, 400, 000 Add: Beginning work in process Total manufacturing costs Less: Ending work in process Cost of goods manufactured ==== 200, 000 $1, 600, 000 400, 000 $1, 200, 000

Direct Materials Used: Beginning inventory Add: Purchases $200, 000 450, 000 Materials available $650, 000 Less: Ending inventory Direct Labor 50, 000 $ 350, 000 The three component parts of 600, 000 a manufactured product. Manufacturing overhead: Indirect labor $122, 500 Depreciation 177, 500 Rent 50, 000 Utilities 37, 500 Property taxes 12, 500 Maintenance 50, 000 Total manufacturing costs added 450, 000 $1, 400, 000 Add: Beginning work in process Total manufacturing costs Less: Ending work in process Cost of goods manufactured ==== 200, 000 $1, 600, 000 400, 000 $1, 200, 000

Cost of goods manufactured from the COGM Statement. Sales $2, 800, 000 Less cost of goods sold: Beginning finished goods inventory $ 500, 000 Add: Cost of goods manufactured Cost of goods available for sale 1, 200, 000 $1, 700, 000 Less: Ending finished goods inventory Gross margin 300, 000 $1, 400, 000 Less operating expenses: Selling expenses $ 600, 000 Administrative expenses Income before taxes ==== 300, 000 $ 500, 000 900, 000 1, 400, 000

Different Costs for Different Purposes

Product Costing Definitions Value-Chain Product Costs Operating Product Costs Traditional Product Costs Production Marketing Customer Service Research and Development Pricing Decisions Product-Mix Decisions Strategic Profitability Analysis Strategic Design Decisions Tactical Profitability Analysis External Financial Reporting

Value-Chain Product Costs Research and Development Production Marketing Customer Service Pricing Decisions Product-Mix Decisions Strategic Profitability Analysis If making any of these types of decisions, I need to look at all costs.

Operating Product Costs Production Marketing Customer Service Strategic Design Decisions Tactical Profitability Analysis On the other hand, for these decisions, we might be able to ignore some of the costs.

Product Costing Definitions For external Research and financial Development reporting, Production we need only these Marketing costs – because Customer Service that is what GAAP Pricingsays Decisions we need. Strategic Design Product-Mix Decisions Value-Chain Product Costs Strategic Profitability Analysis Operating Product Costs Tactical Profitability Analysis Traditional Product Costs Production External Financial Reporting

Types of Costing Systems

Balance Sheet Presentation

Accumulating Manufacturing Costs Two Types of Costing Systems

Cost Accounting Systems Product Costs Job-Order Costing Process Costing Total/Unit Cost

. l.")

Process Costing l. Homogeneous products continuously produced. l. Costs accumulated by process (time). l. Unit cost = total costs for period divided by number of units produced.

Process Costing System Process A DM DL MOH Process B Process C Finished Goods Cost of Goods Sold

Job-Order Costing l. Wide variety of distinct products. l. Costs accumulated by job. l. Unit cost = total costs of the job divided by number of units in the job.

Job-Order Costing Job 100 DM DL MOH Job 101 Work-in-Process Finished Goods Cost of Goods Sold Job 102 Work in Process Finished Goods Cost of Goods Sold

- Slides: 48