Manufacturing Accounting Manufacturing Accounting Recall Assets are measured

– direct")

• raw materials •")

- Slides: 13

Manufacturing Accounting

Manufacturing Accounting • Recall: – Assets are measured at full absorption cost • Includes all costs of acquiring asset and putting in place – Expenses are measured at the carrying value of the asset sacrificed • Issue: How do we measure all the costs?

Cost Allocation • Same issue exists for merchandising firms • Easier for merchandising, – purchase price (major) – shipping cost (minor) – taxes (minor)

Manufacturing costs • Have to include costs for: – direct materials (major) – direct labor (major) – overhead (major) • utilities, indirect labor, depreciation on plant, etc.

• Have to spread between: – inventory (balance sheet) • raw materials • work-in-process • finished goods – cost of goods sold (income statement)

Review of Cost Classification • Period costs--just like merchandising – not part of inventory/cost of goods sold – can’t be matched to a future benefit – charged to expense as incurred – SG&A, most interest costs, etc. • Product costs--cost of obtaining inventory – originally held in inventory account – charged to cost of goods sold when sold

Manufacturing Product Costs • Direct costs--can be traced to units produced – direct labor – direct materials • Overhead--can’t be traced to units – indirect labor--e. g. , janitorial, supervisory – indirect materials--e. g. , miscellaneous supplies – other--e. g. , depreciation, utilities, rent – allocated to units based on “drivers”

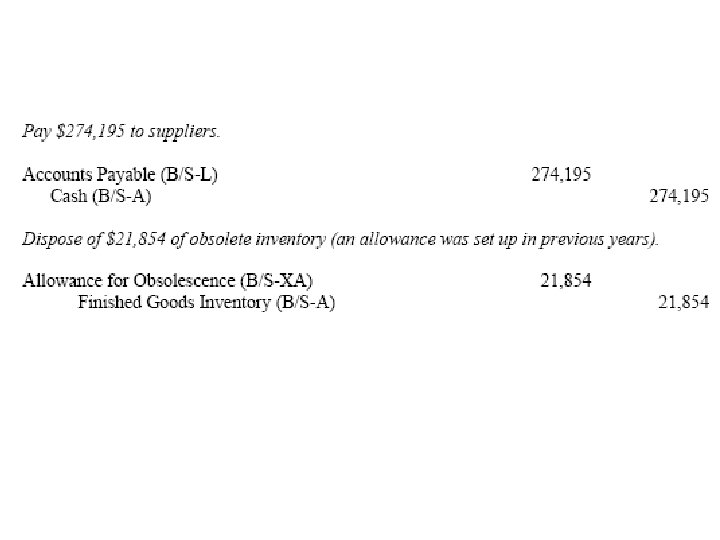

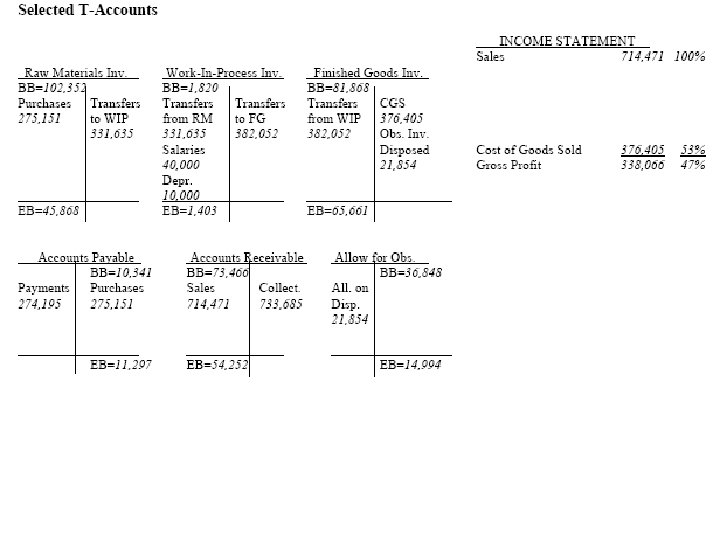

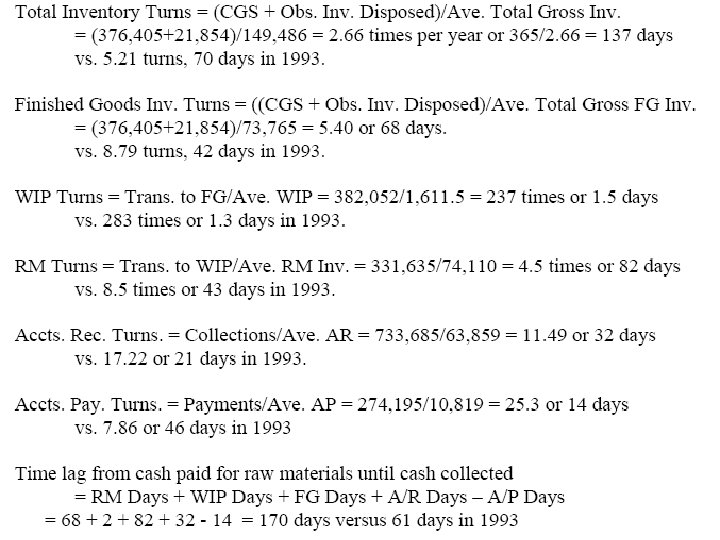

Steps in recording • Place purchases in raw materials inventory • Transfer raw materials inventory to work-in-process inventory when production starts

• Add in direct labor and overhead to WIP • Transfer costs of completed units to finished goods inventory

• Transfer costs associated with sold goods to CGS