Making Economic Decisions Unit 1 Day 2 Opener

- Slides: 12

Making Economic Decisions Unit 1, Day 2

Opener: 8/30/17 Copy these definitions in your binder trade-offs- exchanging one thing for the use of another Opportunity cost - what you cannot buy or do when you choose to do or buy one thing rather than another. Marginal cost - the extra cost of producing one additional unit of output. Marginal benefit - the additional benefit associated with an action.

Trade-Offs • Economic decision making requires that we take into account all the costs and all the benefits of an action. • Economic choices involve trade-offs, or exchanging one thing for the use of another. • For example, when you buy a product, you exchange money for the right to own that product rather than something else you could buy for the same price.

Trade-Offs • People, businesses, and societies make trade-offs every time they choose to use their resources in one way and not in another. • More money for education may mean less money to spend on medical research or national defense.

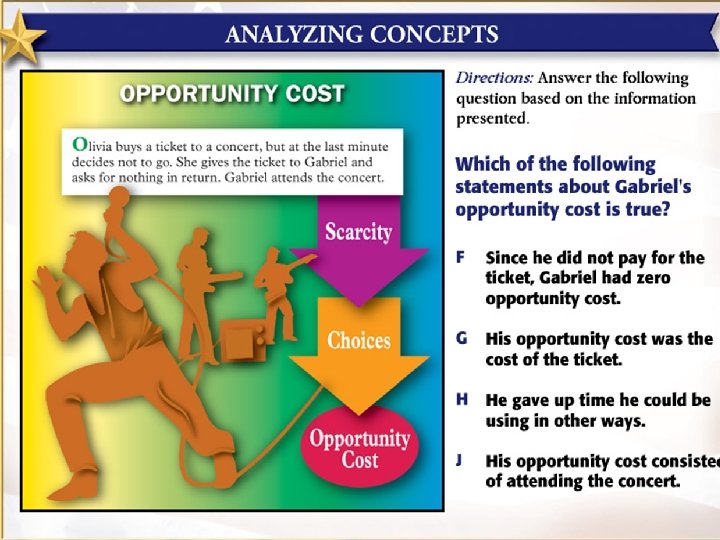

Trade-Offs • Opportunity cost is what you cannot buy or do when you choose to do or buy one thing rather than another. • It is the next best alternative that you had to give up for the choice you made.

Trade-Offs • Opportunity cost includes more than just money. • It also includes the discomforts and inconveniences linked to the choice made. • For example, the opportunity cost of cleaning the house includes not only the price of cleaning products, but also the time you spent cleaning instead of doing something else.

Trade-Offs Measuring costs = • Fixed costs plus variable costs equal total costs. • To find average total cost, divide total cost by the quantity produced. • Marginal cost is the extra cost of producing one additional unit of output. • If it costs an extra $50 to produce one more bicycle helmet, the marginal cost is $50.

Opener 8/31/17 • Your team has a chance to play for your 2 nd straight State Championship, but the game happens to fall on the night of Senior Prom you have to decide what you will miss the game or the prom. You are playing 2 hours from where the prom is so you can’t do both. • Describe how you would make this decision, what you would do, and what the opportunity cost is of your decision.

Trade-Offs • Businesses measure total revenue and marginal revenue to decide what amount of output will produce the greatest profits. • Total revenue equals the number of units sold times the average price per unit. • Marginal revenue is the change in total revenue that results from selling one more unit of output.

Trade-Offs • We usually do something because we expect to achieve some benefit. • Marginal benefit is the additional benefit associated with an action.

Exit Slip • After watching this video https: //www. youtube. com/watch? v=t_N 7 MAr 98 CI&app =desktop Using complete sentences, address the following prompt (5 -7 sentences): How does this video demonstrate the use of a costbenefit analysis? Provide examples from the video.