Looking back is the best basis for Looking

")

Looking back is the best basis for … Looking ahead. (VFB 16 april, 2016)

Long-term value shareholder value has 3 solid pillars q Mission and strategic choices q Solid implementation (‘last domino’) q Culture (‘Performance Ethics’ and ‘Conversation Company’)

Mission : “Shape the bodies and minds of women”

Channel strategy 2004 -2013 Impact on eye and ear of the consumer. Wholesale Retail IV Own stores - R&P III II I - Intimacy - Lincherie (incl. e-com) Franchising - R&P - Lincherie (incl. e-com) 420 customers Lingerie Styling 4. 800 customers Solid basics Operational control

Road : “We follow and improve the fitting room”

‘Performance ethics’ is a culture that combines passion and results. q A company is a bridge of passionate people supporting 2 pillars : customers and shareholders. q There is a mutual duty in life. q Clarity works. q Principles of 4 F : q Focus q Flexibility q Fighting Spirit q Fair Play q Self confidence builds ‘winning’ ‘Winning’ builds self-confidence.

11

In a declining market, over 12 years Vd. V doubled turnover and ebitda and more than quadrupled shareholder value Status 2003 (annual report) Status 2015 (annual report) q Financial data q Financial Data - Turnover : 207 m€ - Turnover : 96, 8 m€ Ebitda : 29, 5 m€ Market Cap (Jan ‘ 04): 254 m€ Enterprise Value : 216, 9 m€ q Key data - 3. 000 independent customers 2 brands 3 own stores - Ebitda : 60, 5 m€ - Market cap (Jan’ 16) : 847 m€ - Distributed dividends & share buy-backs over that period : 315 m€ q Value creation in 11 years : 908 m€ q Key data - 5. 000 independent customers - 3 brands 89 stores (franchised, 0&0, JV)

Turnover more than doubled at CAGR of over 6% 166. 3 250 133. 0 179. 8 181. 8 182. 4 195. 6 206. 7 140. 1 130. 3 123. 0 200 112. 0 94. 6 101. 7 150 100 50 0 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Turnover growth breakdown ‘organic’ vs. ‘acquired’. 210 5 190 13 13 23 170 150 130 206. 7 110 152. 7 90 70 50 30 Turnover Vd. V Intimacy Acquired Donker R&P UK Andres Sarda 14

Ebitda more than doubled at CAGR of nearly 7% 44. 6 43. 4 44. 2 52. 3 53. 8 48. 7 55. 9 60. 5 41. 1 70 38. 1 60 33. 5 29. 5 50 40 30 20 10 0 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ebitda growth breakdown as ‘organic’ vs. ‘acquired’. 65 0. 1 60 55 1 0. 9 1. 3 60. 5 57. 2 50 45 Ebitda Vd. V Intimacy Acquired Donker R&P UK Andres Sarda 16

Van de Velde created 908 million € shareholder value in 12 years, which is an IRR of nearly 15% 315 908 million € 847 254 2004, Jan 1 2016, Jan 1

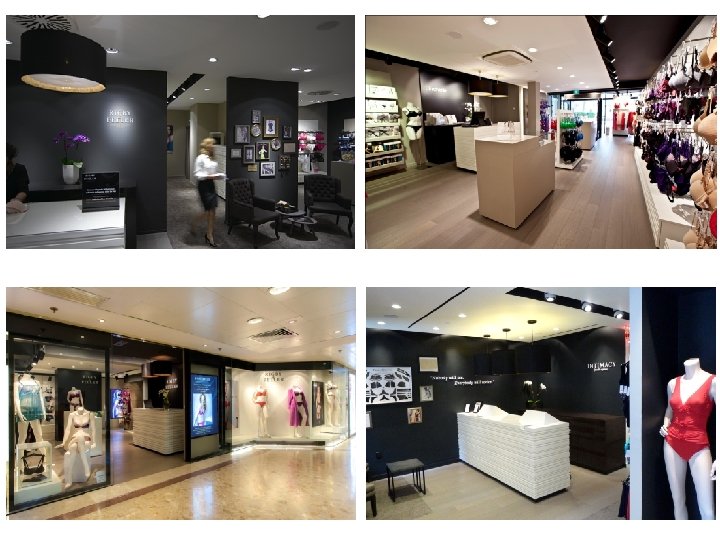

Building blocks of our growth route M&A activities Organic growth initiatives q Brands § § § Prima. Donna Twist. Prima. Donna Swim. Marie Jo Intense Optimise brand spending Pricing upside q Channel § § § Improve and expand sales force. Develop value added services. Develop ‘Lingerie Styling’ program. Enter new countries. Launch e-com q Cost § Close Hungary. § Cost optimizations across system. q Acquire wholesale distribution (< 1 m€) § Switzerland importer. § Agents in North America, Spain. q Acquire Andres Sarda (17 m€) q Acquire Retail (35 m€) § § Intimacy (USA) Lincherie, Donker (NL) Rigby & Peller (UK) JV Getz (Hongkong & China)

What about the next 12 years ? q Always think infinity. q We will continue to work on 3 levers; q Brands to consumers. q The concept of the fitting room. q Supply chain improvements. q Culture (‘performance ethics’ and ‘conversation company’)

We serve a real and well identified need. We follow a clear route. The growth potential of both combined has no end. Why do we exist ? Every woman sees her breasts and figure as important in her self-experience of beauty and femininity. We enhance emotional and physical confidence for women by marketing lingerie and swimwear that provides them more comfort and makes them feel more beautiful. We follow and improve the fitting room experience. By supporting specialty retailers and providing brands and concepts that improve consumer experience and loyalty. By developing the fitting room concepts of the future and coupling technologies, improved consumer service and product delivery systems that encourage consumers to discover the benefits of beauty (fit / style / fashion). What is our strategic ambition ? Today, we ‘only’ serve 0, 1% of the female world population. constrained only by branding and distribution. Our limitations to growth are Our strategic segmentation is ‘Trading Up’. We will only compete in environments with high brand aspirations, high service deliveries, high margins, high consumer experience and consumer loyalty. 20

With the consumer at the center, we build a system of brand aspiration and channel service so as to ensure life long loyalty (2013 -2015) CHANNEL BRAND Wholesale store LS home party Marie Jo LS website LS e-shop Prima. Donna Consumer R&P franchisee R&P store Andres Sarda LS experience center LS new technologies Wholesale channel LS ‘disruptive models’ Retail channel Channels under development LS: Lingerie Styling 21

Important choices for the future. No longer ‘retail’ vs. ‘wholesale’, but channel. q New interesting combinations are actively being tested. q Traditional retail is the ‘least attractive’ growth combination, expressed in ROCE. q International doors open in different ways (eg. USA, India, Poland …) Strongly lead ‘big cup sizes’ in premium category. Only ‘Trade up’.

- Slides: 22