Long Term Care Insurance Uncertainty today whats next

market • Group LTCi situation •")

- Slides: 39

Long Term Care Insurance: Uncertainty today …. what’s next? John O’Leary President O’Leary Marketing Associates December 11, 2012 O’Leary Marketing Associates, 2012 1

Why am I here? Irene O’Leary � Born Mar 7, 1918 � Diagnosed 1993 @ age 75 � Died Oct 23, 2004 � 11 years with Alzheimer’s Rita Maffione � Born Jan 29, 1926 � Diagnosed 2001 @age 75 � Died Mar 4, 2012 � 11 years with Alzheimer’s

Today’s agenda • Long Term Care insurance (LTCi) market • Group LTCi situation • Individual LTCi situation ◦ Contributing factors • Market and situational factors • Economics • Healthcare • LTCi and the future O’Leary Marketing Associates, 2012 3

LTCi an $11 billion category serving 7 million plus consumers Adapted from LIMRA 2011 LTCi In force market data O’Leary Marketing Associates, 2012

Group Observations O’Leary Marketing Associates, 2012 5

Group market: Key carriers exit O’Leary Marketing Associates, 2012

Carrier exits result in large group “closed block” issue *Adapted from 2011 LIMRA Group In Force data ** Includes FLTCIP and CALpers O’Leary Marketing Associates, 2012

Group Issues • Lack of Competition • Has created huge demand/supply imbalance • Little room for “New “sales –cherry picking • High number of “closed block” cases • Employer/broker damage–highly skeptical • Who, if anyone, can fill void? • Group contributing factors –LOW INTEREST RATES exacerbated by: • Long tail (employee average purchase age < 50 ); • Guaranteed issue; Low participation • Fit with other “group products” i. e. capital requirements O’Leary Marketing Associates, 2012 8

Group Assessment • Unfortunately, Group Channel is in “dire straits” • Group provides efficient and broad consumer access • Old players unlikely to return • Hancock possible exception • Old business model hasn’t worked for many • Infusion of new thinking, new models, new players • Opportunities • Closed block management • New sales to ER s with closed blocks • New sales to ERS who haven’t yet bought �Individual Multi-Life; Transition product; others • New approaches that balance consumer need with carrier risk O’Leary Marketing Associates, 2012 9

Individual LTCi Observations O’Leary Marketing Associates, 2012 10

Individual LTCi: Dramatic rate actions make headlines Source: Long term care insurance articles in consumer press-Chicago sun times etc… O’Leary Marketing Associates, 2012

Individual market dynamics • Important carriers have left the business, but key carriers remain • Companies include: Genworth, Hancock, Transamerica, Med. America, Life Secure • Mutuals include: Northwestern, Mutual of Omaha and New York Life • Unlike group -over 80% of the business remains with active carriers • There is a clear “market leader” - 40% plus share • Can lead in pricing/risk management/innovation? • Highly analytical, most claims experience • Broadest distribution access • Management committed to business O’Leary Marketing Associates, 2012 12

Remaining Individual Carriers • AGGRESSIVELY MANAGING RISKS: • Adjusting pricing: Across the board premium hikes; retro and prospectively; Upward adjustment of female rates (NOTE: AFFORDABILITY ALREADY #1 BARRIER TO SALES) • More restrictive underwriting: Family history; More uninsurable conditions i. e. schizophrenia, tobacco use ; Blood and fluids? • Limiting benefits: Elimination of lifetime; cash benefits; limited pay options • Reducing consumer discounts; haircuts on agent commissions • Some interesting product initiatives –Hancock, Med America- Recognition of need to change O’Leary Marketing Associates, 2012 13

Key issues • Short term- restricting product access to the “healthier and wealthier” • Short term fix or long term strategy-Niche versus Growth • Are affordable product options possible today? • Can Underwriting be made more palatable? NOTE *ACA IS GI FOR HEALTH • Longer term • There’s room for Innovation- Is there appetite? • There’s a need for new players- Are there attractive opportunities? • Other • Industry reputation • Distribution commitment • Under priced legacy business-continuing drag? O’Leary Marketing Associates, 2012 14

Contributing factors to how we got where we are O’Leary Marketing Associates, 2012 15

What’s behind carrier actions? • HISTORICALLY LOW INTEREST RATE ENVIRONMENT • LTCi-Already considered “Risky” due to long tail • Initial actuarial assumptions – too optimistic • Lapse rates lower than assumed • Morbidity higher • Mortality lower • Costly plan designs-i. e. Mandated offer- 5% ABI • Result: “Perfect Storm” for LTCi O’Leary Marketing Associates, 2012 16

What’s behind carrier actions? Company situational factors. . . O’Leary Marketing Associates, 2012

What’s behind carrier decisions? Look at the business risks HI Key Decision Variables REWARD • High capital requirements • Questionable predictability • Long time horizon • High financial uncertainty • Low market penetration • Heavily Regulated • Strategic fit ? HI RISK HI REWARD LO LTC Target LO RISK LO REWARD HI RISK LO REWARD LTC Future ? RISK O’Leary Marketing Associates, 2012

Overall Assessment and opportunities Individual LTCi is at a “tipping point” • • Current actions reinforce a “niche” positioning Question: Will the industry undertake innovation required to meet broader range of consumer needs? Opportunities: • Better balance carrier risk with consumer needs • Broaden product appeal beyond “healthy/wealthy” • New thinking to find alternate ways to address emerging long term care crisis O’Leary Marketing Associates, 2012 19

Market and situational factors O’Leary Marketing Associates, 2012 20

Demand: Senior population doubles in the next 30 years Table 12. Projections of the Population by Age and Sex for the United States: 2010 to 2050 (NP 2008 -T 12) Source: Population Division, U. S. Census Bureau O’Leary Marketing Associates, 2012

Cost and need for long term care continues to accelerate O’Leary Marketing Associates, 2012

Future demand is growing; consumer choices shrinking Carriers opting out/raising rates Consumer demand for services rising Cost of Care High and growing CLASS Act deemed not executable The coverage gap widens Medicaid belt tightening Reverse mortgage equity down Inadequate Retiree Savings O’Leary Marketing Associates, 2012

US Family economics- income and age Changes in U. S. Family Finances from 2007 to 2010: Evidence from the Survey of Consumer Finances; Federal Reserve Bulletin June 2012

Takeaways family economics • • • 75% of families don’t have sufficient net worth (including home equity) to self fund 2 years in a Nursing Home at US average Half of seniors couldn’t self fund 3 years of Nursing Home care from net worth Upper 10% -15% of families have sufficient income to pay for long term care protection. Many have sufficient assets to co-insure or fund a significant long term care event Likely family targets for long term care insurance: • Priority Target-Top 20% ~23 million families • Secondary Target- 50 -80% ~35 million families • Not a likely target- Bottom 50% ~58 million • O’Leary Marketing Associates, 2012 25

Healthcare costs person skews heavily to age 65 plus Average Spending Person Age (in years) <5 $2, 468 5 -17 1, 695 18 -24 1, 834 25 -44 2, 739 45 -64 5, 511 65 or Older 9, 744 Sex Male Female $3, 559 4, 635 Source: Kaiser Family Foundation calculations using data from U. S. Department of Health and Human Services, Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey (MEPS), 2009.

Healthcare observations • • • Healthcare is in the midst of a dramatic changes -in part, but not totally due to ACA • In Massachusetts seeing emphasis on cost reductions -provider/insurer collaborations; focus on outcomes • New payment delivery models- fee for service on the way out; pay for outcomes coming …. • (Big) Data-genomics analyses; Electronic medial records; diet and activity monitoring Consumers being forced to be in charge • Higher deductibles and co-pays Innovative wellness programs becoming ubiquitous • Shape up • Healthrageous/ Wellocracy • Live + well-Genworth O’Leary Marketing Associates, 2012 28

News Flash: Scientists concerned with aging are now seeing lifestyle impacts O’Leary Marketing Associates, 2012

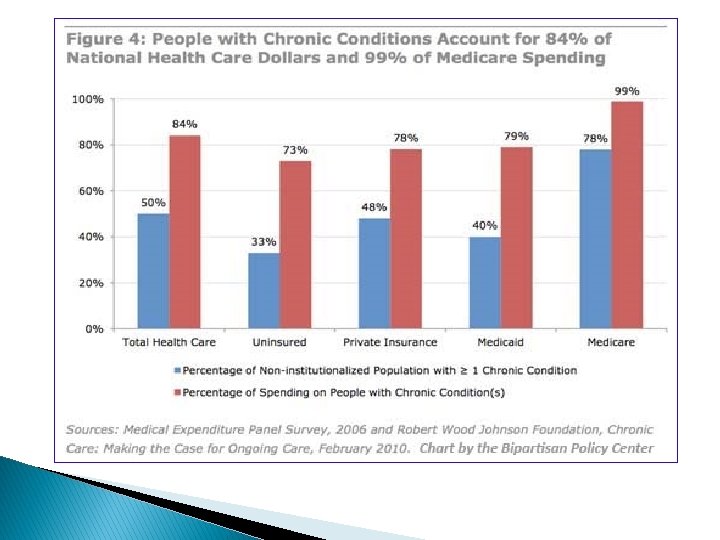

More healthcare observations • Increasing recognition that earlier knowledge and intervention can ameliorate later problems • • • Alzheimer’s issues begin way before symptoms Dr. Deborah Blacker head MGH gerontology “Research is uncovering relationships between Alzheimer’s and diabetes, high BP, high cholesterol, cardio and sleep disorders” Leading to a greater Healthcare focus on senior care and chronic conditions • • That’s where the costs are Two of the Boston leading hospitals have homecare subsidiaries; others have programs O’Leary Marketing Associates, 2012 30

LTCi and the future ? It depends… O’Leary Marketing Associates, 2012 31

Tighten U/W For long term care carriers risk mitigation is key Limits Audience Adjust Premiums Already High Reduce Benefits If lowers costs Share Risks Open to consider Manage Health Uncharted potential But what about consumer needs?

Assessment: Current approaches O’Leary Marketing Associates, 2012 33

Current LTCi products Assessment: Individual LTCi likely to remain a high end niche product without substantial changes; Group market begs for “disruptive innovation”

Current LTCi products Assessment: Proving viable as a small employer product; not yet viable for mid and large sized employers without group infrastructure adds.

Risk limiting approaches Assessment: Each approach holds promise, has potential barriers. Consumer feedback, marketing analysis, consumer research and segmentation may be able to hone future modifications.

Health Management Assessment: While results are unproven, the latest research suggests strong correlations between healthy lifestyles and minimizing chronic conditions and diseases. Warrants further investigation.

Thoughts to leave you with… • • • LTCi at a tipping point-niche vs. growth Private Insurance just one solution-other public/non-profit/private solutions Wellness and Healthcare related to LTC Stakeholder involvement broad Opportunities for “disruptive innovation” and out of the box thinking Remember: the Consumer and that funding is not unlimited O’Leary Marketing Associates, 2012 38

Thank You Questions or further discussion? John O’Leary President OLeary Marketing Associates John. VOLeary@Verizon. net 978 -258 -3567 978 -382 -8227 (mobile) O’Leary Marketing Associates, 2012 39