LOCAL ACCOUNTING STANDARDS INTERNATIONAL STANDARDS WHICH TRANSITIONAL PROCESS

NON")

- Slides: 27

LOCAL ACCOUNTING STANDARDS / INTERNATIONAL STANDARDS: WHICH TRANSITIONAL PROCESS Mr. Salah ESSAYEL CONSEIL DU MARCHE FINANCIER OF TUNISIA 2013 TAFCM- September 20 th, 2013 - Istanbul

KEY TOPICS GENERAL INTRODUCTION - - SUMMARY OF THE CORPORATE ACCOUNTING SYSTEM - SUMMARY OF THE INTERNATIONAL BENCHMARK (IFRS) POSITIONING THE TUNISIAN ACCOUNTING SYSTEM: SIMILARITIES & DIFFERENCES BETWEEN IFRS AND THE TUNISIAN ACCOUNTING SYSTEM - - SMEs ACCOUNTING STANDARDS - ADOPTION PROCESS OF IFRS IN TUNISIA IMPACT OF THE ADOPTION OF IFRS IN TUNISIA - REPORTING REQUIREMENTS ON THE TUNISIAN CAPITAL MARKET -

WHY IMPLEMENTING IAS- IFRS ? • • • THE FOR LOGIC & RELEVANCE OF THE BENCHMARK INVESTORS AND THE MARKET. AN INCREASINGLY DEMANDING INTERNATIONAL ENVIRONMENT: the implementation of the IAS – IFRS benchmark is an entry ticket to the international markets and the global economy. THE WORLWIDE IMPLEMENTATION OF IAS- IFRS WHICH WILL DEVELOP THE INTERNATIONAL EXCHANGES REALATING TO ACCOUNTING SERVICES.

OVERVIEW OF THE TUNISIAN ACCOUNTING BENCHMARK

THE CORPORTAE ACCOUNTING SYSTEM CONSISTS OF: THE ACCOUNTING LAW: enacted on December 30 th, 1996 and consisting of 5 chapters relating to accounting legal and organizational issues. - - THE CONCEPTUAL FRAMEWORK THE ACCOUNTING STANDARDS SUB-DIVIDED AS FOLLOWS: * THE GENERAL PRESENTATION STANDRAD * THE TECHNICAL STANDARDS * THE SECTORAL STANDARDS -

ACCOUNTING STANDARD N° 1 : GENERAL STANDARD DEFINES THE FINANCIAL STATEMENTS PRESENTATION TEMPLATE - DEFINES THE RULES & PRINCIPLES GOVERNING THE ACCOUNTING ORGANIZATION - - DEFINES THE ACCOUNTING TERMINOLOGY APPLIES TO COMPANIES’ FINANCIAL STATEMENTS AND ACCOUNTING ORGANIZATION - APPLIES TO COMPANIES SUBJECT TO THE SECTORAL STANDARADS WHERE THERE IS NO EXCEPTIONS -

SECTORAL STANDARDS - DEDICATE A PART SEPCIFIC TO INTERNAL CONTROL SYSTEMS AND ACCOUNTING ORGANIZATION IN ADDITION TO ACCOUNTS’ TERMINOLOGY. - THE TUNISIAN SYSTEM ALSO PROVIDES FOR PRACTICAL RECOMMENDATIONS (for instance: concerning factoring companies / for REPO treatment

OVERVIEW OF THE INTERNATIONAL ACCOUNTING BENCHMARK

INTERNATIONAL ACCOUNTING BENCHMARK A- DEFINITION OF IAS / IFRS BENCHMARK COVERS THE STANDARDS AND INTERPRETATIONS ISSUED BY THE IASB: INTERNATIONAL ACCOUNTING STANDARDS: IAS • INTERNATIONAL STANDARDS OF FINANCIAL REPORTING: IFRS • RELATED INTERPRETATIONS BY THE RELEVANT BODIES • SUBSEQUENT AMENDMENTS TO THESE STANDARDS AND THEIR RELATED INTERPRETATIONS • STANDARDS AND INTERPRETATIONS TO BE ISSUED / PUBLISHED BY THE IASB •

INTERNATIONAL ACCOUNTING BENCHMARK B- STANDARD-SETTING APPROACH OF IASB & OF IAS / IFRS STANDARDS: IASB APPROACH BASED ON 6 POINTS: - Inspired by the anglo-saxon system and dedicated to investors • based on an approach reflecting the economic activity reality taking into account the market • a benchmark disconnected from any leagl or tax context • the treatment of the accounting operations is based on identical accounting principles • a global benchmark dealing with the accounting rules as well as the financial reporting • a compulsory implementation of all the standards and the interpretations •

INTERNATIONAL ACCOUNTING BENCHMARK STANDARD-SETTING APPROACH OF IAS / IFRS STANDARDS: - Main objective: providing investors for their investment decisions with better information regarding the instantaneous value of the economic entity and the risks involved taking into account its market value. Approach: based mainly on the following: -Prevalence of the income over the profit/loss statement - Introduction of « fair value » concept - Prevalence of the substance over the form - measurement of losses and assets’impairment…

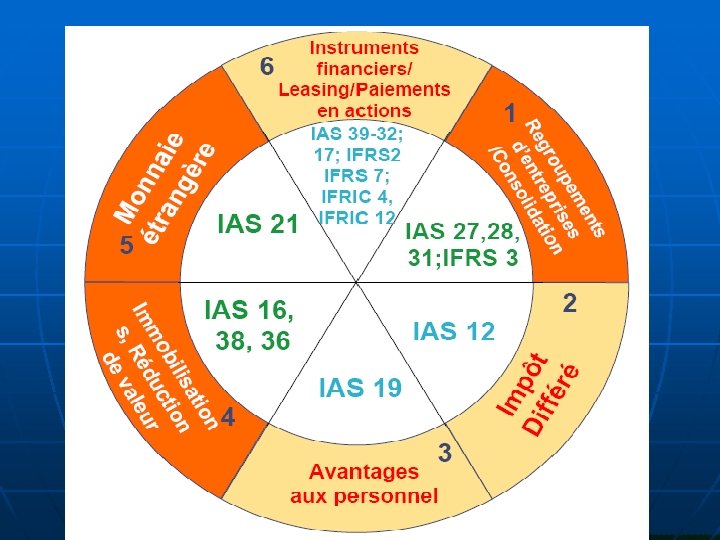

INTERNATIONAL ACCOUNTING BENCHMARK C- CONCEPTUAL FRAMEWORK & BASIC ACCOUNTING PRINCIPLES IT REPRESENTS THE GENERAL FRAMEWORK APPLICABLE TO ALL COMPANIES MAKING ACCOUNTS IN ACCORDANCE WITH IFRS BENCHMARK AND ALLOWS THEM TO REFER TO BASIC CONCEPTS REGARDING THE PARTS INCLUDED IN THE FINANCIAL STATEMENTS. • D- FINANCIAL REPORTING STANDARDS 1. STANDARDS OF FINANCIAL REPORTING (financial statements / additional information) PRESENTATION ( IAS 1/ IAS 7 / IAS 8 / IAS 10/ IFRS 8/ IAS 24 / IAS 33 / IAS 34). 2. Reporting perimeter (IAS 27 / IAS 28 / IAS 31/ IFRS 3/ IFRS 5)

INTERNATIONAL ACCOUNTING BENCHMARK 3. SECTORAL STANDARDS - FINANCIAL SECTOR (IAS 26/ IFRS 4) NON FINANCIAL SECTOR (IAS 41 / IFRS 6) 4. ASSESSMENT & REGISTRATION STANDARDS - NON- FINANCIAL ASSETS AND LIABILITIES ASSESSMENT (IAS 2 / IAS 16/ IAS 36 / IAS 38/ IAS 40/ IAS 17/ IAS 19/IAS 23…) FINANCIAL INSTRUMENTS ASSESSMENT (IAS 32/ IAS 39/ IFRS 2/ IFRS 7…) - Assessment of income and prices’fluctuation (IAS 11/ IAS 12/ IAS 18/ IAS 15/ IAS 21…) - -

POSITIONING OF THE TUNISIAN ACCOUNTING SYSTEM : SIMILARITIES & DIFFERENCES BETWEEN IFRS AND THE TUNISIAN ACCOUNTING SYSTEM

IFRS AND SMEs

MAIN ISSUE -IFRS FOR SMEs: are they an option or a need with respect to the Tunisia context and taking into account the costs/ advantages analysis as well as the available accounting expertise? - What is the organizational and informational impact involved? -

2 STANDARD-SETTING APPROACHES US-GAAP US GAAP IFRS Concept More Less Underlying principles Choice Details level Rules Less More

2 STANDARD-SETTING APPROACHES AMERICAN APPROACH BASED ON DETAILED RULES: Giving rise to an increasing complexity resulting from the quantity & level of details - - risk of structuring of accounting operations and data. INTERNATIONAL APPROACH BASED ON PRINCIPLES: -Giving an important place to interpretation and professional judgement -Less numeric thresholds - less available options. NEED FOR CONVERGENCE: Only one benchmark in order to make easier the comparaison of companies’ financial performances and the listing process on a foreign capital market.

IN THE TUNISIAN CASE A. - - - THE PREREQUISITES TO TRANSITION The system general consistency with the basics of the international benchmark The availability of a conceptual framework Adoption of the memorandum on the prevalence of substance over form Similarities with respect to communication tools and particularly regarding the financial statements’components (balance sheet / profits-loss statement / cash-flow statement and the notes) Adoption of the classification of expenses by destination and setting indicators to be used as measurement and assessment tools of companies’ performances Staff training …

IN THE TUNISIAN CASE B. IMPEDIMENTS TO THE ADOPTION OF IAS/ IFRS The difficult process of upgrading the tax system in accordance with the requirements of IAS / IFRS adoption IFRS are designed in the developped countries’environment and based on the anglosaxon culture - IFRS adoption entails a number of reforms: accounting law, tax system, corporate law, commercial law… - costs of introduction of the benchmark -

IN THE TUNISIAN CASE C- OBSTACLES THE TAX REGULATION INTO FORCE - INCONSISTENCY OF THE PRACTICES WITH THE KEY CONCEPTS OF IFRS: * « fair value » concept * complexity of some accounting treatments - - LOGISTIC SUPPORT & COSTS OF TRANSITION

IMPACT ON FINANCIAL STATEMENTS • Concerning equities: (the re-estimation of the useful lifetime of assets) • Concerning the results (review of depreciation allowances) • The net debt level (capitalization of leasing agreements).

A LARGER IMPACT Building the accounting & financial capacity and improvement of the monitoring bodies - Decompartamentalising and structuring accounting and financial functions - the Enhancing the internal control as well as the internal and external audit functions - Involvment information - - of quality control in financial involvment of the legal department in the project.

REPORTING REQUIREMENTS ON THE TUNISIAN CAPITAL MARKET A- PERIODIC INFORMATION REPORTING IS REQUIRED ON A REGULAR BASIS: Quarterly : (activity indicators) - Half-yearly: interim financial statements, auditor report Yearly: yearly financial statements, auditor report, companies’management report… - B- ON-GOING INFORMATION ANY SIGNIFICANT INFORMATION LIKELY TO HAVE AN IMAPCT ON THE MARKET HAS TO BE DISCLOSED TO THE PUBLIC

REPORTING REQUIREMENTS ON THE TUNISIAN CAPITAL MARKET C- OCCASIONAL INFORMATION: disclosed on the occasion of financial operations on the market (capital increase / listing on the stock exchange / bonds’issuance / a takeover bid…) DCMF MONITORING OF DISCLOSURE REQUIREMENTS COMPLIANCE WITH Monitoring aspects: the deadline for submitting information / The information details as specified in the Law / The consistency of the information… - Enforcement actions likely to be taken by the regulator: - soft actions (reminders: public and nominative ones) - sanctions (financial penalties, issuing orders…) -

THANK YOU