LKAS 12 Income Tax Rangajewa Herath B Sc

(Hons.")

LKAS 12: Income Tax Rangajewa Herath B. Sc. Accountancy and Financial Management(Sp. ) (Hons. ) (USJ) , Master of Business Administration -PIM(USJ)

LKAS 12: Income Tax

Accounting Profit vs Taxable Profit Accounting Profit Permanent Differences Taxable Temporary Differences Deferred Tax Liability Taxable Profit (Taxable Income) Temporary Differences Deductible Temporary Differences Deferred Tax Asset

Objective • The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes is how to account for the current and future tax consequences of: (a) the future recovery (settlement) of the carrying amount of assets (liabilities) that are recognised in an entity’s statement of financial position; and (b) transactions and other events of the current period that are recognised in an entity’s financial statements.

Definitions • Accounting profit is profit or loss for a period before deducting tax expense. • Taxable profit (tax loss) is the profit (loss) for a period, determined in accordance with the rules established by the taxation authorities, upon which income taxes are payable (recoverable). • Tax expense (tax income) is the aggregate amount included in the determination of profit or loss for the period in respect of current tax and deferred tax.

in respect")

Definitions • Current tax is the amount of income taxes payable (recoverable) in respect of the taxable profit (tax loss) for a period. • Deferred tax liabilities are the amounts of income taxes payable I future periods in respect of taxable temporary differences. • Deferred tax assets are the amounts of income taxes recoverable in future periods in respect of: (a) deductible temporary differences; (b) the carry forward of unused tax losses; and (c) the carry forward of unused tax credits.

Definitions • Temporary differences are differences between the carrying amount of an asset or liability in the statement of financial position and its tax base. Temporary differences may be either: (a) taxable temporary differences, which are temporary differences that will result in taxable amounts in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled; or (b) deductible temporary differences, which are temporary differences that will result in amounts that are deductible in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled.

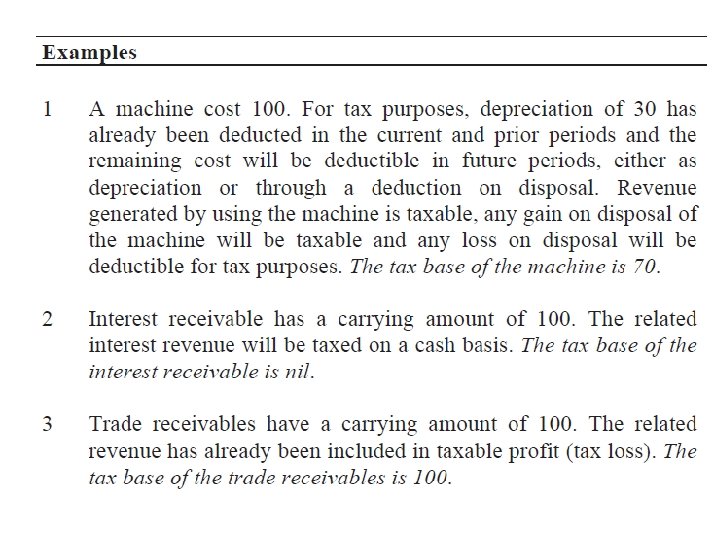

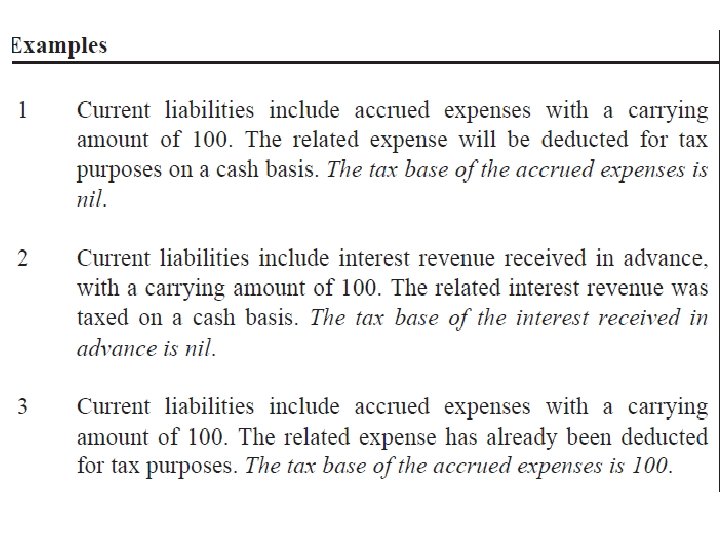

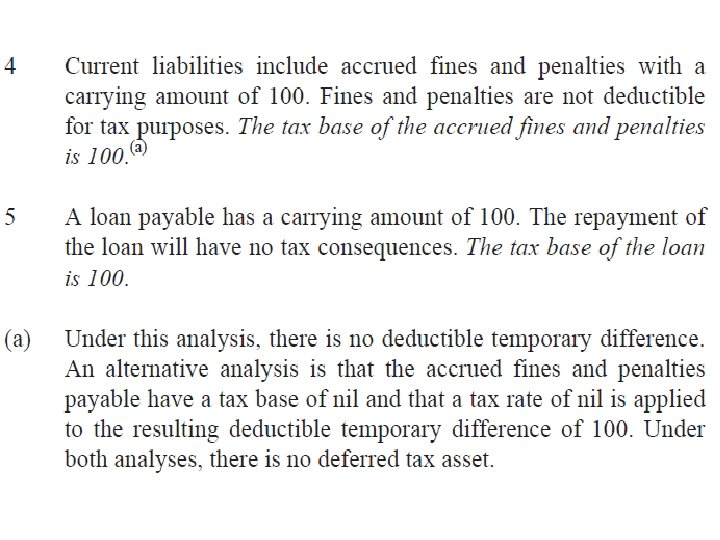

Definitions • The tax base of an asset or liability is the amount attributed to that asset or liability for tax purposes.

Exercise 1 • ABC PLC incorporated on 01. 04. 2015 and the income tax paid under self assessment for the year ending 31. 03. 2016 was Rs. 800, 000 and the total income tax liability for the year was estimated as Rs 1, 200, 000. Deferred tax liabilities and deferred tax asset as at 31. 03. 2016 were Rs. 350, 000 and Rs. 150, 000 respectively. The income tax paid under self assessment for the year ending 31. 03. 2017 was Rs. 900, 000 and the total income tax liability for the year was estimated as Rs 1, 250, 000. Deferred tax liabilities and deferred tax asset as at 31. 03. 2017 were Rs. 750, 000 and Rs. 350, 000 respectively. Required: 1. Prepare the income tax expense account, deferred tax assets and liability accounts 2. Extracts of the financial statements for 2015/16 and 2016/17.

Exercise 2 • XYZ Pl. C incorporated on 01. 04. 2015 and the income tax paid under self assessment for the year ending 31. 03. 2016 was Rs. 600, 000 and the total income tax liability for the year was estimated as Rs. 900, 000. Taxable and deductible temporary differences as at 31. 03. 2016 were Rs. 800, 000 and Rs. 450, 000 respectively. Income tax rate is 25%. • Income tax paid under self assessment for the year ending 31. 03. 2017 was Rs. 750, 000 and the total income tax liability for the year was estimated as Rs. 950, 000. Taxable and deductible temporary differences as at 31. 03. 2017 were Rs. 1, 200, 000 and Rs. 750, 000 respectively. Income tax rate is 25%. Required: 1. Prepare the income tax expense account, deferred tax assets and liability accounts 2. Extracts of the financial statements for 2015/16 and 2016/17.

Exercise 3 Global Pl. C incorporated on 01. 04. 2015. The following information is provided. Income tax paid for the year ending Total income tax liability for the year ending Carrying amount – Plant and machinery Tax base-Plant and machinery Carrying amount – Motor vehicles Tax base-Motor vehicles 31. 03. 2016 ( Rs. 000) 600 925 4, 000 3, 000 2, 400 31. 03. 2017 ( Rs. 000) 500 800 2, 000 1, 800 • Income tax rate is 25%. Required: 1. Prepare the income tax expense account, deferred tax assets and liability accounts 2. Extracts of the financial statements for 2015/16 and 2016/17.

Exercise 4 The following information is provided for Colombo PLC. Income tax paid for the year ending Total income tax liability for the year ending Carrying amount – Plant and machinery Tax base-Plant and machinery Carrying amount – Motor vehicles Tax base-Motor vehicles 31. 03. 2015 ( Rs. 000) 500 825 3, 000 2, 500 31. 03. 2016 ( Rs. 000) 650 850 2, 000 • Income tax rate is 30%. Required: 1. Prepare the income tax expense account, deferred tax assets and liability accounts 2. Extracts of the financial statements for 2015/16 and 2016/17.

Exercise 5 • Kandy PLC was incorporated on 01. 04. 2013 and on the sale date plant and machinery and office equipment were purchased costing Rs. 12 million and Rs. 6 million respectively. Plant and machineries are depreciated at 20% p. a. for accounting purpose and 50% per income tax purpose. Motor vehicles are depreciated at 33. 33% p. a. for accounting purpose and 20% per income tax purpose. Income tax rate is 30%. Total income tax liability for each year was Rs. 2 million and which was paid during the particular year. Required: 1. Prepare the income tax expense account, deferred tax assets and liability accounts 2. Extracts of the financial statements

The tax base • The tax base of an asset is the amount that will be deductible for tax purposes against any taxable economic benefits that will flow to an entity when it recovers the carrying amount of the asset. If those economic benefits will not be taxable, the tax base of the asset is equal to its carrying amount.

Deferred Tax Liability The amounts of income taxes payable in future periods in respect of taxable temporary differences. Deferred Tax Assets The amounts of income taxes recoverable in future periods in respect of : - deductible temporary differences; and - the carry forward of unused tax losses; and -unused tax credits. 19

Unused tax losses and unused tax credits • Deferred tax asset shall be recognized for the carry forward of unused tax losses and unused tax credits to the extent that it is probable that future taxable profit will be available against which the unused tax losses and unused tax credits can be utilised.

- Slides: 20