Liquidity Crises Currency Crises and Currency Wars Assaf

, one good, and a continuum [0,")

. � For")

has highlighted")

discusses various mechanisms that")

and Goldstein")

for commodity-exporters, a country-specific")

floaters; More strongly")

foreign and domestic assets")

or sell (a")

")

")

as")

Summer 2012 --Another round of euro periphery pressure. FX intervention to")

35% 30% 25% 20%")

60% 40% 20% 0% 2000")

. As")

1. 40")

- Slides: 131

Liquidity Crises, Currency Crises, and Currency “Wars” Assaf Razin 2018

Road Map Scope Banking Crises � Currency and Twin Crises Currency “Wars” The Euro Crisis Conclusion � � � 2

The 2008 turmoil � World financial markets exhibit ingredients from all types of financial crises in history: ◦ Banking crises ◦ Currency crises ◦ Credit frictions ◦ Market freezes ◦ Asset bubbles booming and Busting ◦ Sovereign Debt Fragility, especially within Single Currency Areas 3

Types of Fragility ◦ Coordination failure Banks rely on the fact that only forecastable fraction of depositors will have short term liquidity needs. But there is self fulfilling equilibrium where all depositors demand early withdrawal (Diamond and Dybvig). ◦ Strategic Complementarity More depositors withdraw their money the bank is more likely to fail and so other depositors have a stronger incentive to withdraw. 4

◦ Moral hazard in Credit Markets The borrower has the ability to divert resources to himself at the expense of the creditor. This creates a limit on credit. The limit can get tightens when economic conditions worsen (Holmstrom and Tirole Principal-Agent framework). ◦ Risk Shifting An investor who borrow to buy assets benefits from the upside while having limited exposure to the downside risk (Risk shifting Allen and Gale model). ◦ Leverage Cycles The optimists-pessimists composition in the investor population shifts endogenously as a cause for the birth and death of leverage bubbles (Geanakoplos). ◦ Fragilities of Monetary and exchange rate arrangements ◦ European Monetary System and lender of last resort (a EMU member central bank cannot print money—Paul De Grauwe). 5

Panic-Based Banking Crises

Banking Crises � Depository institutions are inherently unstable, because they finance long-term investments with short-term deposits � The maturity mismatch exposes banks to the risk of bank runs: when many depositors demand their money in the short term, banks will have to liquidate long-term investments at a loss 7

Diamond-Dybvig Economy � three periods (0, 1, 2), one good, and a continuum [0, 1] of agents � Each agent is born in period 0 with an endowment of one unit � Consumption � Each occurs in period 1 (c 1) or 2 (c 2) agent can be of two types: With probability the agent is impatient and with probability 1 - she is patient 8

Diamond-Dybvig economy � Agents’ types are i. i. d. ; we assume no aggregate uncertainty � Agents learn their types (which are their private information) at the beginning of period 1 � Impatient agents can consume only in period 1. They obtain utility of � Patient agents can consume at either period; their utility is 9

Diamond-Dybvig economy � Agents have access to a productive technology that yields a higher expected return in the long run. � Utility function u is increasing, and for any c>1 has a relative risk-aversion coefficient >1; u(0)=0 10

Banking Crises Diamond-Dybvig economy � Formulation Based on Goldstein and Pauzner (2005). � For each unit of input in period 0, the technology generates one unit of output if liquidated in period 1 � If liquidated in period 2, the technology yields R units of output with probability p( ), or 0 units with probability 1 - p ( ) � is the state of the economy, drawn from a uniform distribution on [0, 1], unknown to agents before period 2 � p( ) is strictly increasing in , To create incentive for patient depositors to delay withdrawals to period 2: 11

Autarky � In autarky, impatient agents consume one unit in period 1, whereas patient agents consume R units in period 2 with probability p( ) � Because of the high coefficient of risk aversion, a transfer of consumption from patient agents to impatient ones could be beneficial, ex ante, to all agents, although it would necessitate the early liquidation of long-term investments 12

All-Knowing Social Planner �A social planner who can verify agents’ types, once realized, would set the period-1 consumption level c 1 of the impatient agents so as to maximize an agent’s ex-ante expected welfare: The first-best period-1 consumption is set to maximize this ex-ante expected welfare 13

Banking Crises Risk Sharing via Maturity Transformation units of investment are liquidated in � period 1 to satisfy the consumption needs of impatient agents � As a result, in period 2, each of the patient agents consumes � The with probability first-best period-1 consumption is set to maximize this ex-ante expected welfare 14

Banking Crises Risk Sharing via Maturity Transformation � The condition equates the benefit and cost from the early liquidation of the marginal unit of investment � � , period 1 consumption of impatient consumers exceeds the endowment available in period 1: � There is risk sharing, which is achieved via maturity transformation: the transfer of wealth from patient agents to impatient ones so as to provide insurance in period 0. 15

Banks � Assume that the economy has a banking sector with free entry, and that all banks have access to the same investment technology. � Since banks make no profits due to perfect competition, they offer the same contract as the one that would be offered by a single bank that maximizes the welfare of agents 16

Banks and Multiple Equilibria � Suppose the bank sets the payoff to early withdrawal r 1 at the first-best level of consumption � If only impatient agents demand early withdrawal, the expected utility of patient agents is 17

Banking Crises Banks and Multiple Equilibria � As long as this is more than the utility from withdrawing early , there is an equilibrium in which, indeed, only impatient agents demand early withdrawal. � In this equilibrium, the first-best allocation is sustained. � However, as Diamond and Dybvig point out, the demand-deposit contract makes the bank vulnerable to runs. 18

Banking Crises Banks and Multiple Equilibria � The second equilibrium: all agents demand early withdrawal. � When they do so, period-1 payment is r 1 with probability 1/r 1 and period-2 depositor payoff is 0, so that it is indeed optimal for agents to demand early withdrawal. � This coordination-failure equilibrium is welfare inferior to the autarkic regime. 19

Banking Crises withdrawal timing and depositor payoffs Ex Post Payments to Agents 20

Multiple Equilibrium and Welfare Ranking 21

Common Knowledge vs. Private Knowledge � Begin with common knowledge about the fundamental stochastic θ � The possible equilibrium outcomes depend on which one of three regions the fundamental θ: 22

Common Knowledge � Below a threshold, there is a unique equilibrium where all depositors – patient and impatient – run on the bank and demand early withdrawal. � Above a threshold, there is a unique equilibrium where patient depositors do not withdraw. � Between the two thresholds, there are multiple equilibria. 23

Uncommon Knowledge: Unique Equilibrium � Introducing noise in speculators’ information about θ dramatically changes the predictions of the model, even if the noise is very small � The intermediate region between θ and θ is split into two sub-regions: below θ*, a run occurs bank fails, while above it, there is no run and 24

Heterogeneous Signals and Unique Equilibrium � Due to the noise in patient depositors’ information about , their decisions about whether to withdraw no longer depend only on the information conveyed by the signal about the fundamental, but also depend on what the signal conveys about other depositors’ signals � Hence, between θ and θ, depositors can no longer perfectly coordinate on any of the outcomes, as their actions now depend on what they think other depositors will do at other signals 25

Banking Crises Heterogeneous Signals and Unique Equilibrium � A depositor observing a signal slightly below knows that many other depositors may have observed signals above and chose not to run. � Taking this into account, she chooses not to run. � Then, knowing that depositors with signals just below are not running on the bank, and applying the same logic, depositors with even lower signals will also choose not to run. � This logic can be repeated again and again, establishing a boundary well below , above which depositors do not run on the bank. 26

Banking Crises Heterogeneous Signals and Unique Equilibrium � The same logic can then be repeated from the other direction, establishing a boundary well above θ, below which depositors do run on the bank � The mathematical proof shows that the two boundaries coincide at a unique θ*, such that all depositors run below θ* and do not run above θ* 27

Banking Crises Heterogeneous Signals and Unique Equilibrium � In the range between θ and , the level of the fundamental now perfectly predicts whether or not a crisis occurs. In particular, a crisis surely occurs below. � We refer to crises in this range as “panic-based” because a crisis in this range is not necessitated by the fundamentals; it occurs because agents think it will occur, and in that sense it is self-fulfilling. � However, the occurrence of a self-fulfilling crisis here is uniquely pinned down by the fundamentals. 28

Probability of Runs � Knowing when runs occur, one can compute their probability and relate it to the terms of the banking contract. Goldstein and Pauzner (2005) show that banks become more vulnerable to runs when they offer more risk sharing. � That is, the threshold θ* , below which a run happens, is an increasing function of the shortterm payment offered to depositors r 1 29

Deposit Contracts � However, even when this destabilizing effect is taken into account, banks still increase welfare by offering demand deposit contracts � Characterizing the short-term payment in the banking contract chosen by banks taking into account the probability of a run, they show that this payment does not exploit all possible gains from risk sharing, since doing so would result in too many bank runs. � Still, in equilibrium, panic-based runs occur, resulting from coordination failures among bank depositors. This leaves room for government policy to improve overall welfare. 30

Deposit Insurance � One of the basic policy remedies to reduce the loss from panicbased runs is introduction of deposit insurance by the government. � This idea goes back to Diamond and Dybvig (1983), where the government promises to collect taxes and provide liquidity (bailout) to the bank in case the bank faces financial distress � In the context of the model described above, with deposit insurance, patient agents know that if they wait they will receive the promised return independently of the number of agents who run � Hence, panic based runs are prevented: patient agents withdraw their deposits only when this is their dominant action 31

Deposit Insurance � Extending the context of the above model, Keister (2011) has highlighted another benefit of deposit insurance: it helps providing a better allocation of resources by equating the marginal utility that agents derive from private consumption and public-good consumption. � That is, when bank runs occur, private consumption decreases, generating a gap between the marginal utility of private consumption and that of public-good consumption, so with bailouts, the government can reduce the public good and increase private consumption to correct the distortion. 32

Moral Hazard � However, deposit insurance also has a drawback, as it creates moral hazard: when the bank designs the optimal contract, it does not internalize the cost of the taxes that might be required to pay the insurance. � Thus, the bank has an incentive to over-exploit the deposit insurance by setting r 1 higher than the socially optimal level. 33

Bank finance and Modigliani-Miller paradigm Modigliani and Miller tell us that profitable new investment could be financed by selling new shares of stock in the bank as well as borrowing more money from depositors. But the primary reason that the cost of financing investment depend on the mix of debt and equity is that another party bears the difference in costs. In particular, when the government insures a bank’s creditors then increasing the fraction of debt financing can increase the value of this insurance from the government. � � 34

Bank owners prefer debt finance over equity finance Under Bailout Policies Increasing the bank’s debt may make the � bank’s owners better off at no cost to the creditors. But the bank’s gains would be at the expense of the tax-paying public, which is bearing risks that private investors would not accept without being paid a greater interest premium. Public insurance enables banks to borrow at low rates that do not properly respond to greater risks that their creditors must bear when the bank has less equity. 35

FX Market Intervention by the Central Bank: Basics

Figure 5 B: Sterilized Foreign Exchange Market Intervention Sterilized purchase of foreign assets

Currency and Twin Crises

Currency Crises � Governments/central banks try to maintain certain financial and monetary arrangements, most notably a fixed-exchange rate regime, or more recently, a regional monetary union. Their goal is to stabilize the economy or the region. � At times, these arrangements become unstable and collapse leading to debt and banking crises (surveyed in the previous sections). � This strand of the literature analyzes currency crises characterized by a speculative attack on a fixed exchange rate regime. 39

Currency Crises � The best way to understand the origins of currency crises is to think about the basic tri-lemma in international finance. � A tri-lemma is a situation in which someone faces a choice among three options, each of which comes with some inevitable problems, so that not all the three underlying policy objectives can be simultaneously accomplished. 40

Currency Crises In international finance, the tri-lemma stems from the fact that, in most nations, economic policy makers would like to achieve the following goals. First, make the country’s economy open to international capital flows, because by doing so they let investors diversify their portfolios overseas and achieve risk sharing. They also benefit from the expertise brought to the country by foreign investors. � Second, use monetary policy as a tool to help stabilize inflation, output, and the financial sector in the economy. This is achieved as the central bank can increase the money supply and reduce interest rates when the economy is depressed, and reduce money growth and raise interest rates when it is overheated. Moreover, it can serve as a lender of last resort in case of financial panic. 41

Currency Crises � Third, maintain stability in the exchange rate. This is because a volatile exchange rate, at times driven by speculation, can be a source of broader financial volatility, and makes it harder for households and businesses to trade in the world economy and for investors to plan for the future. � The problem, however, is that a country can only achieve adequately two of these three goals. 42

Currency Crises � By attempting to maintain a fixed exchange rate and capital mobility, the central bank loses its ability to control the interest rate or equivalently the monetary base – its policy instruments – as the interest rate becomes anchored to the world interest rate by the interest rate parity and the monetary base is automatically adjusted. � This is the case of individual members of the EMU. � In order to keep control over the interest rate or equivalently the money supply, the central bank has to let the exchange rate float freely, as in the case of the US. 43

Currency Crises � If the central bank wishes to maintain both exchange rate stability and control over the monetary policy, the only way to do it is by imposing domestic credit controls and international capital controls, as in the case of China. � Currency crises occur when the country is trying to maintain a fixed exchange rate regime with capital mobility, but faces conflicting policy needs, such as fiscal imbalances or fragile financial sector, that need to be resolved by independent monetary policy, and effectively shift the regime from the first solution of the trilemma described above to the second one. 44

Two Open Economy Trilemmas The Macroeconomic classic—fixed exchange rate, capital flows, independent monetary policy; The Financial Sector– fixed exchange rate, � capital flows, financial stability; (e. g. , Cyprus, Greece—members of Euro) � 45

The EMS 1979– 1998 Because of differences in monetary and fiscal � policies across the EMS, market participants began buying German assets (because of high German interest rates) and selling other EMS assets. As a result, Britain left the EMS in 1992 and allowed the pound to float against other European currencies. As a result, the exchange rate mechanism was � redefined in 1993 to allow for bands of +/– 15% of the target value in order devalue many currencies relative to the deutschemark. 20 -46 �

Currency Crises First-Generation Model of Currency Crises � This branch of models, the so-called ‘first generation models of currency attacks’ was motivated by a series of events where fixed exchange rate regimes collapsed following speculative attacks, for example, the early 1970 s breakdown of the Bretton Wood global system. � The first paper here is the one by Krugman (1979). � He describes a government that tries to maintain a fixed exchange rate regime, but is subject to a constant loss of reserves, due to the need to monetize government budget deficits. 47

U. S. External Balance Problems Under Bretton Woods The collapse of the Bretton Woods system was � caused primarily by imbalances of the U. S. during the 1960 s and 1970 s. The U. S. current account surplus became a deficit in 1971. ◦ Rapidly increasing government purchases increased ◦ aggregate demand output, as well as prices. Rising prices and a growing money supply caused the U. S. ◦ dollar to become overvalued in terms of gold and in terms of foreign currencies.

Currency Crises First-Generation Model of Currency Crises � These two features of the policy are inconsistent with each other, and lead to an eventual attack on the reserves of the central bank, that culminate in a collapse of the fixed exchange rate regime. � Flood and Garber (1984) extended and clarified the basic mechanism, suggested by Krugman (1979), generating the formulation that was widely used since then. 49

Currency Crises First-Generation Model of Currency Crises � The problem is that this process cannot continue forever, since the reserves of foreign currency have a lower bound. � Eventually, the central bank will have to abandon the solution of the trilemma through a fixed exchange rate regime and perfect capital mobility to a solution through flexible exchange rate with flexible monetary policy (i. e. , flexible monetary base or equivalently domestic interest rate) and perfect capital mobility. 50

Currency Crises First-Generation Model of Currency Crises � Let us provide a simple description of this model: � Recall that the asset-side of the central bank’s balance sheet at time t is composed of domestic assets BH, t � the domestic-currency value of foreign assets St. BF, t � where St denotes the exchange rate, i. e. , the value of foreign currency in terms of domestic currency. � The total assets have to equal the total liabilities of the central bank, which are, by definition, the monetary base, denoted as Mt. 51

Currency Crises . First-Generation Model of Currency Crises � In the model, due to fiscal imbalances, the domestic assets grow in a fixed and exogenous rate: � Because of perfect capital mobility, the domestic interest rate is determined through the interest rate parity, as follows: � Where it denotes the domestic interest rate at time t and it* denotes the foreign interest rate at time t. 52

Currency Crises First-Generation Model of Currency Crises � Finally, the supply of money, i. e. , the monetary base, has to be equal to the demand for money, which is denoted as L(it), a decreasing function of the domestic interest rate. � The inconsistency between a fixed exchange rate regime: with capital mobility and the fiscal imbalances comes due to the fact that the domestic assets of the central bank keep growing, but the total assets cannot change since the monetary base is pinned down by the demand for money, L(it*), which is determined by the foreign interest rate 53

Currency Crises First-Generation Model of Currency Crises � Hence, the obligation of the central bank to keep financing the fiscal needs, puts downward pressure on the domestic interest rate, which, in turn, puts upward pressure on the exchange rate. � In order to prevent depreciation, the central bank has to intervene by reducing the inventory of foreign reserves. � Overall, decreases by the same amount as BH, t increases, so the monetary base remains the same. 54

Currency Regime Switch And Dwindling International Reserves 55

Currency Crises First-Generation Model of Currency Crises � The question is what is the critical level of domestic assets and the corresponding period of time T, at which the fixedexchange rate regime collapses. � As pointed out by, Flood and Garber (1984), this happens when the shadow exchange rate – defined as the flexible exchange rate under the assumption that the central bank’s foreign reserves reached their lower bound while the central bank keeps increasing the domestic assets to accommodate the fiscal needs – is equal to the pegged exchange rate. 56

Currency Crises Second-Generation Model of Currency Crises � Following the collapse of the ERM in the early 1990 s, which was characterized by the tradeoff between the declining activity level and abandoning the exchange rate management system, the so-called first-generation model of currency attacks did not seem suitable any more to explain the ongoing crisis phenomena. � This led to the development of the so-called ‘second generation model of currency attacks, ’ pioneered by Obstfeld (1994, 1996). 57

Currency Crises Second-Generation Model of Currency Crises � A basic idea here is that the government’s policy is not just on ‘automatic pilot’ like in Krugman (1979) above, but rather that the government is setting the policy endogenously, trying to maximize a well-specified objective function, without being able to fully commit to a given policy. � In this group of models, there are usually self-fulfilling multiple equilibria, where the expectation of a collapse of the fixed exchange rate regime leads the government to abandon the regime. � This is related to the Diamond and Dybvig (1983) model of bank runs, creating a link between these two strands of the literature. 58

Currency Crises Second-Generation Model of Currency Crises � Obstfeld (1996) discusses various mechanisms that can create the multiplicity of equilibria in a currency-crisis model. Let us describe one of them, which is inspired by Barro and Gordon (1983). � Suppose that the government minimizes a loss function of the following type: � Here, y is the level of output, y* is the target level of output, and ε is the rate of depreciation, which in the model is equal to the inflation rate. 59

Currency Crises Second-Generation Model of Currency Crises � Hence, the interpretation is that the government is in a regime of zero depreciation (a fixed exchange rate regime). Deviating from this regime has two costs. � The first one is captured by the index function in the third term above, which says that there is a fixed cost in case the government depreciates the currency. � The second one is captured by the second term above, saying that there are costs to the economy in case of inflation. 60

Currency Crises Second-Generation Model of Currency Crises � But, there is also a benefit: the government wishes to reduce deviations from the target level of output, and increasing the depreciation rate above the expected level serves to boost output, via the Philips Curve. � This can be seen in the following expression, specifying how output is determined: � Here, is the natural output, u is a random shock, and is the expected level of depreciation/inflation that is set endogenously in the model by wage setters based on rational expectations 61

Currency Crises Second-Generation Model of Currency Crises � The idea is that an unexpected inflationary shock boosts output by reducing real wages and increasing production. � Importantly, the government cannot commit to a fixed exchange rate. Otherwise, it would achieve minimum loss by committing to ε=0. � However, due to lack of commitment, a sizable shock u will lead the government to depreciate and achieve the increase in output bearing the loss of credibility. 62

Currency Crises Second-Generation Model of Currency Crises � Going back to the tri-lemma discussed above, a fixed exchange rate regime prevents the government from using monetary policy to boost output, and a large enough shock will cause the government to deviate from the fixed exchange rate regime. � It can be shown that the above model generates multiplicity of equilibria. If wage setters coordinate on a high level of expected depreciation/inflation, then the government will validate this expectation with its policy by depreciating more often. 63

Currency Crises Second-Generation Model of Currency Crises � If they coordinate on a low level of expected depreciation, then the government will have a weaker incentive to deviate from the fixed exchange rate regime. � Hence, a depreciation becomes a self-fulfilling expectation. � Similarly, one can describe mechanisms where speculators may force the government to abandon an existing fixedexchange rate regime by attacking its reserves and making the maintenance of the regime too costly. � If many speculators attack, the government will lose many reserves, and will be more likely to abandon the regime. 64

Currency Crises Second-Generation Model of Currency Crises � A self-fulfilling speculative attack is profitable only if many speculators join it. � Consequently, there is one equilibrium with a speculative attack and a collapse of the regime, and there is another equilibrium, where these things do not happen. � Similarly, speculators can attack government bonds demanding higher rates due to expected sovereign-debt default, creating an incentive for the central bank to abandon a currency regime and reduce the value of the debt. 65

Currency Crises Second-Generation Model of Currency Crises � As argued by Paul De Grauwe (2011), the problem can become more severe for countries that participate in a currency union since their governments do not have the monetary tools to reduce the cost of the debt. � As we discussed in the previous section, having a model of multiple equilibria creates an obstacle for policy analysis. � Morris and Shin (1998) were the first to tackle the problem of multiplicity in the second-generation models of speculative attacks. 66

Currency Crises Second-Generation Model of Currency Crises � They first express this model in an explicit market framework, where speculators are players having to make a decision whether to attack the currency or not. � Then, using the global-game methodology, pioneered by Carlsson and van Damme (1993), they are able to derive a unique equilibrium, where the fundamentals of the economy uniquely determine whether a crisis occurs or not. This is important since it enables one to ask questions as to the effect of policy tools on the probability of a currency attack. 67

Third generation Currency Crisis models While the 1 st and 2 nd generation currency � crisis literature focused on the government budget fragility alone, the ‘third-generation’ models of currency crises essentially connect to models of banking crises , private sector credit frictions, sovereign debt crises, etc. 68

Currency Crises Third-Generation Model of Currency Crises � In the 1997, a wave of crises hit the emerging economies in Asia, including Thailand, South Korea, Indonesia, Philippines, and Malaysia. A clear feature of these crises was the combination of the collapse of fixed exchange rate regimes, capital flows, financial institutions, and credit This led to extensive research on the interplay between currency and banking crises, sometimes referred to as the twin crises, and balance sheet effects of depreciations For a broad description of the events around the crisis, see Radelet and Sachs (1998). The importance of capital flows reversals was anticipated by Calvo (1995). 69

Currency Crises Balance Sheet Model of Currency Crises � One of the first models to capture this joint problem was presented in Krugman (1999). � In his model, firms suffer from a currency mismatch between their assets and liabilities: their assets are denominated in domestic goods and their liabilities are denominated in foreign goods. � Then, a real exchange rate depreciation increases the value of liabilities relative to assets, leading to deterioration in firms’ balance sheets. 70

Currency Crises Third-Generation Model of Currency Crises � Because of credit frictions as in Holmstrom and Tirole (1997), this deterioration in firms’ balance sheets implies that they can borrow less and invest less. � The novelty in Krugman’s paper is that the decrease in investment validates the real depreciation in the generalequilibrium setup. � This is because the decreased investment by foreigners in the domestic market implies that there will be a decrease in demand for local goods relative to foreign goods, leading to real depreciation. 71

Currency Crises Credit friction Models of Currency Crises � Hence, the system has multiple equilibria with high economic activity, appreciated exchange rate, and strong balance sheets in one equilibrium, and low economic activity, depreciated exchange rate, and weak balance sheets in the other equilibrium. � Other models that extended and continued this line of research include: Aghion, Bacchetta, and Banerjee (2001), Caballero and Krishnamurthy (2001), and Schneider and Tornell (2004). The latter fully endogeneize the currency mismatch between firms’ assets and liabilities. 72

Currency Crises Twin-Crisis Model of Currency Crises � Chang and Velasco (2001) and Goldstein (2004) model the vicious circle between bank runs and speculative attacks on the currency. � On the one hand, the expected collapse of the currency worsens banks’ prospects, as they have foreign liabilities and domestic assets, and thus generates bank runs, as described in the previous section. Bank runs are more likely in a currency union without a single-currency-wide bank union, or the ability of the central bank to act as a lender of last resort for sovereign debt. 73

Scope Jeff’s paper proposes to define an intermediate arrangement, “systematic managed floating, ” as one where the central bank regularly responds to changes in total exchange market pressure by allowing some fraction to be reflected as a change in the exchange rate and the remaining fraction to Be absorbed as a change in foreign exchange reserves.

Plan of Discussion 1. Scope of the paper 2. Basics of FX market intervention mechanism 3. Examples of “currency war” episodes 4. A general-point critic

Challenges FX Market intervention is one of several tools and targets of monetary policy. FX systematic interventionists is a policy that lies between hard peg and pure unconditional float. There is however no simple way to characterize the many-tool, multiple target package of a monetary regime by a reduced form concept.

Results Two measures of exogenous external shocks are used: (i) for commodity-exporters, a country-specific index of global prices of the export commodities (ii) for other Asian emerging market economies, the VIX. In regressions to test effects on real exchange rates, Jeff finds that positive

External shocks tend to cause: Real appreciation for most systematic managed-(1) floaters; More strongly so for pure floaters; (2) And, not at all for most firm peggers(3)

“implied volatility” A number of factors determines its size. One is the relationship between the market price and the exercise price; if the market price is $10, then the right to buy the asset at $5 must cost at least $5. Another is the length of the options contract; the longer the time period, the greater the chance that prices will Move enough to make the option worth exercising and the higher the premium. Volatility is also very important. If an asset is doubling and halving in price every other day, an option is much more likely to be exercised than if its price barely moves from one trading session to the next. No one knows what future volatility will be. But if investors are keen to insure against rapid market movements, then premiums will rise. This “implied volatility” is the number captured by the Vix.

. [AC 1 Forward Guidance and Signaling In the absence of the portfolio balance effect, sterilized intervention cannot move the exchange rate. The effectiveness of the current foreign exchange market intervention depends also on the commitment of the central bank to do so in the future. Therefore, if is expected to be depreciated in the future, through credible “forward guidance” aided by future interventions will be more depreciated as well

Sterilized FX Intervention Sterilized FX intervention is effective if (1) foreign and domestic assets are imperfect substitutes; (2) the fx market intervention signals that the entral bank will pursue future interventions. If the signal is effective in the eyes of market participants the future expected exchange rate changes and this induces the current exchange rate to change as well.

The signalling mechanism is akin to “forward guidance” whereby the central bank announces in a credible fashion the future path of the policy rate.

Reduced VIX and Capital Flows to Emerging Markets The VIX is the Chicago Board Options Exchange Market Volatility Index. It is a measure of the implied volatility of S&P 500 index options.

purchaser the right, but not the obligation, to buy (a call) or sell (a put) an asset at a given price before a given date. In return, like anyone buying insurance, the purchaser pays a premium. .

Examples of FX Market Intervention “Currency War” Episodes

Non-liquidity trap open economies: The 2009 “Currency War” Nominal Exchange Rate of Various Countries that Engaged in the "Currency War" : Israel, Switzerland, Sweden, Brazil and Indonesia (2007=100) Indonesia 130 Sweden Brazil Israel Switzerland 120 110 100 90 80 70 2005 2006 2007 2008 2009 2010 2011 Note that if the risk premium does not change the sterilized foreign. Source: FRED exchange-market intervention cannot affect the exchange rate.

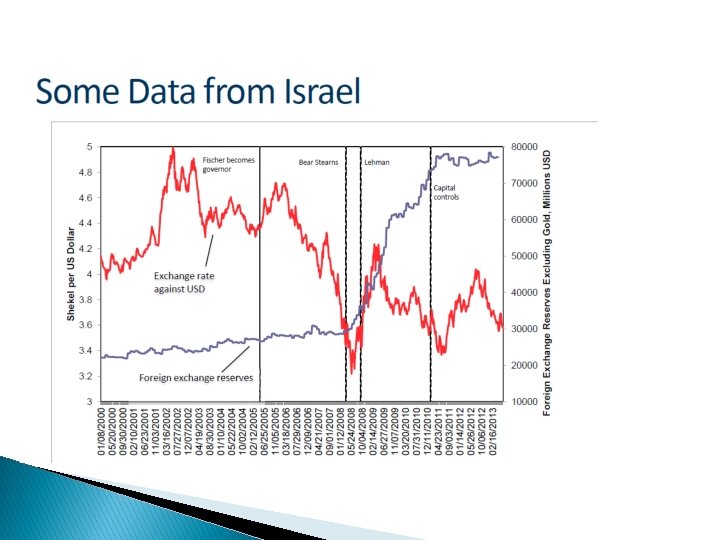

Israel’s Special FX Intervention after the 2008 global trade shock Israel’s fx intervention in the wake of the 2008 global crisis, aimed to boost up aggregate demand, with the help of an enlarged tool kit for central bank policy.

Financial Markets during Israel’s 2009 Foreign- Exchange Market Intervention A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer (usually the creditor of the reference loan) in the event of a loan default (by the debtor) or other credit event.

Israel Foreign Exchange Reserves, 2003– 12

International Comparison of reserve accumulation

Switzerland’s Story: The Reaction to the Euro-crisis Spring 2010—Greece debt default Temporary (2 months) intervention contained the franc appreciation only temporarily, with subsequent appreciation. Obstfeld multiple equilibrium means that the CB validates the expectations on either one of the two equilibria by its interest/money policy.

Swiss SNB August 2011—Italy’s spread hike SNB set 1. 20 (Frank per euro) as a floor in early September. It worked. Interpretation is that the announcement of the floor “killed” Obstfeld’s second appreciation equilibrium. Very little actual fx intervention.

Switzerland’s Story (continued) Summer 2012 --Another round of euro periphery pressure. FX intervention to prevent franc appreciation. Pressure ended with Draghy’s “whatever it takes” speech. Dec 2014 -2015 -ECB prepared the QE, sizable FX intervention to prevent franc appreciation SNB abandons the 1. 20 floor in January

Switzerland’s Current account Intl Reserve accumulation amount to most of the current account surplus — 10 percent of Switzerland GDP.

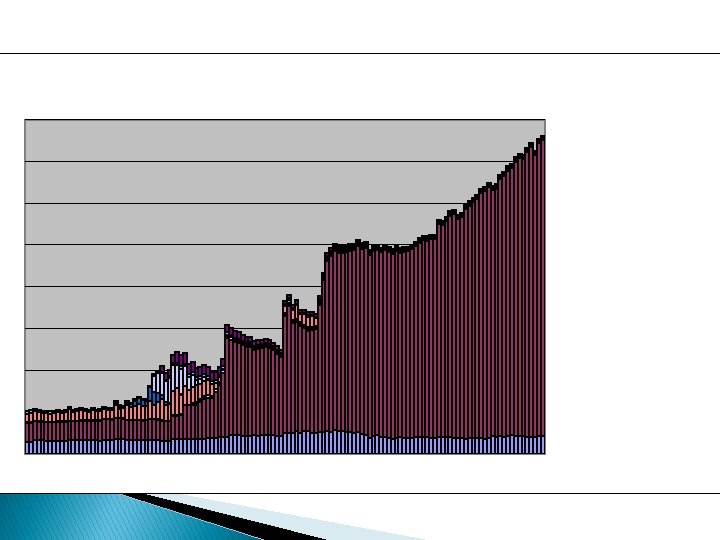

For the Swiss Internationalreserves accumulation the focus is on the charts with net flows splitting the private flows between banks and other, to get the chart below

For reserves accumulation the focus is on the charts with net flows splitting the private flows between banks and other, to get the chart below

Swiss Net Outflows and International Reserves Net outflows (% GDP) 35% 30% 25% 20% 15% 10% 5% 0% -5%2000 2002 2004 2006 2008 2010 2012 2014 2016 -10% -15% -20% Private Reserves Source: Cedric Tille

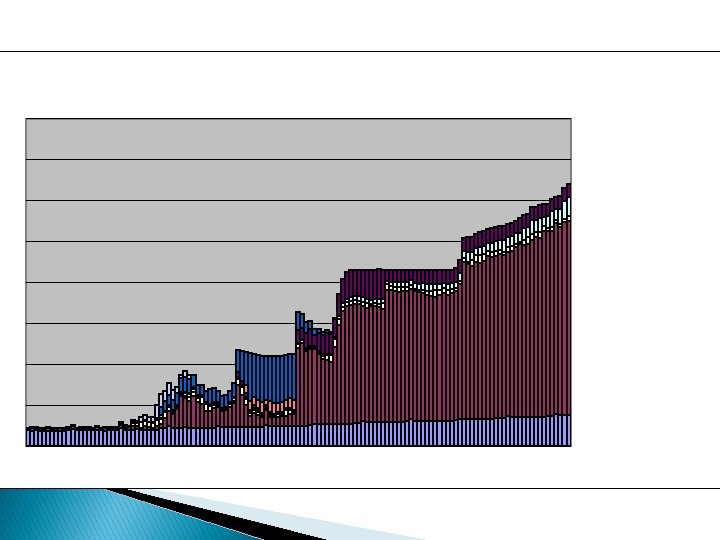

Gross Outflows Source: Cedric Tille Gross outflows (% GDP) 60% 40% 20% 0% 2000 -20% 2002 2004 2006 2008 2010 2012 -40% -60% -80% Private: non banks Private: banks Reserves 2014 2016

bonds among assets. That is, the accumulation of reserves through FX intervention is not sterilized and is this mirrored by higher bank reserves on the liability side, instead of lower domestic bonds on the asset side. See the next two charts.

General-Point Critic Central bank has two tools: 1. buying/selling assets (domestic and foreign). As long as foreign and domestic assets are substitutes, the effect of monetary by intervention in the fx market or in the domestic market will affect the exchange rate value and domestic bonds price similarly. In this sense intervention in the FX market and the domestic bond market are not distinguishable. 2. CB regulation of capital flows and prudential policy. To characterize the foreign exchange policy by changes in reseves (tool) and the value of the exchange rate (only one of the targets) and keep in the “dark” all other measures of the monetary policy and targets would not characterize uniquely the monetary regime.

Jeff’s reduced form classification of “systematic interventionistic CB” is not easily distinguishable from “episodic interventionistic CB” because it lumps together in the cross country panel countries that although are different in the path of reserves and currency value changes they might have changes in domestic bond so that the exchane rate value and chanes in bond prices are very different one from another. That is Jeff’s reduced-form test is not a test of differences in monetary regimes.

Thank You!

10 6

The Asymmetry of CB fx mkt intervention rules Under appreciating pressures there is no limit to CB buying foreign assets (because a monopoly of creating domestic currency). Under depreciating pressures limit to CB selling foreign assets are set by the previously acquired international reserves. Looking at volatility and levels of the foreign currency value in the reaction function of CB, not recognizing that CB reacts differently to a rise and the fall in the fx currency value biases the estimated policy reaction function!

Measuring Free Capital Mobility The real interest parity says that differences in real interest rates (in terms of goods and services that are earned or forgone when lending or borrowing) between countries are equal to the expected change in the value/price/cost of goods and services between countries. How much the Ems deviated from the parity? This is a measure of barriers to capital (Im)mobility

Proposed Measure of International Financial Integration �

Gross Real Interest Rate Adjusted for Real Exchange Rate Changes (US benchmark) 1. 40 1. 30 1. 20 Israel UK 1. 10 20 16 20 14 20 12 20 10 20 08 20 06 20 04 USA (real exchange rate) 20 02 19 98 19 96 19 94 19 90 19 88 0. 90 19 92 Germany Canada 20 00 1. 00

US Monetary Tightness and Emerging Markets Responses to the “taper tantrum” of May-August 2013, when Federal Reserve announced the intention to begin phasing down US quantitative easing by the end of the year, which produced an immediate rise in US interest rates and a reversal of EM capital flows. Singapore mostly intervened while India mostly took adverse shock as a change in the exchange rate, that is, a depreciation, as did the Philippines.

Jeff Frankel’s Test Compute for each country the correlation of the change in the foreign exchange value of the currency (in percent) with the change in reserves (as a percentage of the monetary base). If the correlation is positive and high enough to clear some threshold it is a systematic managed floater. At one extreme, a truly fixed exchange rate will show a correlation of zero, because the exchange rate by definition never changes. At the other extreme, a purely floating exchange rate will again show a coefficient of zero, because reserves by definition never change. But it is not just the residents of fixed and floating corners that will fail to meet this criterion.

Exchange rate regime tested over time Frankel’s systematic-intervention test involves only contemporaneous changes in the foreign exchange value of the currency with the change in reserves. They ignore future market expectations of changes in the foreign exchange value of the currency and future expectations of monetary and exchange rate policy.

Eurozone Crisis

Divergent Real Interest Rates in the Euro Zone Source: Datastream. 20 -115

Taylor Rule in the Euro Area: Core vs. Periphery 11 6

Table 20 -3: Current Account Balances of Euro Zone Countries, 2005– 2009 (percent of GDP) 20 -117

Crisis in the Periphery The Euro zone periphery crisis is essentially a Sudden Stop crisis, where capital flows reverse direction, abruptly. The consequent output depression creates � current account reversals, a la Milesi-Ferreti and Razin (2000). � 11 8

EMU: A Lender of Last Resort ? ECB is less credible than a single currency national central bank. � � Despite the European Central Bank’s promise to � intervene as lender of last resort via its program of outright monetary transactions (OMT), and its 2012 policy “To do what it takes”. � Because in the context of supranational EMU institution there is no similar institution which provides Eurozone fiscal backing. � � Also there is no European Banking Union to enable ECB to bail out banks. � 11 9

Sovereign Debt: Spain vs. UK � There are benefits of retaining a currency on one’s own are visible in the post-crisis interest rates paid on long-term public debt. The ratio of net public debt to gross domestic � product of the UK and Spain are essentially identical. IMF forecasts that in 2017, the ratio is 93 per cent for the UK and 95 per cent for Spain. Yet the yield on UK 10 -year bonds is firmly under 2 � per cent – among the lowest in UK history, and not much above Germany’s. The yield on Spanish 10 -year bonds is much higher than Germany’s. 12 0

Banks and Governments Banks and governments face same problem: � unbalanced maturity structure of assets and liabilities �Making both banks and governments vulnerable for movements of distrust and panics. �Distrust leads to liquidity crisis, which can � degenerate into a solvency crisis. : � �When banks collapse sovereign is in trouble, � �When government collapses banks are in � trouble. � 12 1

Sovereign Debt And Banking Crisis Banks assets include government bonds; a � sudden fall in government bonds prices leads to bank failures and liquidity shortage. Eurozone banks suffer from lack of effective � sovereign lender of last resort because of the absence of bank union in the eurozone. 12 2

Waves for the World Economy

Central Banks Balance Sheets 12 4

Emerging Markets Sudden Retreats: Lessons for GIIPS? 12 5

External Effects on Emerging Markets � Starting with the Fed tapering its quantity easing purchase of long term securities. China’s currency policies over the years and � the Bank of Japan’s recent monetary easing add to the pressure on currencies and central bankers in emerging countries. 12 6

Trends in the world economy 1. As a result of the 2008 crisis, there is a � dramatic slowdown in cross border capital flows. 2. As a result of the Post 2008 crisis collapse in bank lending, international capital flows into foreign direct investment now account for a much larger share. 3. Since the 2013 Summer a wave of sudden � retreats of capital flows into emerging markets. Two forces: the rebalancing of China’s economy � away from investment, and US federal reserve’s tapering of its quantitative easing program. 12 7

India � In the recent past India agricultural policies have driven up food prices. This feds into broader inflation in an economy where food expenditure accounts for a large fraction of average household budgets. The government has proved unable to cut the budget deficit or reform the labor market, and has failed to attract private financing for badly needed infrastructure investment. India’s central bank has to fill in all the gaps, singlehandedly fighting inflation and trying to prop up growth. � � 12 8

Turkey � In Turkey, a sharp increase of interest rates by the central bank has kept the currency’s value from collapsing. This heightened the risk of capital flight. � 12 9

Emerging markets currencies 13 0

Thank you