LIQUID ASSETS Liquid assets are Everything owned by

LIQUID ASSETS

Liquid assets are: Everything owned by an adult or a family in MONEY or in an equivalent form. Considered in the calculation of the allowance, which has the effect of reducing the amount paid.

A few examples of liquid assets: • Funds deposited in a financial institution (e. g. , the money in the client’s bank account) • Investments like a TFSA, a savings account, etc. • The amount excluded from income, earnings, or benefits for the purpose of calculating the benefit • Other: please refer to s. 03. 01 of the Framework Policy

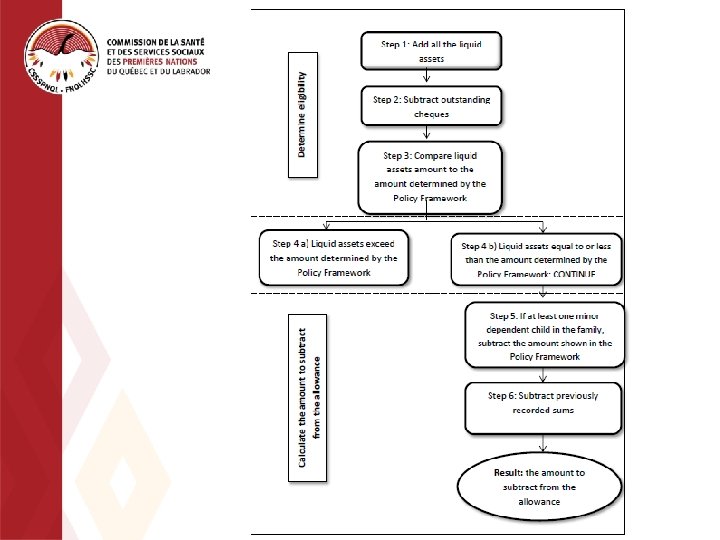

Liquid assets in a new application 05. 06. 08 There are two steps when dealing with liquid assets in a new application: #1: Determine the client’s eligibility* #2: Calculate the amount of the benefit *Clients without severely limited capacity

Determine the client’s eligibility #1: Add all the liquid assets together (all the liquid assets the family owns on the date of the application) #2: Subtract outstanding cheques or preauthorized deductions (rent, heating, electricity) #3: Compare the liquid assets with the amount set out in the Framework Policy

Liquid assets are greater If the liquid assets are greater than the amount indicated in the FP, the client or family is declared to be ineligible. The client or family may cancel the application and apply again during the same month, once their liquid assets have decreased. The officer must perform a new liquid assets test. The client or family may also file an application the following month. See section 05. 06. 08

Liquid assets are equal or below The amount to subtract from the benefit must be calculated before moving on to the next step.

Compare liquid assets Amounts to the amounts determined by the Policy Framework Family composition Dependent children Liquid assets 1 adult 0 $887 1 $1268 2 and + $1502 The amount is increased by $265 for the third dependent child and for each subsequent child 2 adults 0 $1319 1 $1573 2 and + $1807 The amount is increased by $265 for the third dependent child and for each subsequent child Spouse of a student n/a $887 The amount is increased by $289 for a first dependent child and $265 for each subsequent child Adult sheltered or required to be sheltered or minor adult with her child n/a $887

Exercise 1 Determining the client’s eligibility

Scenario: Monique Bellefleur comes to see us to apply for last resort financial assistance. She is a single parent of two children. Her bank account currently shows a balance of $650. 25. She has $450. 75 in a TFSA. She has written a $400 cheque to pay for her children’s daycare. Her electricity payment of $125. 50 will also be deducted during the month. Determine the client’s eligibility.

Exercise 1 - Answer # 1 – Add the liquid assets she owns on the date of the application: $650. 25 + $450. 75 = $1, 101 #2 – Subtract outstanding cheques or preauthorized deductions: 1, 101 – 400 – 125. 50 = $575. 50 #3 – Compare her liquid assets with the amount indicated in the Framework Policy: 1 adult and 2 dependent children: $1, 502 Answer: Because Monique has $575. 50 in liquid assets on the date of the application and her liquid assets are below the amount set out in the FP, she is eligible and the analysis of her file can continue.

Calculating the amount of the benefit # 1 – If the family has at least one dependent child, subtract the amount indicated in the FP from the liquid assets owned. Single parent family Two-parent family or spouse of student Number of minor children Liquid assets reduction 1 $431 1 $289 2 $696 2 $554 Subsequent children $265 An amount of $195 is added for each dependent child receiving the child disability supplement from the RRQ.

Calculating the amount of the benefit #2 – Subtract the amounts already considered, if any (e. g. , income, earnings or benefits already counted are deducted from the liquid assets owned) The result is the amount to subtract from the benefit.

Exercise 2 Calculating the amount of the benefit

Scenario: Let’s go back to Ms. Bellefleur from exercise #1. She owns $575. 50 in liquid assets. How much will her benefit be?

Exercise 2 - Answer #1 – If the family has at least one dependent child, subtract the amount indicated in the FP from the liquid assets owned. Monique has two dependent children, so $696 should be deducted from her liquid assets. #2 – Subtract the amounts already considered: not applicable Answer: $575. 50 (liquid assets owned) – $696 (deduction for two dependent children) = $0 Monique is entitled to the full benefit.

When the application is")

The proportion of the need in a new application (prorata) When the application is filed for a month in progress: Calculate the proportion of the need based on the number of days the client is eligible for income security (Date of the completed application, signed and received).

Calculation of the proportion 1: Identify the number of days for which the client is eligible Number of days in the month - date of the application + 1 1 day is added, since the client is entitled to social assistance for the day he/she filed the application. 2 : Calculate the amount of the eligible need Need for the month/number of days in the month x number of days of eligibility Caution! The amount for special allocations (if necessary) is added to the need without regard for proportion for the month of the application!

Example Let’s say that Ms. Bellefleur applies on May 9 (the month of May has 31 days). She has two dependent children under the age of 5. 1. Identify the number of days for which the client is eligible 31 – 9 + 1 = 23 days 2. Calculate the amount of the prorated benefit $805 /31 x 23 = $597. 26 Monique is entitled to a benefit of $597. 26 for the month of May.

Exercise 3 Calculating a prorated benefit

Scenario: Jean lives alone. He files his first application for benefits on January 3. The calculations are performed and it is determined that he is eligible. Once the basic exclusions are considered, his liquid assets total $500. He has no outstanding cheques when he files the application. During the month, he has received $105, which has already been counted. He has no dependent children, so no subtractions should be performed. How much will Jean’s benefit be?

Exercise 3 - Answer #1: Subtract the amounts already considered: $500 - $105 Amount to subtract from the benefit: $395 Pro rata: 31 days - 3 + 1 = 29 days $669/31 days x 29 days = $625. 83 - $395 = $230. 83 Jean is entitled to a benefit of $230. 83 for January.

Liquid assets are treated")

Liquid assets in an active file (during the assistance period) Liquid assets are treated differently in active files than they are in new applications. First, always look at the liquid assets owned on the last day of the month. This amount is considered to determine how much to subtract from the benefit. Next, subtract the basic exclusion from that amount. The anteriority of the deficit applies during the assistance period of the file.

Anteriority of the deficit The anteriority of the deficit is a rule that uses complex words to mean something quite simple. Every month, the amount of last resort financial assistance is based on the adult or family’s situation on the last day of the preceding month. For example, the benefit for July is calculated on the basis of the client’s situation on June 30. This includes any liquid assets the client owns.

The anteriority of the deficit

(refer to 3. 3. 3) Family composition Employable person or")

Basic exclusions (in process) (refer to 3. 3. 3) Family composition Employable person or with temporary employment limitations Person with severe employment limitations Independent adult $1, 500 $2, 500 Minor sheltered with her child $1, 500 $2, 500 Spouse of a student $1, 500 $2, 500 Family $2, 500 $5, 000 Number of minor children Single-parent family Two-parent family or spouse of student 1 $431 $289 2 $686 $554 Each subsequent $265 These basic exclusions are increased by $195 for each dependent child who receives the supplement for handicapped children paid by the Régie des rentes du Québec (RRQ).

Calculation of liquid assets surplus in an active file Example Here is an example of a calculation for a family with an active file. Mr. and Ms. Awashish have two dependent children. On the last day of June, their liquid assets totalled $3, 500. Basic exclusion for a family: $2, 500 Amount added to exclusion for 2 dependent children: $554 2, 500 + 554 = $3, 054 3, 500 – 3, 045 = $ 446 The benefit for July is therefore reduced by $446.

Exercise 4 Calculating liquid assets surplus during the assistance period

Scenario: Rita and Jean-Pierre are clients with an active file. They have three dependent children. On the last day of the month, they own $4, 200 in liquid assets. Calculate the liquid assets surplus for this family.

Exercise 4 - Answer A family of two adults and three minor children is an income security program client. On the last day of the month, the family has $4, 200 in liquid assets. What is the liquid assets surplus? The basic exclusion for a family during the assistance period is $2, 500. This two-parent family has three minor children, increasing the exclusion by $819. 2, 500 + 819= $3, 319 4, 200 – 3, 319= $881 The liquid assets surplus is $881, and the amount of the benefit the following month will be reduced by that amount.

ESSENTIAL POINTS

Exclusions Certain liquid assets are excluded in whole or in part from the calculation of the last resort assistance benefit. It is important to know what they are to make sure they are not considered and that eligible clients are not declared ineligible. The following sections of the FP lists them: Exclusions for a limited time: 03. 04 Basic exclusions increased: 03. 05 Total exclusions: 03. 06 Partial exclusions: ping. cssspnql. com/adminproc/viewer/tag/2019 V 2/article/03. 07 Amounts paid by the Ministère de la Santé publique:

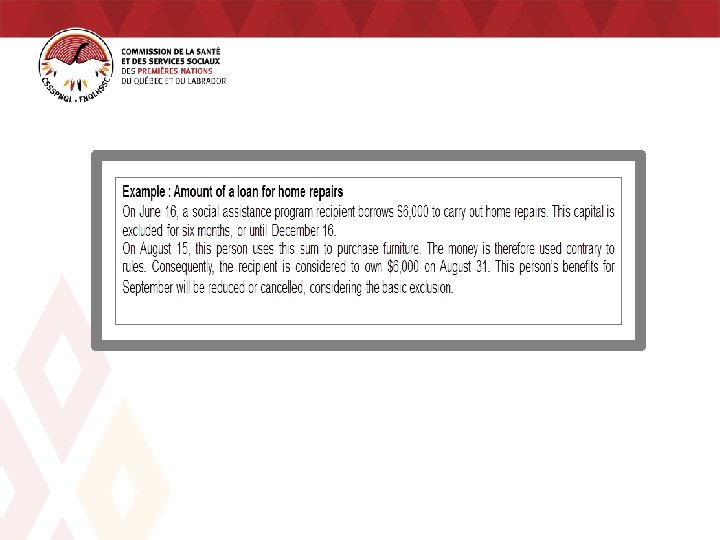

Amount used contrary to rules Liquid assets eligible for exclusion can lose their exclusion for the following reasons: • The amount was used contrary to the purposes for which it was obtained • The amount was not used within the specified time We then say that the amount was used for unsanctioned ends. The amount will be considered to be a liquid asset up to the last day of the month of the contravention.

Squandering Because the income security program provides last resort assistance, clients of the program may not squander* their assets any way they choose. It is therefore important that any large amounts of money they earn or receive is spent reasonably. ** As an officer, if you are informed that a client has squandered a liquid asset, its residual value must be established. To do so, contact the Regulatory Advisor, who will help you determine the month your client will become eligible again. *Spend without fair consideration (without receipts), gamble, give money away, etc. ** See section 03. 12 for details.

- Slides: 36