Life Income Gifts Charitable Gift Annuity 2 Lets

Life Income Gifts Charitable Gift Annuity #2

Let’s review a few key elements…

Charitable Gift Annuities • Easy to understand • Easy to administer • Fixed payments • Tax savings • Attractive to older people

The 3 Players • Donor—The one who makes the gift • Annuitant—The one who receives the annuity payments • Beneficiary—The charity that ends up with the remainder (“residuum”)

The 3 Features 1. Contract between Donor and Charity 2. Fixed Payouts made to Annuitant 3. Irrevocable Gift from Donor

Types of Annuities • Immediate Gift Annuity • Deferred Payment Gift Annuity • Testamentary Gift Annuity

State Regulation Requirements Four types of state regulation: 1. Registration—Meet statutory minimums, obtain a permit, file annual submissions 2. Notification—Meet statutory requirements, notify when issue first CGA in state 3. Conditional Exemption—Meet statutory requirements 4. Silent—Do not address CGAs or say that they are exempt from state law

Regulation Type by State Registration States Alabama, Arkansas, California, Florida, Hawaii, Maryland, New Jersey, New York, North Dakota Puerto Rico, Tennessee, Washington, Wisconsin Notification States Alaska, Connecticut, Georgia, Idaho, Iowa, Mississippi, Missouri, Montana, Nevada, New Hampshire, New Mexico, North Carolina, Oklahoma, Texas, West Virginia

Regulation Type by State Conditional Exempt States Arizona, Colorado, Illinois, Indiana, Kansas, Kentucky, Louisiana, Maine, Massachusetts, Minnesota Nebraska, Oregon, Pennsylvania, South Carolina, South Dakota, Utah, Vermont, Virginia Silent States Delaware, District of Columbia, Michigan, Ohio, Rhode Island, Wyoming

of annuitant(s) Residence address (and mailing,")

CGA Application Process • • • Full name(s) of annuitant(s) Residence address (and mailing, if different) Permission to make direct deposit payouts Dates of birth and gender Social Security numbers of each annuitant City and state of birth Desired frequency of payments Funding assets and value Restrictions or designations of residuum. Final.

Charitable Gift Annuity Risks • Risks to Donor • Inflation • Charity could dissolve • Risks to Charity • Mortality Risk • Investment Risk • Expense Risk

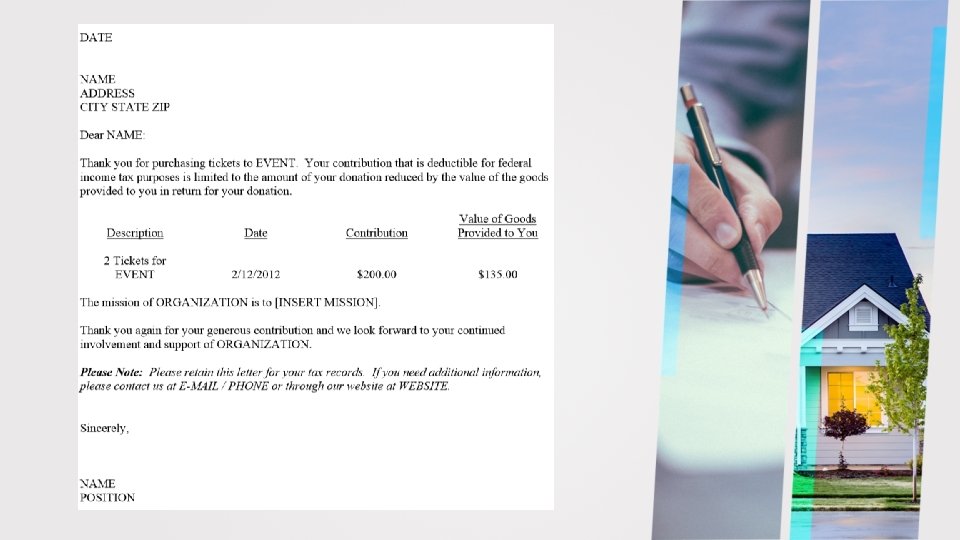

Substantiating Contributions • The donor is required to obtain a “contemporaneous written acknowledgement” when the deduction is $250 or more: • “No goods or services” (quid pro quo—”something for something”) letter as receipt • State charitable amount • Describe asset transferred • No goods or services • Attach gift calculation sheet (see sample)

Substantiating Contributions Cont… • Donor may need to file a gift tax return • Form 709 (if charitable or non-annuitant gift is > annual exclusion) • Form 8282 and 8283 if needed

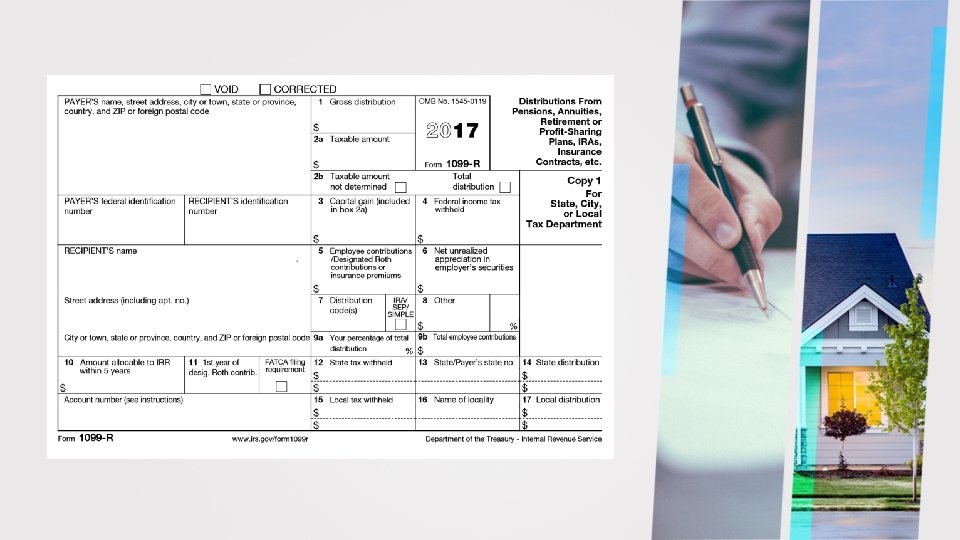

Tax Reporting Requirements • Send a 1099 -R to annuitant and IRS • Due to annuitant by January 31 st • Due to IRS by February 28 th with Form 1096

Maturity • Withdraw remainder of gift annuity from reserves • Make sure charity applies according to donor’s wishes

The 3 Possible Tax Benefits • Charitable Deduction • Partial Tax-Free Payouts • Capital Gain Avoidance and Spread

• The gift portion of CGA qualifies for")

The 3 Tax Benefits—(1. Charitable Deduction) • The gift portion of CGA qualifies for a charitable deduction • The Remainder Interest must be at least 10% of the gift • Use gift calculation software

• Cash Gift (50% of AGI) • LTCG")

The 3 Tax Benefits—(1. Charitable Deduction) • Cash Gift (50% of AGI) • LTCG Gift (30% of AGI) • Eligible for additional 5 -year carryover

• Annuity funded with cash: • Each")

The 3 Tax Benefits—(2. Partial Tax-Free Payouts) • Annuity funded with cash: • Each payout is part • Ordinary Income • Tax free return of principal • Once principal has been repaid, all future payments are treated as ordinary income. • If annuitant dies before reaching life expectancy, deduction for unrecovered basis can be taken on final decedent’s 1040, Schedule A. • The tax character of the annuity payments reported yearly on 1099 -R.

• Annuity funded with appreciated asset: • Each")

The 3 Tax Benefits—(3. Capital Gain) • Annuity funded with appreciated asset: • Each payment is part • Ordinary Income • Capital Gain (spread over life expectancy, if donor is an initial annuitant and non-assignable) • Small amount of tax free return of principal

The Applicable Federal Rate • Determined by the United States Treasury Department • Published in the Wall Street Journal • Crescendo Interactive and PG Calc • Rate can be • Month gift is made • Either of two previous months • Lowest monthly rate results in larger tax free payment and smaller charitable deduction • Highest monthly rate results in larger charitable deduction and smaller tax free payment

Testamentary Gift Annuity • Establish by Will or Trust • Reasons • Income beneficiaries may be too young or inexperienced • Elderly person • Implementation • Direct the personal representative/trustee

of annuitant(s) • Benefit to annuitant")

Early Termination of CGA • Prior to death(s) of annuitant(s) • Benefit to annuitant • Benefit to charity

Gift Annuity for Land—a case study • • • Anna Annuity… [Gift. Law Pro 4. 7. 6 A] Age 79 Owns real estate free and clear valued at $100, 000 Wants retirement income Doesn’t want to pay capital gains tax

Testamentary Current CGA—a case study • Mary Wilson was in her 80 s… [Gift. Law Pro 3. 4. 3 A] • Is very pleased with her CGA • Has high fixed payments • Substantial charitable income tax deduction • Portion of her payments are tax-free return of principle

CGA, A Lifetime Stream Of Income

Insert, play video here. See link below. • http: //www. willplan. org/article/138/other-gift-planningopportunities-usa-canada-videos/a-charitable-gift-annuity-alifetime-stream-of-income • OR • You. Tube link: • https: //www. youtube. com/watch? v=y. V 02 u 64 t. UXY

• Owns stock that has been a good investment • Concerned about leaving savings in the unstable market • Looking for secure retirement income

• Bought stock that has increased in value • The value of the stock fluctuates often • Wants to have a fixed payout

CGA Attractive Qualities • Opportunity of creating a gift to support God’s cause • Easy to understand • Simple and cost effective to administer • Receive fixed payments for life • Preserves life income • Secured by all the assets of the charity

CGA Attractive Qualities Cont • Income tax benefits • Allows for partial forgiveness and partial deference of capital gains • Provides opportunity to convert low-income-producing assets to higher income stream • Direct annuity payouts to person other than donor • Planning flexibility with deferred annuity options • Created during life or by Will or Trust at death

Charitable Gift Annuity http: //inspirationaloutreach. com

Allison and Larry’s Deferred CGA • Both were age 50 • Deferred paying Capital Gains Tax • Received an immediate charitable income tax deduction • At age 65 the CGA would start making payments • Portion of their payments are tax free

Claire’s CGA • Claire transferred $10, 000 of her appreciated stock to her favorite charity for a CGA • Has fixed 6. 4% payout or $640 annually • Now has peace of mind

Patricia’s CGA • Transferred her stock for a CGA • Deferred paying Capital Gains Tax • Received a Charitable Deduction • Will spend more on her Grandchildren!

If Susan is age 65 when CGA is created • Annuity Payment will be 4. 7% (or $4, 700 annually) for her lifetime • $100, 000 is included in Mary’s estate but she will get $32, 313 charitable estate tax deduction • Of Susan’s annual annuity payment $3, 402 will be tax free

Testamentary Current CGA—a case study • Mary decided to create a CGA for her daughter Susan through her will • Mary directed her attorney to include appropriate language in her will • $100, 000 CGA to be created at her favorite charity • Annuitant will be her daughter Susan • Payments are to be made at the one life gift annuity rate • Payments are to be made quarterly • If Susan does not survive Mary the $100, 00 will be given directly to the favorite charity

Another Option Could have been • $100, 000 CGA with a reduced annuity rate • 5. 61% Annuity payout (still $5, 610 annually)

Ana’s Annuity Details • Initial Value of $85, 000 • 6. 6% Annuity payout ($5, 610 annually) • $40, 735 charitable deduction for the CGA • $15, 000 for the difference between the appraised value of the land the CGA contract value

Charity Proposes an $85, 000 Charitable Gift Annuity due to • Uncertainty of the sale price • Ongoing holding costs • Costs to sell the property

Charity’s Concerns • Land could sell for less than $100, 000 • Charity will be responsible for taxes, insurance and maintenance • Charity will pay closing costs between 5% - 8%

NAD PGTRS Manual’s Statement on CGAs • A charity that follows the ACGA rates, which the General Conference Corporation generally accepts for use by church organizations, will rarely lose money on a gift annuity even if the annuitant(s) exceed(s) life expectancy and investment performance is mediocre.

- Slides: 45