Life Cycle Costing an effective asset Welcome management

- Slides: 23

Life Cycle Costing: an effective asset. Welcome management tool “Applying LCC contributes to more costeffective management control of the production facilities of small and medium enterprises (SMEs)” Verdediging afstuderen Asset Management Control B. Kemps

Life Cycle Costing: an an effective asset management tool “Applying LCC contributes to more costeffective. LCC management of costthe “Applying contributescontrol to more productioncontrol of the effective management facilities of small and medium enterprises production facilities of small (SMEs)” and medium enterprises (SMEs)”

Introduction • • Hypothesis Central question Research approach Scope of LCC related to the case study Used LCC model Experimental research conclusions Recommendations

Hypothesis “Applying LCC contributes to more cost-effective management control of production facilities of SMEs. ”

Research question: “How can within a purchasing strategy life cycle cost analysis contribute to improve cost-effective management control throughout SME’s? ”

Exploratory-empirical research approach

Scope of LCC related to the case Perspectives of a life cycle: • Life cycle of the market • Life cycle of the production proces (producer) • Life cycle of the product (customer perspective) Difference between • Life Cycle Costing • Life Cycle Cost Analysis

Scope of LCC related to the case Environment air, sea, land Disposal Mining Clean fuel production Material demanufacture Energy recovery with incineration ial ater m led cyc f re ng o essi roc Rep Product demanufacture Material Processing Monomer / raw material regeneration Remanufacture of reusable components Product take - back Direct recycling Product manufacture Distribution Use + Service Area of interest LCC Analysis Production Installations (like Costumer Perspective) Life Cycle Production Perspective

Scope of LCC related to the case Option A Option B Manufacture parameters Purchase Requirements Option X Operating Support Maintenance Second-hand Spare Demolition € Disposal Area of interest LCC Analysis Production Installations

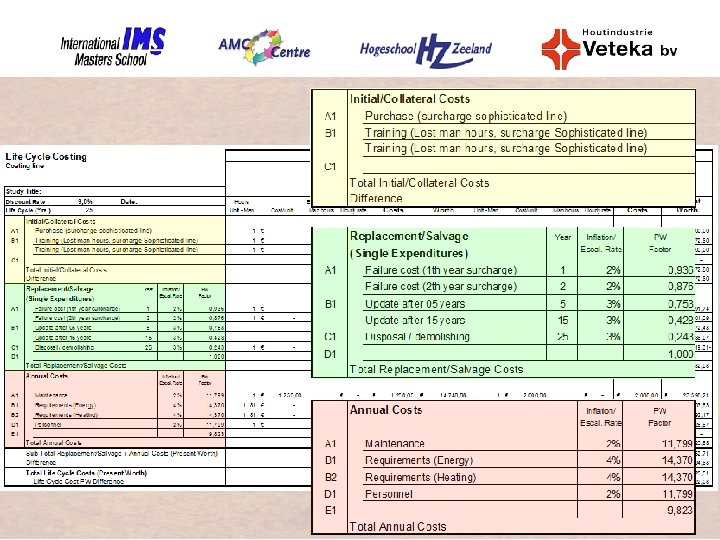

Used LCC Model Dell Isola & Kirk • • • Practical in use Handles a discount and escalation rate Excel based Results easy to interpret Integrated Monte Carlo methods

Used LCC Model

Used LCC Model

Experimental research

Case 4: Double vacuum box

€ 50, 000 Case 4: Double vacuum box € 40, 000 € 30, 000 € 20, 000 € 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 € -10, 000 € -20, 000 € -30, 000 Graph 1, reference Graph 2, discount rate Graph 3, escalation rate Graph 4, surcharge € -40, 000 Graph 1, Graph 2, Graph 3, Graph 4, reference discount rate escalation rate surcharge Discount rate: 9% 7% 9% 9% Escalation labour costs: 2% 2% 4% 2% Escalation hardware costs: 3% 3% 5% 3% Escalation energy costs: 4% 4% 6% 4% Surcharge double box: € 15. 000, 00 € 30. 000, 00 Standard labour costs (/hour): € 20, 10 € 20, 10 Overtime costs (/hour): € 0, 29 € 0, 29 Technical staff costs (/hour): € 25, 00 € 25, 00

Case 4: Monte Carlo - Distribution

Case 4: Monte Carlo Uncertainty Sensitivity

Outcomes from the experimental research • Objective data to compare alternatives • The excel graphs clearly visualizes the impact when changing a parameter • Impact of the discount rate • Transparancy among hidden costs • The importance of accurate parameters • New insights on alternatives

Conclusions • A customer perspective is most appropriate related to this thesis • The modified model of Dell Isola and Kirk has been very useful • More cost effective management: • More data based decisions • Uncertainties and sensitivities can be discussed and evaluated • New perspectives with LCC analysis

Conclusions • Defining an appropriate discount rate • Hidden costs will be revealed with LCC analysis • Using LCC analysis, with only little input parameters it is possible to compare alternatives. • Always use LCC analysis

Recommendations • Further investigation into an appropriate discount rate and escalation rate is necessary. • Further investigation on the input data is recommended. (setting times, RAM’s analysis) • In future investments it is advisible to use LCC analysis.

Life Cycle Costing: an effective Personal Reflection asset management tool “Applying LCC contributes to more costeffective management control of the production Any and questions? facilities of small medium enterprises (SMEs)” Thanks Verdediging afstuderen Asset Management Control B. Kemps