Life and Non Life insurance companies in India

Act, general")

")

is a company registered under the Companies")

: An AFC is")

- Slides: 33

Life and Non Life insurance companies in India

q Insurance has been described as “the product everyone buys, but no one wants to use. ” q Insurance contracts are often described as “least read best sellers. ” q Through insurance, risk transfer take place. q Insurance institutions offer social security and invest the savings of the individuals. q. Insurance in India is influenced by other countries, England in particular.

History q the life insurance business in India was started in 1818 with the establishment of the Oriental Life Insurance Company in Calcutta. q The Indian Life Assurance Companies Act, 1912 it was first statutory measure to regulate life insurance business. q New Insurance act was passed as Insurance Act, 1938 for comprehensive provisions for effective control. q. In 1956, Life Insurance sector got nationalised.

q The LIC absorbed 154 Indian, 16 non-Indian insurers and 75 provident societies. q. LIC had a monopoly till the late 90 s when the insurance sector was reopened to the private sector. q. The Malhotra Committee was appointed in 1993 by Govt. for insurance sector reforms.

Malhotra Committee Recommendations q Private sector was allowed to begin insurance business in India. q. Foreign companies were allowed to enter into Indian financial system with collaboration of Indian companies. q. Insurance regulatory body is to be setup to regulate insurance business in India. ( IRDAI) q Restructuring of LIC. q. No companies would be allowed to do both Life And Non-Life Insurance business.

Life Insurance Companies In India q Total of 24 life insurance companies in India. Of these, Life Insurance Corporation of India (LIC) is the only public sector insurance company. All others are private insurance companies. q. Most private players have tied up with international insurance giants for their life insurance foray. q. Private life insurance companies in India got access in 2000.

Non-Life Insurance q It is commonly called as General Insurance. q General Insurance is related to Motor, Health, Travel and Home insurance. q The popularity of General Insurance increases due to the industrial revolution in the west and growth of sea trade and commerce. q. Triton Insurance Company Ltd was setup in 1850 in Calcutta by the British govt. q. In 1972 with the passing of the General Insurance Business (Nationalisation) Act, general insurance business was nationalized.

q. In 1972 with the passing of the General Insurance Business (Nationalisation) Act, general insurance business was nationalized. q 107 insurers were amalgamated and grouped into four companies, namely National Insurance Company Ltd. , the New India Assurance Company Ltd. , the Oriental Insurance Company Ltd and the United India Insurance Company Ltd. q. The General Insurance Corporation of India was incorporated as a company in 1971 and it commence business on January 1 st 1973. q. GIC was formed to control and operate the business of general insurance in India. The GOI transferred all the assets and operations of the nationalized general insurance companies to GIC.

q In December, 2000, the subsidiaries of the General Insurance Corporation of India were restructured as independent companies and at the same time GIC was converted into a national re-insurer. Parliament passed a bill de-linking the four subsidiaries from GIC in July, 2002. q. There are 34 Non-Life Insurance Companies in India.

Mutual Funds

q Mutual fund is an investment company that sells shares and uses the proceeds to manage a portfolio of securities. q. Major suppliers of funds in financial market. q. Actively participate in primary market and secondary market. q. Accommodate the needs of the corporation, individual investors, government. q. Particularly helpful for small investor in their portfolio diversification.

q. Preference of the investors is consider by the mutual funds in their investment. q. Mutual funds are managed by professional money manager. q. Mutual funds charge fee for the management of fund which vary from one fund to another. q Investment objective of the fund is stated in the prospectus. q. The value of Mutual fund company depends on the performance of the securities. q. No voting right is available to the investor.

Types of Mutual Fund 1. Equity funds 1. Growth Funds- High return, Moderate risk, focus more on value increase than steady income. 2. Income Funds- stable dividend. 3. Growth and Income Funds- Combination of both. 4. International Funds- impacted by currency change. 5. Specialty Funds- focus on one sector(energy, banking etc. ) 6. Index fund- same securities as in index.

• 2. Bond Mutual Fund 1. Income fund –stable income, less credit risk. 2. Tax Free funds- Investment to lower tax liability. 3. High Yield Bond Fund- Junk Bond. 3. Balanced Fund 4. Money Market Fund 5. Gilt Fund 6. Real Estate Fund

NBFC ( NON BANKING FINANCIAL COMPANY)

q. A Non Banking Financial Company (NBFC) is a company registered under the Companies Act, 2013 or Act 1956 of India, engaged in the business of loans and advances, acquisition of shares, stock, bonds, hire-purchase, insurance business and chit-fund business. q. NBFC has financial activity as a principal business. q. Financial activity as principal business is when a company’s financial assets constitute more than 50 per cent of the total assets and income from financial assets constitute more than 50 per cent of the gross income.

Difference between NBFC and Banks q NBFC cannot accept demand deposits. q NBFCs do not form part of the payment and settlement system and cannot issue cheques drawn on itself. q. Deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation is not available to depositors of NBFCs, unlike in case of banks.

q In Section 45 -IA of the RBI Act, 1934, no Non-banking Financial company can commence or carry on business of a non-banking financial institution without obtaining a certificate of registration from the Bank and without having a Net Owned Funds of ₹ 25 lakhs. (₹ Two crore since April 1999). q. NBFCs whose asset size is of ₹ 500 cr or more as per last audited balance sheet are considered as systemically important NBFCs.

q Certain categories of NBFCs which are regulated by other regulators are exempted from the requirement of registration with RBI I. Venture Capital Fund/Merchant Banking companies/Stock broking companies registered with SEBI. Insurance Company holding a valid Certificate of Registration issued by IRDA. III. Nidhi companies as notified under Section 620 A of the Companies Act, 1956. IV. Chit companies as defined in clause (b) of Section 2 of the Chit Funds Act, 1982. V. Housing Finance Companies regulated by National Housing Bank.

Types of NBFCs in India q. Asset Finance Company (AFC) : An AFC is a company which is a financial institution carrying on as its principal business the financing of physical assets. q. Investment Company (IC) : IC means any company which is a financial institution carrying on as its principal business the acquisition of securities. q. Loan Company (LC): LC means any company which is a financial institution carrying on as its principal business the providing of finance whether by making loans or advances or otherwise for any activity other than its own but does not include an Asset Finance Company.

q. Reserve Bank of India has deregulated interest rates to be charged to borrowers by financial institutions (other than NBFC- Micro Finance Institution). The rate of interest to be charged by the company is governed by the terms and conditions of the loan agreement entered into between the borrower and the NBFCs. q NBFCs may get itself rated by any of the six rating agencies namely, CRISIL, CARE, ICRA, FITCH Ratings India Pvt. Ltd, Brickwork Ratings India Pvt. Ltd. and SMERA.

Important Regulations relating to Acceptance Of Deposits by NBFCs q. The NBFCs are allowed to accept/renew public deposits for a minimum period of 12 months and maximum period of 60 months. They cannot accept deposits repayable on demand. q. NBFCs cannot offer interest rates higher than the ceiling rate prescribed by RBI from time to time. The present ceiling is 12. 5 per cent per annum. q. NBFCs cannot offer gifts/incentives or any other additional benefit to the depositors. q. NBFCs should have minimum investment grade credit rating.

q. The deposits with NBFCs are not insured. q. The repayment of deposits by NBFCs is not guaranteed by RBI. q. Certain mandatory disclosures are to be made about the company in the Application Form issued by the company soliciting deposits.

Role of NBFC q Inclusive economic growth. q Innovative financial services to their customers. q. Employment generation. q Wealth creation. q. Financial assistance and guidance.

q Delivering Credit to unorganised sector. q Cheaper loans to their customers. q Support various sector and helps in development of that sector. q NBFC uses innovative technology to satisfy their customers. q. Strengthening of Financial Market

Problems related to NBFC q Proportion of debt is high. q Asset- Liability mismatch. q. Too Big to Fail. q. Liquidity problem. q. Not backed by government.

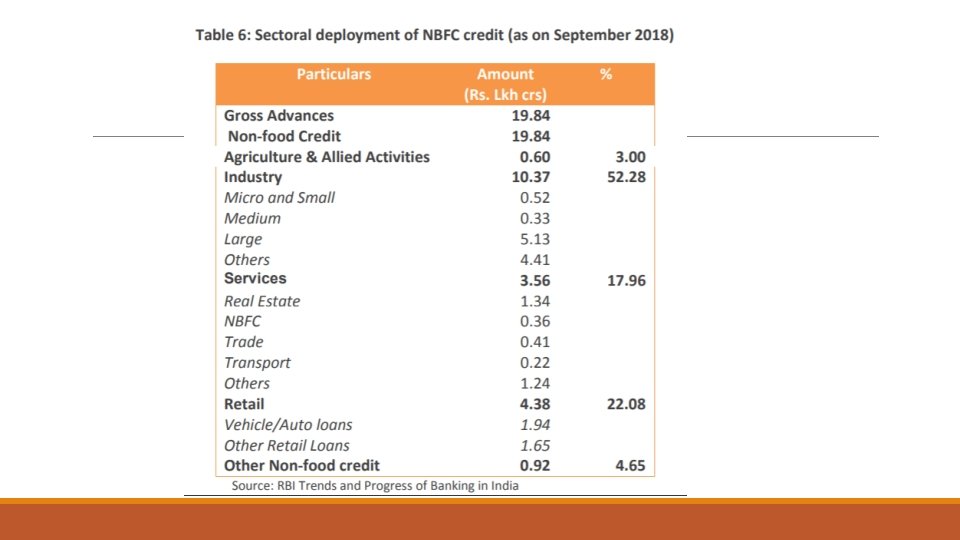

NBFC in India q The NBFC sector, with a size of around 15% of SCBs’ combined balance sheet, has been growing robustly in recent years, providing an alternative source of funds to the commercial sector in the face of slowing bank credit. q. The total balance sheet size of the NBFC-ND-SI comprises 85. 4% of the total balance sheet size of the NBFC sector with the balance 14. 6% accounted by NBFC-D. q. In case of NBFC-ND-SI, 68% of the outstanding borrowing as on 30 September, 2018 is in the form debentures and banks, while NBFC-D have 62% of the outstanding borrowings as bank borrowings and debentures. 42% of the outstanding borrowings of NBFC-ND-SI are debentures while 32% of the outstanding borrowings of NBFC-D is raised via debentures.

q Infrastructure finance companies and loan companies are the ones which have the highest quantum of loans and advances amounting to Rs. 13. 31 lakh crs. This is 81% of the total loans advances by the NBFC sector. q. The total income of the NBFC-ND-SI companies aggregating to Rs. 1. 11 lakh crs comprise around 80% of total income of the NBFC sector.