Liberty BOLD Living Annuity What is a Living

Liberty BOLD Living Annuity

What is a Living Annuity?

90% choose a Living Annuity

Living Annuity Draw down 2. 5% – 17. 5% Greater investment choice BUT: more choice can = bad choice …

Liberty Bold Living Annuity offers clients both the possibility of growth and a BOLD risk enabler guarantee that they won’t lose all their money!

BOLD Risk Enabler Guarantee: Allows investors to make more BOLD investment decisions Allows policyholders to take on more investment risk A “peace of mind” guarantee

Policy Unit Price: Depends on the performance on the underlying investments Each policy gets a policy unit price calculated specific to that policy Measures the growth on the underlying investment portfolios

High Water Mark: Locks in 80% of the highest policy unit price 80% of this high water mark is the guarantee level The highest level reached by the policy unit price as measured at the end of every 3 months

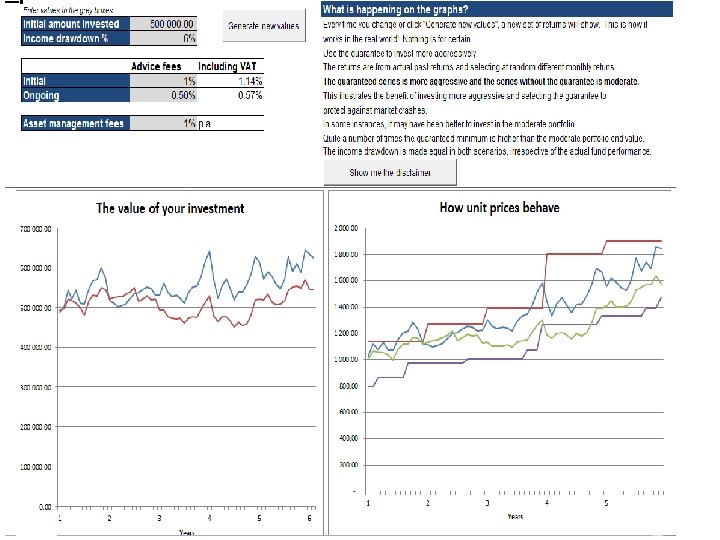

How does the Guarantee Work? 140 120 Unit price 100 80 60 40 20 0 0 3 6 9 12 Months Unit price Guarantee level 15

What do you Get? 140 120 Unit price 100 80 60 40 20 0 0 3 6 Months 9 12 15 1200 Your Income 1000 800 600 400 200 0 0 1 2 3 4 5 6 7 You pay 8 Months Liberty pays 9 10 11 12 13 14 15 16

What are we Offering? Liberty BOLD Living Annuity OAF applies Risk Enabler Guarantee 80% HWM on total investment 80% HWM in on income HWM on total investment only vests after five years Cycle then restarts Very competitive fee structure

Growth Sharing: Applies if the BOLD Risk Enabler Guarantee selected Refers to a portion of the growth above target return that is shared with Liberty

Target Return: The percentage of return above which a growth sharing deduction will apply If the Bold Risk Enabler Guarantee is selected

Price of Guarantee • Initial fee of 1% • On annual basis, only pay if performance exceeds the Target Return – 20% of growth above the 14% Target Return

How do you Pay for the Guarantee? 160 140 120 Unit price 100 What happens here? 80 60 40 20 0 0 3 6 Unit price Months 9 Target Return 12 15

How do you Pay for the Guarantee? You share the growth that is above the Target Return only at the end of each year (from guarantee inception) 100 90 20 Liberty’s share 80 Investor’s share 80 70 60 % Split Growth above target return 50 40 30 20 10 0

Differences to existing HWM guarantees • Always remain invested fully in the portfolio selected • With Bold - small initial fee and thereafter only pay if performance exceeds the target Return • Other – annual fee regardless of performance AND impact of cash drag • Choice of 200 funds with ability to switch between them while retaining guarantee

Risk Enabler Guarantee Year 1 Year 2 Year 3 Year 4 Guarantee resets after 5 years Add the Guarantee at any time Don’t have to have it when you start Stop the guarantee at any time 1% guarantee charge applies every time the guarantee is taken up Guarantee pays on: Income drawdown Fifth anniversary of guarantee inception Death Year 5

Below R 1 million 0.")

Platform Charges Overall investment value Platform charge (including VAT) Below R 1 million 0. 57% Below R 3 million 0. 40% More than R 3 million 0. 29%

Charges Initial charges Ongoing Fees Initial Advice Initial Fee guarantee charge Guarantee Fee Ongoing Advice Fee Growth Sharing 0 -1. 14% p. a. 0 -1. 71% Explicit deduction before allocating investment Platform Fee Portfolio Fee 1% 0. 285%-0. 57% TER (incl VAT) Depending on whether the optional guarantee is taken Initial guarantee charge also applies when switching on a guarantee at a later stage No annual guarantee charge, although there Depending on will be a Taken from balance in underlying unit deduction for investment trusts chosen Growth balance account Sharing at the end of a growth sharing year

Premiums • Minimum premium of R 150 000 • Additional investments only allowed within a certain period and percent to the initial investment if a guarantee exists: § R 50 000 • Additional investments allowed on all policies where no guarantee exists • Compulsory source

Flexibility Commutations are allowed if the value within the fund falls below a specific value The investor may transfer their Living Annuity to another registered insurer through a directive 135 process The Living Annuity can be converted to a Life Annuity at any point

Thank You Questions?

- Slides: 24