Lecture 4 Measuring Risk Return Volatility I Uncertain

I. Uncertain Cash Flows - Risk Adjustment")

TO MEASURE RISK WE NEED A GOAL")

HOW TO MEASURE WHAT TO EXPECT •")

USE VARIANCE TO MEASURE TOTAL RISK 2")

TO GET")

Correlation • Statistical Measure of the Degree")

We")

")

")

")

GENERAL FORMULA Bp =")

QUESTION: If an asset has a B")

CONSIDER STOCK PRICE AND CAPM P =")

- Slides: 21

Lecture: 4 - Measuring Risk (Return Volatility) I. Uncertain Cash Flows - Risk Adjustment II. We Want a Measure of Risk With the Following Features a. Easy to Calculate b. Ranks Assets According to Compensated Risk c. Can be Translated into a Discount Rate, k III. Economy-Wide or Systemic Risk -> Beta Works best for a portfolio of assets. IV. Non-Systematic or Company Specific Risk -> Variance Works best for a single asset.

Lecture: 4 - Measuring Risk (Return Volatility) TO MEASURE RISK WE NEED A GOAL VARIABLE. INVESTORS’ GOAL VARIABLE IS RETURNS % Return = = + = % capital gain (loss) + % Dividend Yield %R = =. 40 or 40% QUESTION: What is risk , or, what does risk-free mean? ANSWER: If exante expected returns always equal expost returns for an investment then we say it is risk- free. If actual returns are sometimes larger and sometimes smaller than expected, the investment carries risk. (we are happy with large ones but unhappy with small ones). A measure of risk should tell us the likelihood that we will not get what we expect and the magnitude of how different our returns will be from the expected.

Lecture: 4 - Measuring Risk (Return Volatility) HOW TO MEASURE WHAT TO EXPECT • Enumerate outcomes i. e. , the different risk scenarios. • Generate a probability distribution - attach probabilities to each scenario that sum to 1 (remember statistics course) EXAMPLE Economic Scenarios High growth ( 5%) Low growth (3%) Recession (-3%) Prob. 30. 40. 30 Sum = 1 IBM Return. 25. 15. 05 Get mean return - expected return - best guess (Note: Book uses k instead of R) E(R) = P i Ri = E(R) = (. 3 *. 25) + (. 4 *. 15) + (. 3 *. 05) =. 15

Lecture: 4 - Measuring Risk (Return Volatility) USE VARIANCE TO MEASURE TOTAL RISK 2 = (Ri - ) 2 Pi or standard deviation; = [ 2]. 5 For IBM 2 IBM = (. 25 -. 15)2(. 3) + (. 15 -. 15)2(. 4) + (. 05 -. 15)2(. 3) =. 006 QUESTION: What is the variance of a stock which has a mean of. 15 and returns of. 15 in all states of the economy? - Zero! VARIANCE FOR A SINGLE ASSET CONTAINS a. Diversifiable Risk (Firm Specific) easily by diversification at little or no cost. b. Undiversified (System) Risk cannot be eliminated through diversification.

Variance Measures the Dispersion of a Distribution Around Its Mean Lecture: 4 - Measuring Risk (Return Volatility)

A Standarized Risk Measure Coefficient of Variation = Standard Deviation/Mean Lecture: 4 - Measuring Risk (Return Volatility)

Portfolio Mean Return and Variance Lecture: 4 - Measuring Risk (Return Volatility) TO GET THE VARIANCE OF A PORTFOLIO WE NEED TO CALCULATE THE PORTFOLIO MEAN RETURN. Portfolio mean return is a linear, weighted average of individual mean returns of the assets in the portfolio. GETTING THE WEIGHTS INVESTMENT $ INVESTED Wi 1 2 3 100 200 100/500 =. 2 200/500 =. 4 E(Rp) = W 1 + W 2 . 10. 05. 15 + W 3 =. 2(. 1) +. 4(. 05) +. 4(. 15) =. 10 GENERAL => E(Rp) = Wi =

Portfolio Variance is More Complex A Nonlinear Function Lecture: 4 - Measuring Risk (Return Volatility) For a two asset portfolio: p 2 = W 12 + W 22 + 2 W 1 W 2 Cov 12 where: Cov 12 = covariance = Corr 12 1 2 and Corr 12 = correlation QUESTION: Diversification reduces variance of portfolio even when corr=0. WHY? - Some asset-specific risk offset one another.

It’s usually best to diversify, except in this case.

Lecture: 4 - Measuring Risk (Return Volatility) Correlation • Statistical Measure of the Degree of Linear Relationship Between Two Random Variables • Range: + 1. 0 to -1. 0 • + 1. 0 - Move Up and Down Together - Exactly the Same Rate • 0. 0 - No Relationship Between the Returns • - 1. 0 - Move Exactly Opposite Each Other

Covariance is a Measure of Risk and Beta is a Standardized Covariance Lecture: 4 - Measuring Risk (Return Volatility) Covariance Measures How Closely Returns For Two Assets. Track Each Other (Closeness to the Regression Line) All else equal, covariance is large when the data points fall along the regression line instead of away from it because, on the line, the deviations from the means of each variable are equal – the products are squares - larger than otherwise.

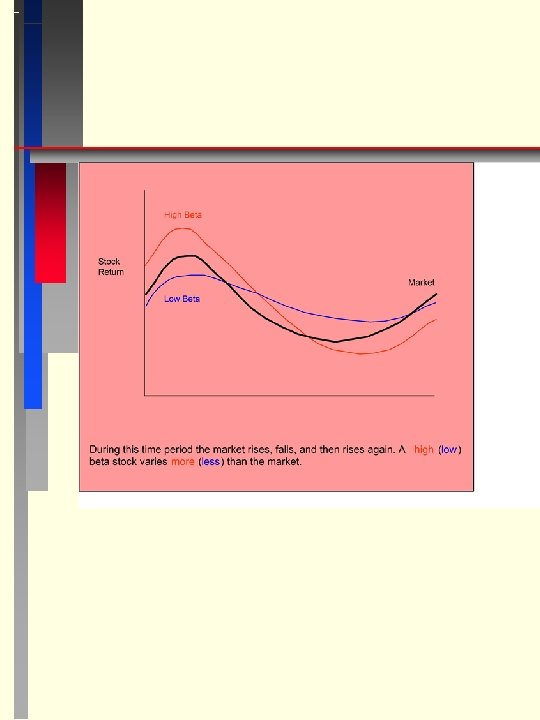

Beta Is a Standardized Covariance Measure Lecture: 4 - Measuring Risk (Return Volatility) We Need Beta (Standardized Covariance Measure) in Order to Make Comparisons of Risk Between Assets or Portfolios. • Measured Relative to the Market Portfolio (the most diversified portfolio is the standard) • Slope of the Regression Line • Slopes Measured Relative to Market Return General Formula Betai = = Beta and the Market (Illustration) • Beta = 1 - Same as Market Risk • Beta > 1 - Riskier than Market • Beta < 1 - Less Risky than Market • Beta = 2 - Twice as Risky as Market

Positive Beta Lecture: 4 - Measuring Risk (Return Volatility)

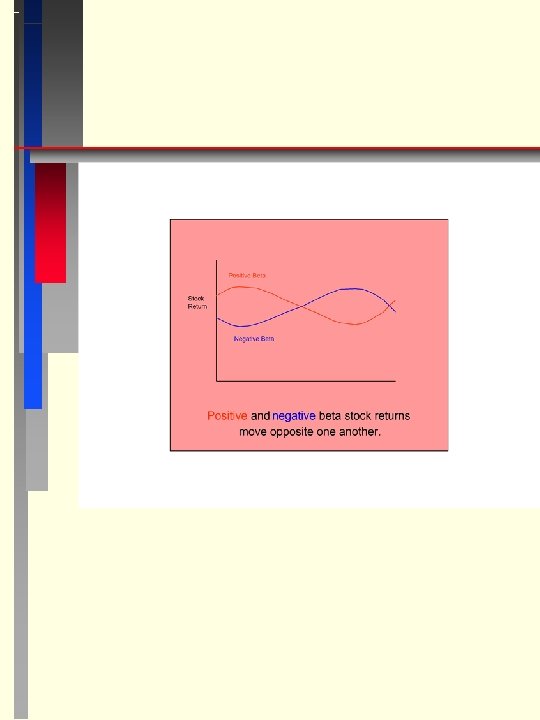

Negative Beta Lecture: 4 - Measuring Risk (Return Volatility)

Zero Beta Lecture: 4 - Measuring Risk (Return Volatility)

Port folio Beta Lecture: 4 - Measuring Risk (Return Volatility) GENERAL FORMULA Bp = Wi Bi Example: Beta for a portfolio containing three stocks. INVESTMENT $ INVESTED Wi 1 2 3 100 400 500 100/1000 =. 1 400/1000 =. 4 500/1000 =. 5 Bp = W 1 B 1 + W 2 B 2 + W 3 B 3 =. 1(2) +. 4(1. 5) +. 5(. 5) = 1. 05 Bi 2. 0 1. 5 0. 5

CAPM “Beta is Useful Because it Can Be Precisely Translated into a Required Return, k, Using the Capital Asset Pricing Model” Lecture 4 - Measuring Risk (Return Volatility) CAPM (Capital Asset Pricing Model) General Formula Ri = ki = Rf + Bi(Rm - Rf) = time value + (units of risk) x (price per unit) = time value + risk premium where, Rf = Risk-Free Rate -> T-Bill Rm = Expected Market Return -> S&P 500 Bi = Beta of Stock i Example: Suppose that a firm has only equity, is twice as risky as the market and the risk free rate is 10% and expected market return is 15%. What is the firm’s required rate? Ri = ki = Rf + Bi(Rm - Rf) = 10% + 2(15% - 10%) = 10% + 10% = 20%

Lecture: 4 - Measuring Risk (Return Volatility) QUESTION: If an asset has a B = 0, what is its return? -> Rf QUESTION: If an asset has a B = 1, what is its return? -> Rm QUESTION: Suppose E(R 1) > E(R 2) AND B 1 < B 2, which asset do you choose? -> 1 QUESTION: How about if E(R 1) > E(R 2) and B 1 > B 2 ? Now we need to know B 1 and B 2 and use the CAPM

Lecture: 4 - Measuring Risk (Return Volatility) CONSIDER STOCK PRICE AND CAPM P = Ri = ki = Rf + Bi(Rm - Rf) QUESTIONS: What happens to price as growth increases? P increases! What happens to price if k increases? P Decreases! What happens to price if Beta decreases? P increases! What happens to price if Rf increases? B >1 ->P increase B<1 -> P decrease What happens to price if Rm decreases? P increases! QUESTION: As financial managers, what variables should we try to change and in what directions? 1. Increase cash flows - or growth in CF’s make superior investment decisions, use the lowest cost financing or manipulate debt/equity ratio 2. Bring cash flows in closer to the present 3. Decrease Beta - Manipulate assets (Labor. Capital ratio).