Lecture 13 Country Risk Analysis Lecture Review Capital

Stable Unacceptable Acceptable Zone Unclear Zone Unstable Political")

$ Foreign Acquisitions of U. S. Firms U. S.")

$ World-wide Cross-Border Acquisitions")

can be")

Canada U. S. Japan Germany")

• These are")

• These are")

• Sight drafts")

• Time drafts")

– These are issued by a bank")

The required documents typically include a draft")

Advice Number: BA 000000094 Amount: Issue Bank Ref: 1234/LMC/5678")

Seller (Exporter) Deliver Goods Request for Credit")

– Variations include • standby L/Cs :")

– This is a time draft that is")

¤ The bank accepting the drafts charges an")

– The importer issues a promissory")

• OPIC is a")

- Slides: 140

Lecture 13

Country Risk Analysis

Lecture Review • • • Capital Budgeting Subsidiary versus Parent Perspective Remitting Subsidiary Earnings to the Parent Input for Multinational Capital Budgeting Multinational Capital Formula Subsidiary versus Parent Perspective Input for Multinational Capital Budgeting Analysis Factors to Consider in Multinational Capital Budgeting Impact of Multinational Capital Budgeting on an MNC’s Value

Country Risk Analysis

Country Risk Analysis • Country risk represents the potentially adverse impact of a country’s environment on the MNC’s cash flows.

Country Risk Analysis • Country risk can be used: – to monitor countries where the MNC is presently doing business; – as a screening device to avoid conducting business in countries with excessive risk; and – to improve the analysis used in making long-term investment or financing decisions.

Political Risk Factors • Attitude of Consumers in the Host Country – Some consumers may be very loyal to homemade products. • Attitude of Host Government – The host government may impose special requirements or taxes, restrict fund transfers, subsidize local firms, or fail to enforce copyright laws.

Political Risk Factors • Blockage of Fund Transfers – Funds that are blocked may not be optimally used. • Currency Inconvertibility – The MNC parent may need to exchange earnings for goods.

Political Risk Factors • War – Internal and external battles, or even the threat of war, can have devastating effects. • Bureaucracy – Bureaucracy can complicate businesses. • Corruption – Corruption can increase the cost of conducting business or reduce revenue.

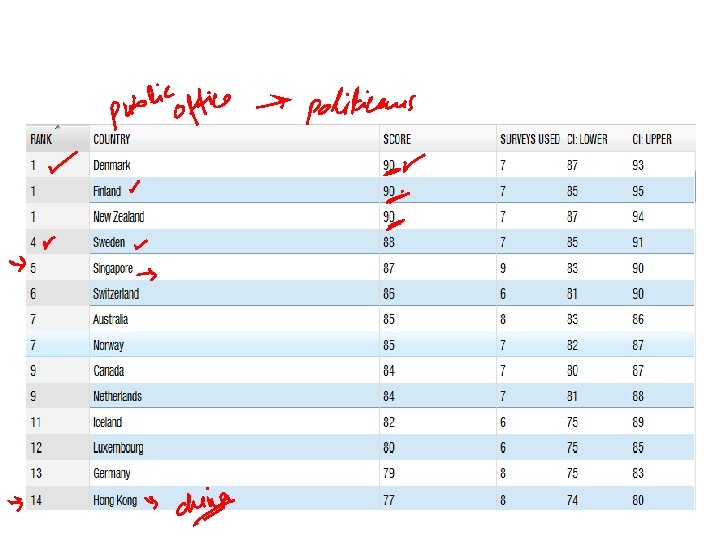

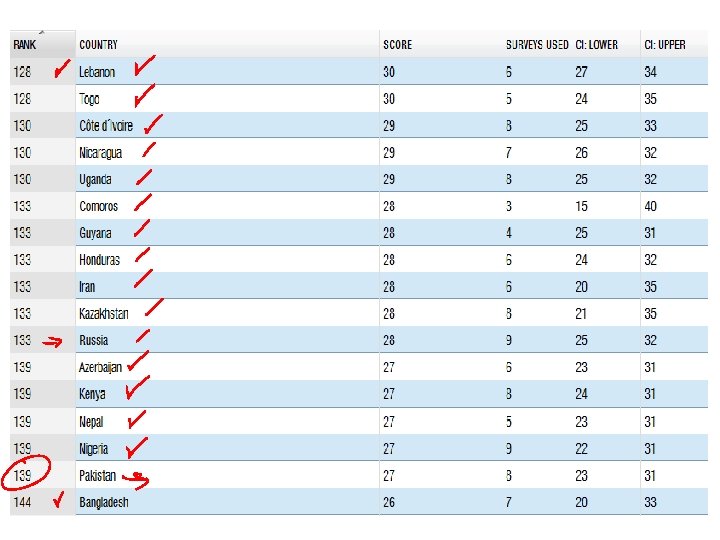

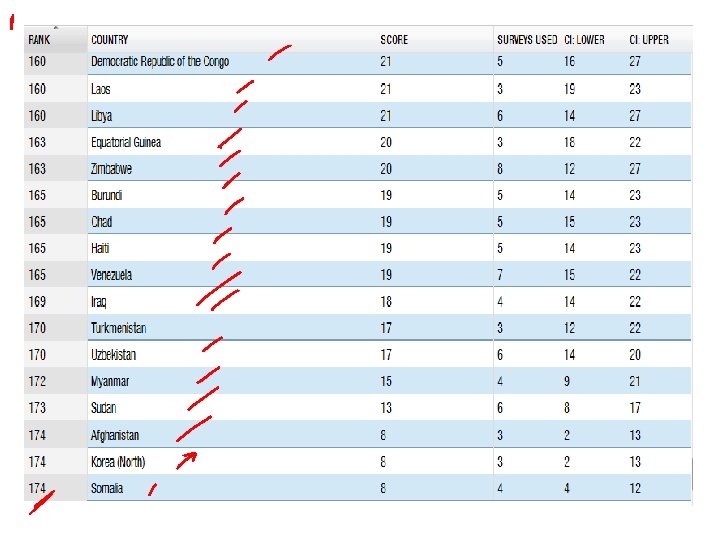

Corruption Perceptions Index • The index, which is published by Transparency International, reflects the degree to which corruption is perceived to exist among public officials and politicians. • Data is given for 2012.

Financial Risk Factors • Current and Potential State of the Country’s Economy – A recession can severely reduce demand. – Financial distress can also cause the government to restrict MNC operations. • Indicators of Economic Growth – A country’s economic growth is dependent on several financial factors - interest rates, exchange rates, inflation, etc.

Types of Country Risk Assessment • A macro-assessment of country risk is an overall risk assessment of a country without consideration of the MNC’s business. • A micro-assessment of country risk is the risk assessment of a country as related to the MNC’s type of business.

Types of Country Risk Assessment • The overall assessment of country risk thus consists of : Macro-political risk Macro-financial risk Micro-political risk Micro-financial risk

Types of Country Risk Assessment • Note that the opinions of different risk assessors often differ due to subjectivities in: – identifying the relevant political and financial factors, – determining the relative importance of each factor, and – predicting the values of factors that cannot be measured objectively.

Techniques of Assessing Country Risk • A checklist approach involves rating and weighting all the identified factors, and then consolidating the rates and weights to produce an overall assessment. • The Delphi technique involves collecting various independent opinions and then averaging and measuring the dispersion of those opinions.

Techniques of Assessing Country Risk • Quantitative analysis techniques like regression analysis can be applied to historical data to assess the sensitivity of a business to various risk factors. • Inspection visits involve traveling to a country and meeting with government officials, firm executives, and/or consumers to clarify uncertainties.

Techniques of Assessing Country Risk • Often, firms use a variety of techniques for making country risk assessments. • For example, they may use a checklist approach to develop an overall country risk rating, and some of the other techniques to assign ratings to the factors considered.

Developing A Country Risk Rating • A checklist approach will require the following steps: Assign values and weights to the political risk factors. Multiply the factor values with their respective weights, and sum up to give the political risk rating. Derive the financial risk rating similarly.

Developing A Country Risk Rating • A checklist approach will require the following steps: Assign weights to the political and financial ratings according to their perceived importance. Multiply the ratings with their respective weights, and sum up to give the overall country risk rating.

Developing A Country Risk Rating • Different country risk assessors have their own individual procedures for quantifying country risk. • Although most procedures involve rating and weighting individual risk factors, the number, type, rating, and weighting of the factors will vary with the country being assessed, as well as the type of corporate operations being planned.

Developing A Country Risk Rating • Firms may use country risk ratings when screening potential projects, or when monitoring existing projects. • For example, decisions regarding subsidiary expansion, fund transfers to the parent, and sources of financing, can all be affected by changes in the country risk rating.

Comparing Risk Ratings Among Countries • One approach to comparing political and financial ratings among countries is the foreign investment risk matrix (FIRM ). • The matrix measures financial (or economic) risk on one axis and political risk on the other axis. • Each country can be positioned on the matrix based on its political and financial ratings.

The Foreign Investment Risk Matrix (FIRM) Stable Unacceptable Acceptable Zone Unclear Zone Unstable Political Risk Rating Financial Risk Rating Unacceptable Zone

Actual Country Risk Ratings Across Countries • Some countries are rated higher according to some risk factors, but lower according to others. • On the whole, industrialized countries tend to be rated highly, while emerging countries tend to have lower risk ratings. • Country risk ratings change over time in response to changes in the risk factors.

Incorporating Country Risk in Capital Budgeting • If the risk rating of a country is in the acceptable zone, the projects related to that country deserve further consideration. • Country risk can be incorporated into the capital budgeting analysis of a project by adjusting the discount rate, or by adjusting the estimated cash flows.

Incorporating Country Risk in Capital Budgeting • Adjustment of the Discount Rate – The higher the perceived risk, the higher the discount rate that should be applied to the project’s cash flows. • Adjustment of the Estimated Cash Flows – By estimating how the cash flows could be affected by each form of risk, the MNC can determine the probability distribution of the net present value of the project.

Applications of Country Risk Analysis • Alerted by its risk assessor, Gulf Oil planned to deal with the loss of Iranian oil, and was able to avoid major losses when the Shah of Iran fell four months later. • However, while the risk assessment of a country can be useful, it cannot always detect upcoming crises.

Applications of Country Risk Analysis • Iraq’s invasion of Kuwait was difficult to forecast, for example. Nevertheless, many MNCs promptly reassessed their exposure to country risk and revised their operations. • The 1997 -98 Asian crisis also showed that MNCs had underestimated the potential financial problems that could occur in the highgrowth Asian countries.

Reducing Exposure to Host Government Takeovers • The benefits of DFI can be offset by country risk, the most severe of which is a host government takeover. • To reduce the chance of a takeover by the host government, firms often use the following strategies: Use a Short-Term Horizon – This technique concentrates on recovering cash flow quickly.

Reducing Exposure to Host Government Takeovers Rely on Unique Supplies or Technology – In this way, the host government will not be able to take over and operate the subsidiary successfully. Hire Local Labor – The local employees can apply pressure on their government.

Reducing Exposure to Host Government Takeovers Borrow Local Funds – The local banks can apply pressure on their government. Purchase Insurance – Investment guarantee programs offered by the home country, host country, or an international agency insure to some extent various forms of country risk.

Chapter Review • Why Country Risk Analysis Is Important • Political Risk Factors – Attitude of Consumers in the Host Country – Attitude of Host Government – Blockage of Fund Transfers – Currency Inconvertibility – War – Bureaucracy – Corruption

Chapter Review • Financial Risk Factors – Current and Potential State of the Country’s Economy – Indicators of Economic Growth • Types of Country Risk Assessment – Macro-Assessment of Country Risk – Micro-Assessment of Country Risk

Chapter Review • Techniques of Assessing Country Risk – Checklist Approach – Delphi Technique – Quantitative Analysis – Inspection Visits – Combination of Techniques

Chapter Review • Developing a Country Risk Rating – Example of Measuring Country Risk – Variation in Methods of Measuring Country Risk – Using the Country Risk Rating for Decision. Making • Comparing Risk Ratings Among Countries • Actual Country Risk Ratings Across Countries

Chapter Review • Incorporating Country Risk in Capital Budgeting – Adjustment of the Discount Rate – Adjustment of the Estimated Cash Flows • Applications of Country Risk Analysis

Chapter Review • Reducing Exposure to Host Government Takeovers – Use a Short-Term Horizon – Rely on Unique Supplies or Technology – Hire Local Labor – Borrow Local Funds – Purchase Insurance • Impact of Country Risk on an MNC’s Value

Lecture 13 Multinational Restructuring

Multinational Restructuring • Building a new subsidiary, acquiring a company, selling an existing subsidiary, downsizing operations, or shifting production among subsidiaries, are all forms of multinational restructuring. • MNCs continually assess possible forms of multinational restructuring to capitalize on changing economic, political, and industrial conditions across countries.

International Acquisitions • Through an international acquisition, a firm can immediately expand its international business since the target is already in place, and benefit from already-established customer relationships. • However, establishing a new subsidiary usually costs less, and there will not be a need to integrate the parent management style with that of the acquired company.

Value of International Acquisitions (billions) $ Foreign Acquisitions of U. S. Firms U. S. Acquisitions of Foreign Firms

Value of International Acquisitions (billions) $ World-wide Cross-Border Acquisitions

International Acquisitions • Like any other long-term project, capital budgeting analysis can be used to determine whether a firm should be acquired. • Hence, the acquisition decision can be based on a comparison of the benefits and costs as measured by the net present value (NPV).

International Acquisitions • NPV = – initial outlay n + S t =1 cash flow in period t (1 + k )t salvage value + (1 + k )n k = the acquisition’s required rate of return n = the lifetime of the acquired firm • If NPV > 0, the firm can be acquired.

International Acquisitions • Note that the relevant exchange rate, taxes, and blocked-funds restriction, should be taken into account. • The cost of overcoming the barriers that may be imposed by the government agencies that monitor mergers and acquisitions should be taken into consideration too.

International Acquisitions • Examples of such barriers include laws against hostile takeovers, restricted foreign majority ownership, “red tape, ” and special requirements.

International Acquisitions • While the Asian crisis had devastating effects, it created an opportunity for some MNCs to pursue new business in Asia. • In Asia, property values had declined, the currencies were weakened, many firms were near bankruptcy, and the governments wanted to resolve the crisis. • However, these MNCs must not ignore the lowered economic growth in Asia too.

International Acquisitions • In Europe, the adoption of the euro as the local currency by several countries simplifies the analysis that an MNC has to perform when comparing various possible target firms in the participating countries.

Factors that Affect the Expected Cash Flows of the Foreign Target-Specific Factors Target’s previous cash flows. These may serve as an initial base from which future cash flows can be estimated. Managerial talent of the target. The acquiring firm may allow the acquired firm to be managed as it was before the acquisition, downsize the firm, or restructure its operations.

Factors that Affect the Expected Cash Flows of the Foreign Target Country-Specific Factors Target’s local economic conditions. Demand is likely to be higher when the economic conditions are strong. Target’s local political conditions. Cash flow shocks are less likely when the political conditions are favorable.

Factors that Affect the Expected Cash Flows of the Foreign Target Country-Specific Factors Target’s industry conditions. Industries with high growth potential and non-excessive competition are preferred. Target’s currency conditions. A currency that is expected to strengthen over time will usually be preferred.

Factors that Affect the Expected Cash Flows of the Foreign Target Country-Specific Factors Target’s local stock market conditions. When the local stock market prices are generally low, the target’s acceptable bid price is also likely to be low. Taxes applicable to the target. What matters to the acquiring firm is the after-tax cash flows that it will ultimately receive in the form of remitted funds.

The Valuation Process • Prospective targets are first screened to identify those that deserve a closer assessment. • Capital budgeting analysis is then applied to each of the targets that passed the initial screening process. • Only those targets that are priced lower than their perceived net present values may be worth acquiring.

Why Valuations of a Target May Vary Among MNCs Estimated cash flows of the foreign target. – Different MNCs will manage the target’s operations differently. – Each MNC may have a different plan for fitting the target within the structure of the MNC. – Acquirers based in certain countries may be subjected to less taxes on remitted earnings.

Why Valuations of a Target May Vary Among MNCs Exchange rate effects on remitted funds. – Different MNCs have different schedules for remitting funds from the target to the acquirer.

Why Valuations of a Target May Vary Among MNCs Required rate of return of the acquirer. – Different MNCs may have different plans for the target, such that the perceived risk of the target will be different. – The local risk-free interest rate may differ for MNCs based in different countries.

Other Types of Multinational Restructuring International Partial Acquisitions • An MNC may purchase a substantial portion of the existing stock of a foreign firm, so as to gain some control over the target’s management and operations. • The valuation of the firm depends on whether the MNC plans to acquire enough shares to control the firm (and hence influence its cash flows).

Other Types of Multinational Restructuring International Acquisitions of Privatized Businesses • Many MNCs have acquired businesses from foreign governments. • These businesses are usually difficult to value because the transition entails many uncertainties cash flows, benchmark data, economic and political conditions, exchange rates, financing costs, etc.

Other Types of Multinational Restructuring International Alliances • MNCs commonly engage in alliances, such as joint ventures and licensing agreements, with foreign firms. • The initial outlay is typically smaller, but the cash flows to be received will typically be smaller too.

Other Types of Multinational Restructuring International Divestitures • An MNC should periodically reassess its DFIs to determine whether to retain them or to sell (divest) them. • The MNC can compare the present value of the cash flows from the project if it is continued, to the proceeds that would be received (after taxes) if it is divested.

Restructuring Decisions As Real Options • Restructuring decisions may involve real options, or implicit options on real assets. • If a proposed project carries an option to pursue an additional venture, then the project has a call option on real assets. • If a proposed project carries an option to divest part or all of itself, then the project has a put option on real assets.

Restructuring Decisions As Real Options • The expected NPV of a project with real options may be estimated as the sum of the products of the probability of each scenario and the respective NPV for that scenario. E(NPV) = S pi NPVi i pi = probability of scenario i NPVi = NPV for scenario i

Chapter Review • Introduction to Multinational Restructuring • International Acquisitions – Trends in International Acquisitions – Model for Valuing a Foreign Target – Barriers to International Acquisitions – Assessing Potential Acquisitions in Asia and Europe

Chapter Review • Factors that Affect the Expected Cash Flows of the Foreign Target – Target-Specific Factors – Country-Specific Factors • The Valuation Process – International Screening Process – Estimating the Target’s Value

Chapter Review • Why a Target’s Value May Vary Among MNCs – Expected Cash Flows of the Target – Exchange Rate Effects on Remitted Funds • Required Return of the Acquirer. Other Types of Multinational Restructuring – International Partial Acquisitions – International Acquisitions of Privatized Businesses – International Alliances • International Divestitures • Restructuring Decisions as Real Options – Call and Put Options on Real Assets • Impact of Multinational Restructuring on an MNC’s Value

Chapter Review • Other Types of Multinational Restructuring – International Partial Acquisitions – International Acquisitions of Privatized Businesses – International Alliances • International Divestitures • Restructuring Decisions as Real Options – Call and Put Options on Real Assets • Impact of Multinational Restructuring on an MNC’s Value

End of Chapter

Multinational Cost of Capital & Capital Structure

Chapter Objectives • To explain how corporate and country characteristics influence an MNC’s cost of capital; • To explain why there are differences in the costs of capital across countries; and • To explain how corporate and country characteristics are considered by an MNC when it establishes its capital structure.

Cost of Capital • A firm’s capital consists of equity (retained earnings and funds obtained by issuing stock) and debt (borrowed funds). • The cost of equity reflects an opportunity cost, while the cost of debt is reflected in interest expenses. • Firms want a capital structure that will minimize their cost of capital, and hence the required rate of return on projects.

Cost of Capital • A firm’s weighted average cost of capital kc = ( D ) kd ( 1 _ t ) + ( E ) ke D+E where D E kd t ke D+E is the amount of debt of the firm is the equity of the firm is the before-tax cost of its debt is the corporate tax rate is the cost of financing with equity

Cost of Capital • The interest payments on debt are tax deductible. However, as interest expenses increase, the probability of bankruptcy will increase too. • It is favorable to increase the use of debt financing until the point at which the bankruptcy probability becomes large enough to offset the tax advantage of using debt.

Cost of Capital Debt’s Tradeoff Debt Ratio

Cost of Capital for MNCs • The cost of capital for MNCs may differ from that for domestic firms because of the following differences. Size of Firm. Because of their size, MNCs are often given preferential treatment by creditors. They can usually achieve smaller per unit flotation costs too.

Cost of Capital for MNCs Acess to International Capital Markets. MNCs are normally able to obtain funds through international capital markets, where the cost of funds may be lower. International Diversification. M NCs may have more stable cash inflows due to international diversification, such that their probability of bankruptcy may be lower.

Cost of Capital for MNCs Exposure to Exchange Rate Risk. MNCs may be more exposed to exchange rate fluctuations, such that their cash flows may be more uncertain and their probability of bankruptcy higher. Exposure to Country Risk. M NCs that have a higher percentage of assets invested in foreign countries are more exposed to country risk.

Cost of Capital for MNCs Larger size Greater access to international capital markets International diversification Exposure to exchange rate risk Exposure to country risk Preferential treatment from creditors Possible access to low-cost foreign financing Probability of bankruptcy Cost of capital

Cost of Capital for MNCs • The capital asset pricing model (CAPM) can be used to assess how the required rates of return of MNCs differ from those of purely domestic firms. • According to CAPM, ke = Rf + b (Rm – Rf ) where ke Rf Rm b = = the required return on a stock risk-free rate of return market return the beta of the stock

Cost of Capital for MNCs • A stock’s beta represents the sensitivity of the stock’s returns to market returns, just as a project’s beta represents the sensitivity of the project’s cash flows to market conditions. • The lower a project’s beta, the lower its systematic risk, and the lower its required rate of return, if its unsystematic risk can be diversified away.

Cost of Capital for MNCs • An MNC that increases its foreign sales may be able to reduce its stock’s beta, and hence the return required by investors. This translates into a lower overall cost of capital. • However, MNCs may consider unsystematic risk as an important factor when determining a foreign project’s required rate of return.

Cost of Capital for MNCs • Hence, we cannot be certain if an MNC will have a lower cost of capital than a purely domestic firm in the same industry.

Costs of Capital Across Countries • The cost of capital may vary across countries, such that: MNCs based in some countries may have a competitive advantage over others; MNCs may be able to adjust their international operations and sources of funds to capitalize on the differences; and MNCs based in some countries may have a more debt-intensive capital structure.

Costs of Capital Across Countries • The cost of debt to a firm is primarily determined by the prevailing risk-free interest rate of the borrowed currency and the risk premium required by creditors. • The risk-free rate is determined by the interaction of the supply and demand for funds. It may vary due to different tax laws, demographics, monetary policies, and economic conditions.

Costs of Capital Across Countries • The risk premium compensates creditors for the risk that the borrower may be unable to meet its payment obligations. • The risk premium may vary due to different economic conditions, relationships between corporations and creditors, government intervention, and degrees of financial leverage.

Costs of Capital Across Countries • Although the cost of debt may vary across countries, there is some positive correlation among country cost-of-debt levels over time.

Costs of Capital Across Countries Costs of Debt (%) Canada U. S. Japan Germany

Costs of Capital Across Countries • A country’s cost of equity represents an opportunity cost – what the shareholders could have earned on investments with similar risk if the equity funds had been distributed to them. • The return on equity can be measured by the risk-free interest rate plus a premium that reflects the risk of the firm.

Costs of Capital Across Countries • A country’s cost of equity can also be estimated by applying the price/earnings multiple to a given stream of earnings. • A high price/earnings multiple implies that the firm receives a high price when selling new stock for a given level of earnings. So, the cost of equity financing is low.

Costs of Capital Across Countries • The costs of debt and equity can be combined, using the relative proportions of debt and equity as weights, to derive an overall cost of capital.

Using the Cost of Capital for Assessing Foreign Projects • Foreign projects may have risk levels different from that of the MNC, such that the MNC’s weighted average cost of capital (WACC) may not be the appropriate required rate of return. • There are various ways to account for this risk differential in the capital budgeting process.

Using the Cost of Capital for Assessing Foreign Projects Derive NPVs based on the WACC. – The probability distribution of NPVs can be computed to determine the probability that the foreign project will generate a return that is at least equal to the firm’s WACC. Adjust the WACC for the risk differential. – The MNC may estimate the cost of equity and the after-tax cost of debt of the funds needed to finance the project.

The MNC’s Capital Structure Decision • The overall capital structure of an MNC is essentially a combination of the capital structures of the parent body and its subsidiaries. • The capital structure decision involves the choice of debt versus equity financing, and is influenced by both corporate and country characteristics.

The MNC’s Capital Structure Decision Corporate Characteristics • Stability of cash flows. MNCs with more stable cash flows can handle more debt. • Credit risk. MNCs that have lower credit risk have more access to credit. • Access to retained earnings. Profitable MNCs and MNCs with less growth may be able to finance most of their investment with retained earnings.

The MNC’s Capital Structure Decision Corporate Characteristics • Guarantees on debt. If the parent backs the subsidiary’s debt, the subsidiary may be able to borrow more. • Agency problems. Host country shareholders may monitor a subsidiary, though not from the parent’s perspective.

The MNC’s Capital Structure Decision Country Characteristics • Stock restrictions. MNCs in countries where investors have less investment opportunities may be able to raise equity at a lower cost. • Interest rates. MNCs may be able to obtain loanable funds (debt) at a lower cost in some countries.

The MNC’s Capital Structure Decision Country Characteristics • Strength of currencies. MNCs tend to borrow the host country currency if they expect it to weaken, so as to reduce their exposure to exchange rate risk. • Country risk. If the host government is likely to block funds or confiscate assets, the subsidiary may prefer debt financing.

The MNC’s Capital Structure Decision Country Characteristics • Tax laws. MNCs may use more local debt financing if the local tax rates (corporate tax rate, withholding tax rate, etc. ) are higher.

Interaction Between Subsidiary and Parent Financing Decisions Increased debt financing by the subsidiary Þ A larger amount of internal funds may be available to the parent. Þ The need for debt financing by the parent may be reduced. • The revised composition of debt financing may affect the interest charged on debt as well as the MNC’s overall exposure to exchange rate risk.

Interaction Between Subsidiary and Parent Financing Decisions Reduced debt financing by the subsidiary Þ A smaller amount of internal funds may be available to the parent. Þ The need for debt financing by the parent may be increased. • The revised composition of debt financing may affect the interest charged on debt as well as the MNC’s overall exposure to exchange rate risk.

Interaction Between Subsidiary and Parent Financing Decisions Host Country Conditions Higher Country Risk Lower Interest Rates Expected Weakness of Local Currency Blockage of Funds Higher Taxes Amount of Local Debt Financed by Subsidiary Internal Funds Available to Parent Amount of Debt Financed by Parent Higher Lower Higher Higher Lower

Using a Target Capital Structure on a Local versus Global Basis • An MNC may deviate from its “local” target capital structure as necessitated by local conditions. • However, the proportions of debt and equity financing in one subsidiary may be adjusted to offset an abnormal degree of financial leverage in another subsidiary. • Hence, the MNC may still achieve its “global” target capital structure.

Using a Target Capital Structure on a Local versus Global Basis • Note that a capital structure revision may result in a higher cost of capital. • Hence, an unusually high or low degree of financial leverage should only be adopted if the benefits outweigh the overall costs.

Using a Target Capital Structure on a Local versus Global Basis • The volumes of debt and equity issued in financial markets vary across countries, indicating that firms in some countries (such as Japan) have a higher degree of financial leverage on average. • However, conditions may change over time. In Germany for example, firms are shifting from local bank loans to the use of debt security and equity markets.

Chapter Review • Introduction to the Cost of Capital – Comparing the Costs of Equity and Debt • Cost of Capital for MNCs • • • Size of Firm Access to International Capital Markets International Diversification Exposure to Exchange Rate Risk Exposure to Country Risk

Chapter Review • Cost of Capital for MNCs … continued – Cost of Capital Comparison Using the CAPM – Implications of the CAPM for an MNC’s Risk

Chapter Review • Costs of Capital Across Countries – Country Differences in the Cost of Debt – Country Differences in the Cost of Equity – Combining the Costs of Debt and Equity • Using the Cost of Capital for Assessing Foreign Projects – Derive NPVs Based on the WACC – Adjust the WACC for the Risk Differential

Chapter Review • The MNC’s Capital Structure Decision – Influence of Corporate Characteristics – Influence of Country Characteristics • Interaction Between Subsidiary and Parent Financing Decisions – Impact of Increased Debt Financing by the Subsidiary – Impact of Reduced Debt Financing by the Subsidiary

Chapter Review • Using a Target Capital Structure on a Local versus Global Basis – Offsetting a Subsidiary’s Abnormal Degree of Financial Leverage – Limitations of Offsets – Differences in Financing Tendencies Among Countries • Impact of Capital Structure Decisions on an MNC’s Value

Part V Short-Term Asset and Liability Management Subsidiaries of MNC with Excess Funds Deposits Provision of Loans Eurobanks in Eurocurrency Market Deposits Purchase Securities Provision of Loans Purchase Securities MNC Parent Borrow Funds International Commercial Paper Market Borrow Funds Subsidiaries of MNC with Deficient Funds Borrow Funds

Financing International Trade

Chapter Objectives • To describe the methods of payment for international trade; • To explain common trade finance methods; and • To describe the major agencies that facilitate international trade with export insurance and/or loan programs.

Payment Methods for International Trade • In any international trade transaction, credit is provided by either – the supplier (exporter), – the buyer (importer), – one or more financial institutions, or – any combination of the above. • The form of credit whereby the supplier funds the entire trade cycle is known as supplier credit.

Payment Methods for International Trade Method : Prepayments • The goods will not be shipped until the buyer has paid the seller. • Time of payment : Before shipment • Goods available to buyers : After payment • Risk to exporter : None • Risk to importer : Relies completely on exporter to ship goods as ordered

Payment Methods for International Trade Method : Letters of credit (L/C) • These are issued by a bank on behalf of the importer promising to pay the exporter upon presentation of the shipping documents. • Time of payment : When shipment is made • Goods available to buyers : After payment • Risk to exporter : Very little or none • Risk to importer : Relies on exporter to ship goods as described in documents

Payment Methods for International Trade Method : Drafts (Bills of Exchange) • These are unconditional promises drawn by the exporter instructing the buyer to pay the face amount of the drafts. • Banks on both ends usually act as intermediaries in the processing of shipping documents and the collection of payment. In banking terminology, the transactions are known as documentary collections.

Payment Methods for International Trade Method : Drafts (Bills of Exchange) • Sight drafts (documents against payment) : When the shipment has been made, the draft is presented to the buyer for payment. • • Time of payment : On presentation of draft Goods available to buyers : After payment Risk to exporter : Disposal of unpaid goods Risk to importer : Relies on exporter to ship goods as described in documents

Payment Methods for International Trade Method : Drafts (Bills of Exchange) • Time drafts (documents against acceptance) : When the shipment has been made, the buyer accepts (signs) the presented draft. • • Time of payment : On maturity of draft Goods available to buyers : Before payment Risk to exporter : Relies on buyer to pay Risk to importer : Relies on exporter to ship goods as described in documents

Payment Methods for International Trade Method : Consignments • The exporter retains actual title to the goods that are shipped to the importer. • Time of payment : At time of sale to third party • Goods available to buyers : Before payment • Risk to exporter : Allows importer to sell inventory before paying exporter • Risk to importer : None

Payment Methods for International Trade Method : Open Accounts • The exporter ships the merchandise and expects the buyer to remit payment according to the agreed-upon terms. • Time of payment : As agreed upon • Goods available to buyers : Before payment • Risk to exporter : Relies completely on buyer to pay account as agreed upon • Risk to importer : None

Trade Finance Methods Accounts Receivable Financing – An exporter that needs funds immediately may obtain a bank loan that is secured by an assignment of the account receivable. Factoring (Cross-Border Factoring) – The accounts receivable are sold to a third party (the factor), that then assumes all the responsibilities and exposure associated with collecting from the buyer.

Trade Finance Methods Letters of Credit (L/C) – These are issued by a bank on behalf of the importer promising to pay the exporter upon presentation of the shipping documents. – The importer pays the issuing bank the amount of the L/C plus associated fees. – Commercial or import/export L/Cs are usually irrevocable.

Trade Finance Methods Letters of Credit (L/C) The required documents typically include a draft (sight or time), a commercial invoice, and a bill of lading (receipt for shipment). – Sometimes, the exporter may request that a local bank confirm (guarantee) the L/C. ¤

Sample Letter of Credit (Confirmation) Advice Number: BA 000000094 Amount: Issue Bank Ref: 1234/LMC/5678 US$: Beneficiary: ABC Company, Inc. Applicant: XYZ Company, Inc. 5278 S. Motorized Blvd 25 Rising Sun Way Tokyo, Japan 120 -113 000 -0000 +000 -0000 We have been requested to advise you of the following letter of credit issued by: Advice Date: Expire Date: April 17, 2002 21 March 2002 21 July 2002 Detroit, MI 48210 First Bank of Japan 123 Cherry Blossom Dr Tokyo, Japan Please be guided by its terms and conditions and by the following: Credit is available by negotiation of your draft(s) in duplicate at sight for 100% of invoice value drawn on us accompanied by the following documents: 1. Signed commercial invoice, one (1) original and three (3) copies. 2. Full set ocean bills of lading consigned to the order of First Bank of Japan, Japan notify applicant and marked freight collect. 3. Packing list, two (2) copies. Evidencing Shipment of: 20, 000 motorized tooth brushes FOB San Francisco Shipment From: Detroit, MI through San Francisco, CA Shipment To: Tokyo, Japan Partial Shipments not allowed. All banking charges outside Japan are for beneficiary's account. Documents must be presented within 21 days from BILL date. At the request of our correspondent, we confirm this credit and engage with you that all drafts drawn under and in compliance with the terms of this credit will be duly honored by us. Please examine this instrument carefully. If you are unable to comply with the terms or conditions, please communicate with your buyer to arrange for an amendment. Sincerely, Jill Moneybags Account Manager International Banking Group • Jack and Jill Bank Corp. • P. O. Box 1234 • Detroit, MI 48201

Documentary Credit Procedure Sale Contract Buyer (Importer) Seller (Exporter) Deliver Goods Request for Credit Documents & Claim for Payment Present Documents Importer’s Bank (Issuing Bank) Payment Send Credit Exporter’s Bank (Advising Bank) Deliver Letter of Credit

Trade Finance Methods Letters of Credit (L/C) – Variations include • standby L/Cs : funded only if the buyer does not pay the seller as agreed upon • transferable L/Cs : the first beneficiary can transfer all or part of the original L/C to a third party • assignments of proceeds under an L/C : the original beneficiary assigns the proceeds to the end supplier

Trade Finance Methods Banker’s Acceptance (BA) – This is a time draft that is drawn on and accepted by a bank (the importer’s bank). The accepting bank is obliged to pay the holder of the draft at maturity. – If the exporter does not want to wait for payment, it can request that the BA be sold in the money market. Trade financing is provided by the holder of the BA.

Trade Finance Methods Banker’s Acceptance (BA) ¤ The bank accepting the drafts charges an all-inrate (interest rate) that consists of the discount rate plus the acceptance commission. – In general, all-in-rates are lower than bank loan rates. They usually fall between the rates of short-term Treasury bills and commercial papers.

Life Cycle of a Typical Banker’s Acceptance 1. Purchase Order Importer Exporter 5. Ship Goods 2. Apply for L/C 10. Sign Promissory Note to Pay 11. Shipping Documents 14. Pay Face Value of BA Importer’s Bank 6. Shipping Documents & Time Draft 8. Pay Discounted Value of BA 3. L/C 7. Shipping Documents & Time Draft 12. BA 16. Pay Face Value of BA Money Market Investor 13. Pay Discounted Value of BA 15. Present BA at Maturity 4. L/C Notification 9. Pay Discounted Value of BA Exporter’s Bank 1 - 7 : Prior to BA 8 - 13 : When BA is created 14 - 16 : When BA matures

Trade Finance Methods Working Capital Financing – Banks may provide short-term loans that finance the working capital cycle, from the purchase of inventory until the eventual conversion to cash.

Trade Finance Methods Medium-Term Capital Goods Financing (Forfaiting) – The importer issues a promissory note to the exporter to pay for its imported capital goods over a period that generally ranges from three to seven years. – The exporter then sells the note, without recourse, to a bank (the forfaiting bank).

Trade Finance Methods Countertrade – These are foreign trade transactions in which the sale of goods to one country is linked to the purchase or exchange of goods from that same country. – Common countertrade types include barter, compensation (product buy-back), and counterpurchase. – The primary participants are governments and multinationals.

Agencies that Motivate International Trade • Due to the inherent risks of international trade, government institutions and the private sector offer various forms of export credit, export finance, and guarantee programs to reduce risk and stimulate foreign trade.

Agencies that Motivate International Trade Overseas Private Investment Corporation (OPIC) • OPIC is a U. S. government agency that assists U. S. investors by insuring their overseas investments against a broad range of political risks. • It also provides financing for overseas businesses through loans and loan guaranties.

Agencies that Motivate International Trade • Beyond insurance and financing, the U. S. has tax provisions that encourage international trade. • The FSC Repeal and Extraterritorial Income Exclusion Act of 2000, which replaced the 1984 Foreign Sales Corporation provisions in response to WTO concerns, excludes certain extraterritorial income from the definition of gross income for U. S. tax purposes.

Chapter Review • Payment Methods for International Trade – Prepayments – Letters of Credit – Sight Drafts and Time Drafts – Consignments – Open Accounts

Chapter Review • Trade Finance Methods – Accounts Receivable Financing – Factoring – Letters of Credit – Banker’s Acceptances – Working Capital Financing – Medium-Term Capital Goods Financing (Forfaiting) – Countertrade