Lecture 13 Bond Valuation and Interest Rate Investment

Lecture 13 Bond Valuation and Interest Rate Investment Analysis and Portfolio Management Spring 2009 CAU Business School

각종 이색채권 Income bond: coupon is paid only if the company’s income is sufficient. Convertible bond: can be swapped for a fixed number of shares of stocks anytime before the maturity at holder’s option. Put bond: allows holder to force the issuer to buy back the bond at a stated price. Exchange bond: 채권 발행 주체가 아닌 다른 기업의 주 식과 교환이 가능한 채권 재앙채권(catastrophe bond): 대규모 자연재해 발생 시 이자와 원금을 지급하지 않는 채권 – 일종의 보험상품

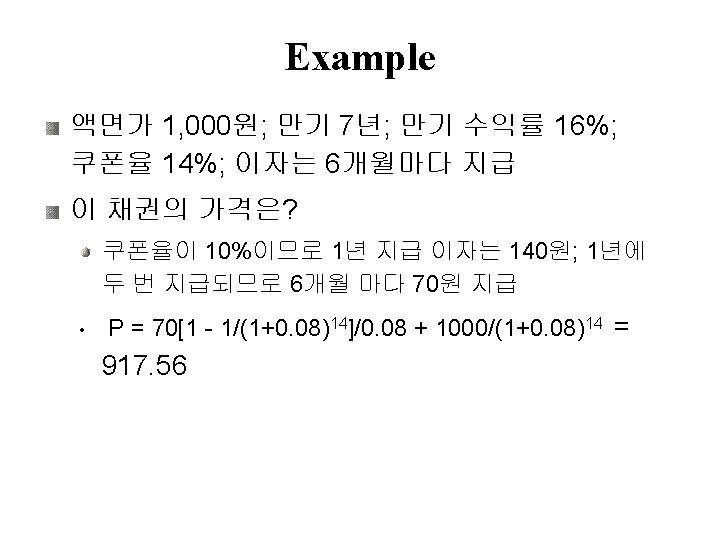

Example Consider a bond with a coupon rate of 10% and annual coupons. The par value is $1, 000 and the bond has 5 years to maturity. The yield to maturity is 11%. What is the value of the bond? P = 100[1 – 1/(1+0. 11)5] /0. 11 + 1, 000 / (1. 11)5 = 963. 04

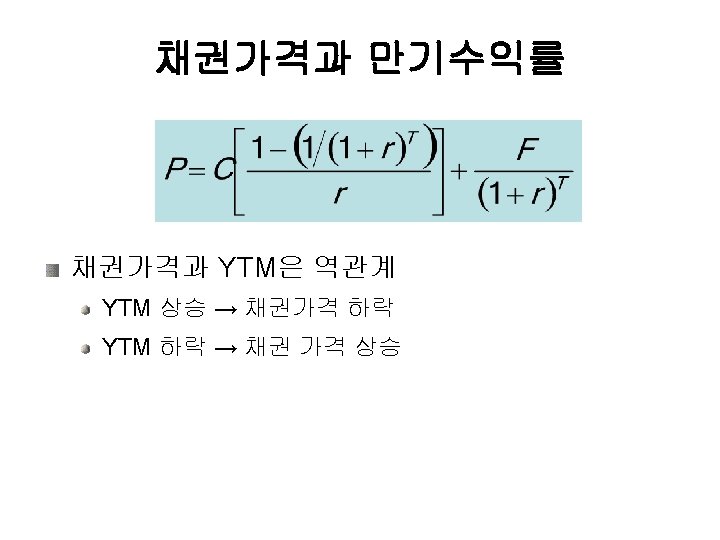

, P = F: par bond If YTM")

채권가격과 쿠폰율 If YTM = CR (쿠폰율), P = F: par bond If YTM > CR, P < F : discount bond If YTM < CR, P > F : premium bond

The Inverse Relationship Between Bond Prices and Yields

채권에서 발생할 미래 현금흐름의 현재가치를 채권의 현재 시장가격과 일치시키는")

각종 채권수익률 만기수익률(yield to maturity) 채권에서 발생할 미래 현금흐름의 현재가치를 채권의 현재 시장가격과 일치시키는 이자율(수익률) Current yield Annual coupon payment/current market price Holding period return HPR = [ I + ( P 0 - P 1 )] / P 0 where I = interest payment P 1 = price in one period P 0 = purchase price

- Slides: 27