Learning Objectives After studying this powerpoint you should

Learning Objectives After studying this powerpoint you should be able to: 1. 2. 3. 4. 5. 6. 7. 8. Explain the concept of leveraged investing Outline how gearing can be used to magnify returns Discuss the income tax consequences of gearing Discuss the capital gains tax consequences of gearing Explain how mortgages work Outline margin lending Explain the benefits and risks of margin lending Outline how derivatives can be used to create leverage.

Introduction • Leveraged investing is the buying of investment assets for the purpose of generating a return using borrowed funds. • Advantages are in the areas of taxation and capital gains. • Investors must have a strategy in place to manage the associated risks. • Leveraging can also refer to the use of derivatives (futures, options and warrants) to create an exposure to significant gains (or losses).

Leveraged investing • Leveraged investing is not new but has been used for many years in the form of mortgages, futures and options. • Today it is increasingly being used for wealth creation. • Leveraged investing generates greater returns than from savings alone.

Gearing • Gearing describes the use of borrowed money to buy investment assets and achieve a return greater than the cost of using the borrowed funds. Benefits of Gearing – Increase in value of leveraged asset – Service debt from existing income Risks of Gearing – ‘Servicing’ (repayment of interest and capital) of borrowed funds – Decline in asset value

Income taxes and geared investments • Dividend, interest or rental income is assessable for tax purposes • Interest expense on a loan for the purpose of investing in income producing assets will be a deductible expense • This will be the case whether the investment is positively or negatively geared

Income taxes and geared investments Table 8. 1 Kevin: no taxes, and returns > costs

Positive gearing • Positive gearing is the use of borrowed funds to purchase an income producing asset where the income is greater than the interest expense and other associated costs. • Not considered tax effective • Good retirement income strategy • Risk-minimisation strategy for investors particularly if seeking long-term capital gains

Negative gearing • Negative gearing occurs – where an investor buys an income producing asset using borrowed funds, and – the costs of owning the asset are higher than the income from the asset. • Popular because the ATO allows losses to be claimed against personal income • Most common types are investment in rental properties, a share portfolio or managed funds

Negative gearing example: • Kevin has assessable income of $20, 800 and allowable deductions of $21, 600 from an investment thus leaving an $800 loss • If we assume he is on the 30% marginal tax rate the he will have a tax shield of $240 to reduce his assessable income and reduce tax payable

Risks of negative gearing • Anticipated annual income is lower than expected • Anticipated expenses are higher than expected • If a lender changes the terms of a loan this may affect the benefits of negative gearing • A reduction to the investors other income could lower their marginal personal tax rate making the tax shield less attractive • The investor is forced to sell at the wrong time in the market cycle • Asset specific factors e. g. bad tenants • The asset does not generate the capital gains anticipated

Gearing ratio • Gearing ratio is used to measure amount of debt in relation to current market value of asset purchased with debt. Gearing ratio = Borrowed funds Investor’s contribution where Investors contribution = market value of asset – borrowed funds

Gearing ratio Table 8. 5 Kevin: gearing ratios

• Date of commencement of the CGT was 19 September")

Capital Gains Tax (CGT) • Date of commencement of the CGT was 19 September 1985 • Assets acquired after 19 September 1985 and before 21 September 1999 generally allow the taxpayer to select either the indexation method or the discount method • Assets acquired from 21 September 1999 generally require the taxpayer to select the discount method to apply to any capital gain • The limiting factor to the selection of the indexation method or the discount method is the requirement that the relevant asset is held for at least 12 months - where this does not apply, the taxable capital gain will be calculated without any application of either the indexation method or the discount method

CGT • Capital losses may only be claimed against capital gains – if there is no capital gain in the year that a capital loss is incurred, the loss may be carried forward • An advantage of shares is that only a part of a share portfolio may need to be sold thus limiting capital gains whereas real estate is a ‘lumpy’ investment

Mortgages • Mortgage – a contract between a lender and a borrower which pledges real estate as security for a loan • Most common types of mortgages: – Standard variable-rate loans (SLV) – Fixed-rate loans • Variations allowed with deregulation: – – Interest-only loans Equity release loans Reverse mortgages (Home Equity conversion loans) Second-mortgage loans

Margin lending • Margin lending – lending for investment where the loan is secured by the investment • Borrower must maintain a loan-to-value ratio (LVR) which is set at the beginning of the loan Loan-to-Value Ratio = (LVR) Debt Current market value of the investor’s contribution + Debt

Margin lending continued • Most lenders require investors to maintain a safety margin above the value of the loan Safety margin = 1 – Borrowing Security recognised by lender • A margin call will be triggered if the value of the security falls below the value required by the lender • Margin calls have to be satisfied within 24 hours (refer to illustrative example 8. 2)

Margin lending continued Table 8. 7 Selected LVRs for CBA margin lending as at 1 April 2013 • • Note: Portfolio LVR is applicable to stocks in a diversifi ed portfolio with 5 or more approved securities. Source: Comm. Sec 2013.

Margin lending continued BENEFITS RISKS • Greater access to wealth-creating assets • Diversification • Liquidity • Personal income tax benefits • Direct investing and management • Capital losses • Funding interest payments • Funding margin calls • Fluctuating value of the portfolio

Derivatives • Derivative – a financial product whose value or price is derived from some other asset • Derivatives include: – Contracts for difference – Futures – Options – warrants

• An agreement between a buyer and a seller to")

Contracts for Difference (CFD) • An agreement between a buyer and a seller to exchange the difference in value of an underlying asset • The buyer is going long and expects the price of the underlying asset to rise • The seller is going short and expects the price of the underlying asset to fall • ASX or over the counter (OTC) CFDs • Can also be used to hedge a physical position

Futures contracts • A futures contract is an agreement to trade an asset in the future: – Either to buy or sell – A specific amount of a specific asset • Deposits are exchanged at beginning of contract to ensure parties will honour their obligations • Future price needs to be greater than current price

Futures contracts continued • Popular in global financial markets because an established futures contract makes it easy for traders and investors to buy and sell the contract • This ability to find buyers and sellers easily is known as ‘liquidity’ • Traded on registered futures exchanges • Investors make profits when they buy futures at a lower price than they sell it

Futures contracts continued Example Date 4 Jan Trade Investment Buy 1 gold contract with a speculation of 1000 oz. Settlement date: 15 March Purchase price: $520 per ounce Value of contract: $520 000 Deposit: 10% of market value – $52 000 10 Mar Gold price increases to $536 per ounce Value of contract: $536 000 Sell futures contract at $536 & lock in profit of: $536 000 – $520 000 = $16 000 + $16 000 Deposit returned + $52 000

Futures contracts continued Realised return • Capital used: At beginning Add profit At end $52 000 $16 000 $68 000 r = $68 000 – $52 000 x 100 $52 000 = 30. 77%

Futures contracts continued • Other issues to consider in relation to futures contracts are – Margins and deposits – The futures exchanges – The clearing house of futures exchanges – Novation

Futures contracts continued BENEFITS RISKS • Liquidity • Credit security • Flexibility • Funding of margin calls • Market volatility • No income stream • Knowledge risk

Options • An option is a security that gives the holder the right but not the obligation to buy or sell something in the future at a fixed price • Buyer of option has no obligation to buy/sell if market price is below the option price • Seller has an obligation to complete the transaction • Two types of options – Put options – Call options

Options continued Rights of option buyers and sellers Type of Option Buyers’ Rights Sellers’ Obligations Call options Choice of buying underlying security or asset Must sell underlying security or asset if option exercised Put options Choice of selling underlying security or asset Must buy underlying security or asset if option exercised

Options continued • Brokers work out the amount to charge for the premium of an option on a financial asset based on: risk, liquidity, time to maturity, volatility, etc. • Options markets are traded worldwide in one of two ways: – On a registered exchange such as the ASX or, – Directly between two parties in an over-thecounter (OTC) transaction

Options continued Pay-off profiles for the buyer and seller of a call option

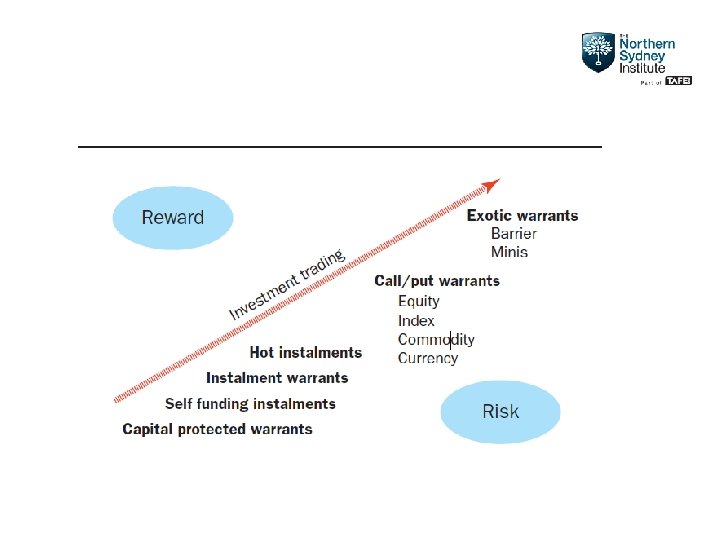

Warrants and other complex leveraged investments • Warrants are leveraged investments in the shares of a company. – Traded on the ASX – Issued in a series • Endowment and instalment warrants are not issued by the company in which the shares are being bought, but by a third party institution

Warrants and other complex leveraged investments continued • The holder of a warrant has the right to buy or sell the underlying asset so an investor would seek to be long if they expect prices to rise or short if they expect prices to fall • Warrants can be broadly categorised as: – Trading style (higher risk / return attributes) or – Investment style (lower risk / return attributes) and includes endowment and instalment warrants which are effectively a long term loan to buy shares

Summary • Leveraged investing is an effective use of small amounts of investment capital to magnify returns • It refers to either the use of borrowed funds or the use of derivatives • Leveraging is increasingly common in a personal investment portfolio.

Summary continued • Leveraging is reliant on expected returns, ability to service debt and tax advantages. • Leveraged investments come with a number of investment risks.

- Slides: 36