International Tax Research James R Hines Jr University

- Slides: 18

International Tax Research James R. Hines Jr. University of Michigan International Tax Policy Forum February 11, 2014

Exciting tax questions, exciting research answers: • What effects do mergers and acquisitions have on tax management by acquired firms? What can we tell from their reported tax rates? • Does taxation really discourage international acquisitions, and if so, then by how much?

Who knew that tax avoidance could drive? • Paper: “Tax avoidance as a driver of mergers and acquisitions, ” by Thomas Belz (Mannheim University), Leslie Robinson (Dartmouth), Martin Ruf (Tubingen University) and Christian Steffens (Mannheim University). • Working Paper, Dartmouth College Tuck School of Business, December 2013. • The paper looks at the effect of international M&A on (measured) tax rates of European target firms between 19962009. • The paper reports that mergers or acquisitions are associated with significant declines in (book definition) tax rates for acquirees, despite no pronounced change in acquiree leverage.

Data. • The paper starts with the Zephyr data on acquisitions of European firms from 1996 -2009. • It then matches these acquisitions to the Amadeus unconsolidated accounting data on European firms, dropping acquirees that are not corporations. • Keeps only those targets for which there accounting data three years before and one year after the merger, which leaves 1, 440 successful targets. Drop those with losses: leaves 1, 078. • Of the 1, 078, only 832 report complete income information, and only 529 (221 domestic; 308 international) provide 3 -year averages of effective tax rates before and after acquisition. • They then add all Amadeus firms for which there are 5 consecutive years of data, deleting all firms with tax losses, which adds 1. 97 million observations. • There is a whole lot of data selection going on.

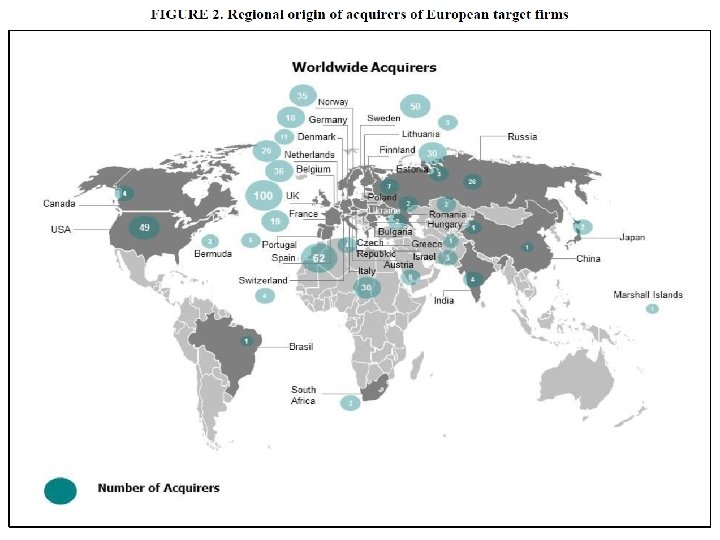

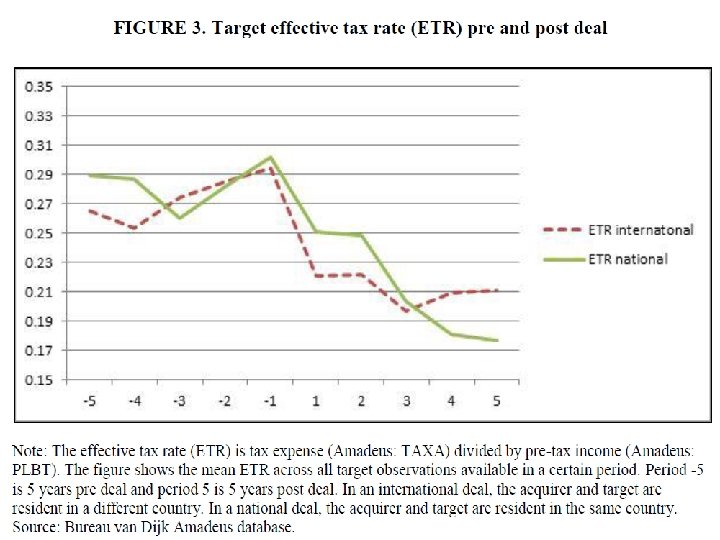

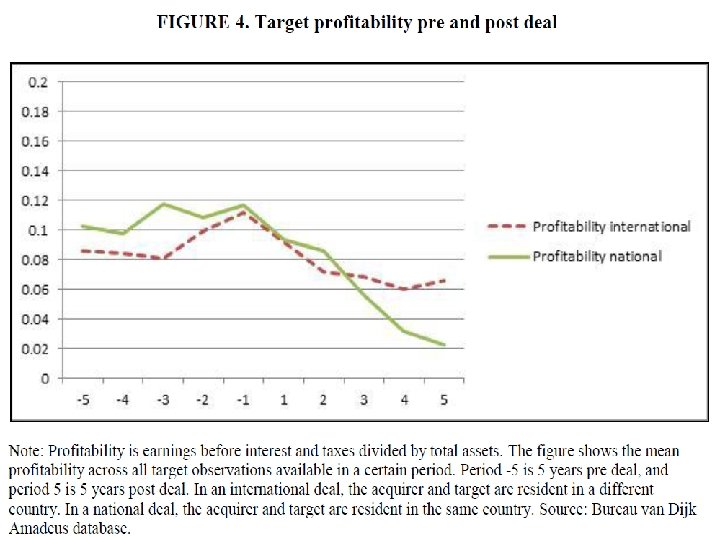

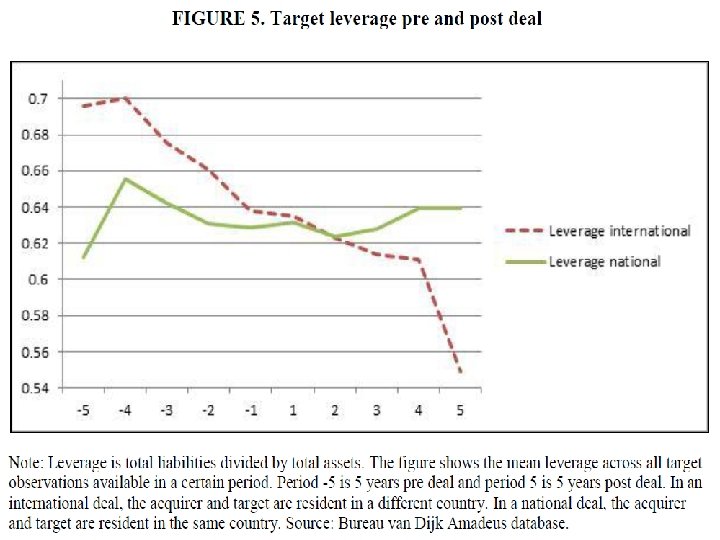

Patterns in the data. • The UK is the biggest acquirer of the European firms in the paper’s sample of firms. • The average profitability of target firms (measured as EBIT/Assets) declines after acquisition. • The average measured effective tax rate of target firms (measured as Tax Expense/Pretax Book Income) declines after acquisition. • There is no apparent effect of domestic acquisitions on average leverage (measured as Total Liabilities/Total Assets). International acquisitions appear to be associated with declines in target leverage.

Statistical evidence. • In order to estimate the extent to which acquisitions per se are associated with greater tax aggressiveness, it is necessary to know what would have happened in the absence of an acquisition. • This is hard. • One can compare effective tax rates of acquirees, before and after acquisition, to potential targets that were not acquired, but in order for this comparison to offer meaningful information, it must be that: ▫ There is nothing importantly different about the sample of acquirees compared to non-acquired firms, from the standpoint of contemporaneous changes in effective tax rates; and ▫ The acquisition must not itself directly affect measured tax rates. • The paper assumes that the second is true, and tries to address the first using propensity score matching (a statistical technique that attempts to identify comparable observations).

Regression results. • Domestic takeover targets have about 4 percent lower effective tax rates in the 3 years following acquisition than do otherwise-similar firms that are not targets. • International takeover targets have 5 percent lower effective tax rates than otherwise-similar non-targets. • Targets acquired by “tax-aggressive acquirers” (those whose effective tax rates are below their country medians) have 8 -10 percent lower effective tax rates than do non-targets; there appears to be little difference for targets acquired by “tax-non-aggressive acquirers. ” • There appears to be very little effect of acquisition on profitability or leverage (though the paper offers some thin evidence on the impact of group taxation regimes), including profitability changes that one might expect if firms reallocated taxable income.

Interpretation. • Does it follow from this evidence that tax rates fall on acquisition due to the tax aggressiveness of acquirers? • There are many interpretive issues here. • The first is the direct effect of acquisition on tax rates. • The second is the difficulty of forming a valid comparison group of companies. • The third is what impact measure the study should consider. Note that the study looks at target tax rates post acquisition, not the change in tax rate upon acquisition. • And the fourth is the reasonableness of the result. If the results are true, does it follow that any firm can have its tax rate reduced via acquisition? And if not – if it works only in certain cases – then in what sense is the evidence statistically valid?

More international acquisitions. • Paper: “Multiple taxes and alternative forms of FDI: Evidence from cross-border acquisitions, ” by Steve Mc. Corriston (University of Exeter), Christos Kotsogiannisz (University of Exeter), and Nils Herger (Study Center Gerzensee). • Oxford Centre for Business Taxation working paper No. 14/01, January 2014. • The paper looks at the effect of taxation on the extent of crossborder acquisition activity. • This is an old topic, and a good one. • What the paper offers is that it analyzes a much larger data set of cross-border acquisitions than do previous studies, with correspondingly greater statistical power in the estimates. • And guess what? Taxes have big effects on cross-border M&A.

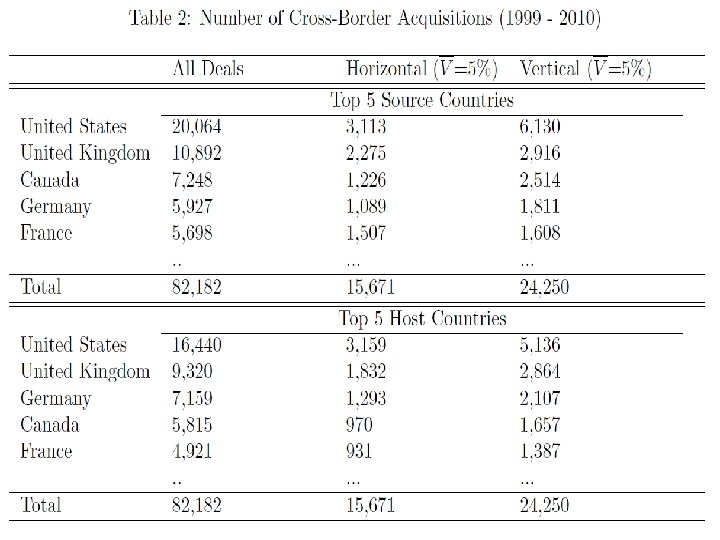

Data used in the study. • The study analyzes SDC Platinum data from Thomson Reuters, which reports information on international acquisitions. • The study considers all acquisitions in 32 high-income countries from 1999 -2010, resulting in 82, 182 observations, more than 90 percent of the world’s crossborder acquisitions during this period. • The study distinguishes horizontal acquisitions, in which the target and the acquirer are in the same industry, from vertical acquisitions, in which they are not (with some adjustments for the extent to which industries use each others’ outputs).

Statistical method and findings. • The study treats every cross-border acquisition equally, and simply adds them by country pair. • Consequently, there are 11, 248 observations, reflecting numbers of acquisitions of targets in country j by firms in country i in year t, for 32 source and 31 host countries, and 12 years (with a few missing observations). • The regressions include country variables that one would expect, such as GDP, distance, Euro Zone membership, trade barriers, labor market variables, etc. • Higher domestic statutory corporate taxation is negatively associated with acquisitions: doubling the corporate tax rate is associated with a 20 percent reduction in acquisitions. • Notably, one gets effects of similar size for domestic sales taxes, which likewise discourage acquisitions.

Effects of international taxation. • The study separately identifies international components of tax burdens associated with acquisitions (withholding taxes and homecountry income taxes. • Greater international taxes are associated with reduced numbers of acquisitions, even after controlling for domestic statutory corporate tax rates. The international taxes have large effects, roughly similar to those of domestic taxes. • Breaking the international tax burden into its components, both withholding taxes and parent company income taxes are associated with reduced cross-border acquisitions. Withholding taxes are estimated to have twice the impact of repatriation taxes. • Results appear to differ for both horizontal and vertical acquisitions, with vertical acquisitions generally responding more strongly to corporate and international tax rates, though sales taxes do not appear to influence vertical acquisitions (which could reflect the impact of company-to-company sales).

Interpretation. • The study looks only at numbers of acquisitions, not character or type, and therefore misses important nuance. Furthermore, it does not focus on the really big deals, which drive the FDI statistics. • That said, the study is quite comprehensive in its treatment of foreign acquisitions, which is really valuable. • The statistical methods are pretty clean, so we are left to interpret the evidence. As usual, one does not know what would have happened in the absence of tax differences. But this is intriguing information.