INTERNATIONAL ACCOUNTING QUESTIONS QUESTION 1 DISCUSS ABOUT THE

INTERNATIONAL ACCOUNTING QUESTIONS

QUESTION 1: DISCUSS ABOUT THE ENVIRONMENTAL AND SOCIAL RESPONSIBILITY ACCOUNTING BY AN INTERNATIONAL BUSINESS ORGANISATION?

INTRODUCTION OF SOCIAL ACCOUNTING Business activity in our country greatly affects the economy of that country-higher the degree of the business activity in an economy higher the degree of the development in that economy as business activity and development are directly related to each other. Social accounting is concerned with the study and analysis of accounting practice of those activities of an organization. Social responsibility accounting is a branch of accounting dealing with the functioning of economic system as a whole. It may be considered as the accounting for community. Social responsibility accounting includes the area like ‘pollution control’, ‘equal employment opportunity’, ‘charitable-contributions’, ‘community relations’, ‘product-quality’, ‘plantsafety’, ‘employee benefits’, and responsiveness to ‘consumer complaints’. The concept of socialistic pattern of society, civil rights movements, environmental protection and ecological conservation groups, increasing awareness of society towards corporate social contribution, etc. Have contributed towards the growing importance of Social accounting.

• The term social responsibility accounting is generally confused with number of terms as social audit, social information system, social reporting, socioeconomic accounting, social accounting social disclosure, corporate social performance, etc. , but all these terms have the same meaning and these terms are used interchangeably for one another. • As far as meaning of social responsibility accounting concerned, it is an accounting report of social activities performed by business units for the welfare of society. Definitions of Social Accounting: “The measurement and reporting, internal and external, of information concerning the impact of an entity and its activities on society. ” —Ralph Estes He viewed that social accounting as an independent discipline which is to measure and report the activities of an entity in so far as they effect the society.

Features of Social Accounting: Social accounting is an expression of a company’s social responsibilities. (ii) Social accounting is related to the use of social resources. (iii) Social accounting emphasize on relationship between firm and society. (iv) Social accounting determines desirability of the firm in society. (v) Social accounting is application of accounting on social sciences. (vi) Social accounting emphasizes on social costs as well as social benefits. (i)

A firm fulfills its social obligations and informs its")

Need/Benefits of Social Accounting: (1) A firm fulfills its social obligations and informs its members, the government and the general public to enables everybody to form correct opinion. (2) It counters the adverse publicity or criticism leveled by hostile media and voluntary social organizations. (3) It assists management in formulating appropriate policies and programmes. (4) Through social accounting the firm proves that it is not socially unethical in view of moral cultures and environmental degradation. (5) It acts as an evidence of social commitment. (6) It improves employee motivation. (7) Social accounting is necessary from the view point of public interest groups, social organizations investors and government. (8) It improves the image of the firm. (9) Through social accounting, the management gets feedback on its policies aimed at the welfare of the society. (10) It helps in marketing through greater customer support. (11) It improves the confidence of shareholders of the firm.

Social Accounting Approaches: 1. Classical Approach 2. Descriptive Approach 3. Integral Welfare Theoretical Approach 4. Programme Management Approach 5. Pictorial Approach 6. Foot Note Disclosures

Models of Social Accounting and Reporting 1. Reporting Seidler’s Model He has suggested reporting formats as under:

Seidler suggested two separate formats for social corporate reporting")

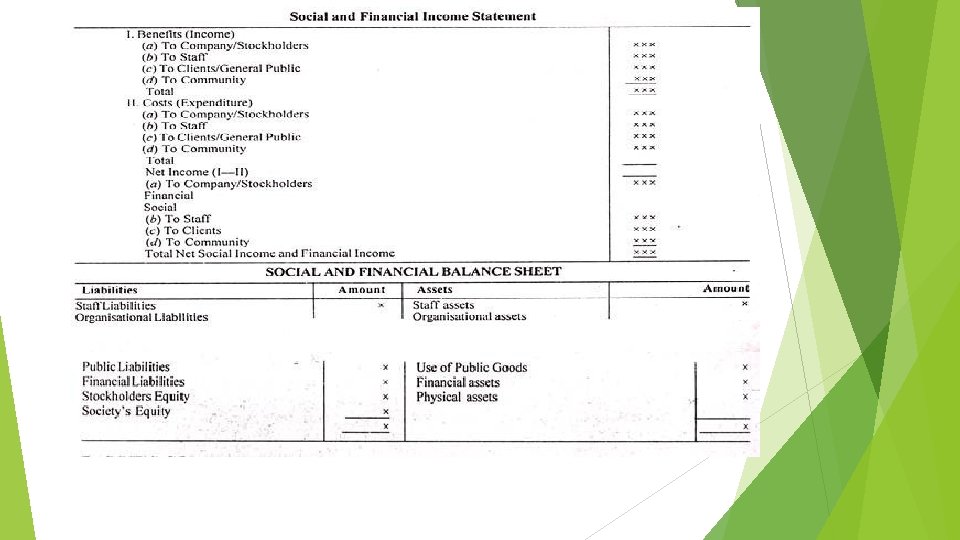

Features of Seidler’s Model: (i) Seidler suggested two separate formats for social corporate reporting by having a distinction between profit and nonprofit organization. (ii) Both formats are comprehensive. (iii) Both formats are flexible enough to accommodate changing social goals. 2. Abt’s Model: This model was developed by Abt associates in United States of America. Under this model social information is presented in a quantitative form through social statements. It consists of two parts. (1) Social Income Statement (2) Social Balance Sheet

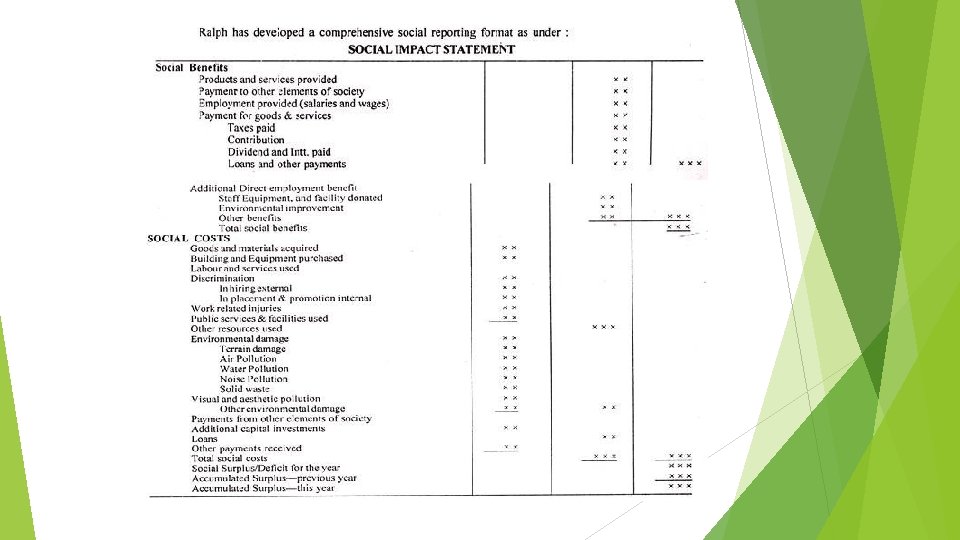

3. Ralph’s Comprehensive Social Benefit Cost Model: Ralph. W. Estes has proposed a comprehensive model and reporting format for social corporate reporting in his book “corporate social accounting” in 1976 at New York USA, Ralph’s Model is based on two items. Social benefits and social costs. Social Benefits: Ralph was of the view while having interaction with society; any corporate unit may provide any benefit to society economic or non-economic, Internal or External. Social Costs: Social costs in Ralph’s view were any cost, sacrifice whether economic or non-economic made by society and is not paid for are included in social cost for example damages to Air, soil and water due to disposal of waste by any business entity and if entity is making any payment for reduction of Air, soil and water pollution, can be shown as social benefits. Ralph has proposed this accounting model by keeping in view the reporting viewpoints of corporate unit as well as society as a whole. Ralph has tried to present his views through following diagram:

Questions 2 How can a multinational company manage a control system through accounting mechanism? Discuss.

INTRODUCTION Management accounting and control Management accounting refers to the processes and techniques that focus on the effective and efficient use of organizational resources, to support managers in their tasks of enhancing both customer value and shareholder value. Control is the process of setting standards, monitoring performance and identifying and correcting deviations from standards so that the organizational objectives are met. In the case of MNCs, which have diverse businesses across countries, the parent company (principal) needs to control the operations of the subsidiary companies (agent) to ensure that overall organizational objectives are met. Even though management control includes a wide spectrum of mechanisms and practices besides accounting, management accounting constitutes an integral part of management control systems. Therefore , accounting describes operations making performance visible and accordingly controllable

Management accounting and control in a multinational context According to Accounting standards II (revised ) A foreign operation is conducted “ When activities are based or conducted in a country other than the country of the reporting enterprise, which are carried out through a subsidiary associate, joint venture or branch, then such activities are called foreign operation. ” Foreign operations are classified into Ø Integral foreign operation Ø Non integral foreign operation Accountants and managers in a multinational and international context face a host of complexities, because of the environmental uncertainties, international capital flows and complex organizational structures. According to Emmanuel et al. (1998), important issues for multinational management accounting are, for example, performance evaluation and control, currency changes, inflation accounting and corporate governance. Performance evaluation and control may be problematic because of the distance between headquarters and local units.

Factors affecting performance evaluation of foreign operations Legal framework Economic conditions Socio cultural values Political factors Technological advancement Capital markets Production factors

CAPITAL MARKETS The availability of capital is another important factor that invitees MNCs to a foreign country. Some countries, especially the developed ones are capital abundant while there may be a paucity of capital in the less developed nations. Efficiency of capital market will vary with countries and an MNC will find itself more comfortable in capital abundant economics. The availability of equity, debt and institutional credit is conducive to the growth of foreign operations but it has accompanying problems like currency conversion, exchange rate risk and transaction exposure i. e. the time gap between a transaction and payment. PRODUCTION FACTORS In addition to entrepreneurship, the major factors of production are materials, labour and capital. Each nation by virtue of its geographic or demographic situation may abound in material or labour which will affect the cost of production or conversion of raw materials into goods. On account of a world economy emerging as a result of rapid globalization, an increase in demand will ultimately lead to a depletion of material inputs and also a labour shortage. Production inputs if abundant help in reducing costs while shortage leads to a cost up thrust since the materials have to imported and transported from outside involving additional costs and also exchange rate issues.

INFLATION q Global phenomenon q Expresses rise in prices of inputs q It occurs worldwide and varies from one country to another q In context of foreign operations, it affects the balance sheet and income statement q The inflationary impact could lead to unreal profits resulting from matching old costs with new revenues , leading to erosion of capital by way of increased rate of dividends after a higher tax liability.

Measures for Performance Evaluation Issued by MNCs include : Share in the Market Host country cordiality Quality control and conformity Productivity Contribution to environment Employees training and growing Manpower safety and welfare Labour or employeer turnover Social responsibility Research and development

QUESTION 3 What are the objectives of International Financial Reporting Standards? Explain the progress of International Financial Reporting Standards?

is a set of accounting standards developed by")

INTRODUCTION ØInternational Financial Reporting Standards (IFRS) is a set of accounting standards developed by an independent, not-for-profit organization called the International Accounting Standards Board (IASB). ØThe goal of IFRS is to provide a global framework for how public companies prepare and disclose their financial statements. IFRS provides general guidance for the preparation of financial statements, rather than setting rules for industry-specific reporting. ØHaving an international standard is especially important for large companies that have subsidiaries in different countries. Adopting a single set of world-wide standards will simplify accounting procedures by allowing a company to use one reporting language throughout. A single standard will also provide investors and auditors with a cohesive view of finances. ØIFRS is sometimes confused with IAS (International Accounting Standards), which are older standards that IFRS has replaced.

HISTORY The history of IFRS can be traced back to 1973 when representatives of the professional accounting bodies from major developed economies-Australia, Canada, France, Germany, Japan, Mexico, the Netherlands, the United Kingdom, Ireland the US-reached an agreement to establish the International Accounting Standards Committee (IASC) with no statutory mandates given by political jurisdictions. In 1975, the IASC pronounced its first International Accounting Standard (IAS). Since then the IASC issued a total of 41 IAS until it was restructured into the International Accounting Standard Board (IASB) in 2001. The IASB has pronounced a total of eight International Financial Reporting Standards (IFRS) as on 2006.

ADVANTAGES FOCUS ON INVESTORS LOSS RECOGNITION TIMELINESS COMPARABILITY STANDARDIZATION OF ACCOUNTING AND FINANCIAL REPORTING IMPROVED CONSISTENCY AND TRANSPARENCY OF FINANCIAL REPORTING BETTER ACCESS TO FOREIGN CAPITAL MARKETS AND INVESTMENTS benefits from adaptation of IFRS over the world to include: better financial information for shareholders and regulators, enhanced comparability, improved transparency of results, increased ability to secure cross-border listing, better management of global operations and decreased cost of capital.

DISADVANTAGES The most noteworthy disadvantage of IFRS relate to the costs related to the application by multinational companies which comprise of changing the internal systems to make it compatible with the new reporting standards, training costs and etc. Another major disadvantage of converting to IFRS makes the IASB the monopolist in terms of setting the standards. And this will be strengthened if IFRS is adopted by the US companies. And if there is competition, such IFRS vs. GAAP, there is more chance of having reliable and useful information that will be produced during the course of competition.

And another disadvantage of IFRS is that IFRS is quite complex and costly, and if the adoption of IFRS needed or required by small and medium sized businesses, it will be a big disadvantage for SMEs as they will be hit by the large transition costs and the level of complexity of IFRS may not be absorbed by SMEs. The issue of regulating IFRS in all countries, as it will not be possible due to various reasons beyond IASB or IASC control as they cannot enforce the application of IFRS by all countries of the world.

OBJECTIVES OF IFRS to develop, in the public interest, a single set of high quality, understandable and enforceable global accounting standards that require high quality, transparent and comparable information in financial statements and other financial reporting to help participants in the world's capital markets and other users make economic decisions; to promote the use and rigorous application of those standards; in fulfilling the objectives associated with (1) and (2), to take account of, as appropriate, the special needs of small and medium-sized entities and emerging economies. to bring about convergence of national accounting standards and International Accounting standards and IFRS to high quality solutions.

IFRS brings transparency by enhancing the international comparability and quality of financial information, enabling investors and other market participants to make informed economic decisions. IFRS strengthens accountability by reducing the information gap between the providers of capital and the people to whom they have entrusted their money. IFRS contributes to economic efficiency by helping investors to identify opportunities and risks across the world, thus improving capital allocation.

Year 1967 1973 2001 Event Accountants’ International Study Group formed, containing The Institute of Chartered Accountants of England Wales, the Canadian Institute of Chartered Accountants and the American Institute of Certified Public Accountants. The International Accounting Standards Committee (IASC) is formed. The IASB replaces the IASC. The IASB offers improved governance over its standard-setting processes.

EU agrees to adopt IFRS from 2005, IASB + FASB agree on joint program for convergence. Australia, NZ, Hong Kong & South Africa agree to adopt IFRS from 2005. Japan agrees to convergence 2005 25 countries, almost 7, 000 companies simultaneously switch to IFRS. 2006 China agrees to convergence program. IASB + FASB agree to fast 2002 2003 2004 track convergence.

2007 100+ 2009 G 20 2012 2014 countries now require or permit IFRS for reporting. supports IASB adoption. The IASB Monitoring Board established. Russia IASB commences use of IFRS + FASB release converged Standard on revenue recognition.

Questions 4 what do you mean by harmonization of accounting practices ? what are the obstacles in the process of harmonization of accounting practices?

INTRODUCTION Globalization has led to large companies looking to increase their sales and growth opportunities beyond national markets. To attract equity and debt financing to achieve these goals, many of these companies are looking to be listed on different stock exchanges. Additionally, investors are expanding their portfolios beyond national borders as global markets have created greater opportunities for investing. As a result, the differences in the reporting practices of such companies is now of great importance as this has led to difficulties for those who prepare, consolidate, audit and interpret financial statements. A great deal of diversity exist in the accounting practices adopted in different countries. To allow the gains from the global economy to be fully realized, it is argued that accounting policy should be standardized among nations.

MEANING Harmonization is a process of increasing the compatibility of accounting practices by setting bounds to their degree of variation. Essentially, harmonization allows countries to use different standards so long as they are not in conflict. In a simplest way it means not only bringing out uniformity by reducing alternatives and differences in procedure by setting bounds, but embraces a blending and combining the elements of accounting practices of various countries into an orderly structure. The aim of accounting harmonization is to make the financial statements of companies comparable with the financial statements of companies in other countries. Accounting harmonization is important because companies want to operate in a business environment in which they can trade, raise capital, list their securities and attract investors in different countries.

NEED FOR HARMONISATION Harmonization ensures high quality financial reporting. Harmonization disclosures. Harmonization enables a systematic reviews along with evaluation of performance of a multinational corporate unit having subsidiaries in various countries where in each country has its own set of GAAP. Harmonization makes the comparison of the corporate unit against the domestic and international peers more easier. Harmonization provides a level of playing ground where no country is advantaged or disadvantaged by its GAAP. Harmonization also leads to internationalization accounting professionals. ensures a reliable financial reporting and

BARRIERS OF HARMONIZATION 1. Spirit of Nationalism: - Spirit of nationalism among accounting professionals in different countries sometimes creates hurdles in accepting compromises which they have to make in changing their accounting practices. National pride prevents them from accepting willingly the idea that his accounting principles are inferior to those of another country, Even though the accountant may be a strong proponent of harmonization. 2. Different Legal Environments: - Legal or statutory environment plays a dominant role in the development of accounting thought in every country. Legal systems differ from one country to the other. Since the legal system in a country exercises a strong influence over the accounting and reporting practices, it is clear that unless and until uniformity in laws is possible, it will be difficult to achieve the goal of harmonisation of divergent accounting practices.

3. Varying Objectives of Financial Reporting: - The purposes of financial reporting differ from country to country. That can be the possible cause of variation in reporting practices also. Financial reporting in every country is done by keeping in mind the targeted audiences. For example in North America target audiences are the investors and creditors where as in European countries like France and Germany, accounting is performed for revenue and government agencies. 4. Lack of Strong Professional Accounting Institutes: - IASC at global level is playing a dominant role for development of IAS’s. This committee operates through national professional institutes for example ICAI, ICWAI are the members of IASC. In countries, where professional institutes are not strong enough to get the standards implemented in their respective countries it will be a difficult task to bring harmonisation in divergent accounting practices. 5. Economic Gap between Developed and Developing Nations: - There is a wide economic gap between developed and developing nations. This gap is a hurdle in bringing out harmonisation in divergent accounting practices. It will be better to understand interaction between economic and accounting system.

QUESTION-5 What do you mean internationalization of capital markets? What are the major reasons responsible for internationalization of capital markets?

CAPITAL MARKET

A capital markets is a market comprising INDIVIDUALS CORPORATE INSTITUTIONS GOVERNMENT that invest or borrow in the form of stocks (owner’s equity) or bonds (debt). q These markets channel the wealth of savers to those who can put it to long term productive use, such as companies or governments making long-term investments. q Financial regulations, such as the UK’s Bank of England (BOE) or the U. S. Securities and Exchange Commission (SEC), oversee the capital markets in their jurisdictions to protect investors against fraud among other duties.

Features of capital markets Link between savers and investment opportunities Deals in long term investments Utilizes intermediaries Determination of capital formation Government rules and regulations

STRUCTURE OF MARKETS Primary Market Refers to the first hand issue or the fresh issue (IPO) of shares and bonds by corporation or the government. Secondary Market Deals in pre-issued securities (EXISTING) and most of the capital market transactions take place here.

INTERNATIONALIZATION OF CAPITAL MARKET q q The expansion of the capital market and its activity beyond political boundaries. It is done through the establishment of economic units in foreign countries by national companies resulting in development of a network between the capitals of different countries.

Objectives of internationalization Economic link between capitalist countries q Expansion of international division of labour and q Globalization of production q

SOURCES OF CAPITAL IN INTERNATIONAL CAPITAL MARKET PUBLIC SOURCES PRIVATE SOURCES

PUBLIC SOURCES q It consists of the official development assistance, comprising grants and multilateral and bilateral loans. q The world bank offers number of loans which are nonconcessional. q Such loans are also provided by intergovernmental agencies and regional development bank agencies. q loans from government, central bank and such agencies refers to bilateral aid. q ODA or Official Development Assistance is a major source of finance.

Private sources q To non-government investment by individuals and companies by way of foreign direct investment and portfolio investment. q Portfolio investment refers to the investment in equity (stocks) or debt (bonds). q The foreign direct investment is the money invested by companies in business ventures outside their home country.

Reasons for internationalization of capital market q Increase sales q Improve profits q Short-term security q Long-term security q Increase innovation q Exclusivity q Economies of scale q Education q Competitive Strike q Government incentives

QUESTION-6 What are the objectives of performance evaluation? Explain the methods you would follow for the evaluation of the performance of foreign operations

Performance evaluation It is the process of determining the success of any activity business or non business. Evaluation is the part of the control system which has to be done in order to ensure that the desired results are achieved or otherwise the deficit or deficiency in performance indicated by under achieved targets is removed.

Evaluating efficiency is central to an effective manage technique. A effectively designed efficiency evaluation system permits best management to q Assure managerial behavior is constant with strategic priorities. q Judge the profitability of current operations. q Spot places which have been not performing as planned. q Allocate limited corporate resources productively. q Evaluate managerial efficiency.

A foreign operation is conducted “when activities")

Foreign operations According to accounting standard 2(revised) A foreign operation is conducted “when activities are based or conducted in a country other than the county of the reporting enterprise, which are carried out through a subsidiary associate, joint venture or branch, then such activities are called foreign operation. ”

Types of foreign operations Foreign operations can be divided as follow: q Integral Foreign Operations: It is a foreign operation, the activities of which are an integral part of the reporting enterprise. q Non Integral Foreign Operations: Non integral foreign operations accumulates cash and other monetary items, incurs expenses generates income and arranges borrowing in local currency.

According to HOWANG PERMUTE, foreign operations can be classified as follows: Ethnocentric: These are home country oriented operations which means they are dominated by the parent companies and its operations are controlled by the parent companies. Polycentric: These are host county oriented operations which are adaptive to local situations due to difference in circumstances between home and host country. Geocentric: These are world oriented which takes into considerations circumstances both at local and global level.

Factors affecting performance evaluation The factors which effects the performance evaluation due unique business environment of different countries or host country are as follows: Legal Framework Economic Conditions Socio-economic Values Political Climate Technological Advancement

Methods of performance evaluation The evaluation criterion used by MNCs can be classified as: Financial Non Measures Financial Measures

Financial measures Return on Investment Return on Assets Comparison Between Actual and Budgeted Profits Cash Flows Profit on Sales

Non- financial measures Share In The Market Host Country Cordiality Quality Control and Conformity Productivity Contribution To Environment Employee Training And Growing Manpower Safety And Welfare Labour And Employee Turnover Social Responsibly Research And Development

QUESTION-7 What is the reporting currency in the area of international accounting? As an accountant in an MNC how will you manage the transaction exposure arising due to foreign currency denomination? Explain by using forward market hedge or money market hedge.

REPORTING CURRENCY DEFINITION of 'Reporting Currency' The currency which is used for an entity's financial statements. The reporting currency in financial statements and other financial reports are easiest to understand when they are compiled using only one currency. However, many large companies have operations in many different countries. This often requires doing business with a variety of currencies. To standardize this process, there a variety of accounting regulations which prescribe a uniform methodology for carrying out this conversion. This helps to maximize the transparency with which these financial reports are presented.

INTRODUCTION Exchange rate risks arise because of international businesses being done in an environment where no uniform acceptable currency is there. In result, operations are generally denominated in currencies other than the domestic one. There are fluctuations in every currency relationship. Management of such risk involved is the most difficult job for a corporate manager.

Exchange rates cannot be forecasted perfectly but the corporate managers at least can measure the exposure to exchange rate fluctuations. Various forms of exposures are: q. Transaction exposure q. Economic exposure q. Translation exposure

TRANSACTION EXPOSURE This exposure is also known as conversion exposure. The degree to which the value of future cash transactions can be affected by exchange rate fluctuations is known as transaction exposure. It is also known as exposure of risk associated with settlement of transactions denominated in foreign currency. For example:

An Indian company sells products to US company during 2008. Suppose US currency depreciates by 50% less what Indian company expected. Indian company will receive 50% less cash flow than what it anticipated. If the Indian company invoiced the products in Indian currency; it would not have subjected to this exposure. Some of the techniques to eliminate transaction exposure:

TECHNIQUES Forward hedge: Forward contracts are being commonly used by big corporations which desire to hedge. Forward contract is an agreement to exchange currencies on specific date in the future at some stipulated price. Union Carbide a known US multinational has mentioned and emphasized on recognition to forward contracts.

MONEY MARKET HEDGE This type of hedge involves a money market position to cover a future receivable or payable position. Hedging of this type will depend upon the cash position of the firm opting for money market hedge. If a firm has excess cash, it can create a short term deposit in the foreign currency that it will need in future.

In many cases firms prefer to hedge payables without using their available cash balances. A money market hedge can even be used in such a situation but it will require two money market positions. (a) Borrowed funds in the home currency (b) A short term investment in the foreign currency

QUESTION-8 Delineate the specific reporting issues of an MNC. What are the regulatory disclosure requirements for that reporting and disclosure?

REPORTING ISSUES Language barriers: Any organization in its routine would generally prepare its financial statements in the language of the country in which it is located. Financial statements being prepared in Pakistan will be in Urdu and it will be very difficult for the users who doesn’t know Urdu language. It will be beneficial on account of such users that the same financial statements may be presented in a global language.

Accounting principles: Another complicated problem is the financial statements prepared in accordance with requirements of countries other than the country of their domicile is the significant difference in accounting principles from the ones they are accustomed. There can be conceptual differences.

Currency problem: Generally financial statements are prepared in reporting currency for example in India they are prepared in Rupees. It would be very difficult for an Indian company to translate its financial statements in US dollars to serve the needs of American investors.

Disclosure requirements: It is possible that the particular information disclosure may have different meanings for different users of financial information. For example any information regarding new product launched is given to its shareholders but at the same time it might reveal the strategic information to competitors thereby reducing the reporting company’s competitive advantage.

Auditing standards: The legitimate function of auditing is to lend credibility to the financial statements prepared by accounting professionals. Harmonization of auditing standards is required particularly in those situations when the package of financial statements prepared by one company in a country has to be used by the users of other country.

REGULATORY REQUIREMENTS United Kingdom: Primarily regulated by company law Section 228 of the act states that while reporting of financial statements the balance sheet and p/l account shall give a true and fair view of company’s affairs. In new British company law of 1989, a number of new disclosure requirements particularly related to groups have been inserted (goodwill and disposal).

U. S. A: Division of corporation finance in SEC in USA has prepared international financial reporting and disclosure issues in 2001 which covers: Overview Recent of disclosure rules to foreign issuers commission action Concept release about IAS Regulation Changing of merger and acquisitions to US GAAP for the primary financial statements

India: Books of accounts should be kept on due basis Preserve Lay their books for 8 years the duty of director before the AGM Schedule VI to provide for details and contents of balance sheet and profit and loss account, Balance sheet must be signed by company secretary and at least two directors. Companies to appoint CA’s within the meaning of CA act 1949 qualified to be appointed as auditors of company.

Income tax act 1961: Mandatory tax audit for those who are getting their business audited. Books to be maintained either on cash or mercantile basis. Valuation of inventory for determining the income under business and profession

QUESTION-9 Discuss about the rationale of harmonisation in accounting and reporting. How is the harmonisation decrease by certain obstacles.

Meaning Harmonisation is a process of increasing the compatibility of accounting practices by fixing the limits to their degree of variation. The aim of accounting harmonization is to make the financial statements of companies comparable with the financial statements of companies in other countries. Accounting harmonisation is important because companies want to operate in a business environment in which they can trade, raise capital , list their securities and attract investors in different countries

Need for harmonisation 1. Harmonisation reporting. ensures high 2. Harmonisation ensures a reporting and disclosures. quality financial reliable financial 3. Harmonisation enables a systematic reviews along with evaluation of performance of a multinational corporate unit having subsidiaries in various countries where in each country has its own set of GAAP.

4. Harmonisation adds to the global credibility of a corporate unit. 5. Harmonisation makes the comparison of the corporate unit against the domestic and international peers more easier. 6. Harmonisation provides a level of playing ground where no country is advantaged or disadvantaged by its GAAP. 7. Sometimes Harmonisation can prove to be crucial to the economic development of a country.

Meaning of Standardisation refers to the imposition of a more rigid and narrow set of rules. In accounting, concept of standardisation adopted by European Community (EC) is harmonisation which permits the prevalence of different standards in different member nations.

Need for standardisation Pressure for harmonisation from both Those who prepare and regulate financial statements Those who use the financial statements

Barriers to harmonisation 1 . Spirit of Nationalism: - Spirit of nationalism among accounting professionals in different countries sometimes creates hurdles in accepting compromises which they have to make in changing their accounting practices. National pride prevents them from accepting willingly the idea that his accounting principles are inferior to those of another country, Even though the accountant may be a strong proponent of harmonization.

2. Different Legal Environments: - Legal or statutory environment plays a dominant role in the development of accounting thought in every country. Legal systems differ from one country to the other. . Since the legal system in a country exercises a strong influence over the accounting and reporting practices, it is clear that unless and until uniformity in laws is possible, it will be difficult to achieve the goal of harmonization of divergent accounting practices.

Objectives of Financial Reporting: - The purposes of financial reporting differ from country to country. That can be the possible cause of variation in reporting practices also. Financial reporting in every country is done by keeping in mind the targeted audiences. For example in North America target audiences are the investors and creditors where as in European countries like France and Germany, accounting is performed for revenue and government agencies. 4. Lack of Strong Professional Accounting Institutes: IASC at global level is playing a dominant role for development of IAS’s. This committee operates through national professional institutes for example ICAI, ICWAI are the members of IASC. 3. Varying

In countries, where professional institutes are not strong enough to get the standards implemented in their respective countries it will be a difficult task to bring harmonization in divergent accounting practices. 5. Economic Gap between Developed and Developing Nations: - There is a wide economic gap between developed and developing nations. This gap is a hurdle in bringing out harmonization in divergent accounting practices. It will be better to understand interaction between economic and accounting system.

QUESTION-10 How is financial statement analysis associated with the international financial reporting standards and the economy of any nation? How are the international financial reporting standards prepared and finalised Explain ?

Meaning of financial statement Financial statement analysis is the process of reviewing and evaluating a company’s financial statements (such as the balance sheet or profit and loss statement), thereby gaining an understanding of the financial health of the company and enabling more effective decision making. Financial statement records financial data however this information must be evaluated through financial statement analysis to become more useful to investors, shareholders, managers and other interested parties.

Types of Financial Analysis On the basis of material used External analysis Internal analysis On the basis of modus operandi Horizontal analysis Vertical analysis

On the basis of material used External – it is carried out by outsiders of the business-investors, credit agencies, government agencies, creditors etc. who does not access to internal records of the company depending mainly on published accounts. Internal- It is carried out by persons who have access to internal records of the companyexecutives, manager etc-by officers appointed by government or courts in legal litigation etc. under power vested in them.

On the basis of modus operandi Horizontal data - relating to more than one year comparison with other yearsstandards or base year- expressed as percentage changes-dynamic analysis. Vertical – Quantitative relationship among various items in statements on a particular date –inter firm –inter department comparisons- static analysis

IFRS The International Financial Reporting Standards, usually called the IFRS Standards, are standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB) to provide a common global language for business affairs so that company accounts are understandable and comparable across international boundaries. They are the rules to be followed by accountants to maintain books of accounts which are comparable, understandable, reliable and relevant as per the users internal or external

Objectives of IFRS General Objective: Provide information that is useful to present and potential investors, creditors, and other users in making rational investment, credit, and similar decisions Derived External User Objective: Provide information that is useful to present and potential investors, creditors, and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts from dividends and interest, and the proceeds from the sale, redemption, or maturity of securities or loans

Other objectives To provide financial information useful for estimating the earning potentials of the firm. To provide other information about changes in economic resources and obligations To disclose other information relevant to statement users need.

Qualitative characteristics for financial information Understandability: transactions and events must be accounted for and presented in the financial statements in a manner that is easily understandable by a user. 2. Comparability: comparability enables users to identify the real similarities and differences in economics events between companies. 3. Timeliness: timeliness means having information available to decision makers before it loses its capacity to influence decisions. 4. Verifiability: occurs when independent measures, using the same methods, obtain similar results 1.

Procedure for standard setting ASB determines a particular area in which the need of standards is required. In preparation of standards , various study groups constituted for special subjects assist the ASB while forming these study groups, gives a special attention to the participation of various members of institute and others. A discussion is conducted with representative of government, public sector undertakings, industry and other organisations.

Cont…. An exposure draft is prepared by keeping in view the ideas and views expressed during the discussion with representatives. Exposure draft of the proposed standard is published in the journal “The Chartered Accountant” for inviting the comments of members of the institute on exposure draft. The draft standard is finalised by the ASB after taking into consideration the comments of the members.

Cont… Finalised draft standard is submitted to the council for approval, the council may decide to modify the draft with the consultation of ASB. At final stage , the accounting standard is issued under the authority of the council.

Financial Reporting Standards practices These reporting practices can be divided into four categories listed as under: 1. Supplementary information: provide some additional information which help them in better understanding. 2. Restatements: restate the income figures according to GAAP of another country. 3. Dual financial reporting: company has to prepare two sets of financial statement a primary and other a secondary.

Primary statements: based on accounting and reporting standards of domicile country. Secondary statements: prepared specifically for audience of interest in foreign countries. 4. Translation: concept of global investor may compel to translate financial statements. This may take two forms: i. Language translated ii. Language and currency translated.

- Slides: 105