INTERNATIONAL ACCOUNTING INTERNATIONAL TRANSFER PRICING Transfer Pricing in

A Direct or indirect Both A and")

FULL COST")

PARTIAL COST As the name suggests, it can never be the full cost.")

(d) Appropriate for transactions which are not capable of being")

Bench")

- Slides: 45

INTERNATIONAL ACCOUNTING INTERNATIONAL TRANSFER PRICING

Transfer Pricing in India- Background Prior to April 1, 2001 � Basic provisions existed but were rarely applied � Expert Group set up in November 1999 to study global transfer pricing practices April 1, 2001 onwards � Comprehensive legislation introduced in Union Budget 2001 � Detailed Rules providing guidance for application of the legislation framed

TRANSFER PRICE REGULATIONS India International OECD formulated “Guidelines on transfer pricing”. They serve as generally accepted practices by the tax authorities The Finance Act 2001 introduced the detailed TPR w. e. f. 1 st April 2001 The Income Tax Act AS-18 Other Relevant

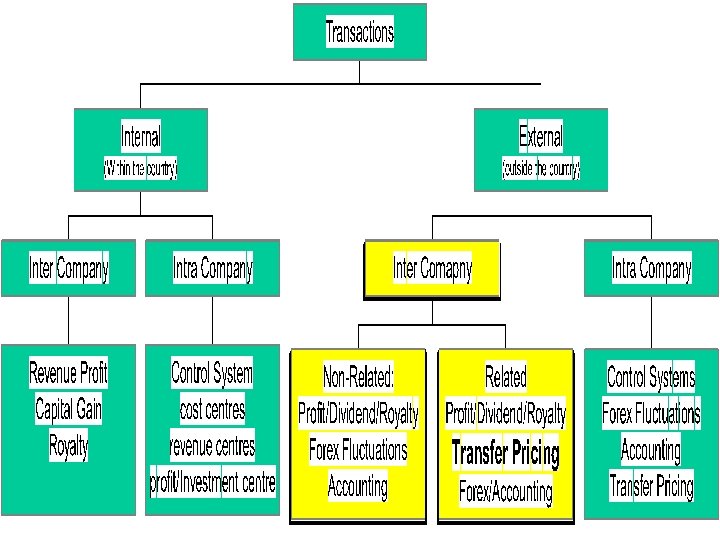

Transfer Pricing Background Transfer pricing is the determination of price on the exchange of goods or services between related parties. These transfers are also referred to as intercompany transactions. Upstream transfers go from subsidiary to parent, downstream transfers are from parent to subsidiary. Transfers also occurs between different subsidiaries of the same parent. 11 -5 A significant proportion of international

of TRANSFER PRICING A price between unrelated parties is known as the “arm’s length” price Transfer Pricing refers to pricing of international transactions between two associated enterprises (AEs) Due to special relationship between related parties, transfer price may be different than the price that would have been agreed between unrelated parties

DEFINITION Transfer price is the price established for goods and services sold by one division of the organisation to another division of same organisation. According to HORNGREN & FOSTER The Transfer Price is the price one segment of organisation (sub unit, department, division) charges for product or service supplied to another segment of same organisation. The modern view of Transfer Price is inter company transfers between affiliates.

OBJECTIVES WORLDWIDE TAX MINIMISATIO N REDUCING IMPORT DUTIES MANAGEME NT OF CURRENCY FLUCTUAION

Applicability • • The provisions of Section 92 to 92 F of the Act are applicable only if: – There are two or more enterprises (defined in Sec 92 F) – The enterprises are Associated enterprises (defined in Sec 92 A) – The enterprises enter into a transaction (defined in Sec 92 F) – The transaction is an International transaction (defined in Sec 92 B) Consequences of these provisions: – Computation of income/ expenses having regard to the Arm’s length price (Section 92(1)) – Maintenance of prescribed Documentation (Section 92 D & Rule 10 D) – Obtaining of Accountant’s report (under Form 3 CEB) (Section 92 E) – To ensure compliance with the arm’s length principle, stiff Penalties have been prescribed

Concept Associated enterprise Independent entity International transactions - goods - services - intangibles - loans Resident Transfer price Resident Arm’s length price

ASSOCIATE ENTERPRISE: 92 A Direct Control/Control through intermediary Holding 26% of voting power Advance of not less than 51% of the total assets of borrowing company. Guarantees not less than 10% on behalf of borrower Appointment of more than 50% of the BOD Dependence for 90% or more of the total raw material or other consumables

Meaning of Associated enterprises (Section 92 A) A Direct or indirect Both A and B B participation are associated enterprises of C (through one or C more D A D and E are also intermediaries) in associated B E enterprises of C since they have a management, common ultimate C parent (A) control or capital

INTERNATIONAL TRANSACTIONS: 92 B v Transactions between two or more associated enterprises, either or both of whom are non-residents Transaction relates to Ø purchase, sale or lease of tangible or intangible property; or Ø provision of services; or Ø lending or borrowing money; or Ø any other transaction having a bearing on the profits, income, losses or assets of the enterprises; or Ø mutual agreements or arrangements for allocation or apportionment of, or any contribution to, any cost or expense incurred

RELATED PARTIES As per Accounting Standard 18, Requires disclosure of ‘any elements of the related party transactions necessary for an understanding of the financial statement Control by ownership � 50% of the voting right Control over composition of board of directors � Power to appoint or remove the directors Control of substantial interest � 20% or more interest in the voting power

ARM’S LENGTH PRICE Price which two independent firms would agree on. v Price which is generally charged in a transaction between persons other than associated ü

FACTORS AFFECTING TRANSFER PRICING Internal factors Externa l Factors • Performance Measurement • Evaluation • • • Accounting Standard Custom Duty Currency Fluctuations Risk of Expropriation Income Tax

HEADQUARTERS SETUP TRANSFER PRICE SENT TO DIVISION BASED ON TRANSFER PRICE, DIVISION REPORTS BACK TO HEADQUARTERS WITH THE DEMAND

SIGNIFICANCE OF INTERNATIONAL TRANSFER PRICING Promotes goal congruence and sustained high level of management effort. It has become an important area of multinational corporate policy. Management gurus have suggested MNCs that if they have MANAGEMENT problems then MBO, Divisionalisation & Decentralisation are the only solutions. Transfer pricing is part of DIVISIONALISATION It helps in evaluation of the performance of each division. It also helps to guide managers to take best possible

APPROACHES TO TRANSFER PRICING ECONOMIC ANALYSIS MATHEMATIC AL PROGRAMMIN G CONVENTION AL ACCOUNTING MEASURES OF COST LINEAR PROGRAMMIN G DECOMPOSITI ON PRINCIPLE QUADRATIC PROGRAMMIN G

Performance Evaluation, Cost Minimization, and Transfer Pricing Performance evaluation systems Transfer prices directly affect the profits of the divisions involved in an intercompany transaction. Some performance evaluation systems are based on divisional profits. The effectiveness of these performance evaluation systems is influenced by the fairness of transfer prices. The effectiveness of performance evaluation systems affects the satisfaction

ECONOMIC ANALYSIS § § § Problem of interdivisional transfer pricing was solved by implementing techniques and tools of micro-economic analysis by HIRSHLEIFER in 1956. He said that there are two independent profit centres in a firm i. e. manufacturing division and the distribution division, each wants to maximise the profits. Both are to work under the rules and restrictions of overall management He gave a conclusion that in a COMPETITIVE MARKET, marginal cost pricing would be appropriate in producing Goal Congruent Results. But in the imperfect market it would not be suitable. OPERATIONAL PROBLEMS: Feasibility of computations Constraints No divisional autonomy

CONVENTIONAL ACCOUNTING METHODS ACCOUNTING MEASURES OF COST BASED METHOD MARKET BASED METHOD MODIFIED MARKET PRICE MISCELLANE OUS TRUE COST NEGOTIATED MODIFIED COST TARGET STANDARD COST DUAL PARTIAL COST

Sale of Tangible Property Comparable uncontrolled price method Widely considered the most reliable measure when a comparable uncontrolled transaction exists. Transfer price is determined based on reference to the company’s sales of the same product to an unrelated buyer. Reference to transactions between two unrelated parties for the same product are acceptable. If an uncontrolled transaction is not exactly comparable, an adjustment is allowable.

1. COST BASED METHOD THIS METHOD IS SUITABLE : Most appropriate when comparable uncontrolled transactions don’t exist and sales subsidiary does more than simply distribute finished goods. Transfer price is determined buy adding gross profit to the cost of production. Gross profit is determined by reference to uncontrolled parties. Factors influencing the comparability of uncontrolled transactions include: complexity of manufacturing process, procurement activities, and testing functions. Form of cost Full cost Modified full cost Standard cost Partial cost

Transfer price can be determined by using any form of cost. (A) FULL COST This method of transfer price takes into account the total cost i. e. direct and indirect costs, fixed as well as variable. This method is very simple, easily available & determined in exact terms. (B) STANDARD COST This main reason for using the standard cost is that the inefficiencies of the selling division are passed on to the buying division in form of inflated prices. But if standard cost is used then it will help to reduce this short-coming.

(C) PARTIAL COST As the name suggests, it can never be the full cost. So in simple terms, partial is the cost of the unit transferred but it does not cover all the costs. This means only the part of cost is considered like the variable costs. (D) MODIFIED COST Many modifications in the cost can be done to determine the transfer price. So under this model, the product or service is charged by an inflated price. The addition is a fixed amount per unit or a

Cost Plus Method Identification of direct and indirect costs of production incurred in tested party transactions Identification of normal gross profit with reference to uncontrolled transaction(s) Normal gross profit adjusted to account for functional and other differences if any Adjusted gross profit added to total costs identified in step 1 Sum arrived above is taken to be arm’s length price

Sale of Tangible Property Cost-plus method Learning Objective 5 11 -29

2. MARKET PRICE METHOD Market price based on Price of semifinished product On the price of ultimate market price Market price can only be used when intermediate market exists for the product or service. Selection of market price can solve the problems of the cost based methods. Transfer price based on market price is fair, objective measure of value of product

Sale of Tangible Property Comparable profits method Underlying principle is that similar companies should earn similar returns over a period of time. One of the two related parties in the transactions is chosen for examination. Transfer price is determined via reference to an objective measure of profit of an uncontrolled company involved in comparable transactions. Typical measures of profit include: ratio of operating income to operating assets, and operating income to sales. Learning Objective 5 11 -31

Sale of Tangible Property Profit split method Treats the two related parties as one economic unit. Profit from the eventual sale to an uncontrolled party is allocated between the related parties. Allocation is based on relative contribution of each party. Contribution is determined by functions performed, risk assumed, and resources employed. There actually two versions: comparable profit split method and residual profit split method. Learning Objective 5 11 -32

Sale of Tangible Property Resale price method Generally used when the affiliate is a sales subsidiary and simply distributes finished goods. Transfer price is determined by deducting gross profit from the price charged by the sales subsidiary. Gross profit is determined by reference to uncontrolled parties. The most important factor in choosing this method is the similarity in function of the affiliated sales subsidiary and the uncontrolled reference company. Learning Objective 5 11 -33

Profit Split Method-Rule 10 B(1)(d) Appropriate for transactions which are not capable of being evaluated separately Calculates the combined operating profit resulting from a whole inter-company transaction based on the relative value of each associated enterprise's contribution to the operating profit The contribution made by each party is determined on the basis of a division of functions performed, valued, if possible using external comparable data Applicable for analysing tangible, intangible or services issues

Profit Split Method Determination of combined net profit of the associated enterprises arising out of international transaction Evaluation of relative contributions by each enterprise on the basis of functions performed, risks assumed and assets employed Splitting of combined net profit amongst enterprises in proportion to their relative contributions Profit thus apportioned to the tested party is used to arrive at the arm’s length price

3. OTHER METHODS As the name says, it is the price settled after the bargaining between the selling and the buying division. OTHER METHOD S Negotiated price Target profit price Negotiated price- Target Profit Price. Under this method, the transfer price is so formed to provide a reasonable profit to the selling divisions say 10% of the standard costs r actual costs. Dual pricing – Sometimes in an organisation, it is not possible to have single transfer price for meeting goal congruence divisional autonomy and

CONDITIONS FOR CHARGING LOW OR HIGH TRANSFER PRICE Corporate tax rate Inflation rate Ad valorem tariffs Political stability Export subsidy or tax credit on value of exports.

ACCOUNTING ISSUES IN INTERNATIONAL TRANSFER PRICING A. B. SEGMENTAL ACCOUNTS WERE NOT MANDATORY IN INDIA TILL 2001. COMPARABILITY IN SPECIAL CIRCUMSTANCES LEGAL ISSUES IN TRANSFER PRICING: The main legal issue is the taxation related to transfer price. With the growth in the volume of intrafirm trade, the transfer pricing practices of the MNCs have come under the taxation authorities.

ADVANCED PRICING AGREEMENTS § § MNCs have adopted a mechanism known as the Advances Pricing Agreement (APA) to settle the disputes with tax authorities. An APA is an agreement between the company and a tax authority under which the company can use a specified method of transfer pricing for a fixed term which shall be accepted by the tax authority. Such agreements are formal and has set terms and conditions. Apple computer was the first company to enter into such an agreement in early 1991.

Problems faced while setting the Transfer Pricing Determination of Arm’s length price (ALP) Bench marking Data bases Allegation of Dumping Sub Optimal Decision Making

TRANSFER PRICING IN INDIA Legal Status- The finance Act 2001 introduces with effect from assessment year 2002 -03 detailed transfer pricing regulations vide Section 92 to 92 F of the income tax Act 1961. The CBDT has come out with Transfer Pricing Rules -Rule 10 A to 10 E. Applicability- Transfer pricing provisions are applicable based on some criteria: v v v v There must be an international transaction. Such transaction must be between two or more associated enterprises either or both of whom are nonresident. Comparable Uncontrolled Price Resale Price Method Cost Plus Method Profit Split Method Transactional Net Margin Method

DOCUMENTATION IN INDIA 13 different types of documents are required to be maintained in India which can be categorised into three parts: � Enterprise wise documents � Transaction specific documents � Computation related documents PENALITIES IN INDIA Penality for concealment of income or furnishing inaccurate particulars thereof 100% to 300% of the tax sought to be evaded. Penality for failure to keep and maintain documents in respect of international transaction is 2% of the value each transaction. Penality for failure to furnish report under sec 92 E is Rs.

Trend visible in annual reports of companies in India Companies Amount transferred in crores Reliance Industries Ltd. 988 Ballarpur Industries Ltd. 194 Century textiles Ltd. 23 Asian Paints (1) Ltd. 10

OVERALL MANAGEMENT DIVISION MANUFACTURING DISTRIBUTION DIVISION MAXIMISE PROFIT

THANK YOU