Internal Audit in LISD MISSION PURPOSE AND STRUCTURE

- A Global Institution recognized authority on")

Mission: To enhance and protect organizational value")

Consideration of Fraud According to AU section 316, school")

")

Internal Audit Express an opinion on the financial")

Internal Audit External Audit Approach Sufficient work undertaken")

Comprehensive AFR (CAFR) Minimum")

- Slides: 30

Internal Audit in LISD MISSION, PURPOSE AND STRUCTURE FOR LEANDER ISD

Agenda Legal Requirements Mission & Purpose of Internal Audit Structure & Responsibilities Risk Assessment Process and Audit Plan Fraud Hotline Board Communications and Updates Internal vs External Audit

International Requirements Institute of Internal Auditors (IIA) - A Global Institution recognized authority on Internal Auditing around the world International Professional Practices Framework (IPPF) • Core principles for the profession • Definition of Internal Auditing • Code of Ethics • International standards

Legal Requirements The Board shall select the internal auditor if a district employs an internal auditor. The internal auditor shall report directly to the board. Texas Education Code 11. 170

Legal Requirements An audit working paper of an audit performed by the district auditor, including any audit relating to the criminal history background check of a public school employee, is excepted from public disclosure. If information in an audit working paper is also maintained in another record, that other record is not excepted. Texas Government Code 552. 116

Mission & Purpose of Internal Audit (IIA) Mission: To enhance and protect organizational value by providing risk-based and objective assurance, advice, and insight. Purpose: The Institute of Internal Auditors (IIA) defines Internal Audit as: “An independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. The Internal Audit activity helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes. ” Institute of Internal Auditors, International Professional Practices Framework (IPPF), Revised 2016

Purpose of Internal Audit (TEA) Consideration of Fraud According to AU section 316, school districts’ auditors are expected to perform procedures to assess the risk of fraud. The management of a school district is responsible for implementing appropriate administrative systems and policies that will sufficiently diminish the risk of fraud. . It is recommended that school districts that have an enrollment of 5, 000 and larger perform a periodic selfassessment of the risk for fraud. If a school district does not have an internal audit department, the selfassessment may be obtained through a contract with a public accounting firm. Texas Education Agency’s Financial Accountability School Resource Guide (April 2012)

The Three Lines of Defense

Internal Audit Responsibilities Internal Audit Charter Risk Assessment & Audit Plan Financial Assurance Services Compliance LISD Fraud Hotline Operational Control Self-Assessment Services (CSA) Efficiency Reviews Consulting Services Assurance Service:

Internal Audit Charter Standard 1000 – Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent with the Definition of Internal Auditing, the Code of Ethics, and the Standards. The chief audit executive must periodically review the internal audit charter and present it to senior management and the board for approval. Interpretation: The internal audit charter is a formal document that defines the internal audit activity's purpose, authority, and responsibility. The internal audit charter establishes the internal audit activity's position within the organization, including the nature of the chief audit executive’s functional reporting relationship with the board; authorizes access to records, personnel, and physical properties relevant to the performance of engagements; and defines the scope of internal audit activities. Final approval of the internal audit charter resides with the board. Copyright © 2017 by The Institute of Internal Auditors, Inc. All rights reserved.

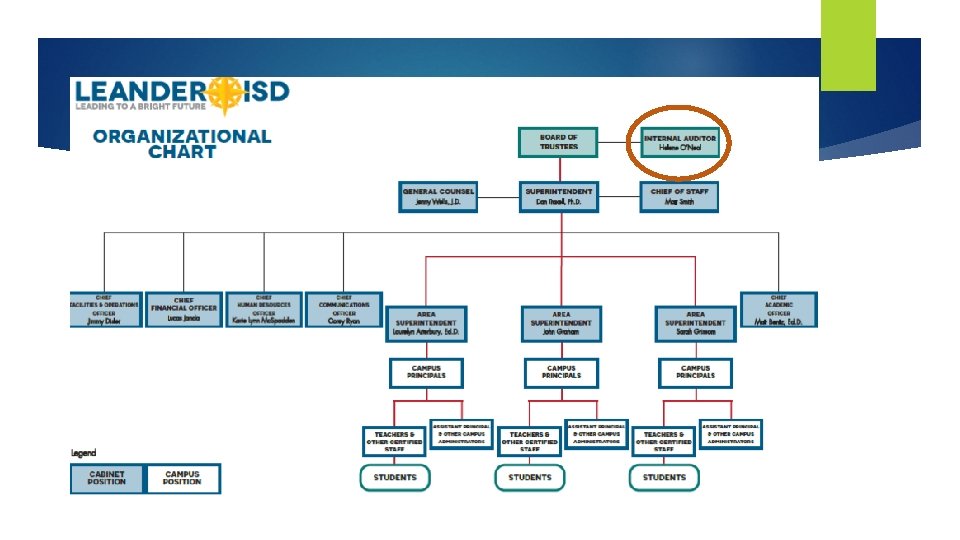

Internal Audit Structure Standard 1110 – Organizational Independence The chief audit executive must report to a level within the organization that allows the internal audit activity to fulfill its responsibilities. The chief audit executive must confirm to the board, at least annually, the organizational independence of the internal audit activity. Interpretation: Organizational independence is effectively achieved when the chief audit executive reports functionally to the board. Examples of functional reporting to the board involve the board: Approving the internal audit charter. Approving the risk-based internal audit plan. Approving the internal audit budget and resource plan. Receiving communications from the chief audit executive on the internal audit activity’s performance relative to its plan and other matters. Approving decisions regarding the appointment and removal of the chief audit executive. Approving the remuneration of the chief audit executive. Making appropriate inquiries of management and the chief audit executive to determine whethere are inappropriate scope or resource limitations. Copyright © 2017 by The Institute of Internal Auditors, Inc. All rights reserved.

Risk Assessment & Audit Plan Annual process performed in late spring Management completes risk matrix Audit reviews and makes adjustments Draft audit plan created Risk assessment results provided to Executive Management for review & additional input Audit plan adjusted (in necessary) Risk Assessment results and proposed Audit Plan presented to Board of Trustees approves annual Audit Plan in August/September

Risk Factors: District Financial Impact Frequency/Complexity/Volume of Transactions Regulatory/Legal Impact District Image/Reputation or Market/Customer Impact Changes in Area/Management/Systems or Processes Quality of Internal Control System Availability & Reliability of Computer Systems Importance/Integrity of Data & Reports Opportunity of Fraud/Waste or Abuse Safety & Security Time Since Last Audit

Risk Factors: Campus Enrollment Budget Turnover in critical functions Activity Funds Time Since Last Audit Note: All LISD campuses have been audited at least once

Internal Audit Projects Employee Leave Purchasing / Procurement Card State Assessment Construction Projects ITS General & Security Fueling Process Disaster Recovery/Business Continuity Athletics Department PEIMS Contract Management IMA / Textbooks Payroll Fixed Asset/Controllable Inventory Accounts Payable CSA Consulting Projects: EPR Phase I - Finance ERP Phase II – HR/Payroll

LISD Fraud Hotline Anonymous reporting available 24/7 English and Spanish options Supports Leander ISD’s 10 -Ethical Principals and Policies Communication to organization Review committee

Board Communications & Updates Internal Audit Management reports Audit Observation Status Reports Assurance Reports – audit projects, confidential areas and followups Board of Trustee Liaison

Audit Observation Status Reports This report is developed from the Campus/Corrective Action Plans (CAPs) created to address audit observations identified in audit reports. Updates of this report are provided to the Board usually on a quarterly basis. Status Definitions: IN PROCESS – District/Campus implementation or resolution in process, Internal Audit will follow-up later to confirm AFFIRMED – Management declares task resolved; Internal Audit will verify at a later time COMPLETE – Internal Audit has confirmed that the task is fully resolved and closed at this time RISK ACCEPTED - District has accepted current or residual risk of this task NOT ON TRACK – Task estimated completion date has lapsed; District/Campus is currently not in process of resolution

Internal Audit vs. External Audit (continued) Internal Audit Express an opinion on the financial condition Shareholders via Board & Chief Financial Officer (CFO) Fair representation of financial statements Primary Audience Analyze and improve controls and performance Board of Trustees, works closely with management Enhance and protect organizational objectives and values The IIA’s International Standards for the Professional Practice of Internal Auditing Board, executive management Timing Past/Present/future, ongoing Past, point in time Purpose Reporting relationship Focus Standards Copyright © 2017 by The Institute of Internal Auditors, Inc. All rights reserved. Generally Accepted Auditing Principles, Generally Accepted Auditing Standards Investors, public interests

Internal Audit vs. External Audit (continued) Internal Audit External Audit Approach Sufficient work undertaken to provide insight Sufficient work completed to form an and give informed assurance to the Board opinion on the financial statements Scope Organizational operations Fiscal financial records Skills Interdisciplinary Accounting, finance, tax Employment Relationship An organization’s employee, Independent of A contracted third party Management Copyright © 2017 by The Institute of Internal Auditors, Inc. All rights reserved.

Internal Audit is… • NOT the police • Part of the District’s control structure • Not responsible for implementation or oversight of the district’s controls • A resource to assist in developing or evaluating operational processes and systems • Not something to be afraid of, we are on the same side

Annual Audit Report THE LEGAL REQUIREMENTS AND THE FINANCIAL PERFORMANCE OF LISD

Key Areas of External Review Board minutes Budget and cash management Board Compliance with all laws Management Questionnaires Grant management Related party transactions Maintenance of effort State aid reconciliation Procurement Recording of settle-up Use of taxpayer funds Spending requirements Financial statement accuracy Internal controls Litigation Payroll accuracy / coding Tax collections Third party confirmations

Differences in Types of External Audits Annual Financial Report (AFR) Comprehensive AFR (CAFR) Minimum requirement for school districts Highest level of transparency in financial reporting Basic financial statements Required supplementary information Includes everything in an AFR along with the following: Combining & individual statements Schedules & statistical tables

Leander ISD 2016/2017 Audit

Key Points of LISD Audit General Fund Unmodified opinion $ 11, 681, 286 surplus Highest level of assurance $148, 888, 849 in fund balance Clean audit report Debt Service Fund Satisfies highest reporting standard $ 6, 725, 053 deficit ASBO Award $ 28, 544, 170 in fund balance GFOA Award

What is the Purpose of Fund Balance? Covering cash flow deficits in the fall until property taxes are collected in January Legislative cuts and unfunded mandates Lower interest rates on district bonds Ongoing support for educational programs Unforeseen expenditures and disasters

Fund Balance Guidelines The State provides guidance to schools that each district should have two months of cash disbursements to cover any cash flow deficits – no focus is given to the debt service fund. The foresight of the LISD Board includes the following expectations of administration for fund balance: Maintain two months of operating funds in reserve Goal shall be to have three months of operating funds in reserve Maintain at least 20 percent of the next year’s interest & sinking requirements Goal shall be to have 30 percent of next year’s interest & sinking requirements

Questions? Answers