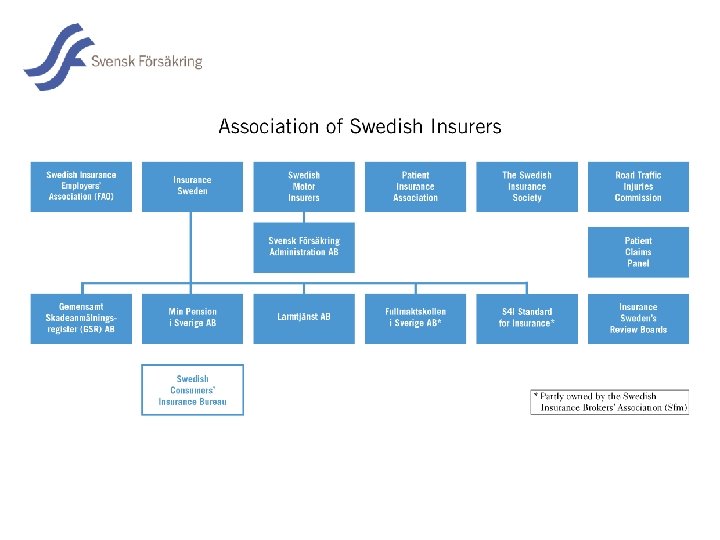

Insurance Sweden and the Swedish Insurance Market Pr

• Sofisticated market with a wide")

• Modest market concentration - Five")

- Slides: 34

Insurance Sweden and the Swedish Insurance Market Pär Karlsson, Senior Adviser Insurance Sweden 2019 -09 -11

Agenda • Insurance Sweden • The Swedish Insurance Industry • Non-life and Life Insurance • Cyber Risk and Cyber Insurance

Main areas • Good business conditions for Insurance Companies • Increased confidence in the Insurance Industry • Increased understanding for Insurance Principles • Provision of some industrywide infrastructure

Role in a major crisis 1. Communication 2. A meeting place for crisis coordination 3. Dialogue with authorities Some events: • Ferry Estonia (1994) • Tsunami (2004) • The storm Gudrun (2005) • Evacuation of Lebanon (2006) • Finance crisis (2008) • Vulcano ashes (2010) • Riots in Husby (2013) • Forest fires i Västmanland (2014) • Terror attack at Drottninggatan (2017)

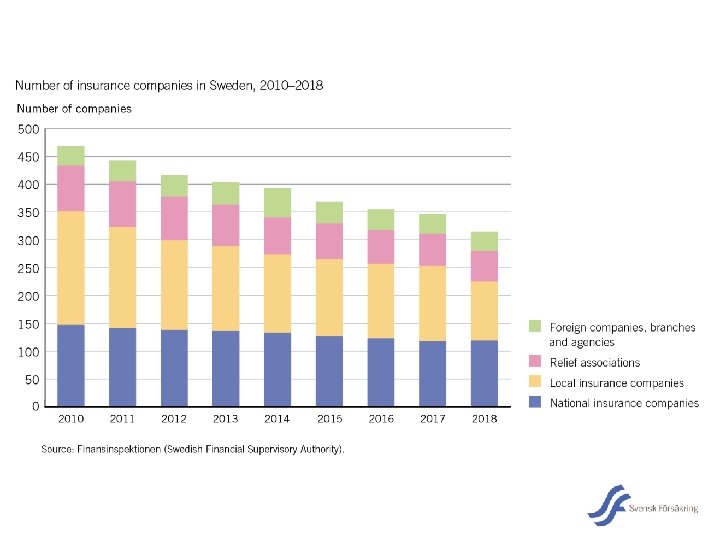

Different types of insurance companies Mutuals and hybrid companies Listed on the Stockholm Stock Exchange Foreign-owned companies Non-life Dina, Patientförs. LÖF Sveland Djur Ica Försäkringar If (Sampo, Finland) Trygg Hansa (RSA, UK) Moderna (Tryg, DK) Zurich (Schweiz) Gjensidige (Norge) Full range insurance (life and non-life) Folksam, Länsförsäkringar, AFA Försäkring Life Alecta AMF Skandia Handelsbanken Liv Nordea Liv o Pension Swedbank Försäkring SEB Pension o Försäkring SPP (Storebrand, Norge) Danica (Danske Bank, DK) 6 Private ownership Movestic

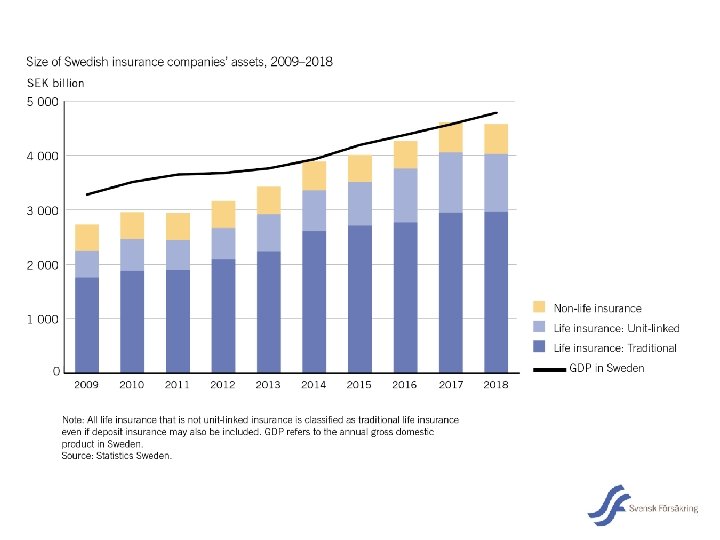

The insurance industry provides key functions in society Provides risk capital and financing Most important institutional investors in Europe Provides security for individuals and companies Pensions, savings products, personal injury insurances, property insurance Governance May affect how capital is allocated in society, e. g. by promoting CSR Damage prevention activities Promoting crime prevention, fire prevention, road safety, climate resilience, etc. An important pillar of the Nordic welfare model

Legislation for insurnace EU - EU regulation or directive - Supplementing acts, based on delegations in regulation or directive - Guidelines from European Insurance and Occupational Pensions Authority (EIOPA) National legislation - Implementation of directive in national law - Further national requirements - Implementation of directive in supervisory regulations Self regulation - Recommendations and guidelines

Principles for private insurance 1. Insurance will only cover unforeseen and sudden events (fire, accidents, injuries) 2. The insurance premium should correspond to the additional risk the individual will bring to the collective 3. The total insurance premium should cover future claims payment to the collective

Non-life insurance in Sweden Total premium income 2018: SEK 84 bn Others 7% Animal 5% Personal injury/accidents 13% Motor 26% Traffic: Compulsory third-party liability 11% Corporate and commercial property 17% 14 Home insurance 21%

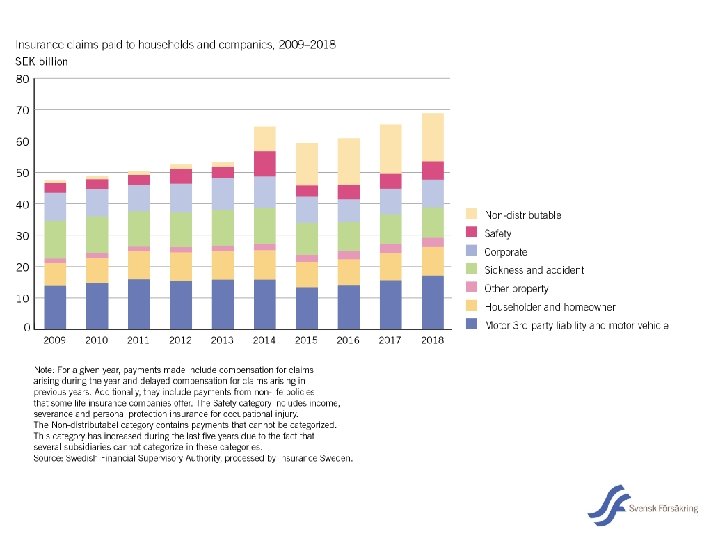

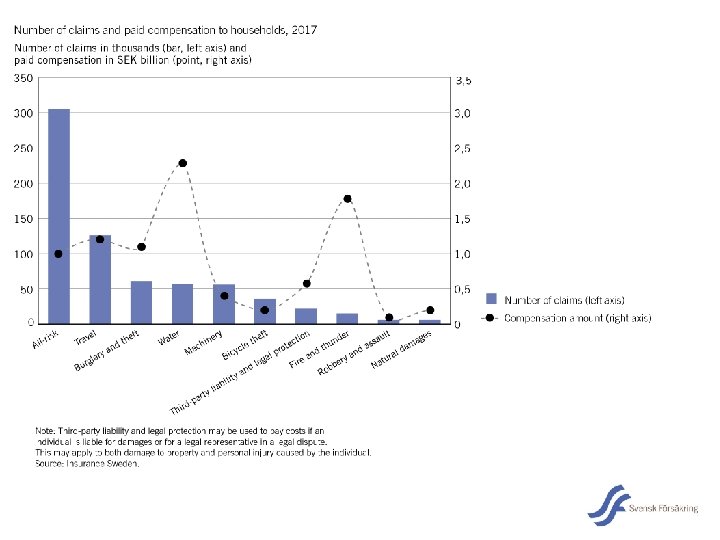

Claims payments Total claims payments: EUR 6 bn - of which EUR 3 bn relates to previous claims (e. g. annuities for personal injuries) 3 million claims are settled annually Most important insurance events: • 233 000 vehicle accidents, value EUR 0. 5 bn • 20 000 fires, value EUR 0. 4 bn • 150 000 traffic third-party liability, value EUR 0. 3 bn • 66 000 water damages, value EUR 0. 3 bn • 440 000 multirisk and travel damages, value EUR 0. 2 bn • 150 000 thefts and burglaries, value EUR 0. 2 bn • 28 000 nature damages (storm/flooding, forest fire), value EUR 0. 1 bn • 22 000 third-party liability (other than traffic), value EUR 0. 1 bn 20

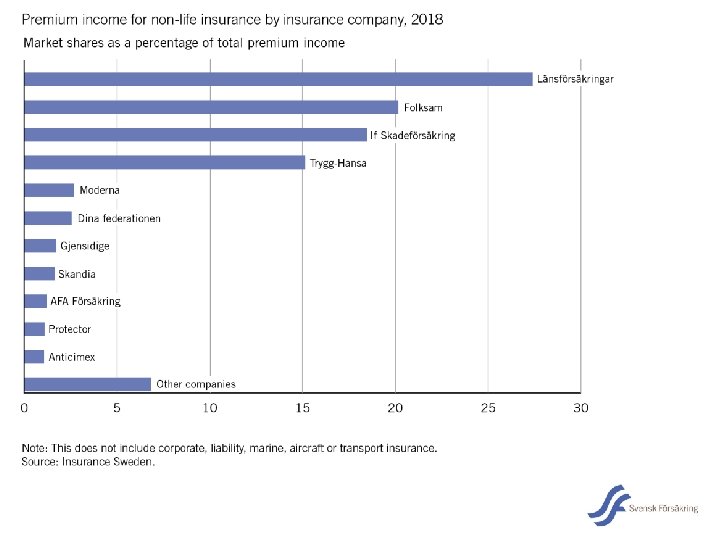

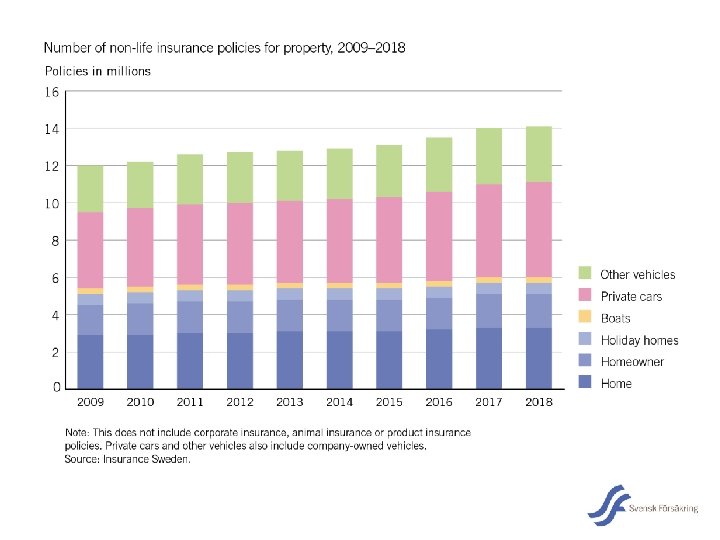

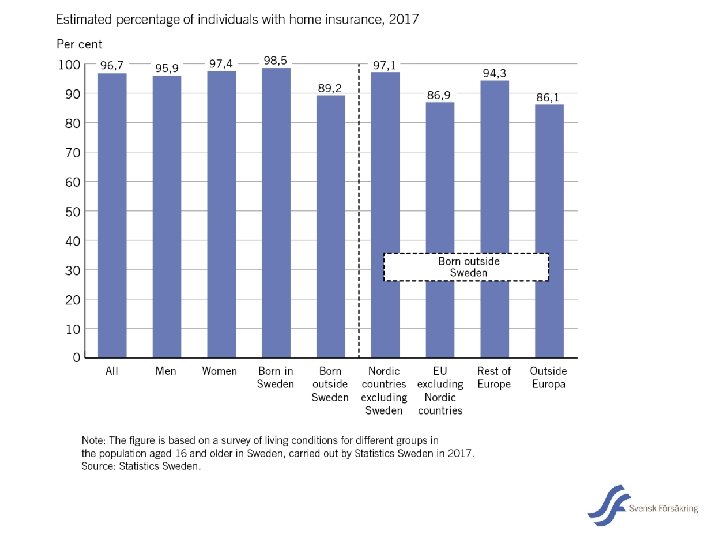

Characteristics of Swedish non-life insurance • Mature market • Product development mainly focusing on areas bordering the government welfare system, e. g. health insurance and unemployment insurance. • Insurance coverage is high: - 99% of vehicles are covered by traffic third-party liability insurance - 96% of population covered by home insurance • Insurance products with extensive coverage: - Home insurance normally includes cover for e. g. travels, nature damages, third-party liability, legal protection and multirisk • High market concentration: - Four largets companies have a market share of 80% • Several foreign companies are active on the Swedish non-life market • Captives are important in the segment for corporate and commercial property insurances • Re-insurance cover is provided by the global market players 21

Life insurance in Sweden

Insurance products are an important part of the financial savings 24

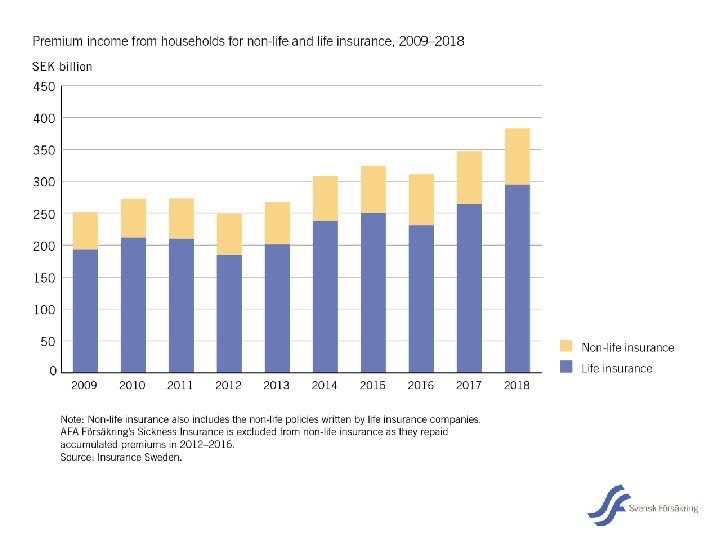

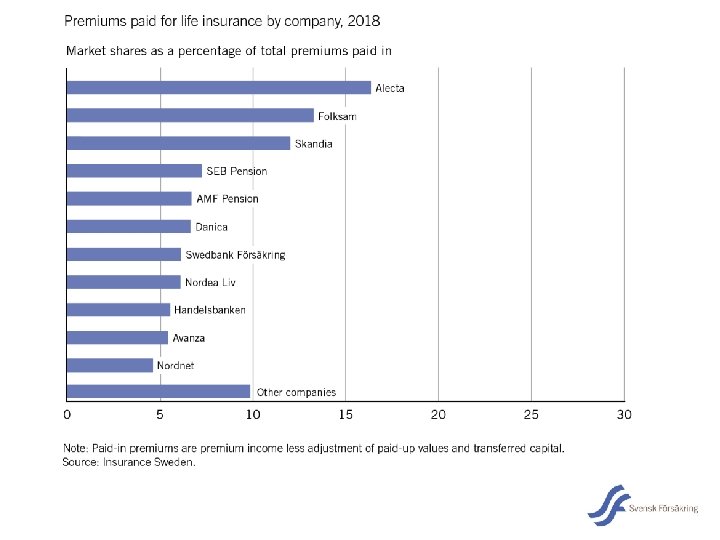

Characteristics of the Swedish life insurance market (i) • Sofisticated market with a wide range of products • Insurance products almost 50% of households financial savings • Occupational pension products (collectively-bargained) are the most important life insurance products • Occupational pensions have traditionally been offered by insurance companies (which is not the case in other EU countries) • New legislation differentiate between incurance and occupational pension, which will have a large impact on the structure of the Swedish insurance market. • Mutual companies are dominating the market • Few foreign companies are active in the Swedish life market 25

Characteristics of the Swedish life insurance market (ii) • Modest market concentration - Five biggest companies have a market share of 57% • Strong growth in occupational pension • Private pension has almost disappeared following changes in tax legislation a few years ago

Cyber Risk and Cyber Insurance

What is Cyber Risk? • Definition is missing • Effect of an attack • Different attackers • Not just IT!

Cyber risks on the rise • Digitalisation and interdependencis • Easy and sophisticated • Low cost and low risk for attacker Bild: Global Risks Report 2019, World Economic Forum

Common threats • Malware • DDo. S attack • Phishing • Ransomware • Advanced Persistent Threat (APT)

Growing demand for insurance • Stand alone cyber insurance • Never a substitute for good risk management 2020 USD 9 billion 2018 USD 6 billion 2016 USD 3 billion ”Estimated growth in gross written premiums of standalone cyber insurance. ” Source: OECD

What is included? Direct losses • Loss of revenue • Costs incurred to keep business operational • Cost to recreate/restore data Third party damage • Legal costs and damages from claims Assistance • Forensic investigations • Legal services • Notification • Crisis management • Prevention/risk assessments

Some challenges ahead • Access to risk data • Aggregated risk • Silent Cover • Taxonomi In a digitalised world we need protection for intangibel assets!