INSTITUTIONAL INVESTORS LIABILITIES AND EMERGING MARKETS Bruno Bonizzi

INSTITUTIONAL INVESTORS LIABILITIES AND EMERGING MARKETS Bruno Bonizzi and Annina Kaltenbrunner

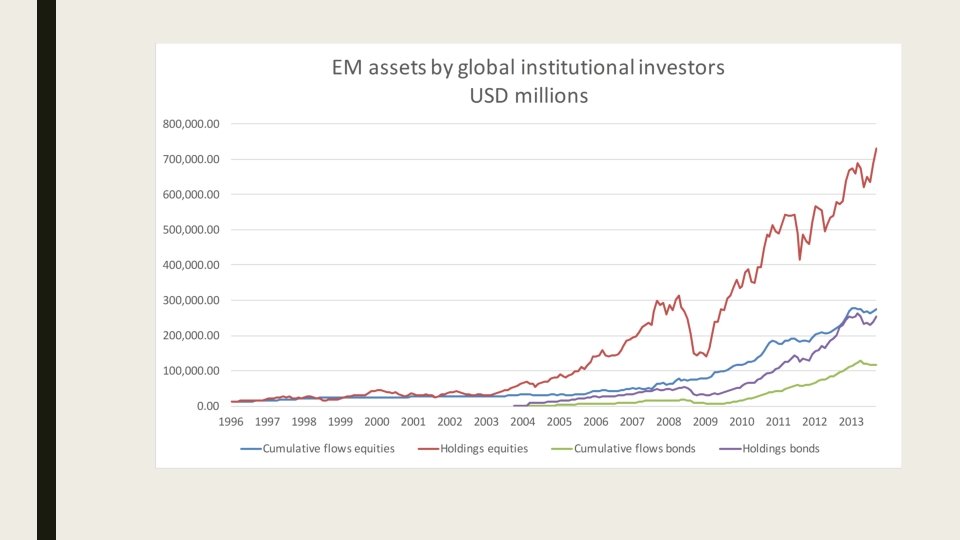

Background and key message ■ In 2014 institutional investors held about 30% of global bond and stock markets ■ Increasingly, they also invest in emerging markets ■ Liabilities are a primary determinant of institutional investors behaviour ■ By understanding the role of liabilities, we can understand the stability of asset demand by institutional investors in general and in emerging markets in particular

Liabilities and asset choice ■ Liabilities affect asset choice on two levels: 1. Assets are classified (and demanded) depending on their ability to face liabilities: – Liability-matching: protect balance sheet from volatility of liabilities – Return-seeking: grow asset size in line with the growth of liabilities 2. The choice between return-seeking and matching assets depends on how well liabilities are funded, i. e. the funding ratio

Assets and liabilities

Historical trends ■ Low funding ratios, low interest rates. Conflictual forces: – Need to generate returns – Need to protect balance sheets from volatility of liabilities ■ Result: divestment from traditional assets (domestic equities) towards foreign assets and “funds”

Shifts in asset allocation

cannot match liabilities: 1. They bear credit")

Implications ■ Emerging market assets (incl. bonds) cannot match liabilities: 1. They bear credit risk (especially if hard-currency) 2. They are denominated in a foreign volatile currency (if in local currency) 3. They respond to a different yield curve

Implications ■ Emerging markets are by definition return-seeking so the stability of investments will depend on: 1. The extent to which return-seeking assets are needed, which depends on funding ratios 2. The volatile composition of the return-seeking portfolio ■ Both imply a potentially unstable situation

Thank you!

- Slides: 10