Indian Financial System Dr Manish Dadhich Financial System

borrowing instruments")

was established in 1988 but")

• Established in October 2003 by")

- Slides: 42

Indian Financial System Dr. Manish Dadhich

Financial System • A financial system is a set of institutions, such as banks, insurance companies, and stock exchanges, that permit the exchange of funds. Financial systems exist on firm, regional, and global levels. • Borrowers, lenders, and investors exchange current funds to finance projects, either for consumption or productive investments, and to pursue a return on their financial assets. • The financial system also includes sets of rules and practices that borrowers and lenders use to decide which projects get financed, who finances projects, and terms of financial deals.

Financial System • According to Prasanna Chandra, • “financial system consists of a variety of institutions, markets, and instruments related in a systematic manner and provide the principal means by which savings are transformed into investments”. �A Financial System is a composition of various institutions, markets, regulations and laws, practices, money manager, analysts, transactions and claims and liabilities

Financial System �Financial System: An institutional framework existing in a country to enable financial transactions. � Three main parts: 1. Financial assets (loans, deposits, bonds, equities, etc. ) 2. Financial institutions (banks, mutual funds, insurance companies, etc. ) 3. Financial markets (money market, capital market, forex market, etc. ) �Regulation is another aspect of the financial system (RBI, SEBI, IRDA, FMC) �Payment and Settlement System Plays a crucial role in it.

INTRODUCTION TO INDIAN FINANCIAL SYSTEM �The financial system plays an important role in promoting economic growth not only by channeling savings into investments but also by improving allocative efficiency of resources. �The recent empirical evidence, in fact, suggests that financial system contributes to economic growth more by improving the allocative efficiency of resources than by channeling of resources from savers to investors. An efficient financial system is now regarded as a necessary pre-condition for growth

Functions of Financial System in India 1. Liquidity function 2. Payment function 3. Saving function 4. Risk function 5. Transfer function 6. Reformatory functions 7 Allocation of Funds:

1. Liquidity function • The most important function of a financial system is to provide money and monetary assets for the production of goods and services. Monetary assets are those assets which can be converted into cash or money easily without loss of value. All activities in a financial system are related to the liquidity-either provision of liquidity or trading in liquidity.

2. Payment function • The financial system offers a very convenient mode of payment for goods and services. The cheque system and credit card system are the easiest methods of payment in the economy. The cost and time of transactions are considerably reduced.

3. Saving function • An important function of a financial system is to mobilize savings and channelize them into productive activities. It is through the financial system the savings are transformed into investments.

4. Risk function • The financial markets provide protection against life, health, and income risks. These guarantees are accomplished through the sale of life, health insurance, and property insurance policies.

5. Transfer function • A financial system provides a mechanism for the transfer of resources across geographic boundaries.

6. Reformatory functions • A financial system undertaking the functions of developing, introducing innovative financial assets/instruments services and practices and restructuring the existing assets, services, etc, to cater to the emerging needs of borrowers and investors.

7 Allocation of Funds: • In the allocative functions of financial institutions lies their main source of power. By granting easy and cheap credit to particular firms, they can shift outward the resource constraint of these firms and make them grow faster. • On the other hand, by denying adequate credit on reasonable terms to other firms, financial institutions can restrict the growth or even normal working of these other firms substantially.

Objective of Financial System 1. Financial system provides payment system to the country. 2. Financial system gives time value money. 3. it compensates risk-taking for desirable action. 4. it ensures regular and adequate supply of funds. 5. To ensure safety on investment.

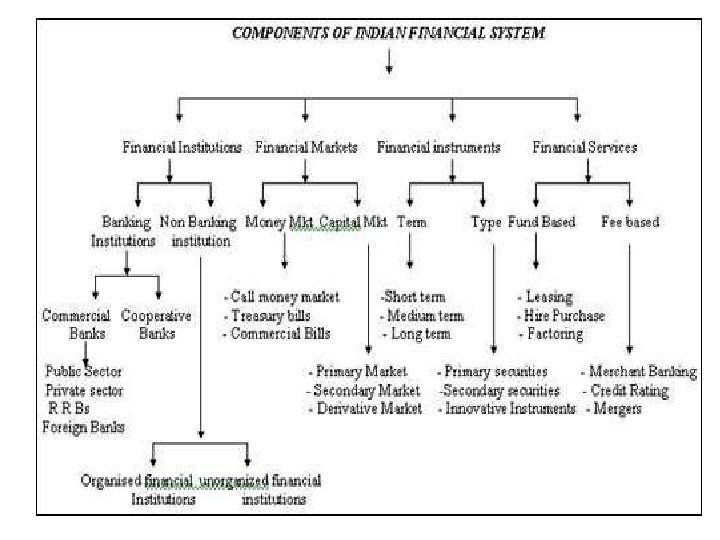

Overview of Indian Financial System • The financial system of a country is an important tool for economic development of the country as it helps in the creation of wealth by linking savings with investments. It facilitates the flow of funds from the households (savers) to business firms (investors) to aid in wealth creation and development of both the parties. • The institutional arrangements include all condition and mechanism governing the production, distribution, exchange and holding of financial assets or instruments of all kinds.

Overview of Indian Financial System • There are four main constituents of the financial system as follows: • Financial Services • Financial Assets/Instruments • Financial Markets • Financial Intermediaries

1. Financial Services • Financial Services is concerned with the design and delivery of financial instruments, advisory services to individuals and businesses within the area of banking and related institutions, personal financial planning, leasing, investment, assets, insurance etc. These services include:

Financial Services • Banking Services: Includes all the operations provided by the banks including to the simple deposit and withdrawal of money to the issue of loans, credit cards etc. • Foreign Exchange services: Includes the currency exchange, foreign exchange banking or the wire transfer.

Financial Services • Investment Services: It generally includes the asset management, hedge fund management and the custody services. • Insurance Services: It deals with the selling of insurance policies, brokerages, insurance underwriting or the reinsurance. • Some of the other services include advisory services, venture capital, angel investment etc.

2. Financial Instruments/Assets • Financial Instruments can be defined as a market for short-term money and financial assets that is a substitute for money. The term short-term means generally a period of one year substitutes for money is used to denote any financial asset which can be quickly converted into money. Some of the important instruments are as follows:

a. Call/Notice money • Call/Notice money is the money borrowed on demand for a very short period. When money is lent for a day it is known as Call Money. Intervening holidays and Sunday are excluded for this purpose. • Thus money borrowed on a day and repaid on the next working day is Call Money. When the money is borrowed or lent for more than a day up to 14 days it is called Notice Money. No collateral security is required to cover these transactions.

b. Treasury Bills • Treasury Bills are short-term (up to one year) borrowing instruments of the union government. It’s a promise by the Government to pay the stated sum after the expiry of the stated period from the date of issue (less than one year). They are issued at a discount off the face value and on maturity, the face value is paid to the holder.

c. Certificates of Deposits • Certificates of Deposits is a money market instrument issued in dematerialised form or as a Promissory Note for funds deposited at a bank, other eligible financial institution for a specified period.

d. Commercial Paper • CP is a note in evidence of the debt obligation of the issuer. On issuing commercial paper the debt is transformed into an instrument. CP is an unsecured promissory note privately placed with investors at a discount rate of face value determined by market forces.

3. Financial Markets • The financial markets are classified into two groups: a. Capital Market: b. Money Market

a. Capital Market: • A capital market is an organised market which provides long-term finance for business. Capital Market also refers to the facilities and institutional arrangements for borrowing and lending long-term funds. Capital Market is divided into three groups:

A. Corporate Securities Market: Corporate securities are equity and preference shares, debentures and bonds of companies. The corporate security market is a very sensitive and active market. It can be divided into two groups: primary and secondary. B. Government Securities Market: In this market government securities are bought and sold. The securities are issued in the form of bonds and credit notes. The buyers of such securities are Banks, Insurance Companies, Provident funds, RBI and Individuals. C. Long-Term Loans Market: Banks and Financial institutions that provide long-term loans to firms for modernization, expansion and diversification of business.

b. Money Market • Money Market is the market for short-term funds. The money market is divided into two types: Unorganised and Organised Money Market. • Unorganized Market: It consists of Moneylenders, Indigenous Bankers, Chit Funds, etc. • Organized Money Market: It consists of Treasury Bills, Commercial Paper, Certificate Of Deposit, Call Money Market and Commercial Bill Market. Organised Markets work as per the rules and regulations of RBI controls the Organized Financial Market in India.

Classification on the basis of seasoning of claim 1. Primary markets • Primary markets are those markets which deal in the new securities. • Therefore, they are also known as new issue markets. • These are markets where securities are issued for the first time. 2. Secondary market • Secondary markets are those markets which deal in existing securities. • Existing securities are those securities that have already been issued and are already outstanding. • Secondary market consists of stock exchanges.

Classification on the basis of timing of delivery 1. Cash/spot market • This is the market where the buying and selling of commodities happens or stocks are sold for cash and delivered immediately after the purchase or sale of commodities or securities. 2. Forward/future market • This is the market where participants buy and sell stocks/commodities, contracts and the delivery of commodities or securities occurs at a pre- determined time in future.

Other types of financial market: 1. Foreign exchange market: Foreign exchange market is simply defined as a market in which one country’s currency is traded for another country’s currency. It is a market for the purchase and sale of foreign currencies. 2. Derivatives market: The derivatives are most modern financial instruments in hedging risk. The individuals and firms who wish to avoid or reduce risk can deal with the others who are willing to accept the risk for a price. A common place where such transactions take place is called the derivative market.

4. Financial Intermediaries • A financial intermediary is an institution which connects the deficit and surplus money. The best example of an intermediary is a bank which transforms the bank deposits to bank loans. • The role of the financial intermediary is to distribute funds from people who have an extra inflow of money to those who don’t have enough money to fulfil the needs. Functions of Financial Intermediary are as follows:

4. Financial Intermediaries • Maturity transformation: Deals with the conversion of short-term liabilities to longterm assets. • Risk transformation: Conversion of risky investments into relatively risk-free ones. • Convenience denomination: It is a way of matching small deposits with large loans and large deposits with small loans.

Regulatory System of Financial intermediaries

1. RBI • After its nationalization in 1949, RBI is presently owned by the Govt. of India. It has 19 regional offices, majorly in state capitals, and 9 sub-offices. It is the issuer of the Indian Rupee. RBI regulates the banking and financial system of the country by issuing broad guidelines and instructions. Role of RBI • Control money supply • Monitor key indicators like GDP and inflation • Maintain people’s confidence in the banking and financial system by providing tools such as ‘Ombudsman’ • Formulate monetary policies such as inflation control, bank credit and interest rate control

2. SEBI • Securities Exchange Board of India (SEBI) was established in 1988 but got legal status in 1992 to regulate the functions of securities market to keep a check on malpractices and protect the investors. Headquartered in Mumbai, SEBI has its regional offices in New Delhi, Kolkata, Chennai and Ahmedabad. • Role of SEBI • Protect the interests of investors through proper education and guidance • Regulate and control the business on stock exchanges and other security markets • Stop fraud in capital market • Audit the performance of stock market

3. IRDAI • IRDAI is an autonomous apex statutory body for regulating and developing the insurance industry in India. It was established in 1999 through an act passed by the Indian Parliament. Headquartered in Hyderabad, Telangana, IRDA regulates and promotes insurance business in India.

4. Pension Fund Regulatory and Development Authority (PFRDA) • Established in October 2003 by the Government of India, PFRDA develops and regulates the pension sector in India. The National Pension System (NPS) was launched in January 2004 with an aim to provide retirement income to all the citizens. The objective of NPS is to set up pension reforms and inculcate the habit of saving for retirement amongst the citizens.

Intermediaries Type of Market Example of institutions Role Performed Stock Exchanges Capital Market NSE, BSE, Calcutta Stock Exchange, Secondary markets to Cochin stock exchange etc. securities Investment Bankers Capital Market, Credit Market Underwriters Capital Market, Money Market Registrars, Depositories, Custodians Capital Market Commercial banks, cooperative banks Corporate advisory services, Issue of services Development banks, NBFC Subscribe to unsubscribed portion of securities Insurance companies, mutual fund Issuance of securities companies, and so on. to the investors on behalf of the company. Handle share transfer activity. Primary Dealers Satellite Dealers Money Market Forex Dealers Registered entities, commercial banks The market making in and their subsidiaries which have the government securities. license to purchase and sell government securities like SBI. Foreign Exchange Western Union Ensure exchange link Market currencies