INDIA AHOY STEEL SECTOR World Steel Industry Top

")

HISTORIC TRENDS 58 m. T in 2008 1. 25")

CAGR – 7. 0%")

Year Per Capita Steel")

- Slides: 52

INDIA AHOY!!!!!

STEEL SECTOR

World Steel Industry – Top Ten 8 4 7 Germany Russia 45. 8 m. T 68. 5 m. T 1 Ukraine 38. 6 m. T China 502 m. T 2 10 Japan 118. 7 m. T Italy 30. 6 m. T USA 91. 4 m. T S. Korea 53. 6 m. T India 3 6 58. 1 m. T 5 Brazil 33. 7 m. T 9 Global crude steel Production: 1326. 5 million tonnes (m. T) Source: IISI

Global ranking of Indian steel

Indian Steel Industry

Supply With trade barriers having been lowered over the years, imports play an important role in the domestic markets. Demand The demand is derived from sectors that include infrastructure, consumer durables and automobiles. Barriers to entry High capital costs, technology. Bargaining power of suppliers The government’s move on railway freight costs and grid power costs would determine the final price of the metal. Bargaining power of customers High, presence of a large number of suppliers and access to global markets. Competition High, presence of a large number of players in the unorganized sector.

Indian Potential for Steel Huge Potential for Demand • High GDP growth rate of 7% • 1 billion population • Low per capita steel consumption of 33 kg (World av. 181 kg) Skilled Human Resources Growth factors for India Abundant Iron Ore Reserves 23 billion tonnes Government Policy • Stable currency • Easing of regulations • Strong Banking & judicial system • Encouraging trade relations with ASEAN and other countries • Infrastructure building • Exploring new Energy resources

Indian Steel Industry – An Overview Ø Fifth largest producer of steel in the world and second largest producer of crude steel - Press Information Bureau Ø Steel production reached 28. 49 million tonne (MT) in April. September 2009. Ø About 50% of the steel produced in India is exported. Ø India accounts for over 7% of the total steel produced globally Ø India accounts for around 5 per cent of the global steel consumption Ø Huge Iron Ore reserves – 23 bn. tonnes Ø Indian Steel Producers are increasingly looking for overseas acquisitions in steel as well as raw materials. Ø Positive overall growth in the production of crude steel

Composition of Steel Production -A Value Proposition HR Quantity %age Long Prods. 13. 928 42% HR 7. 254 22% Plates 1. 832 5% CR 2. 251 7% GP 4. 790 14% Pipes 3. 616 11% Total 33. 670 100%

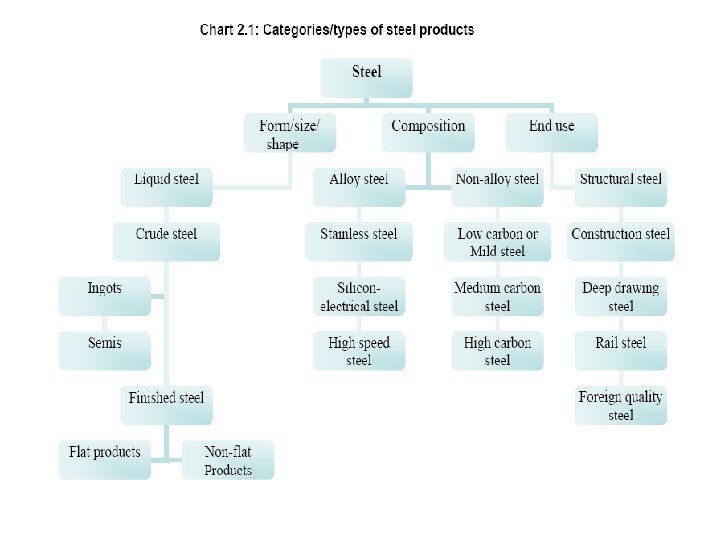

Steel - Products

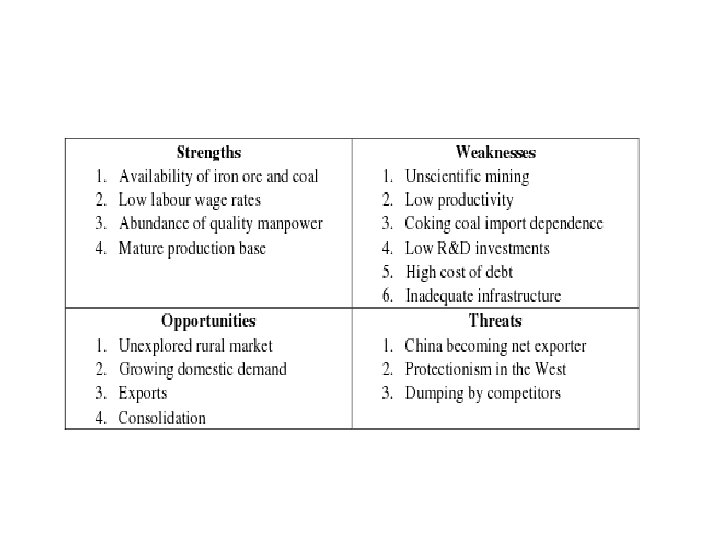

Indian Steel Industry SWOT Analysis

SWOT ANALYSIS OF INDIAN STEEL INDUSTRY STRENGTHS WEAKNESSES • Abundant resources of iron ore • High cost of energy • Low cost and efficient labour force • Higher duties and taxes • Strong managerial capability • Infrastructure • Quality of coking coal • Strongly globalised industry and emerging global competitiveness • Labour laws • Modern new plants & modernised old plants • Dependence on imports for steel manufacturing equipments & technology • Strong DRI production base • Regionally dispersed merchant rolling mills • Slow statutory clearances for development of mines

SWOT ANALYSIS OF INDIAN STEEL INDUSTRY OPPORTUNITIES • Huge Infrastructure demand • Rapid urbanisation • Increasing demand for consumer durables • Untapped rural demand • Increasing interest of foreign steel producers in India THREATS • Slow growth in infrastructure development • Market fluctuations and China’s export possibilities • Global economic slow down

Michael Porters Five Forces Analysis Buyers’ Power • Increasing Demand for Steel • Fragmented Coke Suppliers’ Power • High Raw Material Prices • Lack of Captive Source Hurting Steel Producers • Lack of Transportation • Backward Integration Intensity of Competition • Competition from Foreign Players • Spurt in Merger and Acquisition Activities Threat of New Entrants • High Cost of Basic Inputs and Services Threat of Substitutes • Use of Aluminum/Plastic

PEST Analysis Political Factors • Recommendations on Captive Mines • National Steel Policy to Remove Bottlenecks Economic Factors • GDP Growth Rate • Reduction in Customs Duty Social Factors • Rural-Urban Divide • Higher Disposable Income Technological Factors • Popularity of Steel Portals • Application of SML (Steel Markup Language)

Top 10 Players • • • 1 st; 103. 3 mmt; Arcelor. Mittal 2 nd; 37. 5 mmt; Nippon Steel 3 rd; 35. 4 mmt; Baosteel Group 4 th; 34. 7 mmt; POSCO 5 th; 33. 3 mmt; Hebei Steel Group 6 th; 33. 0 mmt; JFE 7 th; 27. 7 mmt; Wuhan Steel Group 8 th; 24. 4 mmt; Tata Steel 9 th; 23. 3 mmt; Jiangsu Shagang Group 10 th; 23. 2 mmt; U. S. Steel Source: World Steel Association

Arcelor. Mittal • largest steel company, with 315, 867 employees in more than 60 countries. • formed in 2006 by the merger of Arcelor and Mittal Steel. ($38. 3 billion ) • It ranks 28 th on the 2009 Fortune Global 500 list. • the market leader in steel for use in automotive, construction, household appliances and packaging. • Arcelor. Mittal is looking to develop positions in the high-growth Indian and Chinese markets.

MAJOR PLAYER - SAIL • fully integrated iron and steel maker. • GOI - 86% of SAIL's equity • However, SAIL, by virtue of its "Navratna" status, enjoys significant operational and financial autonomy. • SAIL and TISCO (which enjoy the benfits of captive ore mines) are among the lowest cost producers of steel in the world.

Major units of SAIL are as under: . Integrated Steel Plants • Bhilai Steel Plant (BSP) in Chhattisgarh • Durgapur Steel Plant (DSP) in West Bengal • Rourkela Steel Plant (RSP) in Orissa • Bokaro Steel Plant (BSL) in Jharkhand Special Steel Plants • Alloy Steels Plants (ASP) in West Bengal • Salem Steel Plant (SSP) in Tamil Nadu • Visvesvaraya Iron and Steel Plant (VISL) in Karnataka Subsidiaries • Indian Iron and Steel Company (IISCO) in West Bengal • Maharashtra Elektrosmelt Limited (MEL) in Maharashtra • Bhilai Oxygen Limited (BOL) in New Delhi

SAIL’S GROWTH PLANS m. T 2005 -06 2011 -12 Hot Metal 14. 60 22. 5 Crude Steel 13. 47 21. 6 Saleable Steel 12. 05 20 - Planned Investments of US$ 7. 7 bn. - Includes only growth in existing Units

Other Major steel producers • • • Tisco JSW Essar Steel RINL MECON MOIL MSTC KIOCL NMDC

TATA STEEL LIMITED • • • Tisco -1907 country's single largest Integrated steel plant ranks 34 th in the world Technical collaboration with Nippon Steel & Arcelor • In January 2007 Tata Steel made a successful $11. 3 billion offer to buy European steel maker Corus Group PLC.

STEEL SECTOR TRENDS • India - world’s largest producer of direct reduced iron (DRI) or sponge iron with nearly 20 million tonnes production in 2008 -09. • Estimated steel production capacity -124 million tonnes by the year 2011 -12. • Generate additional employment of around 4 million by 2020 for production of around 295 million tonnes of crude steel by 2019 -2020. • 222 Mo. Us have been signed with various States for planned capacity of around 276 million tonnes

Steel: Key facts

Performance of PSUs

Production, consumption and growth of steel

Crude steel production

Trends in production, private/public sector

Turnaround in Industrial Activity Services Industry Agriculture Services and Industry contribute to higher GDP growth

Indian Steel Growth Co nf id en ce -Slowly, Steadily l Stagnatio n ro t on c De Controlled Regime 1951 1991 2005

Proof of the Pudding !

Booming Capital Market Indicators 2003 -04 2004 -05 2005 -06 BSE Index as on March 31 5591 6493 11280 Market Capitalisation as on March 31 (US$ bn. ) 266. 8 377. 33 671. 5 Foreign Institutional Investors Net Purchases in Equity market (US$ bn. ) 6. 7 8. 65 10. 4 (For Calendar Year)

Other Key Indicators v Exports crossed US$100 bn. mark in 2005 -06. Fourth consecutive year of more than 20% exports growth v Imports of Capital goods increasing v Moderate inflation rate - within 4 -5% v Stable Rupee against US dollar v Growing corporate sector profits v Growing Forex reserves - US$ 160 bn. v Business Confidence at all time high

Steel Sector The Back Seat Drivers!

BOOMING STEEL CONSUMING SECTORS Capital Goods Construction Manufacturing Consumer Durables Industrial growth led by Manufacturing Capital and Consumer Goods sectors flag bearers of manufacturing sector growth

INDIA’S CRUDE STEEL PRODUCTION (MT) HISTORIC TRENDS 58 m. T in 2008 1. 25 m. T in 1948 India gains independence in 1947 GH I H ES OD M SLOW TH GROW * Year indicates FY TH 16. 2 m. T in 1991 6. 6 m. T in 1973 T OW R G H WT O GR Enabled by India’s Economic liberalization process

Apparent Finished Steel Consumption (m. T) CAGR – 7. 0%

National Steel Policy Addressing the Weaknesses & Harnessing the Opportunities Approved by Government of India in September 2005

OBJECTIVE v To have modern and efficient steel industry of world standards, catering to diversified steel demand. v To achieve global competitiveness in cost, quality, productmix, efficiency and productivity v To attain Finished Steel production of 110 m. Tpa by 2019 -20 Production Imports Exports Consumption 2019 -20 110 6 26 90 CAGR (Base – 08 -09) 7. 3% 7. 1% 13. 3% 6. 9%

STRATEGY v Demand Side – Strengthening of delivery chain – Interface between producers, designers of steel intensive products, fabricators and ultimate user – Creating awareness about cost-effective and technically efficient end-use of steel v. Supply side – Enhanced and easy access to critical inputs – iron ore & coking coal – Expansion and improvement in quality of infrastructure – Well developed financial market – Increased focus on R&D, training of manpower and integrated information services

New Capacities

Proposed state-wise capacity additions upto 2012. J’khand: 34 mtpa W Bengal: 4 mtpa Ch’garh: 9 mtpa Orissa : 38 mtpa AP: 3. 3 mtpa Karnataka: 9. 7 mtpa SAIL Tata Steel RINL Essar Bhushan JSPL JSW Ispat Sterlite Mittal POSCO MMK

Future of Indian Steel Industry You ain’t seen nothing yet !

Projected per Capita consumption of Finished Steel in India (kg) Year Per Capita Steel Consumption 2011 -12 48 2019 -20 80 2024 -25 110 2029 -30 135 2034 -35 175 India’s current population is - 1100 million It is assumed that till 2051, population would be about : 1. 4 bn.

GROWTH SCENARIOS Optimistic Case Medium Growth Conservative Fin. Steel Cons. Growth Rate Consum- Fin. Steel ption Cons. Growth (m. Tpa) Rate Consumption (m. Tpa) Fin. Steel Cons. Growth Rate Consumption (m. Tpa) 20052020 7. 6% 100 6. 9% 90 * 5. 5% 76 20202030 6. 5% 188 5. 5% 147 4. 5% 118 20302040 5. 0% 305 4. 0% 217 3% 158 20402050 5. 0% 498 4. 0% 322 3% 212 * - Also projected by National Steel Policy

INDIAN STEEL INDUSTRY A BRIGHT FUTURE RESOURCES Abundant Iron Ore reserves Strong Managerial skills in Iron and Steel making Large pool of skilled Man-power Established steel players with strong skills in steel making OPPORTUNITIES High economic growth driven increasingly by industry Faster Urbanisation Increased Fixed Asset Building Automobiles and component industry growth POLICY Pro-active stance of Govt. Encouragement for overseas investments

• Currently with a production of 56 million tones India accounts for over 7% of the total steel produced globally, while it accounts to about 5% of global steel consumption. • The steel sector in India grew by 5. 3% in May 2009. Globally India is the only country to post a positive overall growth in the production of crude steel at 1. 01% for the period of January – March in 2009.

Highlights of 2008 -09 • Crude steel production was at 54. 52 million tonnes, a growth of 1. 23% over last year with capacity utilisation at 89% during the year. It grew at more than 9% annually from 38. 72 million tonnes (MT) in 2003 -04. • The growth was driven by capacity expansion from 43. 91 million tonnes per annum (MTPA) in 2003 -04 to 64. 40 MTPA in 2008 -09.

Financial Year '09 • • • first half it experienced an extraordinary spurt in demand backed by expansion of key consumer sectors. second half experienced a significant demand contraction on account of the global financial crisis. Thus overall, India’s crude steel production grew by 1. 2%Yo. Y to 54. 5 MT. • The various monetary and fiscal packages announced by the government helped the domestic steel industry to counter the slowdown and thus the demand started reviving upwards from the fourth quarter onwards. • Domestic steel prices and international steel prices experienced a divergent trend in FY 09. While during the first half, international prices touched an all time high levels backed by robust demand, the second half witnessed more than 50% fall in the prices on account of significant contraction in demand due to the global credit crisis. Raw material prices like iron ore and coking coal also experienced a similar trend. It may be noted that most of the domestic steel players entered into an annual contract for coking coal in June-July 2009 when prices were at their peak. Hence the industry experienced a severe pressure on the margins.