IAS 19 Employee Benefits 13 April 2011 IAS

IAS 19 Employee Benefits 13 April, 2011 陳蓓琪, 執業會計師

IAS 19 課程大綱 • 適用IAS 19的範圍 • 員 福利主要內容說明 • 採行IFRS的衝擊及其影響 • 草案修正提案暨實務分享 • Q&A © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 1

之情形外,IAS 19涵括其他所 有員 福利之規範(包括:短期員")

範圍 • 員 福利係指企業以各種形式之對價提供予公司員 、 員 眷屬或其他對象,以換取員 之服務。除適用 IFRS 2 (股份基礎給付)之情形外,IAS 19涵括其他所 有員 福利之規範(包括:短期員 福利、退職後福 利、其他長期員 福利及資遣給付等)。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 3

• 有薪休假給付係依據員 過去所提供之服務且為累積 性質(亦即可累積至未來年度)時,雇主應估列相關休 假給付義務。 © 2011 KPMG, a Taiwan partnership and")

帶薪假 (休假給付) • 有薪休假給付係依據員 過去所提供之服務且為累積 性質(亦即可累積至未來年度)時,雇主應估列相關休 假給付義務。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 4

• 休假給付估列之重點為: 過去所提供之服務,且 可累積至未來年度 衡量方式: 負債金額係企業對員 未使用之休假權利予以估列, 即以資產負債表日,員 剩餘休假天數為依據。 © 2011 KPMG, a")

帶薪假(續) • 休假給付估列之重點為: 過去所提供之服務,且 可累積至未來年度 衡量方式: 負債金額係企業對員 未使用之休假權利予以估列, 即以資產負債表日,員 剩餘休假天數為依據。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 5

• 釋例: – A員 於 2008年 7月1日服務滿一年,故享有7天的休假。截 至 2008年 12月31日,A員 尚有3天休假未休,而依公司政 策此休假可累積至 2009年")

帶薪假-釋例(一) • 釋例: – A員 於 2008年 7月1日服務滿一年,故享有7天的休假。截 至 2008年 12月31日,A員 尚有3天休假未休,而依公司政 策此休假可累積至 2009年 12月31日以前休完即可。 – 依IAS 19之規定,對2008年 12月31日財務報表之影響為何? 選項如下: 1. 2009年認列即可 2. 2008年估列 7天休假給付 3. 2008年估列 3天休假給付 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 6

• 釋例: –產假及陪產假要如何處理? –國定假日休假要如何處理? =>是否要先行估列員 福利? © 2011 KPMG, a Taiwan partnership and")

帶薪假-釋例(二) • 釋例: –產假及陪產假要如何處理? –國定假日休假要如何處理? =>是否要先行估列員 福利? © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 7

Answer 大多數情形下,產假及陪產假係屬或有性質, 取決於未來發生之事件而並非”累積”,所以, 此類成本只於休假發生時才認列。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 8 8

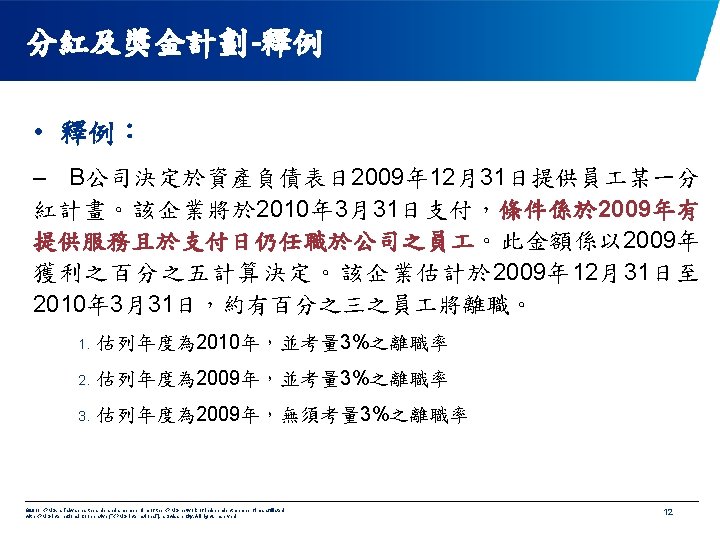

分紅及獎金計劃 • 當企業目前具有法定或推定義務且可合理估計時, 應估列員 分紅及獎金計畫之預期成本。 • 衡量之金額係企業所預期支付金額之最佳估計數。 何謂法定義務及推定義務? © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 9

n 合約 n 法律 / 法令 © 2011 KPMG, a")

法定義務與推定義務 義務 l 法定(legal) n 合約 n 法律 / 法令 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. l 推定constructive n 過去實務 n 公開政策/聲明 n 詳細的現在聲明 n 使他人確切預期企業 將會執行某行動時 10

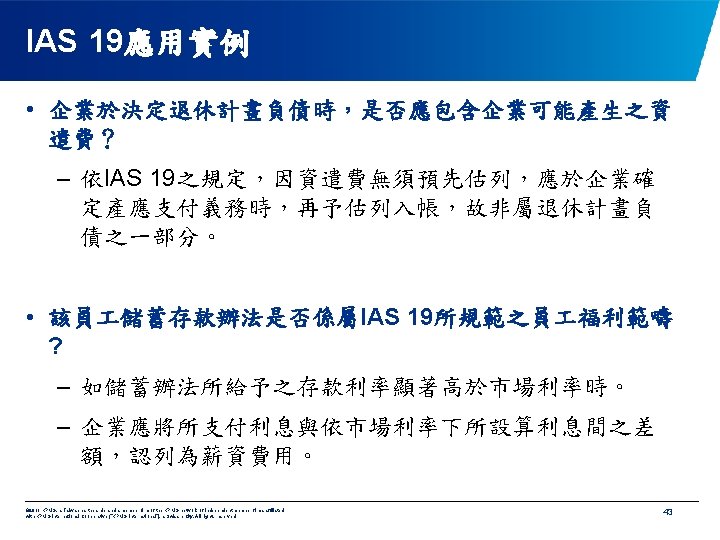

,則於衡量該負債時應予考慮該條件(及放棄 (forfeiture)之可能性)。 © 2011 KPMG, a Taiwan partnership")

衡量 • 衡量之金額係企業所預期支付金額之最佳估計數。 • 假設支付金額附有條件(例如:員 繼續任職提供 服務),則於衡量該負債時應予考慮該條件(及放棄 (forfeiture)之可能性)。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 11

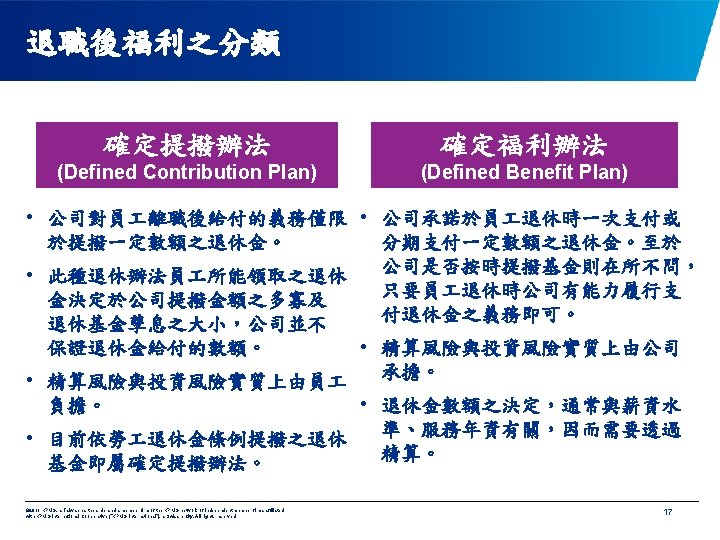

去支付其他任何 金額。 確定福利辦法 其他非屬確定提撥辦法者, 皆屬於確定福利辦法。")

退職後福利之分類 退 職 後 福 利 確定提撥辦法 企業提撥固定金額至某一獨立 個體後,即沒有任何其他義務 (法定或推定)去支付其他任何 金額。 確定福利辦法 其他非屬確定提撥辦法者, 皆屬於確定福利辦法。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 16

確定福利辦法之退休基金資產 • 退休基金資產包含:由法律上獨立之基金所管理之 資產,且: –僅可於支付員 之福利時才可動用 –不得支付雇主之負債,且 –僅於已支付員 福利的退回或此一基金已提列過剩時,才 可將其退回予企業。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 19

確定福利辦法-退休基金資產之衡量 • 退休基金資產應以公平價值衡量。當退休基金資產 有市場公開報價時,根據金融資產公平價值之衡量 規定,應以其公開報價之買價衡量之。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 20

認 列 方 式 若增加給付之 權利無未來服 務條件 該權利為立即既得,企業應 立即全數認列費用並增加負債。 尚未既得 費用應於既得期間內按直線 法分攤認列為費用。 ©")

前期服務成本(續) 認 列 方 式 若增加給付之 權利無未來服 務條件 該權利為立即既得,企業應 立即全數認列費用並增加負債。 尚未既得 費用應於既得期間內按直線 法分攤認列為費用。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 22

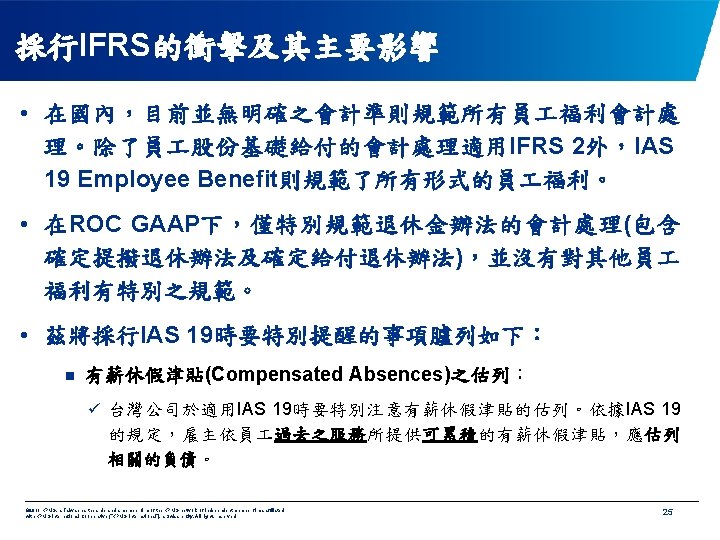

• 確定給付退休金會計處理的差異: 公開發行公司 原已適用財務會計準則公報第 18號 「退休金會計處理準則」予以精算 非公開發行公司 未適用財務會計準則公報第 18號 「退休金會計處理準則」-皆未精算 © 2011 KPMG,")

採行IFRS的衝擊及其影響(續) • 確定給付退休金會計處理的差異: 公開發行公司 原已適用財務會計準則公報第 18號 「退休金會計處理準則」予以精算 非公開發行公司 未適用財務會計準則公報第 18號 「退休金會計處理準則」-皆未精算 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 26

對公開發行公司之衝擊 一、首次適用IAS 19 : 可適用IFRS 1 --累積之精算損益調整至保留盈餘。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 28

二、續後退休金損益變化(精算損益)未攤銷數之會計 處理: 可選擇下列方式進行處理 立即認列於股東權益 或 依緩衝區法或更快的方式 認列於損益表中 在ROC GAAP下,精算損益僅可認列於損益表項下 © 2011 KPMG, a")

對公開發行公司之衝擊(續) 二、續後退休金損益變化(精算損益)未攤銷數之會計 處理: 可選擇下列方式進行處理 立即認列於股東權益 或 依緩衝區法或更快的方式 認列於損益表中 在ROC GAAP下,精算損益僅可認列於損益表項下 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 29

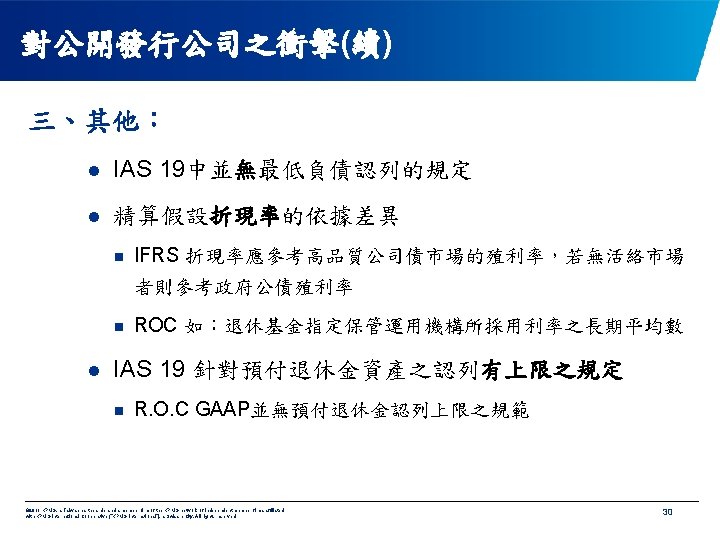

對非公開發行公司之衝擊 • 我國非公開發行公司依經濟部 850228商第 85201058 號規定,迄今,尚未適用財務會計準則公報第 18號 「退休金會計處理準則」。 若與IFRS接軌 對非公開發行公司之 淨退休金成本、退休金負債及淨值 將產生重大之影響! © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 32

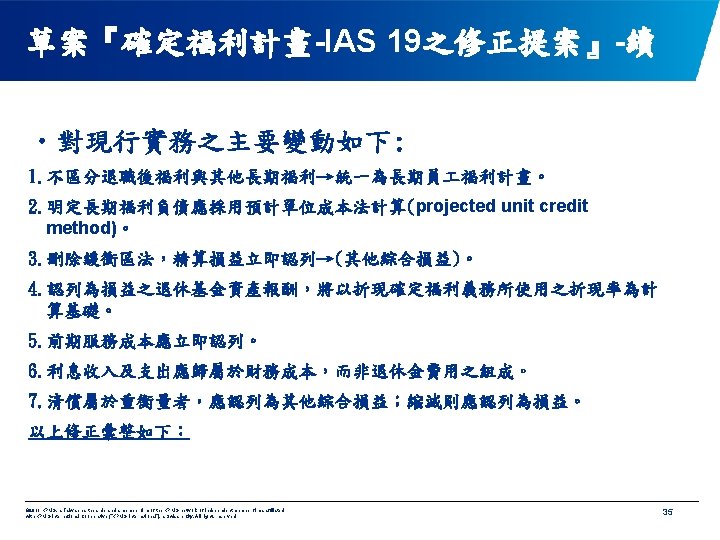

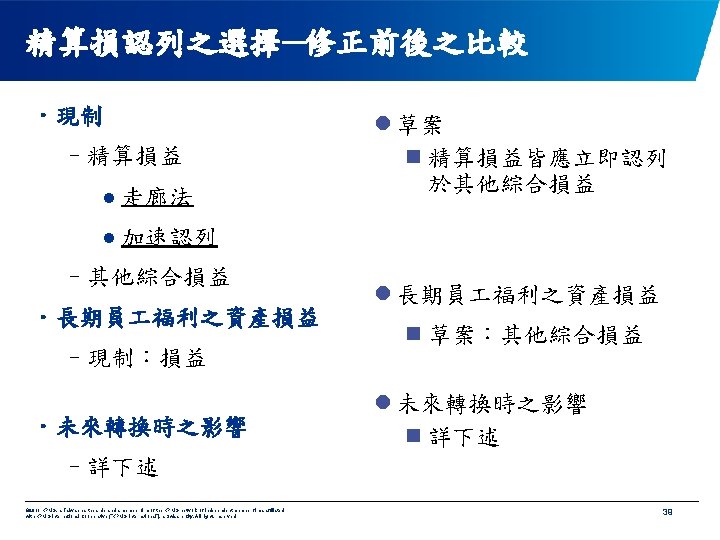

• 修正緣由: 全球金融危機使資產負債表外風險之議題更受關切。 採用緩衝區法認列精算損益之會計處理所產生之表外 退休金負債備受關注。 © 2011 KPMG, a Taiwan partnership and")

草案『確定福利計畫-IAS 19之修正提案』(2010/4/29) • 修正緣由: 全球金融危機使資產負債表外風險之議題更受關切。 採用緩衝區法認列精算損益之會計處理所產生之表外 退休金負債備受關注。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 34

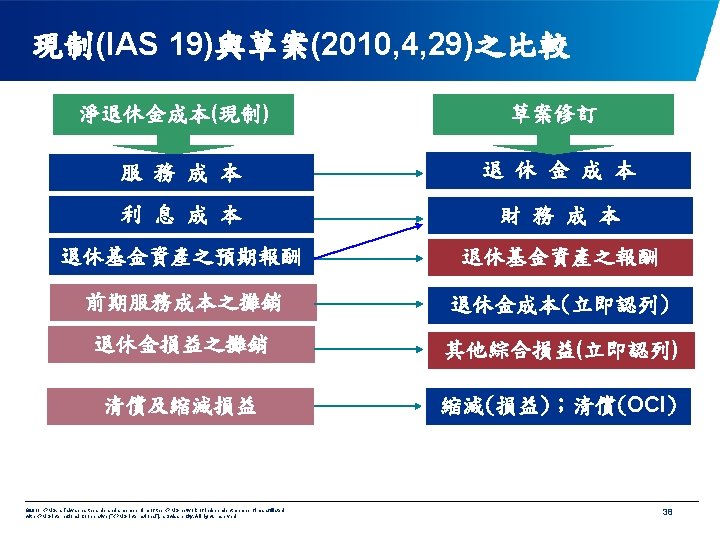

財務成本(損益 ) 重衡量 其他綜合損益 ©")

草案『確定福利計畫-IAS 19之修正提案』-續 服務成本 長期員 福利 計畫 淨利息損益 退休金費用(損 益) 財務成本(損益 ) 重衡量 其他綜合損益 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 36

草案『確定福利計畫-IAS 19之修正提案』-續 • 對企業可能造成之衝擊: 1. 企業獲利層面之影響: ü取消以往可以遞延分年認列退休金成本之方式。 2. 企業財務融資層面之影響: ü重新檢視與金融機構所簽訂之財務融資限制條款,如:獲利 率、負債權益等等。 © 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. 37

Q&A 44

Thank you Presenter’s contact details 陳蓓琪, 執業會計師 安侯建業聯合會計師事務所 +886 2 8101 6666 ext. 02411 peggychen@kpmg. com. tw www. kpmg. com. tw 45

© 2011 KPMG, a Taiwan partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

- Slides: 47