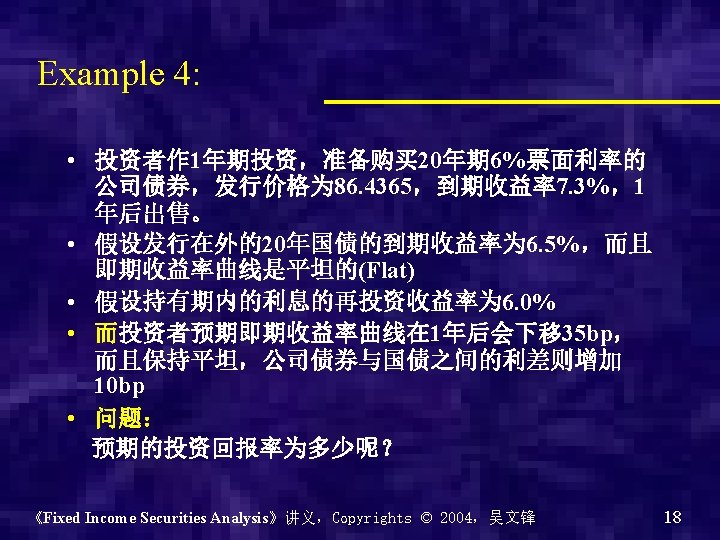

HPR holding period return horizon return total return

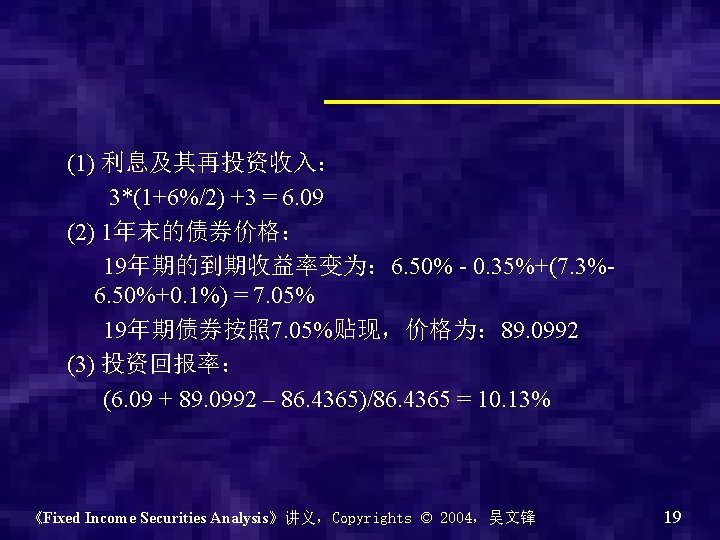

利息及其再投资收入: 到期日 45 45 45 …… 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋")

0. 5年 1年 1. 5年 2年 2. 5年 3年 即期收益率 3. 25%*2 3.")

债券投资风险概述 利息再投资收入 债券投资收入 纯利息收入 资本利得Pn – P 0 Reinvestment* Interest rate* Yield Curve*")

为什么叫 Duration? • 下表为零息券的久期 期限 1年 2年 3年 4年 5年 到期收益率 5% 5%")

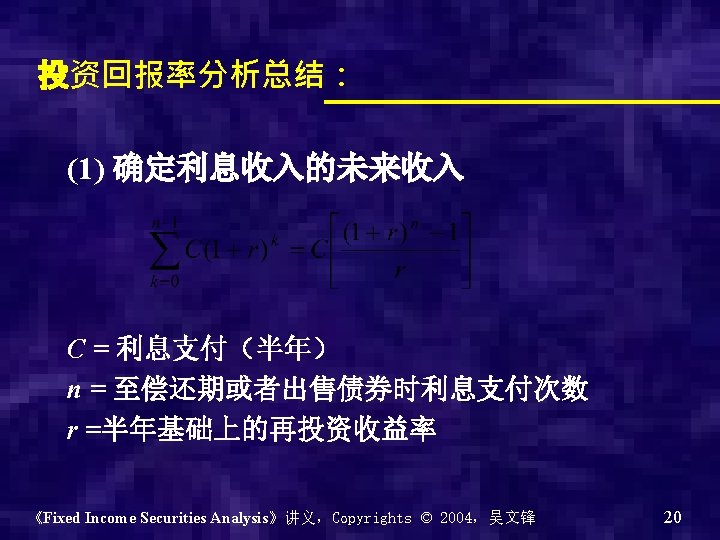

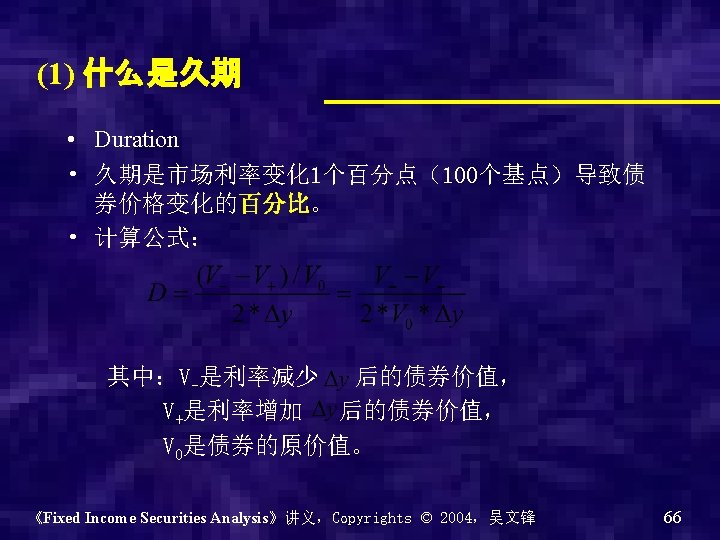

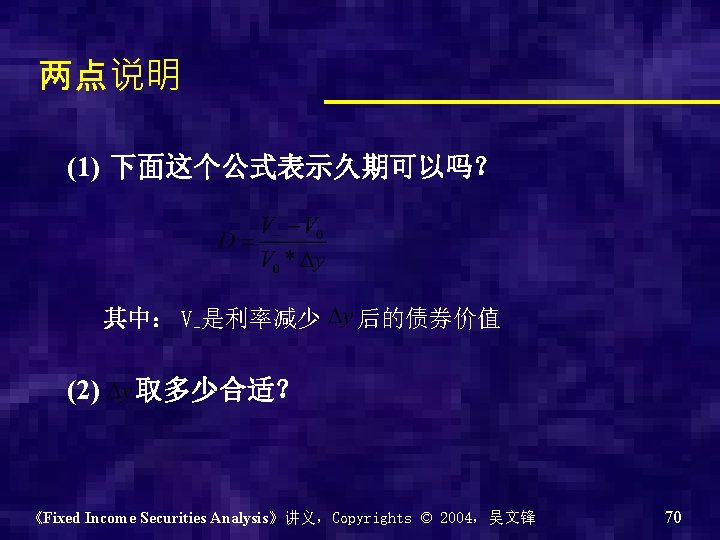

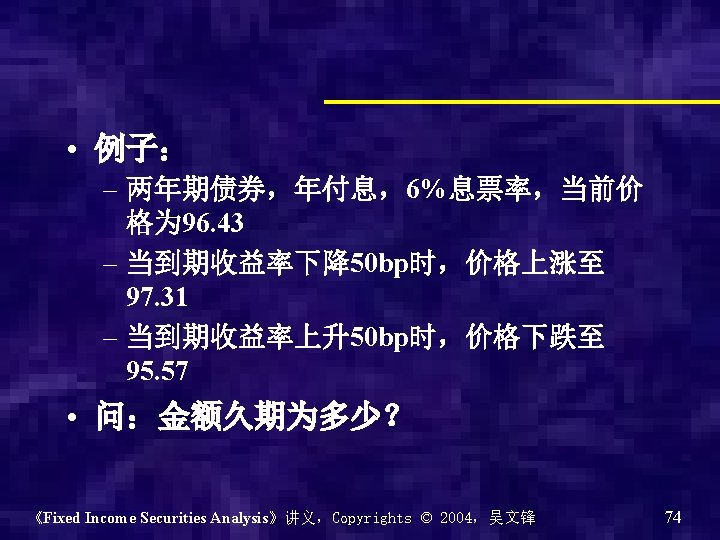

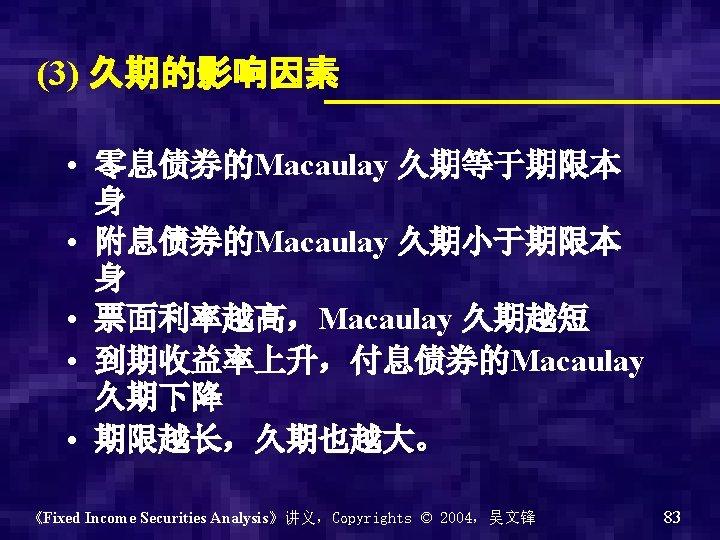

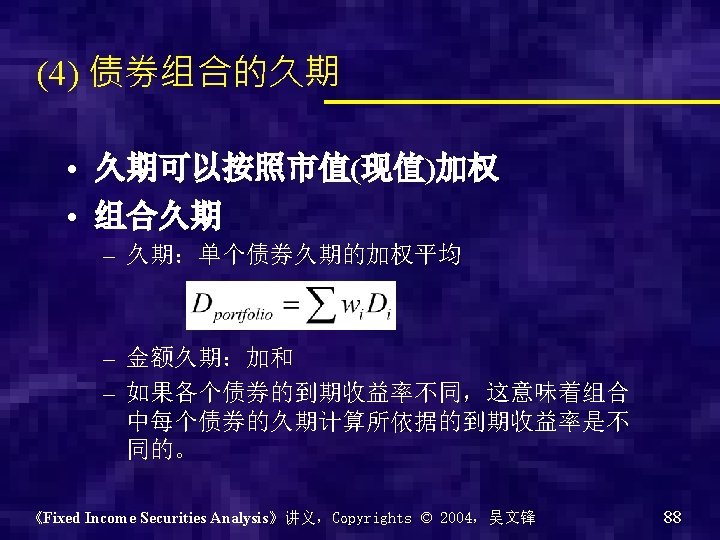

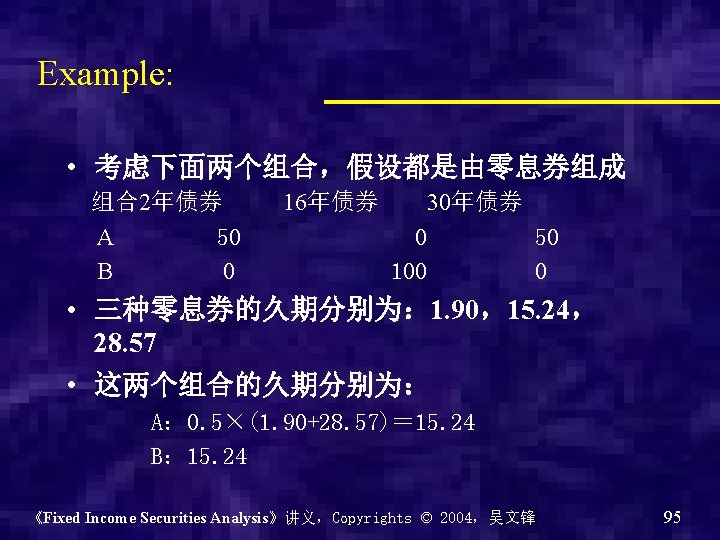

就是:期限的加权平均, 权重为现值。 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋")

D = 10. 87/(1+0. 045) = 10. 40 价格变化: -10.")

凸性的计算,也可以通过久期: 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 115")

- Slides: 120

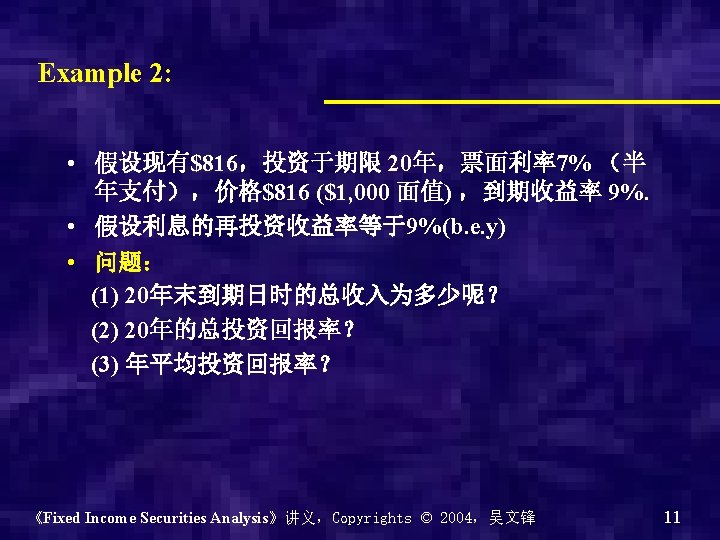

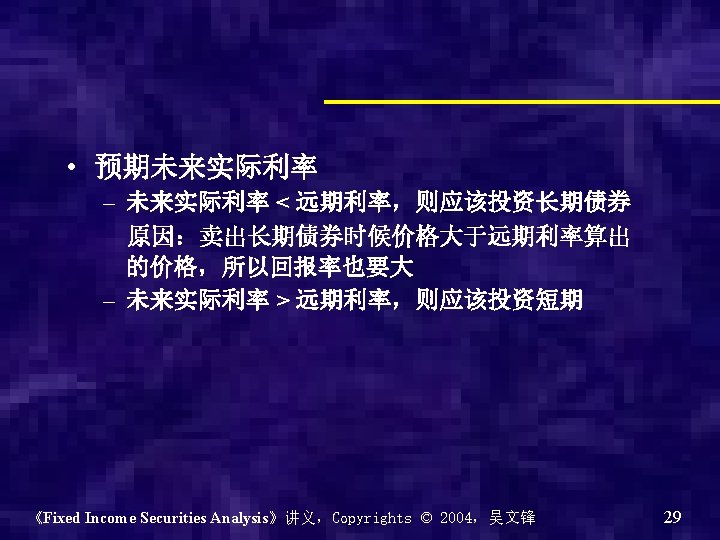

持有收益率和投资回报率 • 持有收益率 HPR – holding period return, horizon return, total return, realized compound yield. – HPR is 债券持有期间的投资收益率 – 其大小取决于债券资本利得与再投资收益。 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 5

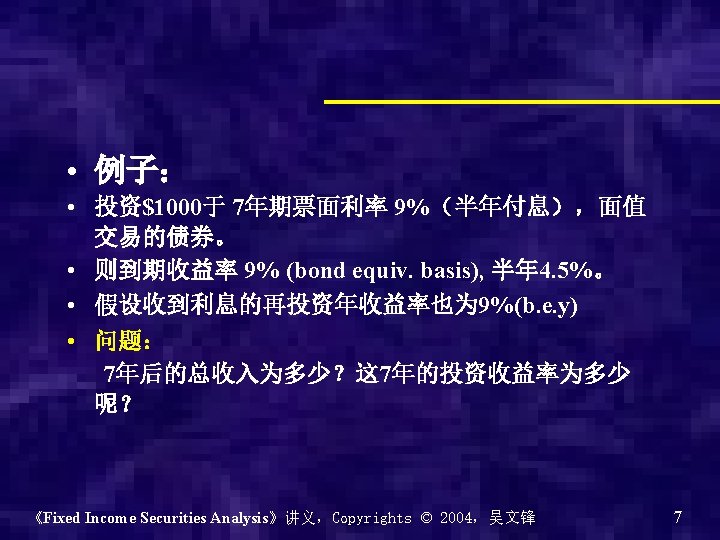

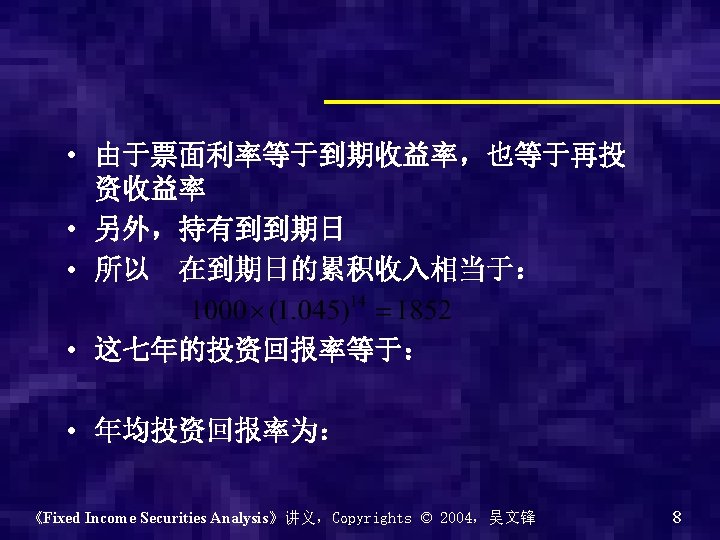

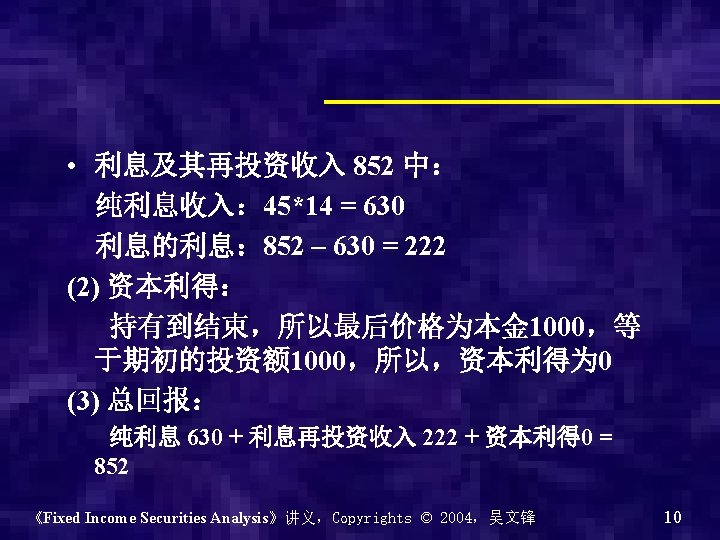

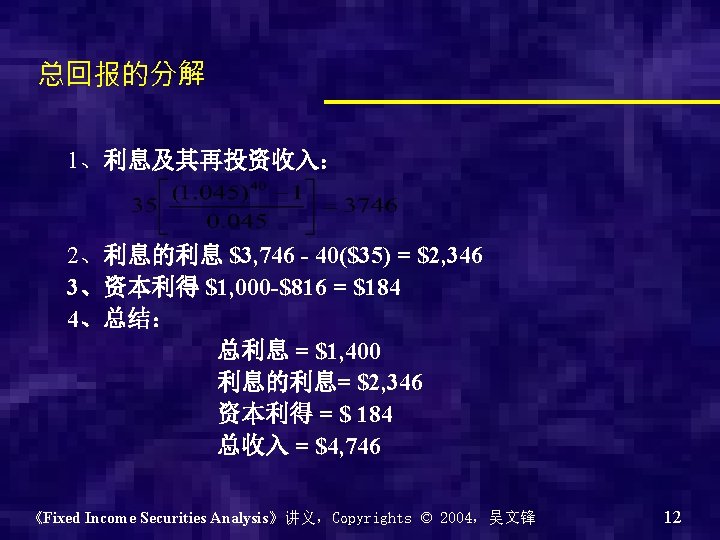

总收入分解 (1) 利息及其再投资收入: 到期日 45 45 45 …… 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 9

t(期限) 0. 5年 1年 1. 5年 2年 2. 5年 3年 即期收益率 3. 25%*2 3. 50%*2 3. 70%*2 4. 00%*2 4. 20%*2 4. 30%*2 单期远期利率f(t-1, t) 3. 25%*2=6. 50% 3. 75%*2 4. 10%*2 4. 91%*2 5. 00%*2 4. 80%*2 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 14

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 15

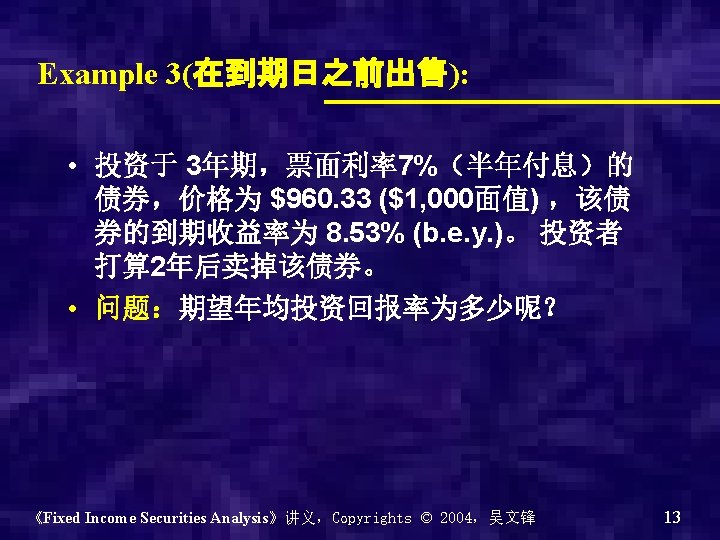

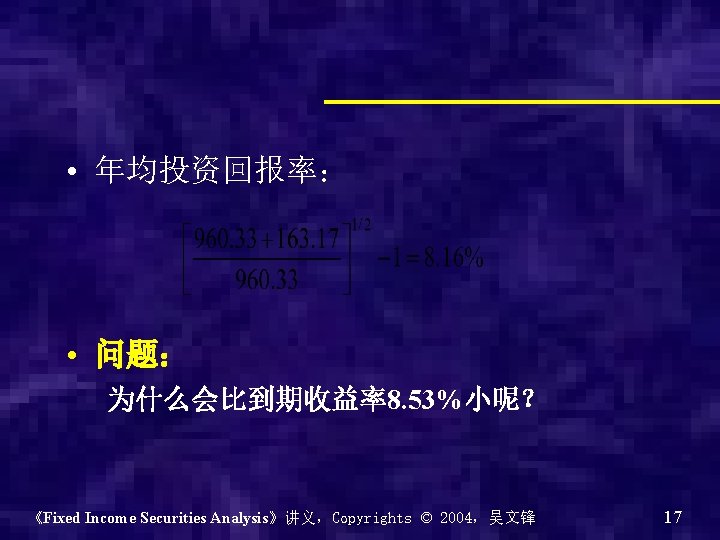

1. 求2年后债券的卖出价格: 所以投资者预期资本利得为: $973. 90 - $960. 33 = $13. 57 2. 求累积利息: $35(1. 0375)(1. 0410)(1. 0491) + $35(1. 0410)(1. 0491) +35(1. 0491) + $35 = $149. 60 3. 总预期回报金额 =$13. 57 + $149. 60 = $163. 17 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 16

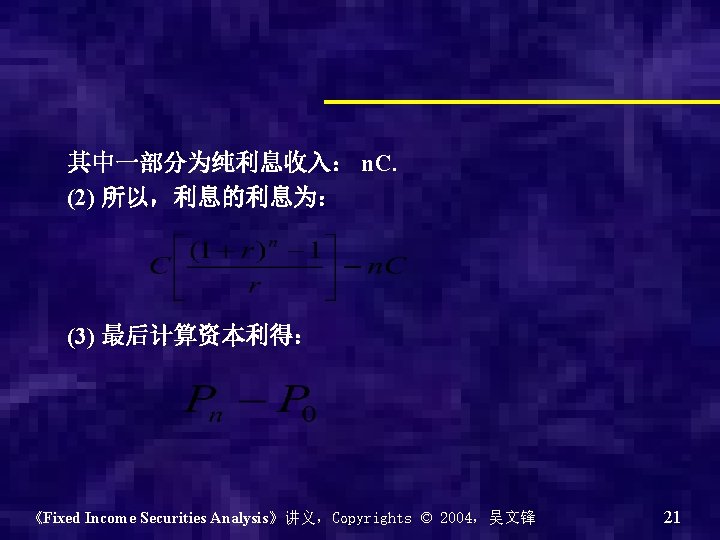

(2) 债券投资风险概述 利息再投资收入 债券投资收入 纯利息收入 资本利得Pn – P 0 Reinvestment* Interest rate* Yield Curve* Credit Spread Liquidity Event Call, Prepayment Exchange rate 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 Inflation Political 22

Reinvestment Risk • This risk is greater for those investors who depend on a bond’s coupon for most of their return • Minimized with low or zero-coupon bond issues or when time horizons are short • 例外: – 如果刚好需要拿利息另有所用的,就不用考虑这 个风险 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 23

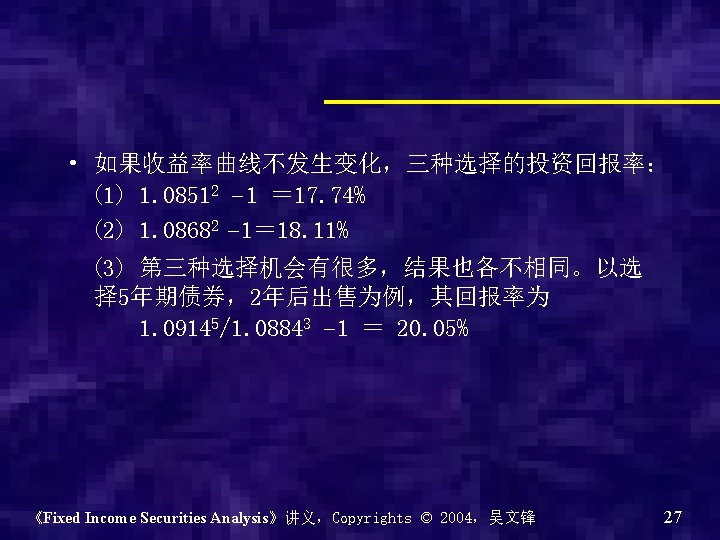

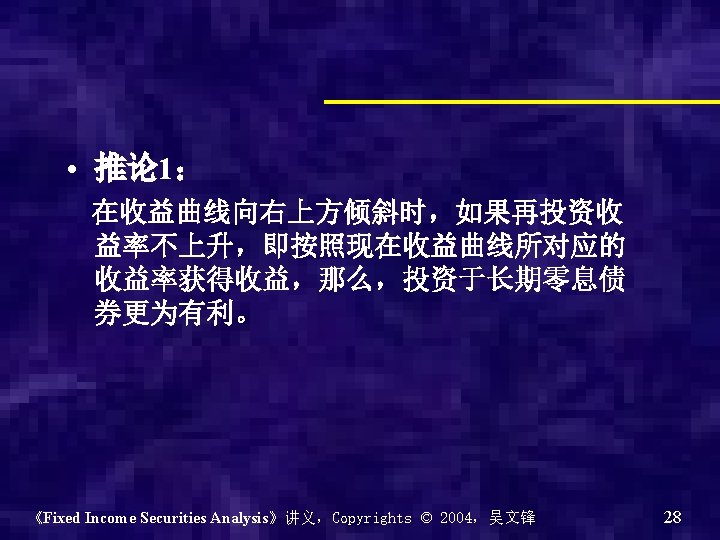

零息票国债的到期收益率 期限 0. 5 1 1. 5 2 2. 5 3 4 5 6 7 8 9 10 11 12 13 14 15 即期利率 8. 42% 0. 9604 8. 51% 8. 59% 0. 8837 8. 68% 8. 76% 0. 8107 8. 84% 8. 99% 9. 14% 9. 28% 9. 41% 9. 54% 9. 66% 9. 77% 9. 87% 9. 97% 10. 05% 10. 13% 10. 21% 折现因子 0. 9216 考虑两种情况: 0. 8467 (1)不对未来收益率曲线做 预测,计算各个选择的预期 收益率 0. 7756 0. 7086 0. 6458 0. 5871 0. 5327 0. 4824 0. 4362 0. 3938 0. 3551 0. 3198 0. 2878 0. 2589 0. 2327 (2)假设收益率曲线 2年内 不发生变化,应如何选择 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 26

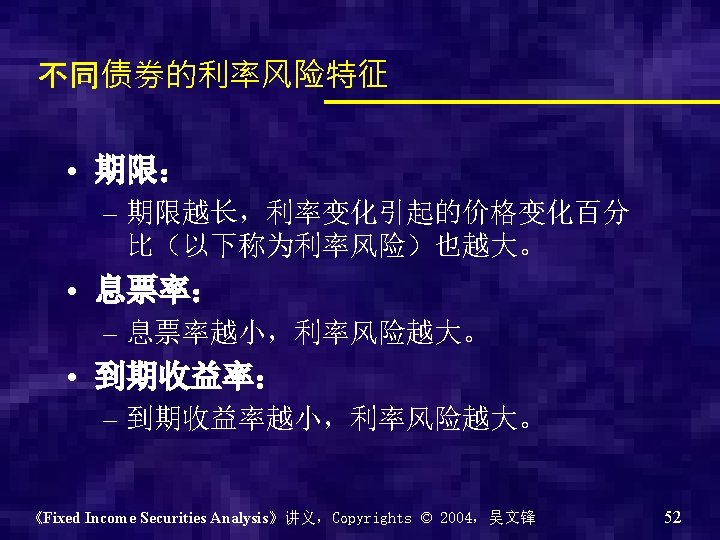

Interest rates Risk • Interest rates and bond prices show inverse relationship – Bondholders lose when the interest rates rise – Bondholders gain when interest rates fall • 例子: – 隔夜风险都很大 – 在美联储开会前的交易平淡 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 31

Yield Curve Risk • Interest rates risk measures when yield curve has a parallel shift • The risks investors face when yield curve changes non-parallelly means yield curve risk. • 几个问题: – 从风险源看,跟利率风险类似 – 但主要是针对认为已经消除利率风险的投资者 – 现金的长短期分配 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 32

Credit Risk 1. Default risk Recovery rate 2. Credit spread risk Yield on risky bond = yield on default-free bond + risk premium 3. Downgrade risk Higher rating (upgrade), lower rating (downgrade) Yields rise for downgrades and fall for upgrades 例子: – 公司债要着重分析这种风险 – 评级机构的影响 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 33

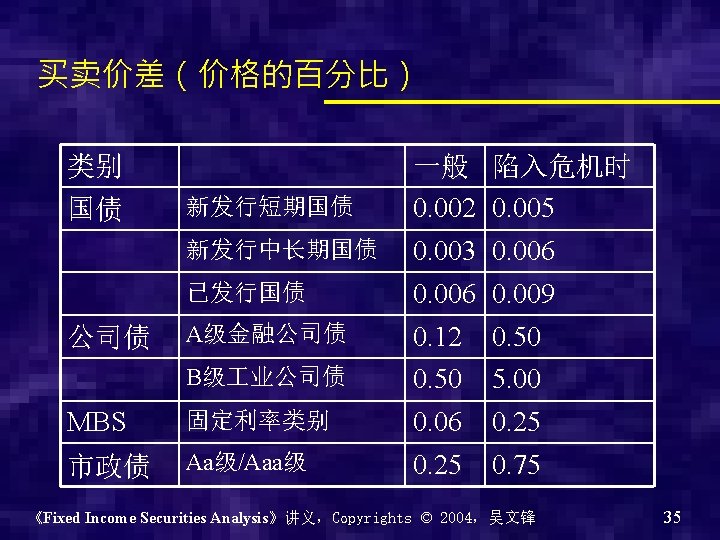

Liquidity Risk • Likelihood that an investor will be unable to sell security quickly and at a fair price • Estimated by using the bid-ask spread • Marking positions to market—liquidity risk is important even if instruments issues are held to maturity 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 34

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 36

Call and Prepayment Risk • Unpredictable cash flows • Reinvestment risk • Price compression 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 37

Prepayable Amortizing Securities • Reinvestment risk is compounded for lenders when borrowers prepay their principal obligations • If a borrower prepays, the investor gets their money back sooner than they expected in a low interest rates in a market • 银行对按揭贷款的提前还款是要罚款的 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 38

Price Volatility Risk • The greater the volatility of the underlying price, the greater the value of an embedded option • When expected yield volatility increases, the value of the call option increases and the value of the callable bond decreases • Value of callable = value of noncallable –value of embedded option 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 39

Exchange Rate Risk • The investor bears the risk of receiving an uncertain amount when these payments are converted into the home currency – If home currency appreciates against foreign currency of the bond payments, each foreign currency unit will be worth less – If home currency depreciates against foreign currency of the bond payments, each foreign currency unit will be worth more 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 40

Inflation Risk • Possibility that prices of goods and services will increase • Purchasing power goes down with fixed coupon bonds and increasing inflation • 投资者如何避免? 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 42

Event Risk • Disasters • Corporate takeovers and restructurings • Regulatory issues • Political risk 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 43

定价 现金流 贴现率 利率 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 47

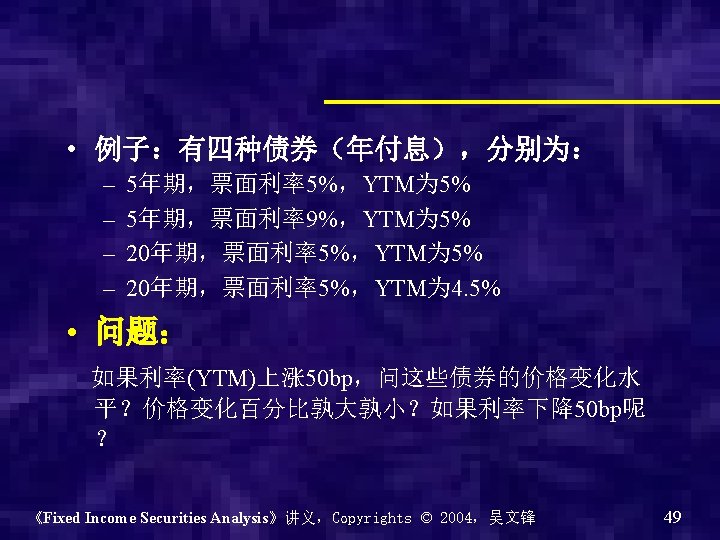

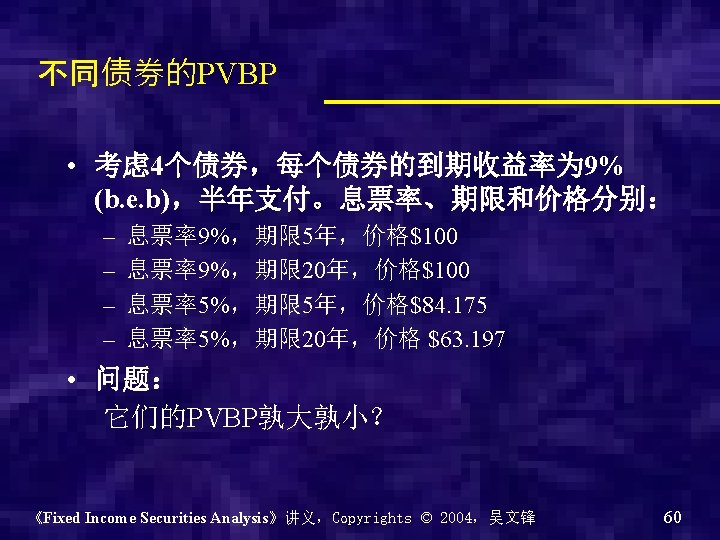

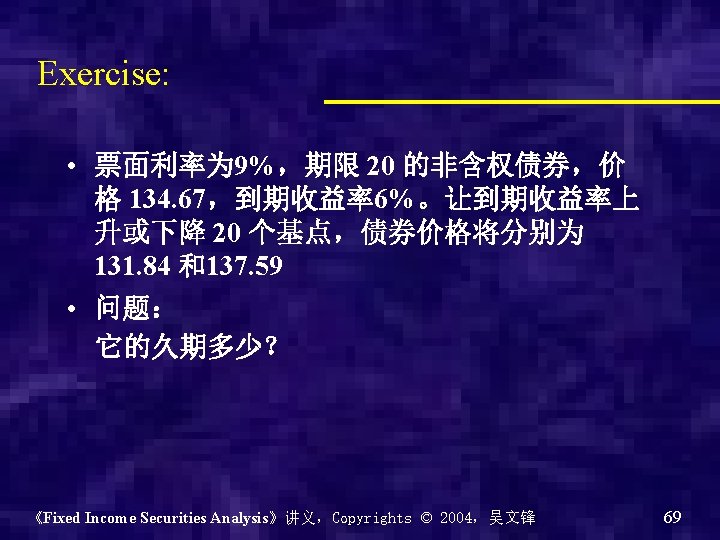

Price 1: 5年,息票率5% Price 2: 20年,息票率5% Price 3: 20年,息票率9% 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 50

Price 1: 5年,息票率5% Price 2: 20年,息票率5% Price 3: 20年,息票率9%,除以息票率为 5%的价格 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 51

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 54

new yld BP change 9%, 5 yr 9%, 20 yr 5%, 5 yr 5%, 20 yr 6 -300 12. 7953 34. 6722 11. 5603 25. 2458 8 -100 4. 0554 9. 8964 3. 6591 7. 114 8. 9 -10 -0. 3947 -0. 9135 -0. 3558 -0. 6523 9. 01 1 -0. 0396 -0. 0919 -0. 0357 -0. 0657 9. 5 50 -1. 9541 -4. 4408 -1. 7613 -3. 1636 10 100 -3. 8609 -8. 5795 -3. 4789 -6. 0945 12 300 -11. 0401 -22. 5694 -9. 9349 -15. 8589 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 61

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 62

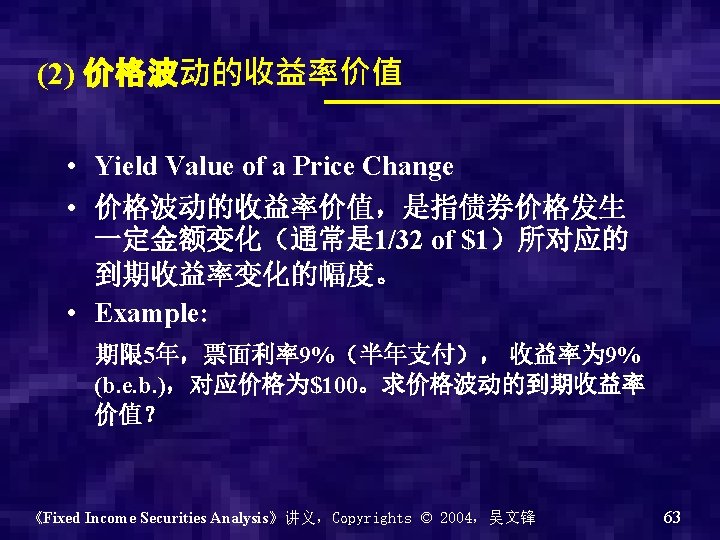

• 解答: 所以: 价格波动的收益率价值 = 9% - 8. 992% = 0. 008% 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 64

• 解答: 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 68

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 71

(2) 为什么叫 Duration? • 下表为零息券的久期 期限 1年 2年 3年 4年 5年 到期收益率 5% 5% 5% 久期 0. 952 1. 901 2. 856 3. 801 4. 763 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 75

久期的连续形式 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 76

其中:dt为t时刻的贴现因子,PVt为t时刻的现值。 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 77

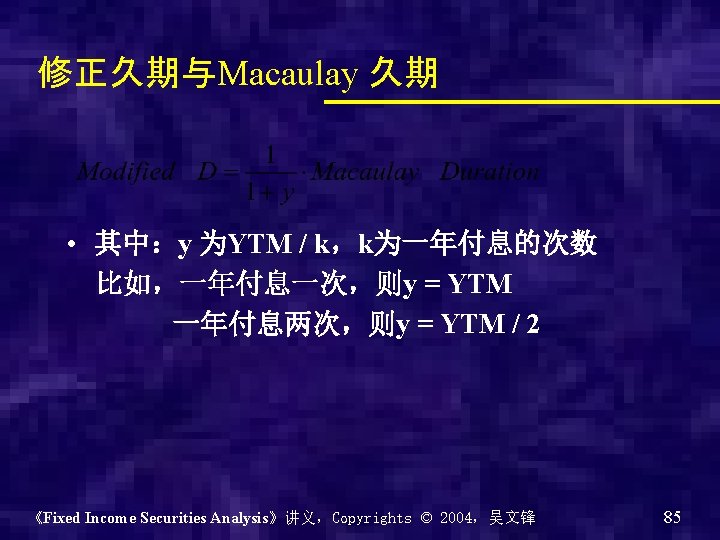

Macaulay 久期 • Macaulay 久期 (DM) 就是:期限的加权平均, 权重为现值。 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 78

term spot rate% df 1 8. 5056 0. 9216 2 8. 6753 0. 8467 3 8. 8377 0. 7756 4 8. 9927 0. 7086 5 9. 1404 0. 6458 6 9. 2807 0. 5871 7 9. 4136 0. 5327 8 9. 5391 0. 4824 9 9. 657 0. 4362 10 9. 7675 0. 3938 11 9. 8705 0. 3551 12 9. 9659 0. 3198 13 10. 0537 0. 2878 14 10. 134 0. 2589 15 10. 2067 0. 2327 16 10. 2718 0. 2092 17 10. 3292 0. 1880 18 10. 379 0. 1691 19 10. 4212 0. 1521 20 10. 4557 0. 1368 total PV 9. 2161 8. 4672 7. 7564 7. 0862 6. 4576 5. 8714 5. 3272 4. 8244 4. 3619 3. 9379 3. 5507 3. 1982 2. 8783 2. 5888 2. 3274 2. 0920 1. 8805 1. 6906 1. 5206 15. 0532 100. 0866 t*PV 9. 2161 16. 9343 23. 2693 28. 3446 32. 2881 35. 2282 37. 2906 38. 5955 39. 2568 39. 3788 39. 0572 38. 3782 37. 4182 36. 2433 34. 9117 33. 4725 31. 9677 30. 4310 28. 8906 301. 0648 911. 63 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 80

period cash flow 1 2 3 4 5 6 7 8 9 10 Total 3 3 3 3 3 103 discount factor PV 0. 9569 2. 871 0. 9157 2. 747 0. 8763 2. 629 0. 8386 2. 561 0. 8025 2. 407 0. 7679 2. 304 0. 7348 2. 204 0. 7032 2. 109 0. 6729 2. 019 0. 6439 66. 325 88. 131 t(PV) 2. 871 5. 494 7. 887 10. 063 12. 037 13. 822 15. 431 16. 876 18. 168 663. 246 765. 895 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 82

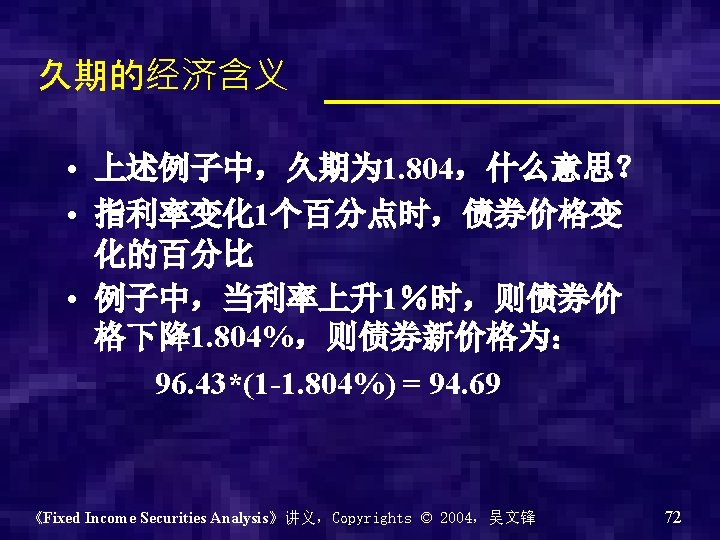

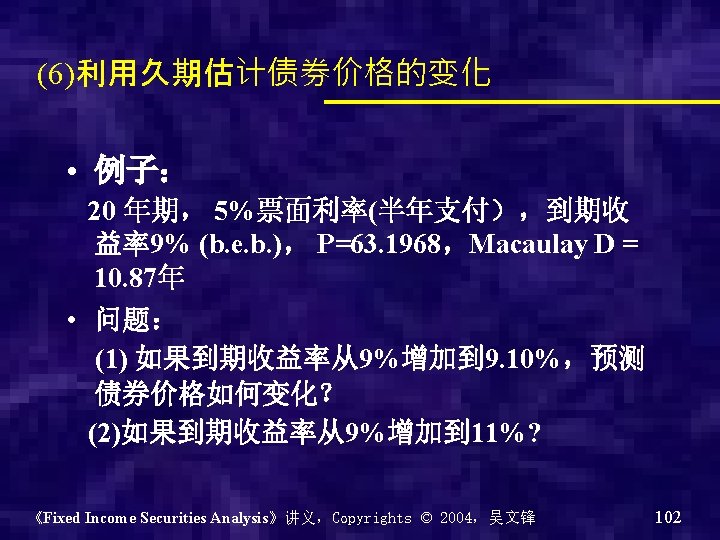

• 解答: (1) D = 10. 87/(1+0. 045) = 10. 40 价格变化: -10. 40(. 0010) = -1. 04% 实际变化: -1. 03% (2) 价格变化: -10. 40(. 020) = -20. 80% 实际变化: -17. 94% 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 103

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 105

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 108

凸性的计算 • 计算公式: 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 109

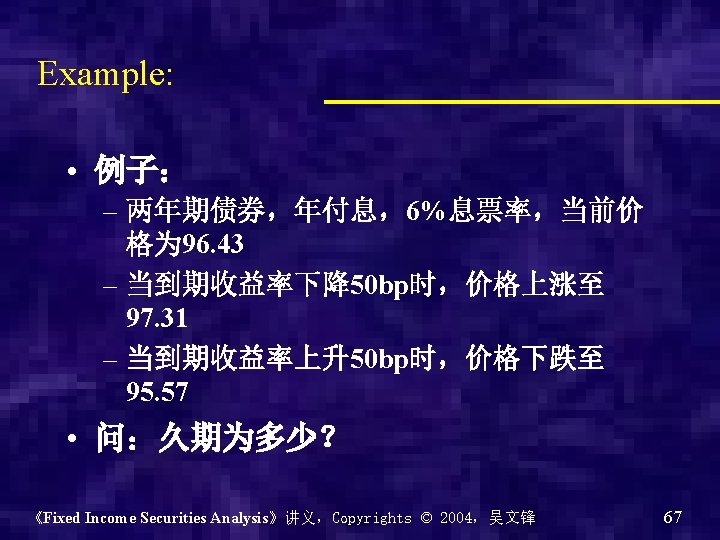

Example: • yield=6%, V 0 =134. 67, yield=6. 2%, V+ =131. 84, yield=5. 8%, V- =137. 59 • 则: 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 110

《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 112

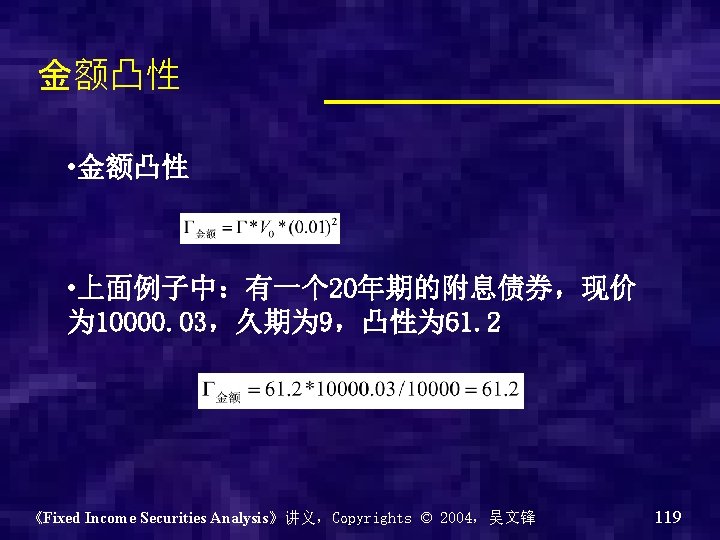

(2) 凸性的计算,也可以通过久期: 《Fixed Income Securities Analysis》讲义,Copyrights © 2004,吴文锋 115